Weekly Macro Note: The War Goes On, Food and Fertilizer Price Impacts, Technical Trainwreck

In this Weekly Macro Note - we discuss the latest Middle East war developments, highlight food & fertilizer price impacts from the Strait of Hormuz closure, highlight portfolio strategy updates & more

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

It’s officially day 15 of the conflict between Israel and Iran - and there are few signs right now of the conflict abating over the next week. While Trump is calling on China to stop the Strait closure, it appears that we’ve currently bit off more than we can chew from an energy price standpoint. While domestic production in the US allows domestic consumers to avoid things like shortages, because oil is a global market, eventually these prices become too high to bear. One of the most clear outcomes from the last month is the immediate pricing out of cuts through the summer. While we strongly questioned the need for rate cuts as they were deployed over the last six months, it’s not out of the question to start seeing the curve price in the ‘other’ outcome as a possibility later in the year.

In the futures open, oil is up slightly with CL at about $100, spot WTI is also trading about $100 - physical barrels are trading significantly higher at around $150/bbl in the Middle East. This week is going to be key in seeing where we’ll trend directionally for WTI - and sideways action would actually be a fairly positive development for bulls after the doubling in price from January. Natural gas and gasoline prices are also higher, along with diesel, and NQ is up about 0.3% - all of the moves are very quiet. The broader indices themselves are approaching six months of sideways price action, which is much more important than focusing on these daily whipsaw moves up and down a few points. Bitcoin is up about 72.5K and has rebounded a tad off of the local lows from the impulsive wave lower. The Yen pair is at about 160.

Geopolitical volatility and oil prices will continue to drive market action this week, so that will continue to be the bulk of my focus until anything in the current market regime changes. Energy equities are going to benefit tremendously from the WTI > 80bbl environment, though above $100/bbl really seemed to have the political apparatus squirming today. Expect that they lob out more headlines and press releases this week about new plans to combat a potential energy price shock.

With that being said, let’s dive in.

Not a MacroEdge Ozone Subscriber? Try MacroEdge Ozone for one week & experience all of our data, portfolio strategy, equity research, commentary, and much more below:

MacroEdge is at the forefront of cutting-edge economic advisory services. Get in touch with our team today and schedule a conversation about how we can put you in the driver’s seat for today’s rapidly changing macro landscape:

A Taste of Trident*

Building on the cutting-edge macro research, equity research, and portfolio strategy we deliver at MacroEdge, we are opening the doors to register interest in the Trident I Global Macro Fund. This boutique vehicle is engineered to capture high absolute returns by identifying structural inflection points across global FX, rates, commodities, and equities. Modeled after unconstrained mandates, the Fund moves beyond traditional benchmarks to capitalize on mispriced macro fundamentals through a disciplined, thematic process. For accredited partners looking to move from analysis to execution, Trident offers a focused path into high-conviction global themes with a rigorous emphasis on downside control and liquidity.

Complete the form below to get in touch with our team & learn more about how we’re turning real-time data into real-time strategy:

Macro Week Ahead

Monday: Empire State Mfg Index

Tuesday: n/a

Wednesday: PPI, FOMC Decision

Thursday: BoJ Rate Decision, Industrial Production, Philly Fed Mfg Index

Friday: Japan Real Exports & Imports

Notable earnings reports this week:

Micron

Accenture

FedEx

Food and Fertilizer Price Impacts

Food and fertilizer price impacts are already occurring from the Strait of Hormuz closure and fuel price increase.

Looking at DBA, which measures ag firms, the index is approaching its all-time high set earlier in the year.

Gulf Urea prices (fertilizer futures) are also starting to accelerate:

There will supposedly be an announcement from the Administration on a step they’re taking to combat a surge in fertilizer prices. Technically, the downtrend was blown through, and with some resistance above, fertilizer prices will directionally depend now on how the Middle East situation evolves.

