Weekly Macro Note: The Global Bubble, Macro Week Ahead, Government Shutdown Odds, Technicals, Crypto Signals, & More

In this Weekly Macro Note - we dive into the global bubble phenomenon - from Spain, to Germany, Canada, and more, talk about the continued rise in metals, crypto signals, the week ahead, and more.

(@DonMiami3, MacroEdge Chief Economist)

Good Sunday evening MacroEdge Readers and Community,

It hasn’t been long since we last connected for the Redeye Macro Note that was released very early this morning - but in this Weekly Macro Note - we’re going to look into the global trends - including with the AI bubble thematic we’ve discussed for the last several reports, look at the week ahead for macro data, government shutdown odds, crypto signals and more.

Under the macro shifts of today, towards a more federally controlled equity market & economy for megacaps - we’ve continued to see that bid hold up for the time being. The scenario over the long run is completely unsustainable, and we’ve reached the territory where it doesn’t take much going wrong for things to spiral the wrong way and force another intervention. Politicians and fiscal policymakers continue to sit on their hands while things continue to worsen with things like the small business insurance crisis mounting, cost of living pushes the birthrate lower, and we shift into the ‘South African’ economic patterns I’ve so frequently mentioned over the last few years. Bubbles are exciting for those playing with them (and especially profiting from them) but it’s usually the hangover that leaves us wondering what went wrong… While we appear to have a ways to go for that scenario in things like data centers, it’s more & more valid by the day to wonder how far they’re willing to push things… Thus, the safe havens like gold and silver will continue to call the fiscal bluff of even knowing what they’re doing. Let’s get rolling.

Starting off this Macro Note with yet another all-time high for gold futures. Funny enough, I found a photo on my camera roll of a physical purchase I made back in early July 2019, not too disappointed there.

Positioning for More: Two Portfolio Strategies Arriving with MacroEdge Institutional Research

As we prepare the gradual rollout of MacroEdge Institutional Research over the month October - we’ll be introducing our two flagship portfolio strategies, the MacroEdge Institutional Research Portfolio (MIRP) - led by @SixFinance, and the Global Macro Strategy Portfolio (GMSP) led by myself.

MIRP is an absolute return-seeking index, focused on asymmetry with a global macro focus. Not benchmarked against the S&P.

GMSP is a commodity, event-driven, and volatility-focused index, with an emphasis on left-tail and black swan events.

Within Institutional Research, clients will get access to real-time portfolio updates, notes, adjustments, and monthly performance reviews as it pertains to both portfolio strategies.

In addition to that, Institutional Research includes:

Full MacroEdge Research Dashboard: 50+ interactive charts, live data updates, and analytics to monitor global macro, labor, real estate, and market volatility in real time.

Portfolio Strategy & Alerts: Actionable trade ideas, asymmetric opportunities, and risk-hedge adjustments delivered directly to client portfolios with timely alerts.

Monthly Institutional Research Report: Deep-dive thematic analysis, inter-month macro notes, and coverage of global/domestic market shifts. Access to all Ozone Macro Notes, and portfolio strategy updates in real-time.

Direct Access to the MacroEdge Team: Quarterly IR strategy calls, scenario modeling, and proactive intelligence.

To access MacroEdge Institutional Research for a month - starting 10/1 - submit the form via the button below to get on the list. A team member will be in touch on 10/1 with the link for access, and to activate your profile:

Macro Week Ahead

Monday, Sept 29

Japan:

• BoJ Summary of Opinions

• Industrial Production (prel Aug)

• Retail Sales (Aug)US:

• Pending Home Sales (Aug)

• Dallas Fed Manufacturing Index (Sep)

• Fed speakers: Waller, Hammack, Musalem, Williams, Bostic

Tuesday, Sept 30

Japan:

• Tankan Survey (Q3) – Large Manufacturers, Non-Manufacturing, Capex Outlook

• S&P Global Manufacturing PMI (final Sep)US:

• JOLTs Job Openings (Aug)

• CB Consumer Confidence (Sep)

• Fed speaker: Goolsbee

Wednesday, Oct 1

Japan:

• 10-Year JGB Auction

• Foreign Bond/Stock Investment flowsUS:

• ADP Employment Change (Sep)

• ISM Manufacturing PMI (Sep)

• Construction Spending (Aug)

• EIA Weekly Energy Inventories

Thursday, Oct 2

Japan:

• Unemployment Rate (Aug)

• Job-to-Applicant Ratio (Aug)

• Services & Composite PMIs (final Sep)

• BoJ Gov Ueda SpeechUS:

• Initial Jobless Claims (Sep 27)

• Challenger Job Cuts (Sep)

• Factory Orders (Aug)

• Fed Balance Sheet

Friday, Oct 3

US:

• Non-Farm Payrolls (Sep)

• Unemployment Rate (Sep)

• Average Hourly Earnings (Sep)

• Participation Rate (Sep)

• ISM Services PMI (Sep)

Government Shutdown Odds

Trump is meeting with Congressional leaders to attempt to avert a government shutdown before the 10/1 funding lapse begins, he’s playing hardball as it pertains to mass layoffs, and using that as a tool to keep the government operating. Schumer & the Dems have somewhat of an upper hand on optics, especially with midterms a little over a year away now.

