Weekly Macro Note: Tariff Cannon, FOMC Rate Decision Projection, Yields Rise, Technical Outlook, Portfolio Strategy Update

In this Weekly Macro Note, we discuss the latest temporary tariff cannon, discuss the FOMC rate decision this week, talk about rising yields globally, portfolio strategy update, & more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers and Community,

This evening, we’re following up on the Saturday Macro Note with macro data, portfolio strategy, and a discussion on the upcoming FOMC week. It’s about a 0% chance that the FOMC moves on rates this year as the short-end has started popping higher. With all of the celebrations about prelim headline GDP and how golden this era is, there’s even less reason to reduce rates this month. With data quality in question and little sign of a slingshot moment for unemployment, as inflation remains entrenched, I expect the Fed to tilt its mandate focus slightly in commentary.

On the equity market front, the QQQ and S&P have continued to lag, while industrials and small caps have outperformed. I strongly believe we’re going to see the differentiation thematic from a performance standpoint really accelerate over the remainder of the quarter. For the time being, AI and interventions remain top of mind for everyone, as the ‘TACO’ thematic continues to dominate. On Friday, we saw the NY Fed acting on behalf of the Treasury, conducting rate checks on the USDJPY pair.

Tonight I am going to cover the latest developments on the tariff front - including Canada’s Carney walking back his own ‘trade deal’ with China - talk about the macro week ahead, highlight all of the evidence pointing towards an FOMC hold this week, highlight my latest technical outlook, discuss AI performance, & briefly cover some of the latest developments in energy markets. I will be back on the road tomorrow, en route to Arizona for a very brief 24-hour stop, before heading back east and getting ready for our next week on the road. Lots of exciting developments ahead, and continue to stay tuned for everything we’re doing. Futures are pointing to a tepid opening, now having bounced off the lows, but directionally, the distributive pattern continues in the things that will actually matter for market direction… (ie: NVDA)

Interesting datapoint of the weekend:

If you haven’t yet joined our MacroEdge Ozone community, make sure to join our Ozone network below, and get all of our data, research, reports, and more below:

7-day trial access is available through Substack.

Macro Week Ahead

Monday: Durable Goods (US)

Tuesday: Japan SPPI (JP), CB Consumer Confidence (US)

Wednesday: ADP Employment Change (US), FOMC Rate Decision (US)

Thursday: Tokyo CPI (JP), Pending Home Sales (US)

Friday: Personal Income / PCE (US), UMich Consumer Sentiment (January - Final)

FOMC Week

This week, I expect the Powell/Fed v Trump Admin war to heat up. With the very low chance of a rate cut this week, we may hear an announcement on the Powell replacement, though that is still a few months out.

