Weekly Macro Note: War Resumes (Again), Hormuz Traffic Analysis, Why War Is Bullish, A Look at Asian Markets Part 3

In the Weekly Macro Note - we discuss (yet another) resumption of the war and why this time, the US is going to get more worried about a Hormuz reopening, talk Hormuz traffic, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge readers and community,

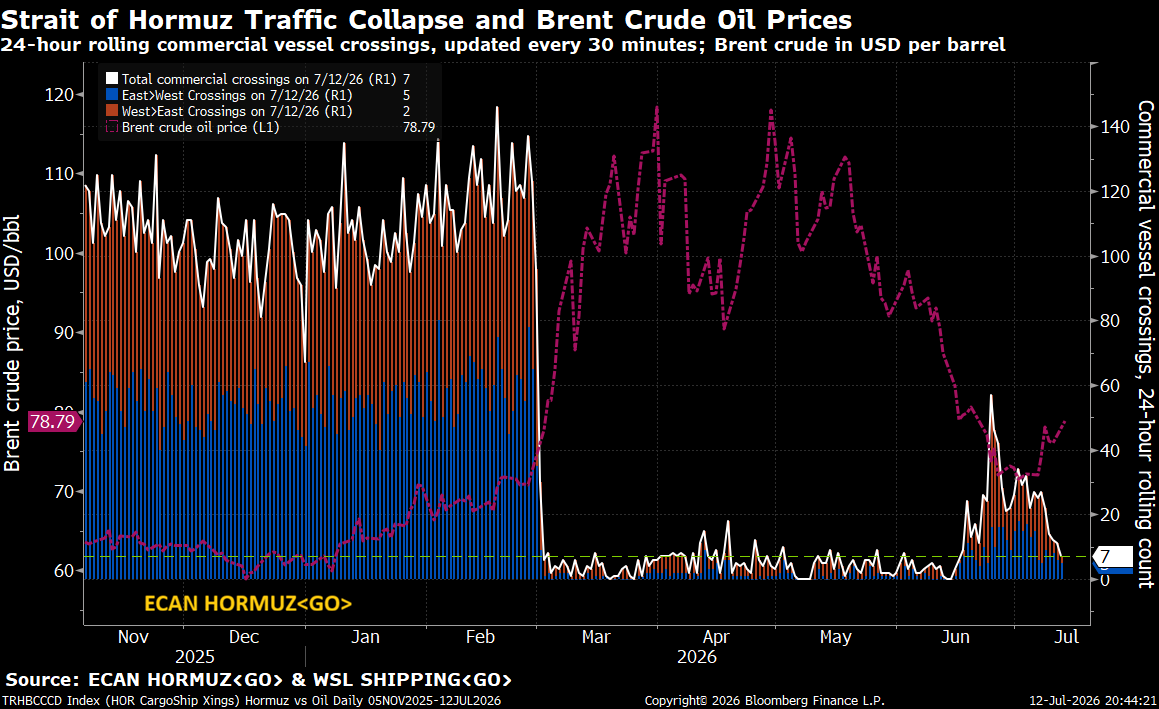

This evening we’re watching some escalation signals in the Iran-war - namely, as both sides battle over Hormuz control. Iran has exerted greater control over Hormuz in the last 48 hours (as we expected in the last Weekly Macro Note) because oil prices have gotten too low for them to be happy. Ideally, Iran wants Brent ~$85/bbl - and GCC nations also wouldn’t mind this - even though they won’t say it out loud. Some of the loudest energy bears on FinTwit have gotten extremely loud this weekend, expecting oil prices to do something like a pandemic waterfall - which makes absolutely no sense with demand as robust as it is - and countries continuing to run down their strategic petroleum inventories.

Trump will likely panic on a 5-7% up move on oil, and WTI is very close to reclaiming the 200-day to the upside; something is going to have to give with the Strait of Hormuz, because as I highlight in the section below, traffic is almost back to zero - and we’re in Mid-July now. This comes as the SPRs globally (ex-China) are at or near tank bottom levels. The resolution here is quite clear - they either escalate militarily to take Hormuz, or accept much higher WTI/Brent price levels once again - and I don’t think they want the latter, even though the former is inflationary. We’re basically at inflation^2 right now.