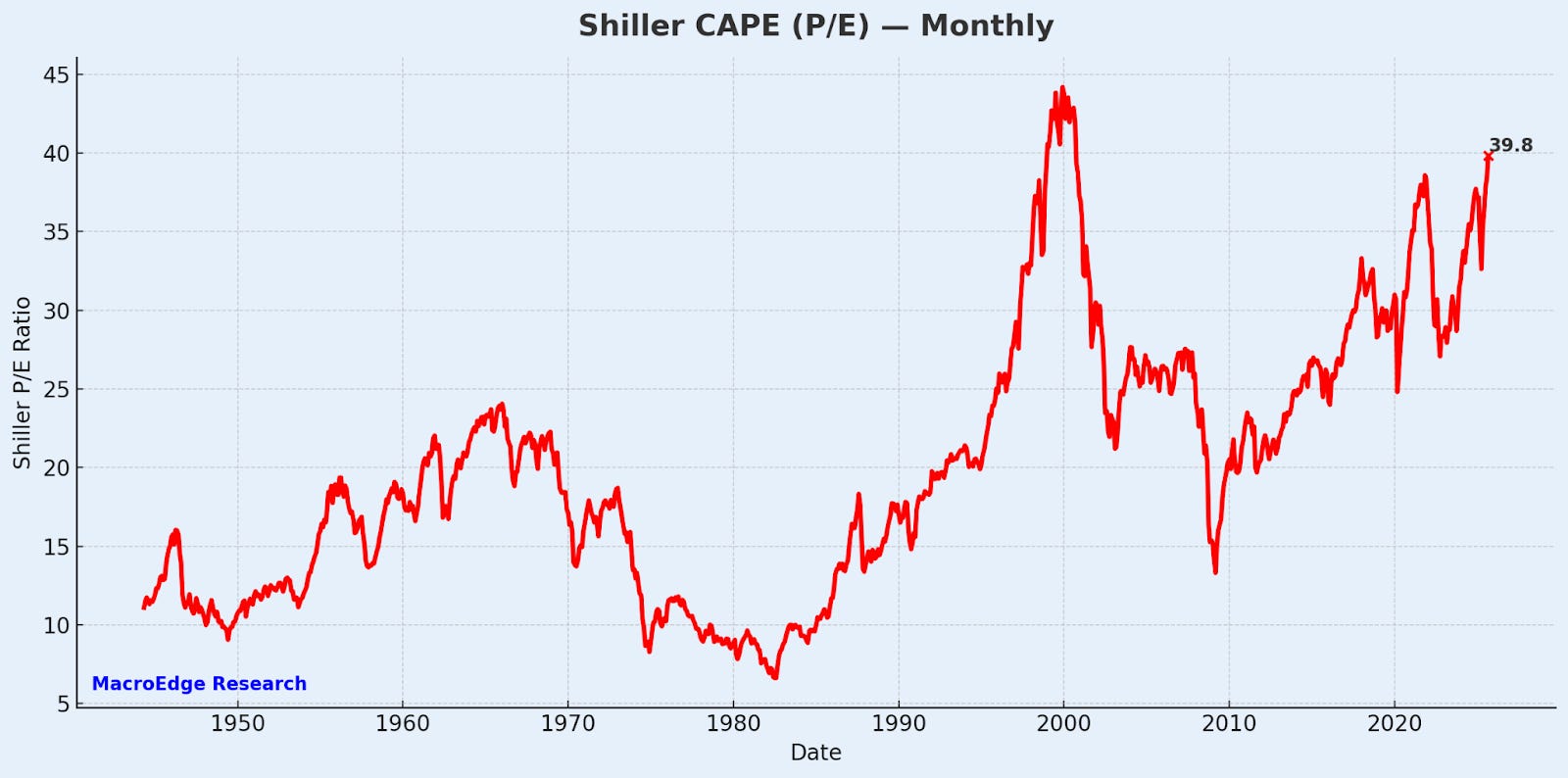

AI Bubble – Making 2000 Look Tame

Multiple expansion has pushed CAPE & other valuation metrics near record highs, but this beast still has some teeth left for higher…

Valuations are not timing instruments, and we don’t yet have a solidly defined technical risk/reward ratio.