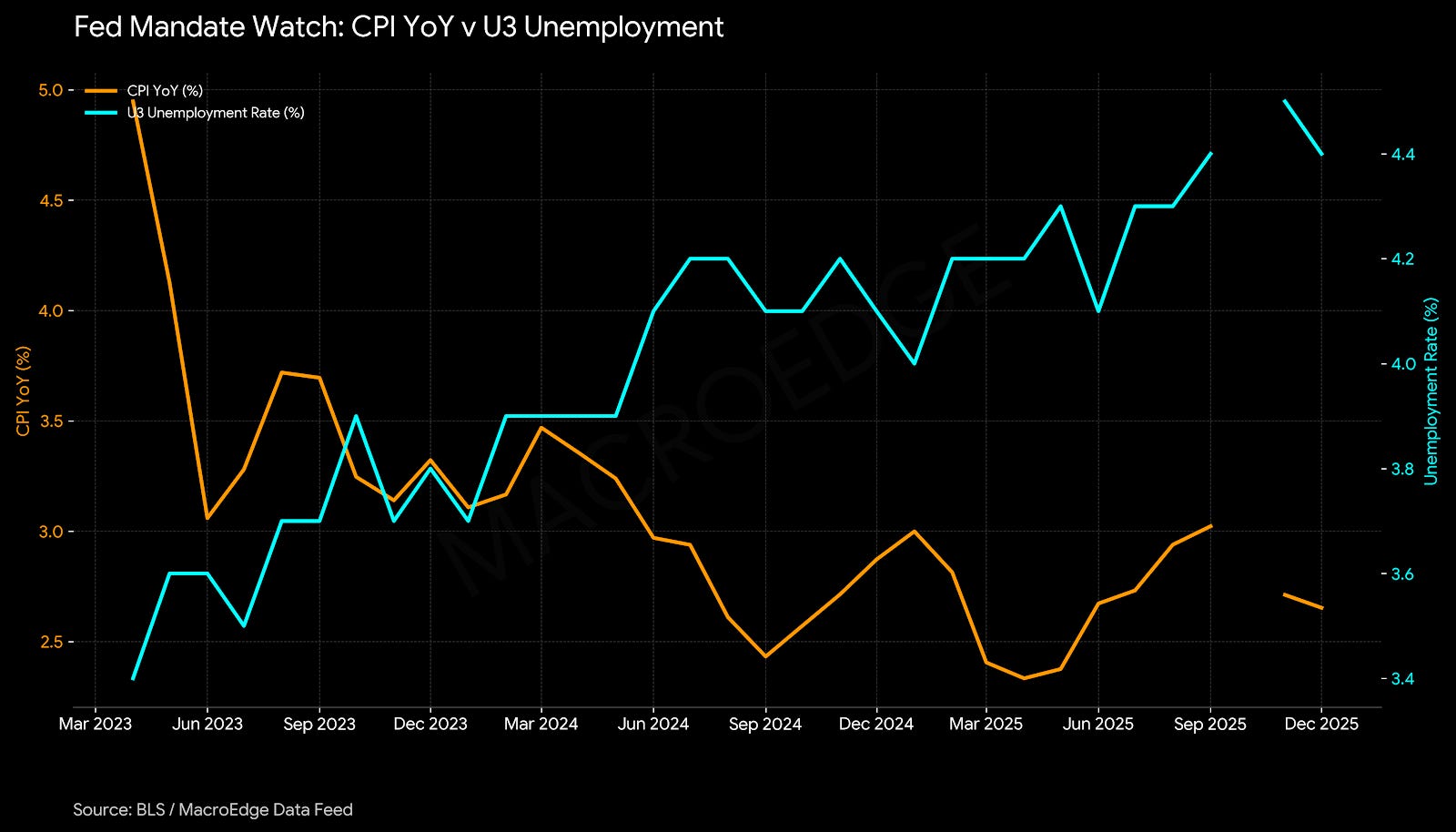

Fed mandate watch:

Until U3 eclipses 4.9%- the Fed’s focus should continue to be on inflation, with current demographics. While there are some downside price impulses, the broad based consumer basket of things we actually buy and pay for every month continues to go up. Because of the huge 2020-2023 CPI spike, it’s going to take consumers a substantial period of time to adjust to these new price levels.

