Weekly Macro Note: The Asian Risk, Pre-4th Macro Week, Warnings from 06 and 07

In the Weekly Macro Note - we discuss the latest on the Asian Risk - which continues to get larger in recent days - highlight MacroEdge updates - discuss the pre-4th Macro Week, and highlight warnings

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers and Community,

It’s great to be back for the last Macro Note of June, joined by John - Six will be out for the evening having a much more exciting weekend than I did, but I’ve enjoyed what actually feels like the first days of summer. For the 4th, I will be popping up to North Florida and enjoying some continued planning for the second half of the year as we prepare to expand our operations now with both MacroEdge, and all firms operating under our broader umbrella. I expect that this week - as frequently has been noted to me by John - is going to be the ‘Tonka Traders’ aka retail hour, which means that you get left with ‘Ocean Drive’ for the week, instead of Wall Street - who is already firing up jets and blasting down to either Florida or the Carribea… though some may be hitting that bizarre late season snow that I’ve seen in the Mountain West… Some crazy weather is happening all around the country!

This evening we’re going to cover the Asian risk - which is expanding dramatically with superbubbles in both Korea and Japan (which make actually lessen the damage here slightly), I will provide an update on Portfolio Strategy - which will finally be going live in Q3 - we’ll discuss being ‘back in our cadence’ and what to expect on the MacroEdge Radio front given that it’s been on about a two month hiatus. In addition to that, we’ll lay out the schedule for the week and what to expect on things like updates, a note to wrap up the 1st half of 2026 (hard to already believe that it’s behind us), and we’ll discuss new opportunities coming from MacroEdge and our ecosystem as they are coming available - many of which will be soon.

On the war front, what we’re seeing has pretty much become noise for equity markets. The ceasefire remains in place, and there are some volleys back in forth of inconsequential strikes not actually doing all that much. The one time we have been seeing Iran escalate is when too many tankers/freighters start using the Oman traffic lane in the Strait of Hormuz, and I expect that to continue for months. Traffic is nowhere near normalizing - and as I’ve said for months - I expect that it will take until the end of 2026 before we see actual ‘normal’ figures. Every brief spike up to this point has faded.