Wheat futures (and corn, so on and so forth) are all moving higher:

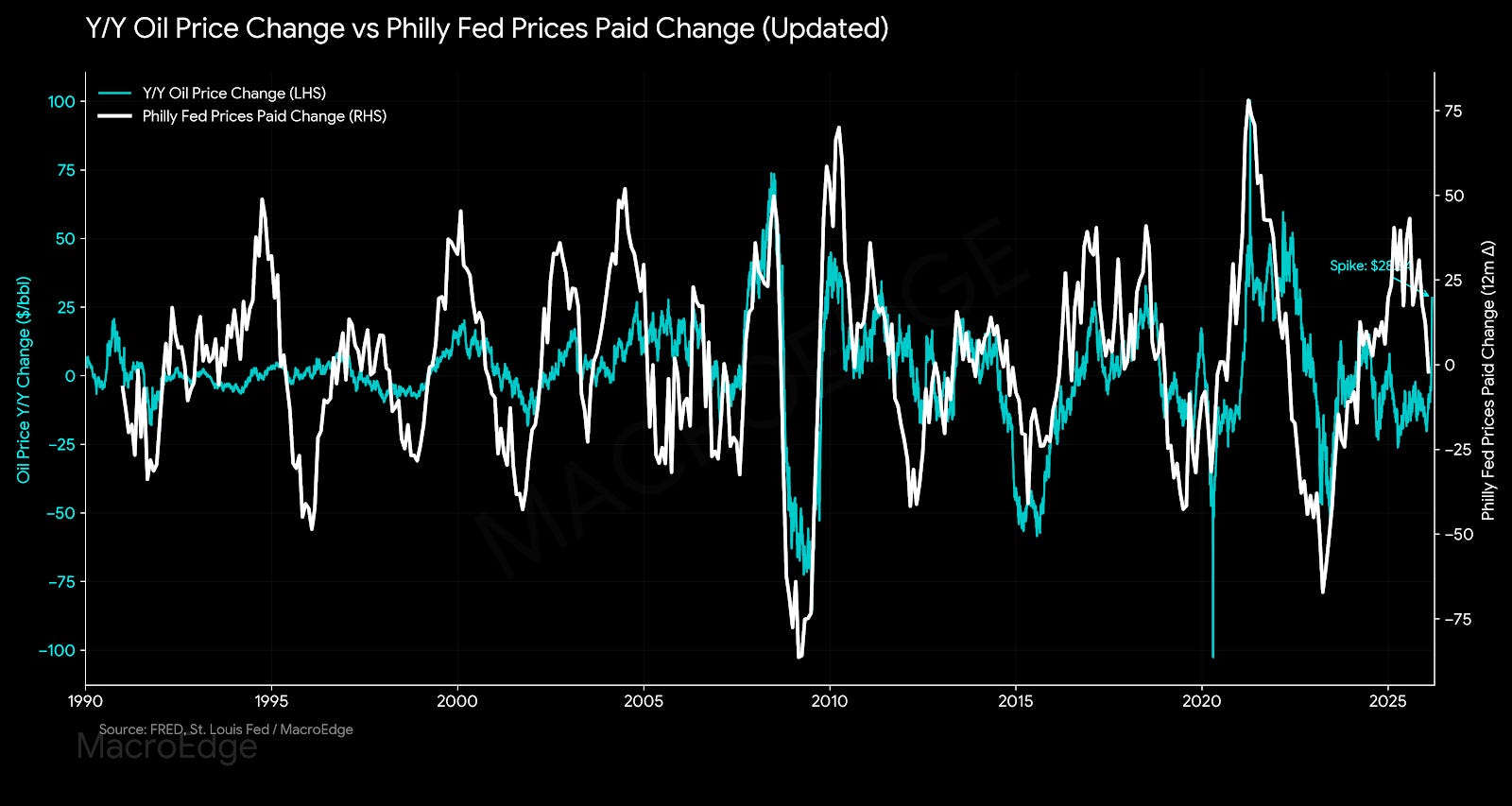

Oil & Prices Paid Relationship

Oil and prices paid (which are directly represented through PPI, and particularly PPI - commodities) are a critically important relationship. Right now, given the huge oil move of the last two months, they are starting to diverge (at one of their largest levels we’ve seen) - and one usually catches the other:

If this move in energy prices sustains, we will likely see this begin to feed into prices in the April data, especially in businesses with significant supply chain costs - costs are going to start rising across the board - and even though the end result may be demand destruction, higher oil and input costs mean more expensive everything else.