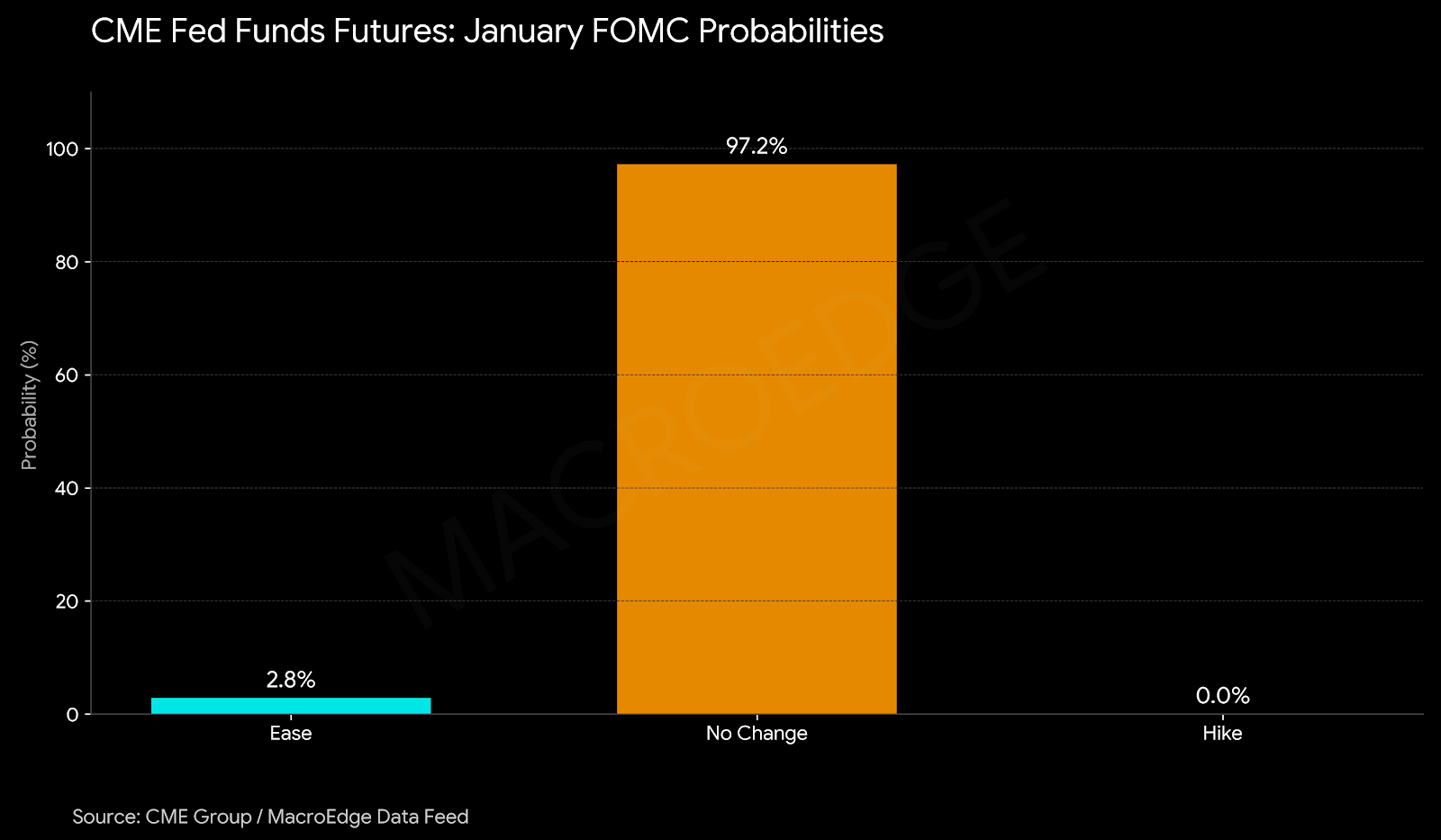

The 1-month yield is showing some signs of upward movement this month, yet another indicator of the looming FOMC decision:

CME Fed Funds Odds for January, now almost 0% for a cut this month:

Outside of the facts above, the FOMC v Trump Administration war is hitting a boiling point, and if Trump picks a dove to replace Powell, that would crank rates lower against the bond market’s wills, expect the long end to continue to move higher… Yes, it really does beg the question: is YCC in our eventual future, too? I happen to think so.

Continued below: (technical outlook & equity markets, AI performance, energy markets & opportunity, MacroEdge Portfolio Strategy & Commentary - Six, gold update)…

Technical Outlook & Equity Markets

Bitcoin and other cryptocurrencies look very weak on many timeframes:

As capital has flowed into metals and other commodities, cryptos have suffered.

Nasdaq (QQQ) - 3~ month period of distribution continues.

NVDA

The Big Four Bubble: Nikkei, KOSPI, TSX, IBEX35

Nikkei - developing a significant negative weekly divergence, which hasn’t happened since July 2024:

KOSPI -

TSX - Canada -

IBEX35 -

BCOM - All Commodities Index

Pushing above the 2022 level.