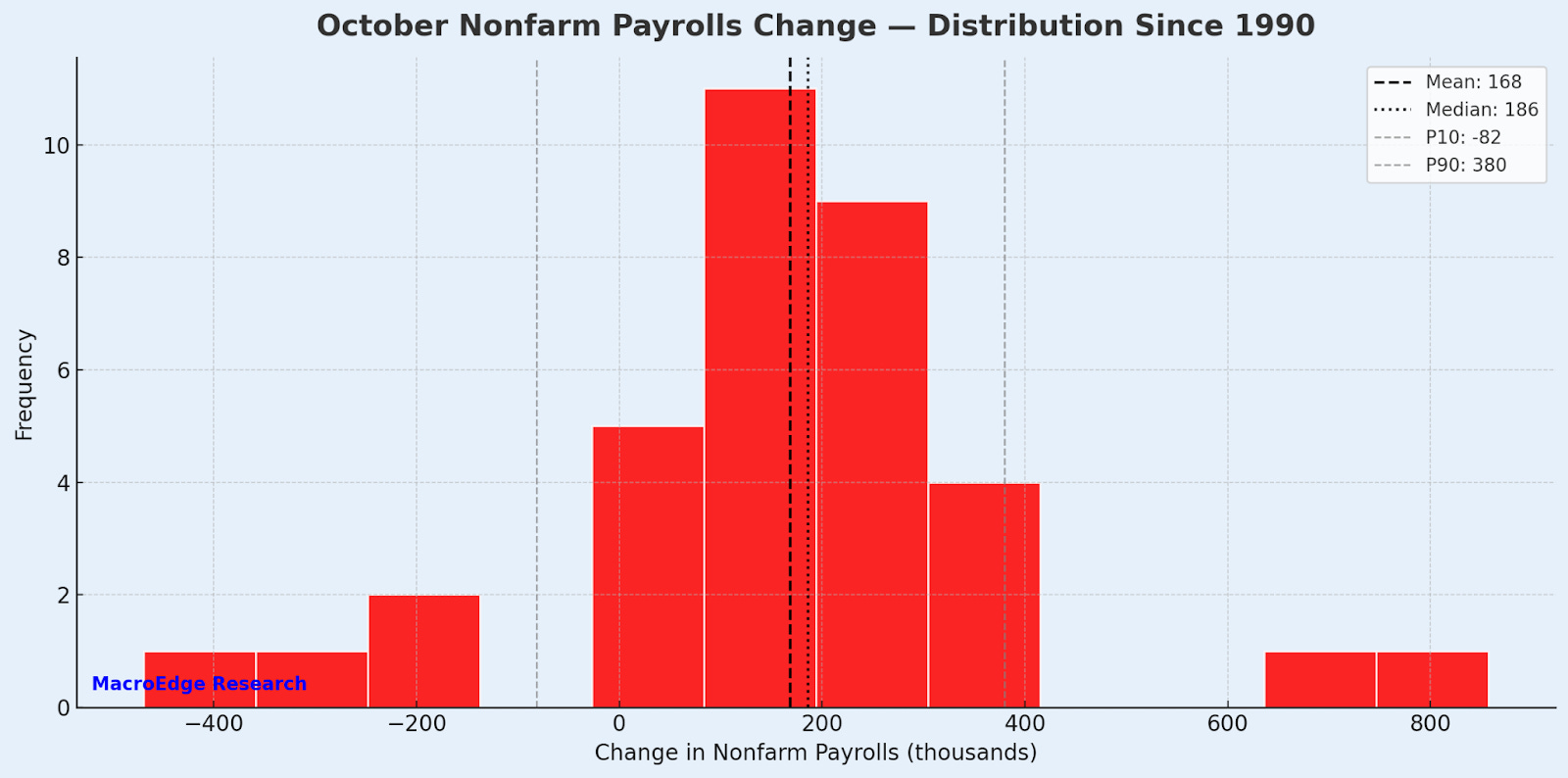

Employment Data Week, Again

We’ve got another employment data release this week - and the Fed has been concerned about the cooling labor market. With residential construction employment near the place of no return, without a restart to population tailwinds or housing demand (note that the problem with residential real estate is prices, not rates), the question now presents itself whether the Fed can stave off further deterioration in employment given where we’re at in the cycle. Employment data lags both ways, but for ‘swan’ events this week - don’t rule out the potential for a delayed employment data release if the government shuts down. While not under the non-critical functions, typically not impacted by a shutdown, Trump has threatened mass layoffs if the government shuts down… They may use this, if the report is directionally skewed against what they want, to push back the report.

October nonfarm distribution:

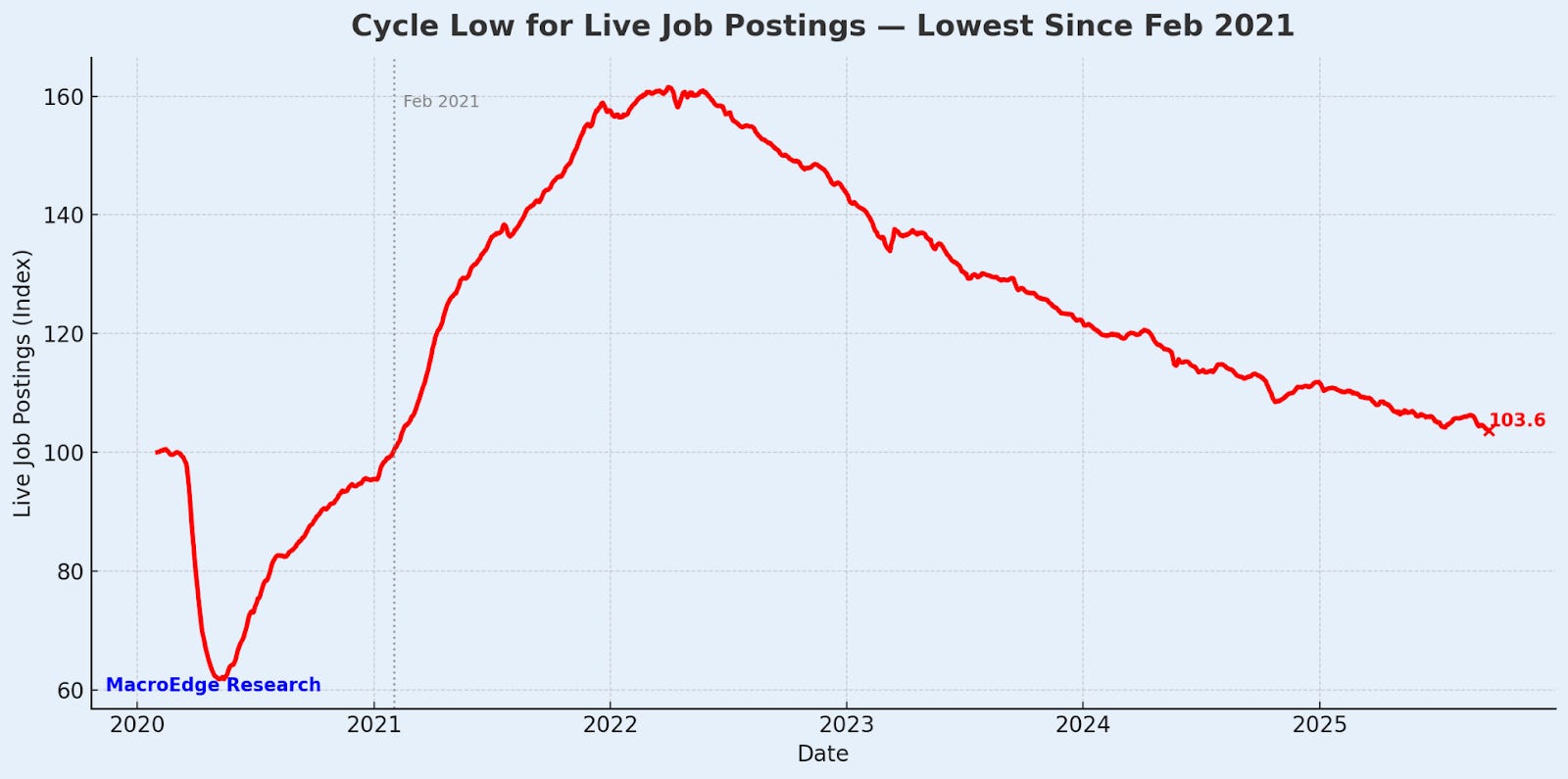

Job postings continue to fall, per Indeed live data:

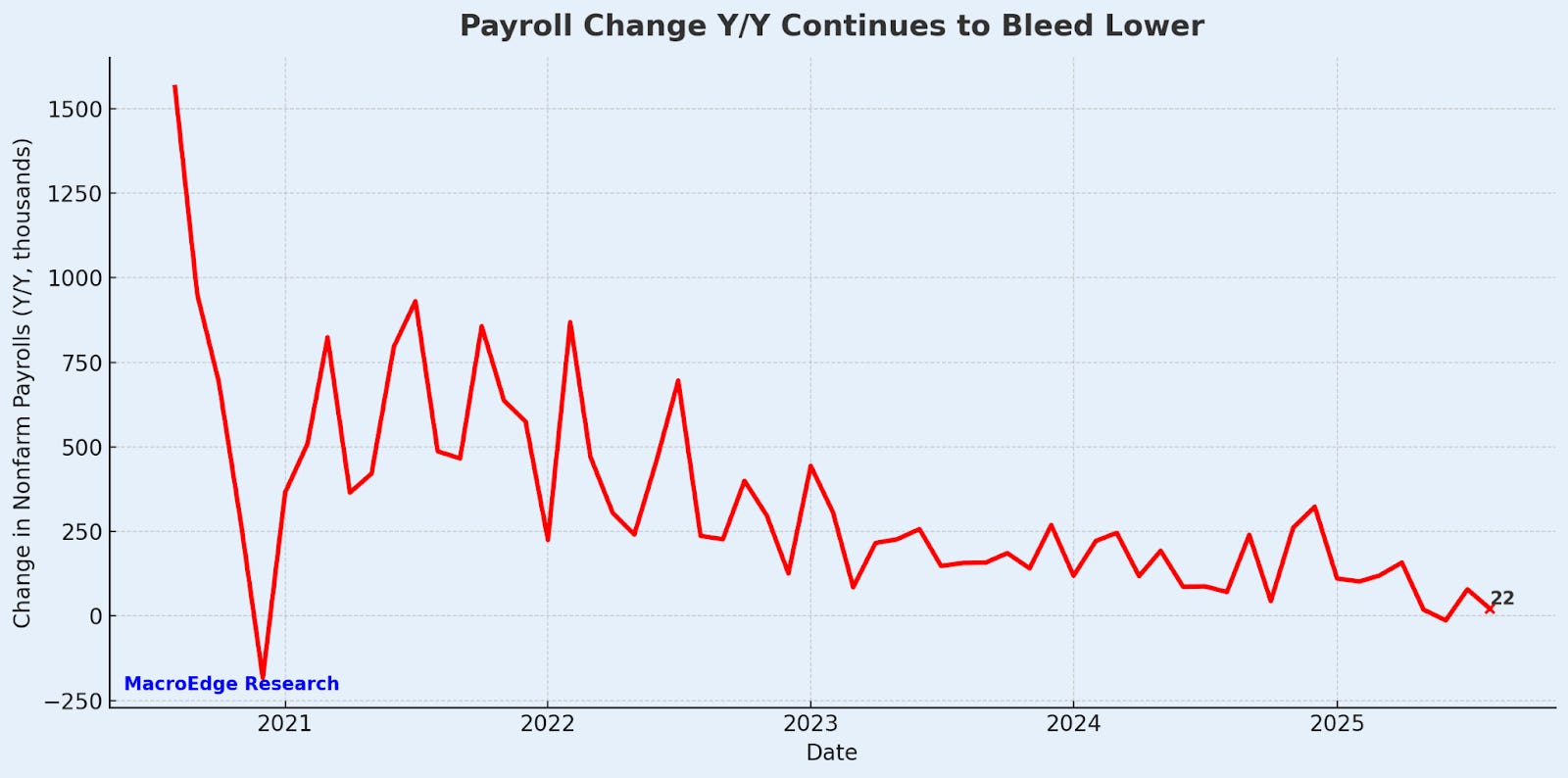

Payroll growth continues to meaningfully slow…

Cyclicals remain the story… or if we go full ‘China’ on the data front, that’ll matter too.