Additional Energy Equity Research, Strategy Update

Not yet a MacroEdge Ozone subscriber? Stay ahead of the rest and join us to access all of our data, research, & much more. Try for 7 days and stay for a lifetime.

On Wednesday, I will have the latest update on our energy portfolio strategy with an update - and highlight two additional names that warrant attention in looking at the oil and gas basket. I want to see how oil & gas equities perform in the first half of the week to get a better picture of how they’re going to behave in this dramatically improved price environment. My focus continues to be on unhedged, maximum-torque opportunities that will be repriced in this WTI > $80 environment. Some producers, drillers, and equipment service providers are still being priced like we’re in a $50 WTI environment - and obviously in a $100 environment things look world’s different from a fundamental standpoint at so many of these operators.

Geopolitical Update

There have not been any major developments or changes geopolitically since the note yesterday. We are seeing the Administration mention the Strait more frequently - and they are clearly not happy about the energy price spike that has materialized over the past few weeks.

The Kurdistan Regional Government (KRG) in Iraq confirmed that exports offline are currently sitting around 300Kbpd - and the numbers continue to add up across the region. Global leaders are playing a game of commodity ‘Russian Roulette’ and things are going to get significantly worse from a price shock standpoint if the current dynamics and supply outage persist for another two weeks.

The Technical Trainwreck

The indices continue a brutal sideways churn and have faked many out over the past few months. I expect that we will see the Administration take steps to try and push things higher this week, though the FOMC meeting on Wednesday will give us solid direction on where things are headed on the FFR-front. Right now, we’re back at less than one full cut being priced for this year, though in the game of whiplash, this likely swings at some point if cool data starts to roll back in. A combination of the 73/08 scenario is what the Fed fears most, and we’re going to dive into some of both this week - and talk more about private credit tomorrow.