VIX (Vol) is working on putting in a base:

2Y Yield - Rate Cut Delusion if This Moves Higher…

AI Performance

We’re starting to see mixed performance in the AI-space, though the basket has continued to move higher on rampant speculation and due to its close correlation with Asian market movements (hello Japanese financing)... The Trump Administration and BoJ alike are terrified of what a Carry Trade unwind might mean, given where the Nikkei currently sits, and another BoJ hike is on hold for the time being after the rhetoric last week. With the interventions and harsh comments from the new Prime Minister, the trend in higher yields and a weaker yen may resume in very short order once the interventions start to wind down in the interim.

With the leaders like NVDA having stalled, keep an eye on the broader basket (AIS) and data center trends over the remainder of the quarter for further clues on direction here. Data center postponements and cancellations are up, and the construction spending YoY rate is slowing quite considerably from the peak.

Energy Markets and Opportunities

Natural gas has staged one of its largest 7-day rallies on record, surpassing $6 in spot markets.

Forecasters and my preferred modelers are projecting a third major arctic blast arriving next Thursday and lasting for several days. It doesn’t appear there’s a bunch of precipitation in the coming wave.

Oil has continued to hold at $54 for almost a year now, and a break and hold of key moving average trends would be very bullish for oil. For the time being, the Administration has stepped on oil every single time it’s looked like it was about to rally to higher levels.

XLE - oil & gas index:

OIH - oilfield services

RIG - Transocean (offshore drilling)

IEO - exploration and production

Oil has been one of the last commodities to not participate in the unprecedented moves we’re seeing. Energy names (in the baskets above) are starting to catch on, and it could be a very interesting catch-up play if conditions remain constructive. The Administration is hyper-focused on keeping oil (for gasoline) prices under control, but a combination of market tightness and a geopolitical event could get things moving considerably higher. If CL doesn’t break below the 54 level, I think it looks quite positive, even with the headwinds above.

Below, Six will continue with our portfolio strategy update and commentary, talking about opportunities in software and much more.