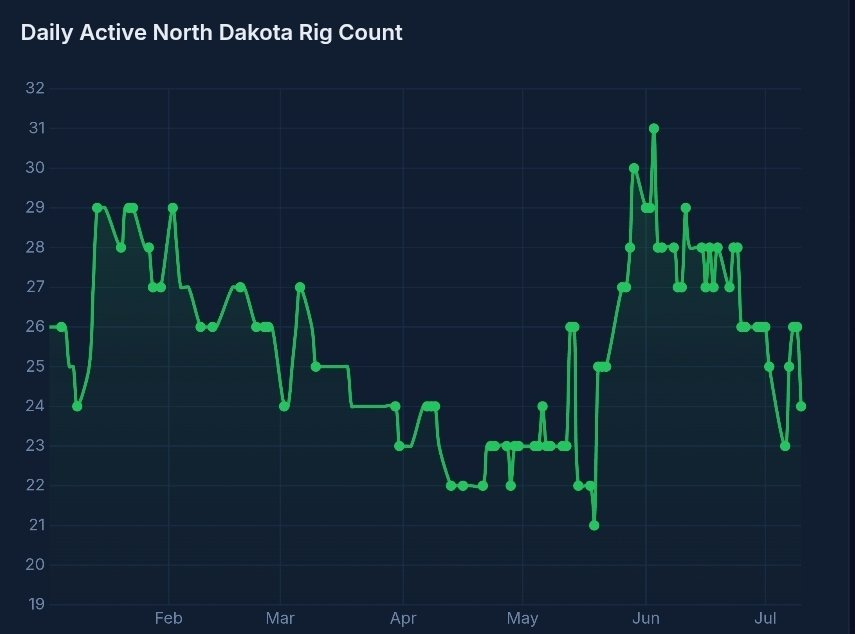

In markets this evening - the Nasdaq is off about a percentage point and leading lower - WTI/Brent are very close to pushing back above their 200 day moving averages - losses are leading in Asia with the KOSPI sidecar halted at one point. The regime that I continue to expect is a sideways one as long as we see war rage. If WTI >85 and Brent >90, then we will see significant downside pressures emerge as the Fed will seriously have to begin discussing a rate hike. I strongly dislike the obsession with these overnight Sunday moves - but I think what’s going on in Asia is going to drive the semiconductor and AI action here as those markets begin to violently wobble. The amount of gapping, halting, etc. being seen in South Korea is flashing potential Asian market crisis - and Japan is not far behind in their market dynamics. South Korea is just the worst - as highlighted frequently by our Global Bubble Index - due to the extreme utilization of leverage into hyper-concentrated areas within the semiconductor and technology trades. The sweet spot for WTI is going to continue to be in the $71-$81bbl range now for E&P companies, but we need to see actual stability for anyone to start rigging up. For the time being (as I highlighted with some North Dakota rig count data yesterday evening), it would be absolutely foolish to launch new drilling endeavors right now until we can establish a 3m/6m average price floor and get some confidence in where that demand/price equilibrium is.

MacroEdge in the news… MacroEdge employment data recommended for the Warsh Federal Reserve due to labor market data issues:

Not yet a MacroEdge Ozone subscriber? Upgrade below to get all of our research, data, portfolio strategy, and more.

Macro Week Ahead

This week is fairly busy with macro data - focusing primarily on (already) outdated inflation data - which we should not overweight. The Fed will use the incoming data for the July rate cut decision - and as we’ve seen in the latest Japanese inflation data - inflation is shaping up to be more embedded than policymakers thought with just the energy shock issue. While WTI at $75/bbl really has no inflation problem potential - all of the other inputs are still way up Y/Y - and its price levels continue to rise in nominal terms.

Monday: No data

Tuesday: CPI (US), Warsh rate hike signals

Wednesday: PPI, Warsh testimony day 2

Thursday: June retail sales

Friday: Housing starts & building permits

For earnings >500bn market cap:

JP Morgan Chase

United Health

Taiwan Semiconductor

There are other sizable names reporting as well, but keeping it simple for the sake of our filter. SK Hynix will also begin trading tomorrow.

War Resumes (Again)

U.S. Launches More Strikes on Iran: U.S. Central Command (CENTCOM) conducted multiple rounds of retaliatory strikes targeting Iranian missile sites, air defense systems, and paramilitary Revolutionary Guard boats to degrade their ability to disrupt international commercial shipping.

Iran Retaliates Across the Persian Gulf: Following the U.S. strikes, Iran launched an array of drones and missiles, hitting U.S. facilities in Bahrain, Kuwait, Qatar, Jordan, and Oman, and threatening to completely collapse ongoing interim ceasefire negotiations.

IDF Strikes Hamas Arms Facility: The Israeli Defense Forces bombed a temporary weapons production facility in Gaza City, claiming Hamas operatives were utilizing the site to aggressively restore their capabilities in violation of existing agreements.

Ukraine Strikes Russian Energy Infrastructure: Ukrainian forces heavily damaged the Syzran Oil Refinery in Samara Oblast—roughly 800 kilometers from the frontline—triggering severe explosions and a massive fire amid an intensified long-range campaign targeting Russian fuel networks.

Russian Advances in Donetsk: Intense fighting continues on the ground as Russian forces secured a solid foothold in eastern Kostyantynivka, advancing north of the city’s railway station and battling deep into the urban center.

Hormuz Traffic Analysis

Strait traffic is once again closer to zero than any sort of normalized level - and the oil bears have gotten really cocky about flows over the weekend and the US’ ability to maintain flows at any sustainable level:

Continued below: Hormuz traffic analysis, Why War Can Be (or is) Bullish, A Look at Asian Markets Pt. 3, A Chart to Make One Think - John