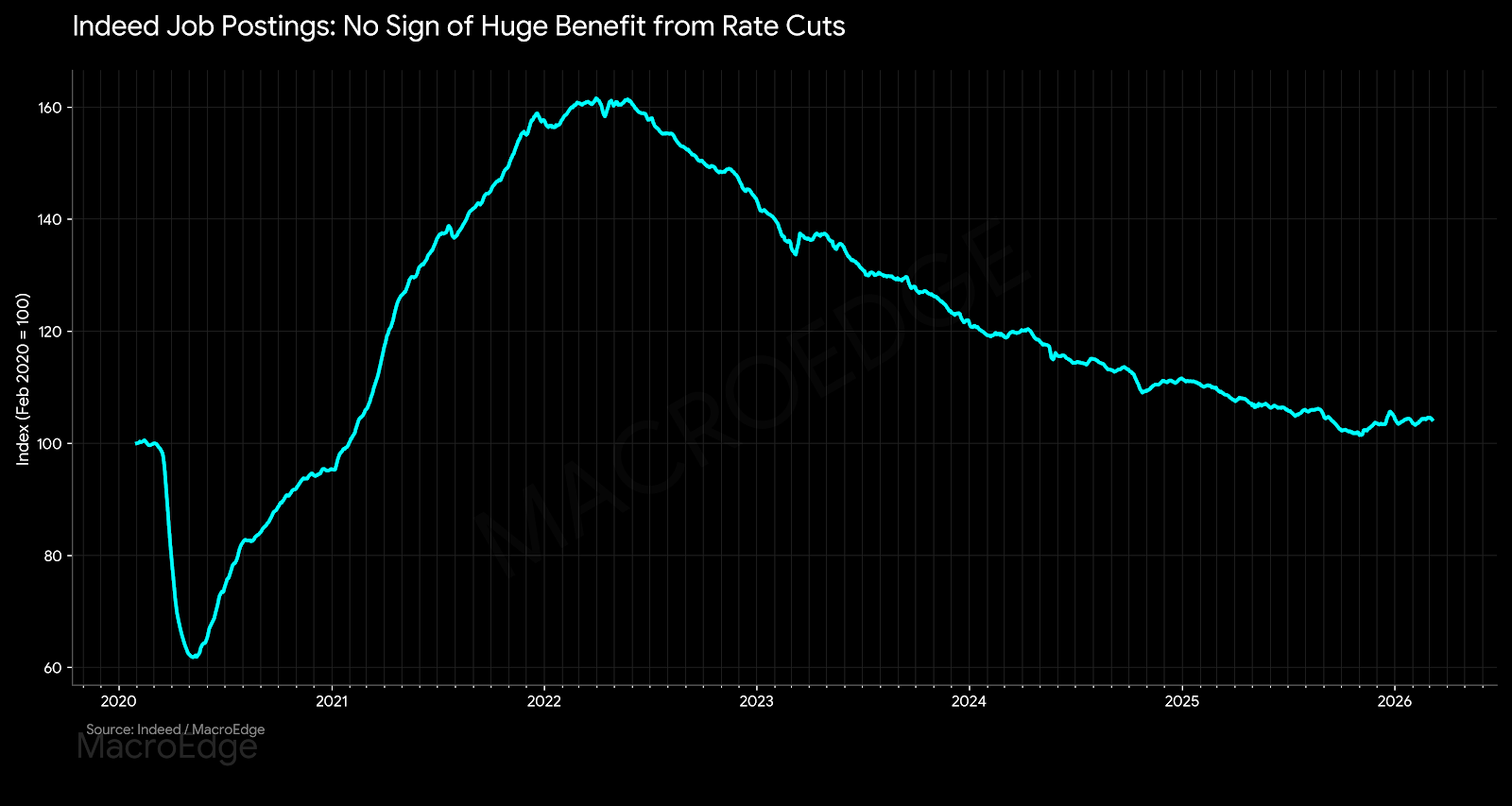

The Latest 30,000-Foot Employment Signals

After all of the rate cuts, there is still not any sort of broad signal that we’re seeing an improvement in labor market conditions. We’re in a bizarre environment of extremely low hiring & we’re sort of at a ‘labor force ceiling’ which is why I expect the Administration to start seeking out new job creation through legal migration or other similar means.

Without any improvement in these real-time signals, it’s hard to say that the rate cuts to this point have really done much other than bounce job openings very slightly. I also expect that the recent spike in mortgage rates will temper activity - so cyclical activity once again remains suppressed by the long end doing the job of the Fed, at least to a degree.

Report Schedule this Week:

Monday: War Note, Private Credit, & FOMC Preview

Wednesday: FOMC Recap & Energy Strategy Update

Friday: Redeye Macro Note (released Saturday morning)

Saturday: Saturday Geopolitical Note

Sunday: Weekly Macro Note

Have a great start to your week and MacroEdge on.

Don

MacroEdge Portfolio Strategy Update - March 15, 2026 (@SixFinance, Head of Research)

Opening Trade: Long Wheat /ZW

While energy prices command headlines, agricultural commodities are being hit by a dual shock. Roughly a fifth of the world’s oil supply moves through the Strait of Hormuz, but roughly a third of global seaborne fertilizer transits the Strait.

Urea fertilizer, the most commonly used fertilizer for wheat, is already responding to the supply shock. According to the USDA, fertilizer is 34-45% of wheat operating costs.

Energy accounts for roughly 70% of nitrogen fertilizer production costs (per Fitch), and fertilizer capacity is already beginning to come offline. In addition to a supply shock that, on a relative basis, is larger than the oil shock, the primary input costs to wheat production are now rising.