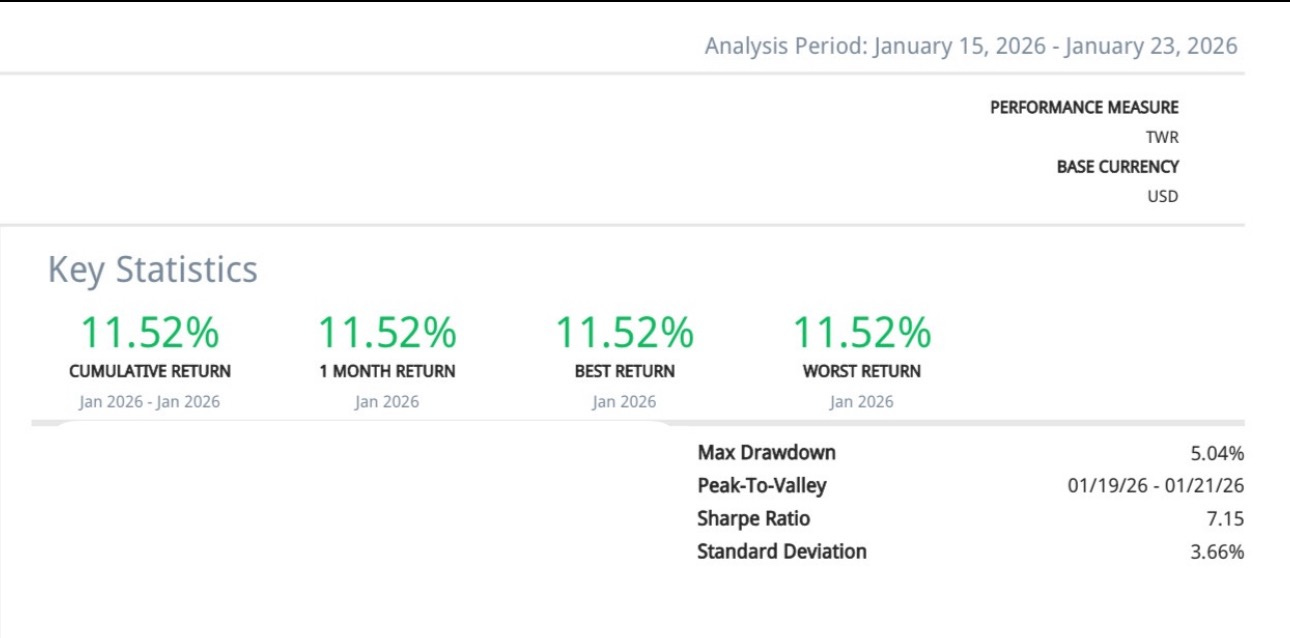

MacroEdge Portfolio Strategy Update - January 25, 2026 (@SixFinance, Head of Research)

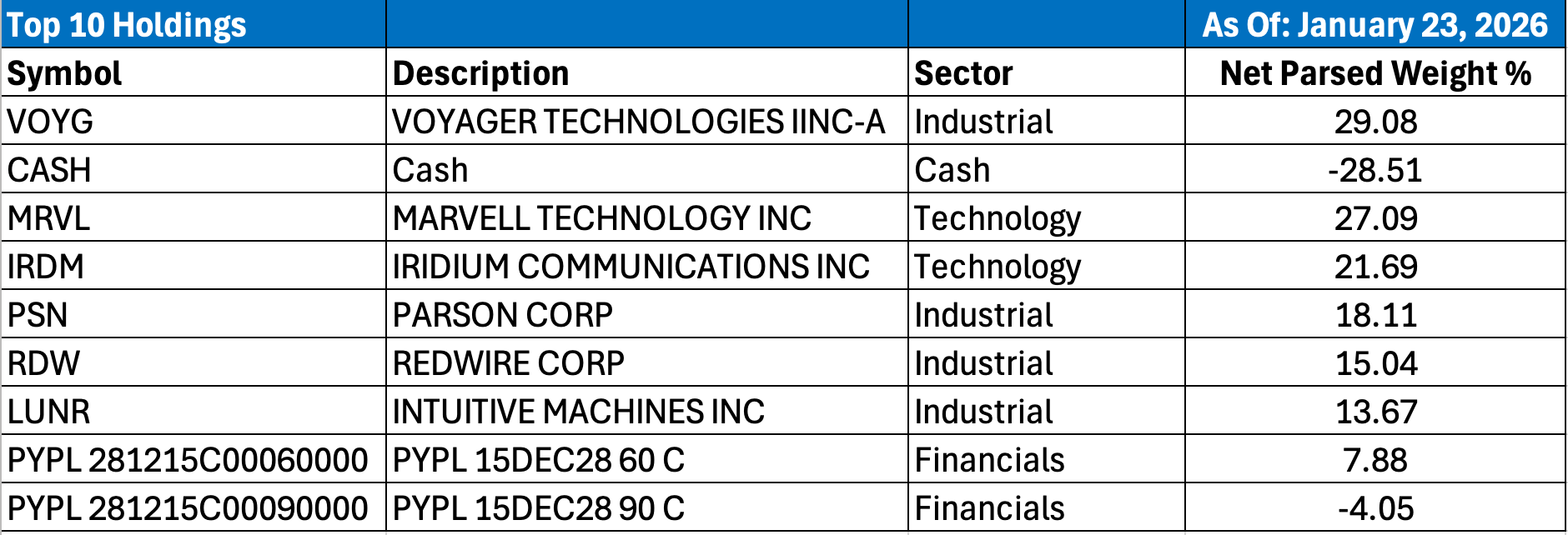

Performance has continued to be very strong in the portfolio since the migration to IBKR on the 15th. Current positioning remains unchanged since the last midweek update. The portfolio continues to exhibit large amounts of volatility, as expected. It’s what I signed up for when I decided to press the aerospace and defense trade.