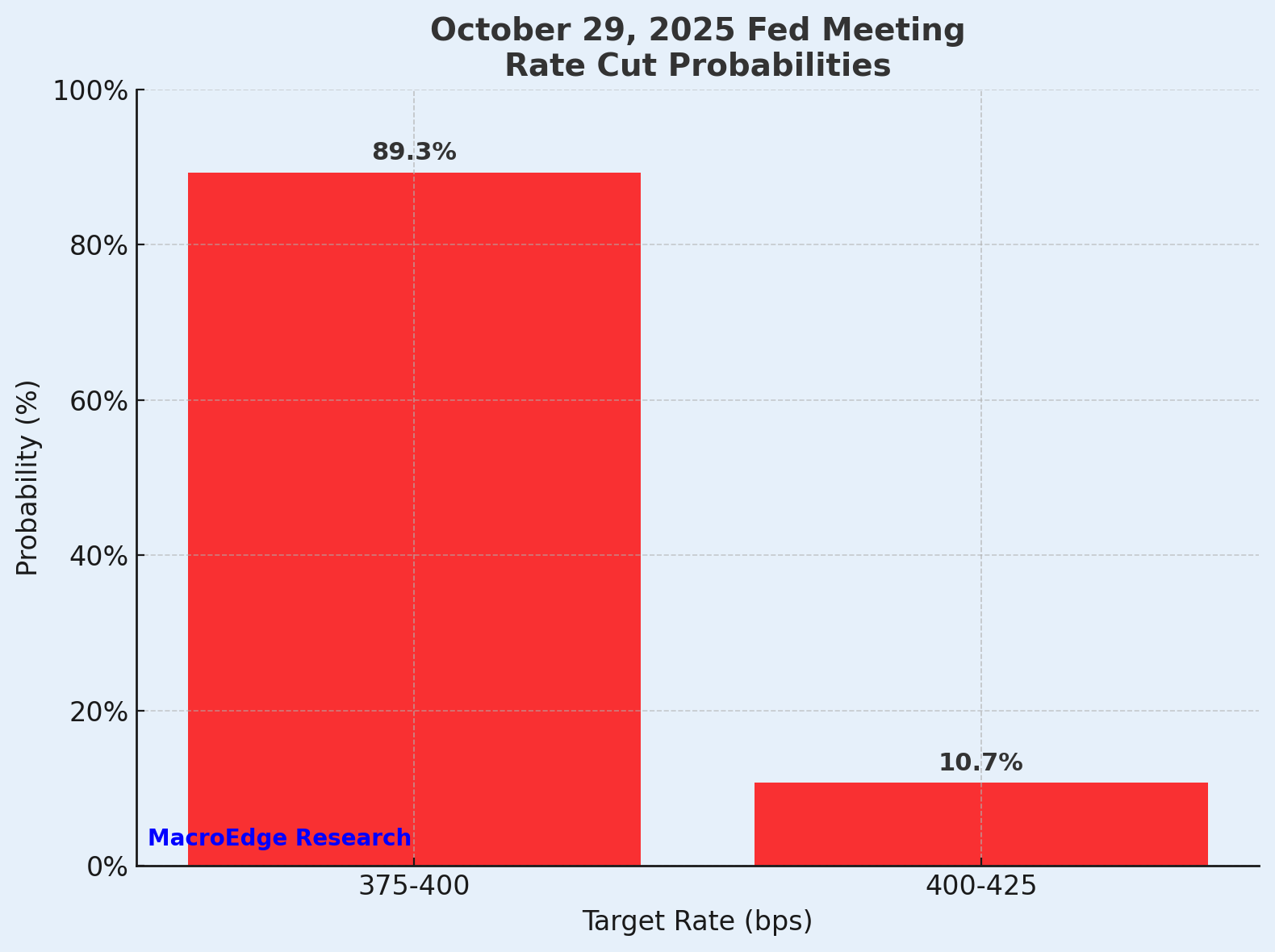

October Rate Cut

Odds of an October rate cut stand at about 90% (9 in 10) for a 25bp rate cut. This seems mispriced in the event of a hotter-than-expected print, or no print at all.

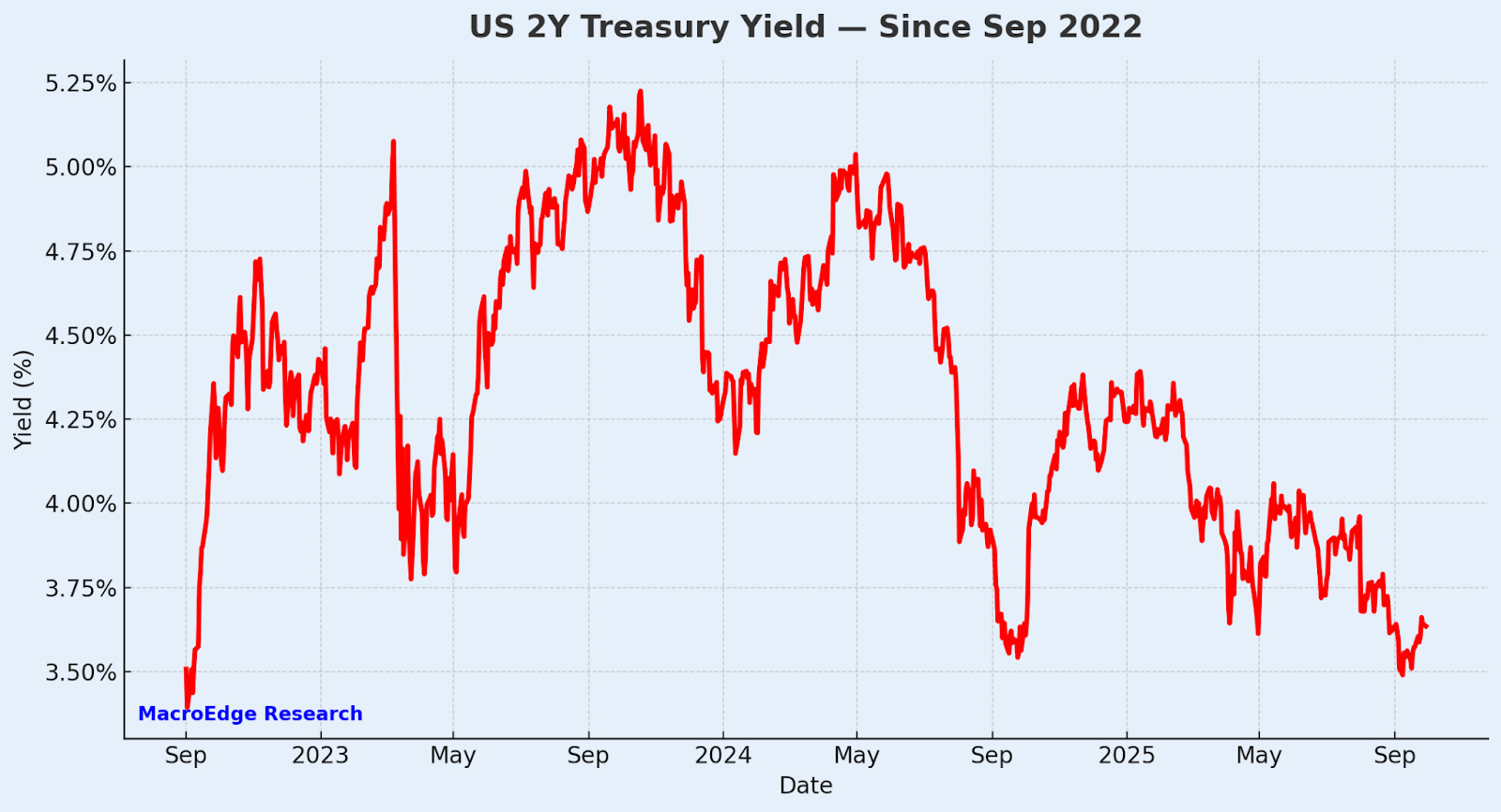

We can let the 2Y continue to be our signal on policy being too loose or too tight:

Pushing on a String - the Global Bubble in Germany, Japan, UK, Spain, South Africa, Canada

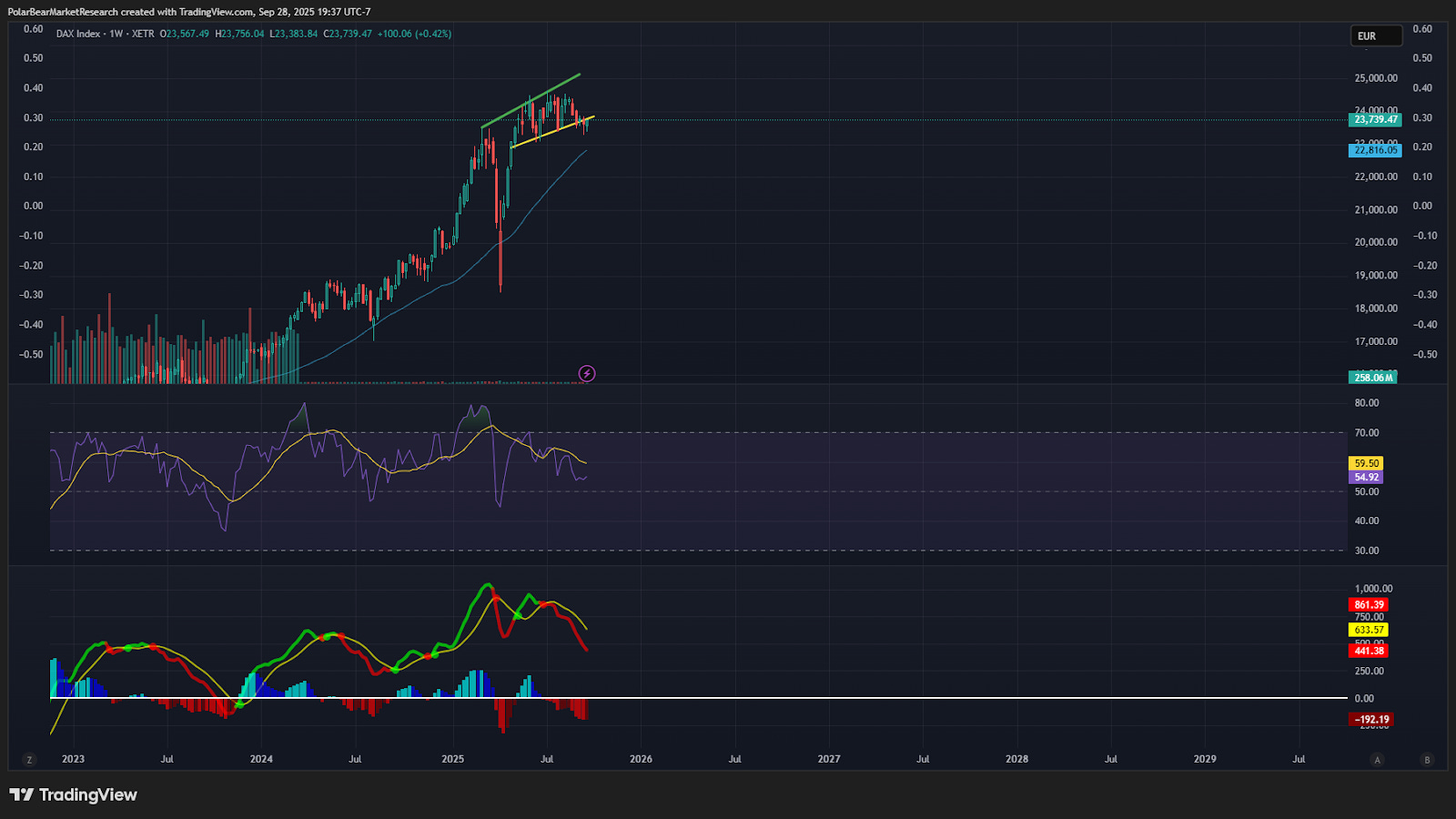

This has been something we’ve been wanting to discuss for a while - the global bubble - from Canada, to Japan and beyond. Major indices in these countries have decoupled from macro data (much like what has occurred in the United States) - which has meant continued records in the TSX, Nikkei, DAX (more stalled), close records in the IBEX, and in South Africa as well. Below we break down each country’s major index individually, looking at both technical conditions, and if they’re worthy of a ‘head scratcher’ rating - giving this macro-decoupling… With the first country on the list being Germany:

DAX

The DAX has been flat for much of the year after a steep rebound from the April intervention lows - the bearish divergence here spells trouble, and the German economy is in the dumpster, especially from an industrial standpoint. Global technology and software companies have fared better than German midcaps:

Japan - Nikkei 225

A similar setup to the technology bubble in the US

The Bank of Japan a week ago announced plans to begin a more extensive balance sheet rolloff - including of its stock & ETF holdings…

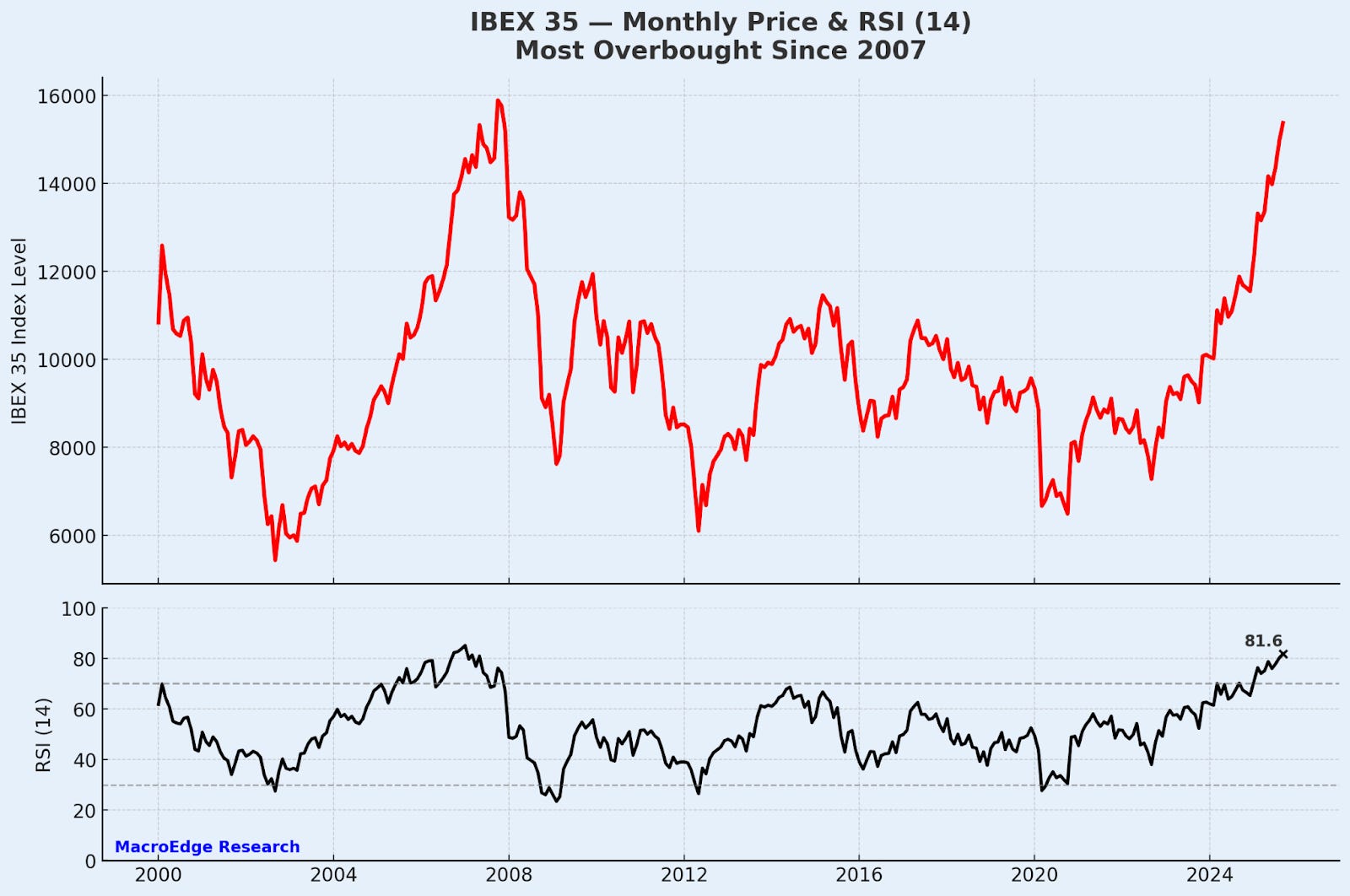

Spain

One of the most egregious bubbles, and called the ‘flagship’ of EU growth due to persistent migration from Africa and South America. The IBEX is now the most overbought since early 2007:

Our MacD oscillation reading on the monthly is on track to set a record print too… printing people through immigration seems to be a successful way to pump equities, along with easy fiscal and monetary policy, the real question becomes – will it ever end? The answer is always: of course…

Most overbought readings in Spain since January 2007.

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.