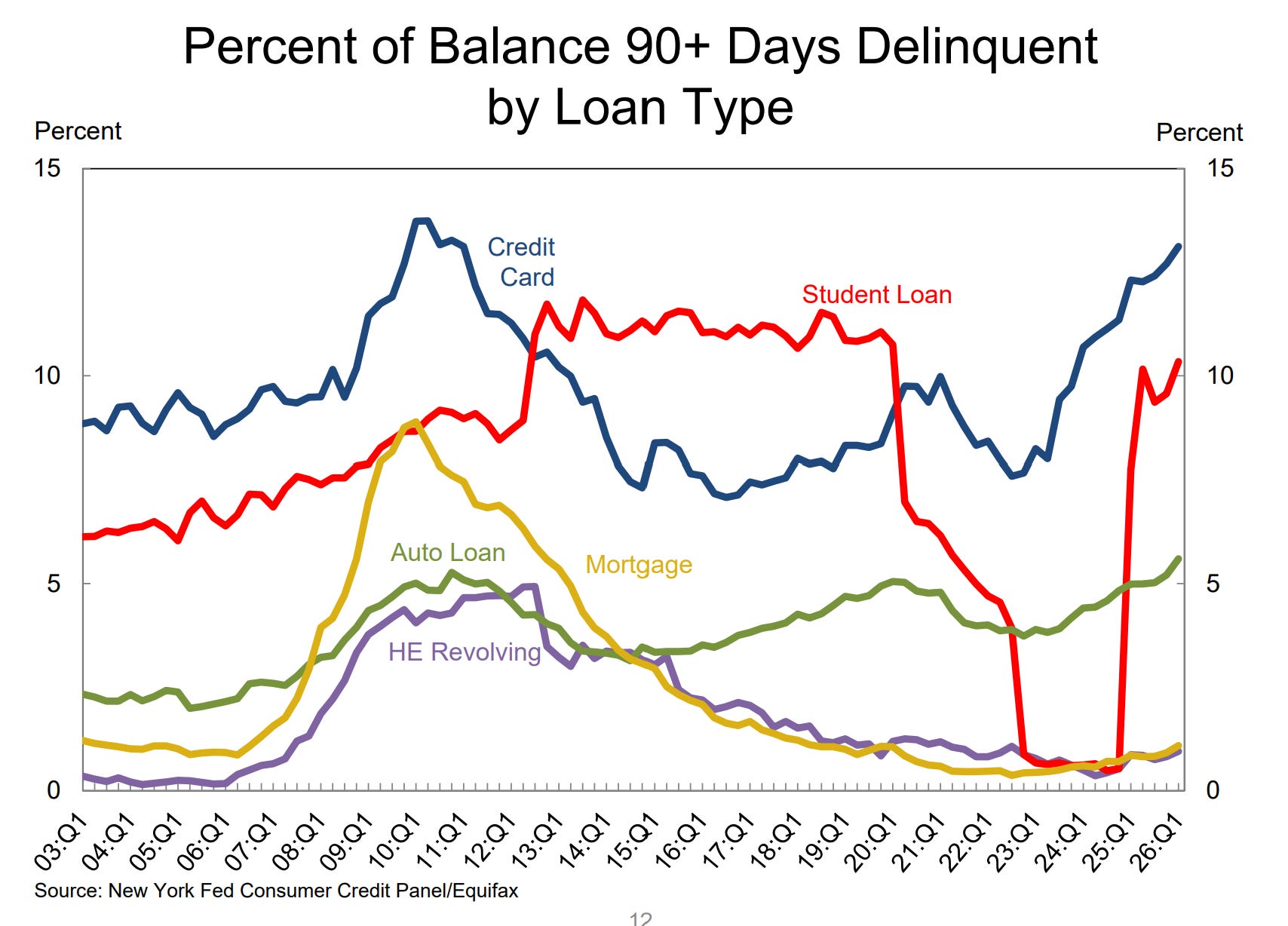

Consumers are likely in their final hurrah for what looks to be many months - there are a lot of contributing factors to this - but the debt load that the average consumer is facing is significant. Once the final holiday hurrah is through (which is next weekend), I expect markets to start caring more about the below data:

We know that the stock market is in fact the economy for the upper ‘i’ - and if the stock market halts its nominal gains, expect consumer spending to taper across the board. The FIFA bump is another effect likely occurring, and I am seeing restaurants really struggle under the latest weight of the inflation wave from the Iran-war energy shock. Once equities and nominal price levels stop rising, it will be over for this economy (and the market) in a feedback loop.

It’s a softening market backdrop, and I want to see weakness hit the Dow - particularly in housing and trucking equities - which have not softened as much as the MAGS and tech giants. Things are rattling in the markets from a technical and an internal standpoint, which I will provide an update on later in the week. This dumpster fire environment - or one might call a ‘bubble’ has been hit over and over and over with steroids, and the poor thing is now like a fat cat that’s struggling to get up and even walk to the food bowl. Yes there are midterms coming up in November - but we continue to just run the deficit drunken high like a bunch of fools and the punchbowl must be taken away, though I am afraid we are going to get the complete opposite scenario with things like YCC & rate cuts eventually coming right back in to play for a final grand finale (ie: Japan scenario - as I’ve covered for going on 12+ months now). While nominally, they are going to want to keep the party going this week, I would put very little cadence in what will likely be a low volume week.

Not yet a MacroEdge Ozone subscriber? Upgrade below and get all of our research, data, portfolio strategy, and much more:

MacroEdge Portfolio Strategy - Update Soon

We are having some exciting meetings of late relating to the direction of Portfolio Strategy - and actually being able to invest in model portfolios that will be led by Six. These discussions and our planning continues, so stay tuned for some exciting news and announcements in the 3rd quarter as we spool up Portfolio Strategy - and expand it outside of the Ozone ecosystem… This will include both a research and portfolio component combined, and when we have more information available - it will be shared as soon as possible.

Back into our Cadence in Q3 & MacroEdge Radio

One of the most challenging things about growing an organization is our limited bandwidth as a team. We’re solving a problem here, driving a boat across a frenzied lake (figuratively - I have not had to do this yet), the next minute to solve another problem, developing a new dataset, and traveling across the country and world to interact with our customers. As a founder-led organization, when we’re away from our office - that means things like our Macro Report cadence suffer, and that is something I am fully committed to changing in the second half of 2026.

At minimum, you will be getting 3 reports per week out of Ozone - with the Weekly Macro Note and at least two other Macro Notes (the Midweek) and sometimes we will extend that to 4 during special situations - as we did during the Iran war for energy coverage.

On top of that, we are bringing back MacroEdge Radio on a weekly cadence, and when I am traveling, it remains extremely difficult to host the show remotely from my device with John joining, so we’ve figured out a new workaround that should enable us to never miss a beat on the show front. There are so many new guests and faces I look forward to inviting on the show with John (including myself at some point) - but wanted to note this since it was a question that’s popped into my email several times in the last 2-3 months.

For the week ahead:

Tuesday: Energy Note & Update to the Inventory Situation (is the trade cooked?), Employment Data Preview

Thursday: The 1H 2026 Sendoff, Global Technicals, & What’s in Store For 2H from MacroEdge & More

Friday: Redeye Macro Note - 4th of July, Employment Data Review

Thursday Nonfarm expectations are for something relatively modest.

Pre-4th Macro Week Ahead

It’s a relatively quiet week on the macro data front, with labor data coming in on Thursday because of the Friday market holiday in observance of the 4th. On top of that, it’s quiet for earnings too. I expect Asia to drive much of our market action this week - and keep an eye on both JPY and KRW - as well as the KOSPI and Nikkei - which continue to endure violent volatility and swings.

Monday - n/a

Tuesday - MacroEdge Job Cuts Tracker - June

Wednesday - Japan Consumer Sentiment, Kevin Warsh speech

Thursday - June Nonfarm Payrolls - expect FIFA impact to wane

Friday - US Market Closed

The Asian Risk

The Asian risk is something that I’ve flagged now since the beginning of the year - pre-Iran market pumping - and it’s something that has only grown in magnitude, especially during the war. Markets there are facing record concentration risk, currency risk, and weak currencies, and meteoric leverage usage has enabled these parabolic rallies. With risks mounting to things like the AI and semiconductor trade (highlighted by John below) and the BIS, expect that these risks only multiply here in the next 1-2 months. If the currencies strengthen or the markets continue to wobble as they are, the tech stall will get more pronounced in the US and elsewhere.

Continue reading below by upgrading to Ozone…