The largest detractor from performance thus far has been MRVL, a position funded by selling shares in the aerospace basket, costing several additional percentage points of PnL. My primary bull thesis in MRVL is concentrated in the memory optimization section of the business. MRVL lies uniquely positioned to address the current memory shortage that has sent MU, SK Hynix, SNDK, and other memory firms into an explosive parabolic move to the upside. Their technology allows for both the pooling of memory to reduce chip downtime, and for old legacy DDR4 memory to be used for AI applications, of high value in a memory shortage.

While I remain more bearish on hyperscaler capex over the medium term than consensus, I feel a degree of additional safety being long one of the firms mitigating one of the key bottlenecks in the AI supply chain, and would like to see management more directly highlight the memory optimization line of business at earnings to remain long. I see the potential for a dramatic repricing higher over the next 6-12 months should they execute properly on both execution and rhetoric around the segment.

Software

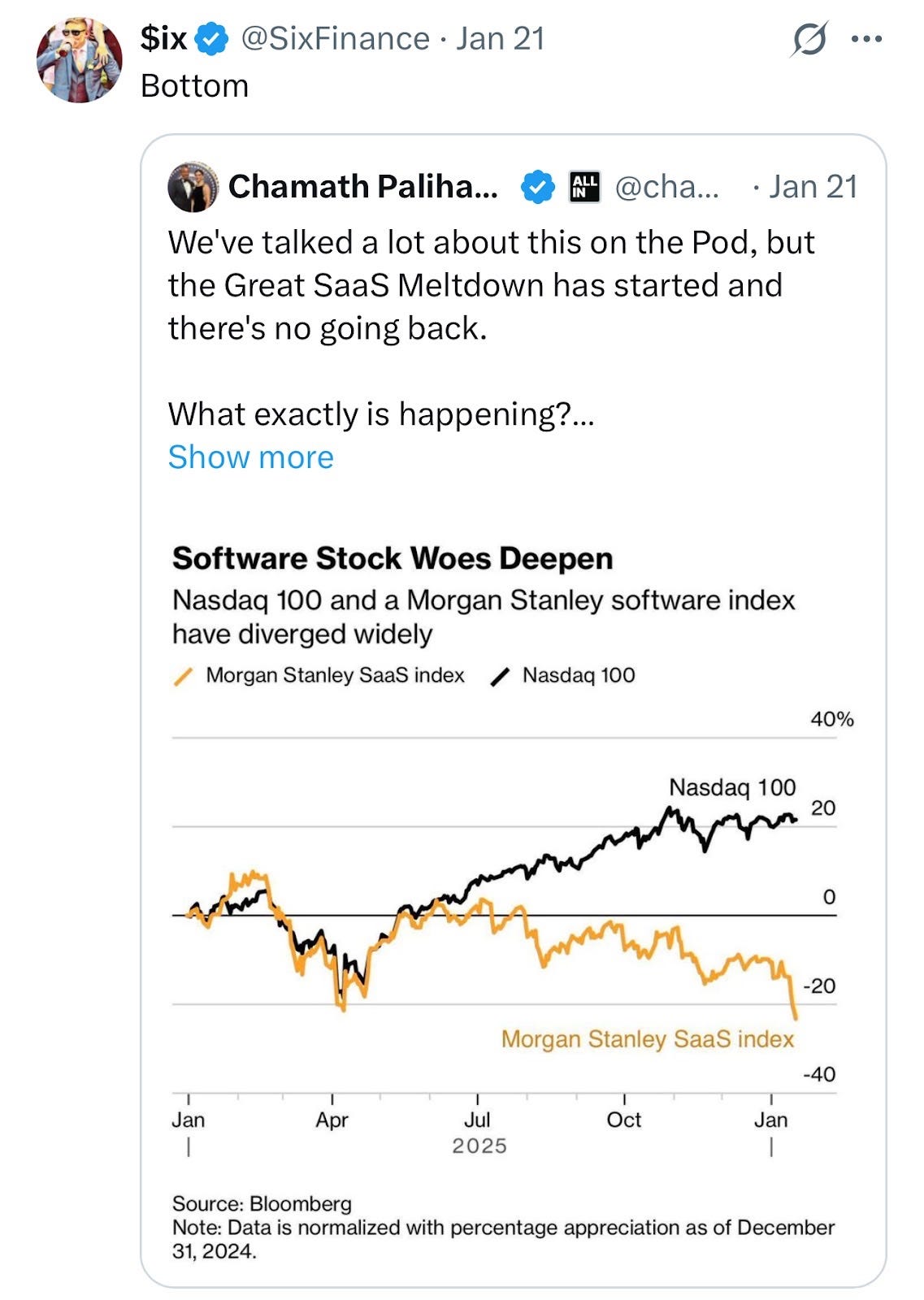

Funnily enough, it looks like Chamath has gone max bearish on software in the hole, helping to put in at least local lows across much of the sector. As feared, I did in fact neglect to seize the opportunity to put risk on right at the turn, and therefore missed the point of maximum profitability. Nevertheless, JPMorgan’s bullish analyst rhetoric last week around software right at the trough in sentiment helps to derisk the sector from my point of view. They argue, in line with my own beliefs, that the software sector arguably sees tailwind opportunities from AI rather than headwinds. Opportunities for margin expansion and further growth.

I plan to open bullish option combos tomorrow, opening put credit spreads to finance call debit spreads. This could just as easily be done by simply going long common shares, but I want the embedded leverage as I see the opportunity for a drastic reversal in sentiment as hyperscaler AI capex continues to be the financing agent for ex-hyperscaler growth and margin expansion across the market. I will open these tomorrow in TEAM, NOW, and SAP.

I will see how the market is reacting to the politically polarizing events of this weekend before putting this on, as well as the software sector behavior as well, before finalizing how wide I want the spread on the credit spreads, and how much downside exposure I really want to open myself up to, but overall I believe the direction of travel in software broadly is now higher. Right now, I’m hunting for a large countertrend rally, but I will be buying enough time in the options to allow for a larger move higher should it materialize.