China is the largest producer of nitrogen fertilizer at roughly 26% of global output, followed by India at ~14%, then the U.S., Russia, and the Gulf states. But production and exports are very different stories. China has indicated no urea exports until August 2026, so that capacity is essentially domestic-only. The Gulf states (Saudi Arabia, Qatar, UAE, Oman, and Iran) punch way above their weight on the export side. They are responsible for nearly half of the globally traded urea and a huge share of traded ammonia, all of which transits Hormuz. Russia is a major exporter too but faces its own sanctions complications. What the Gulf dominates is the tradeable surplus that the rest of the world depends on, and that’s what’s currently locked behind the strait.

Gulf-produced fertilizer cannot reach export markets. Even the limited selective reopening for non Western ships doesn’t move the needle.

“Because fertilizer has less value than oil and gas, political and business leaders expend fewer resources to make sure it keeps flowing. A ship captain bold enough to brave drone strikes and dash through the Strait of Hormuz would prefer to carry oil rather than fertilizer, a preference that would be shared by any potential navy escort, which the United States is, in any case, not yet able to provide. G7 countries don’t maintain strategic fertilizer reserves to match their oil stockpiles. The pipeline that Saudi Arabia built to enable exports through the Red Sea rather than the Strait of Hormuz is for oil, not ammonia products.” - Carnegie Endowment for International Peace.

Making matters worse, beyond China’s export restriction, European nitrogen production has been running at about three-fourths of capacity since the 2022 Russia-Ukraine gas shock. The global nitrogen market was already tight before a single bomb dropped on Iran. Crude oil drives diesel and fertilizer production costs, fertilizer drives per-acre crop costs, and that reprices grain futures, especially during planting season when application decisions are being made in real time.

Fund positioning is another major amplifier to price action. In wheat specifically, managed money has flipped from near record short to net long in less than two weeks. StoneX estimates funds bought 31,000 SRW futures contracts in just two sessions. In HRW wheat, funds went long for the first time since August 2023.

Wheat is a bellwether crop in the agricultural commodity space here for several reasons. Not because it’s the most fertilizer-intensive crop(that would be corn), but because it sits at the intersection of multiple price drivers. Energy cost pass-through, fertilizer input costs, speculative repositioning, Plains weather risk, and a record cold front in January are headwinds to crop yields.

Why is wheat above the others in the agricultural commodity complex?

Winter wheat is already in the ground. You can’t shift acreage like you can with a corn-to-soybeans pivot. The only decision to be made now is nitrogen topdressing application rates. If urea costs too much, yields take a direct hit.

The Middle East and North Africa consumer over 200lbs of wheat per capita annually. Egypt is one of the world’s largest importers. Surging wheat prices were a direct contribution to the Arab Spring. When food security stockpiling begins in net-importer countries, wheat is at the top of the buy list.

While wheat prices have repriced modestly higher, the effects on the spring planting season are largely not priced in. The timing here is the crucial factor. Should this disruption persist for several more weeks, when fertilizer application decisions are irreversible, this is about as bad as it gets for transmission into actual crop yields. A disruption of this magnitude in August or November would matter far less for agriculture specifically.

Then the real factor on timing, and here is where I will speculate rather wildly, is the Trump-Xi summit in China at the end of March. While this is by no means a core tenet of my thesis, Trump’s operation against a China ally right before their summit that has been long-awaited by markets over the last year adds another layer of complexity to the timeline. If Trump demonstrates to the entire world that the markets are the one place you can hit America to end any conflict, and even Iran can bring the US to its’ knees by targeting oil prices, it risks a show of enormous weakness into the summit meeting, and shines the largest spotlight imaginable on the United States of America’s achilles heel.

I am long 33% of NAV notional in /ZW May futures, with the mental model that the longer this goes on, higher wheat prices become more of a sure thing with every passing day.

*Important Disclosure: This post is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any interests in Trident I Global Macro Fund, LP. Any such offering will be made only by the Private Placement Memorandum (PPM) and Subscription Agreement. Rule 506(c) offerings are limited to Accredited Investors only. Investing in private funds involves high risk and is not suitable for all investors.

For more details, please refer to our Terms and Conditions.