General

I’ve spent a lot of time lately thinking about whether we have truly crossed the Rubicon into a multipolar world. This carries enormous weight from an allocation standpoint as Democrats lead in midterm projections by a wide margin. Many of the thematic trades we have been afforded by the political sea change are at risk of being unwound should policy broadly move in the other direction, and if done in a spiteful manner, the tails are wider still.

From a China standpoint, I think supply chain diversification will remain a prevalent theme as both political parties seem to agree on throttling China, though the practical application will probably differ depending on who gains political power in the midterm elections.

The announced government investment into USAR over the weekend likely reignites excitement in the critical minerals trade, as many of the smaller players have traded sideways for months, such as LAC, NB, and others. Albemarle has gone straight up since the summer, and is a decent example of how some of these trades could perform following the initial manic price appreciation, followed by a selloff leading to a period of price stabilization and cooling off.

LAC presents an interesting opportunity for a sustained move higher if lithium prices sustain at these levels or bid further.

Bold moves to stabilize the Japanese Yen create an interesting buying opportunity at these levels, although the large losses I sustained in that particular trade last year make me hesitant to get involved again. I may do so. Looking at it from a constraints perspective, the JGB market may force a rollback of its more aggressive policies. The Japanese PM risks getting evicted from her position by the bond market.

I continue to struggle to see any meaningful value across the U.S. yield curve, as the powers that be wage war against the front end of the curve, and fiscal policy continues to be a tailwind for long-end yields. Without further deterioration in employment, it’s difficult to find the bull case in the long bond, and the bear case is equally challenging with Bessent at the helm of Treasury, actively capping yields.

Moving into this week, we have fresh tariff threats on Canada, and the shutdown to potentially be priced in. The vol controllers are still hard at work, with Trump noting the minuscule dip in1M EU trade war threats over Greenland. I will be watching closely to deliver in a hurry, if needed, although I still think it’s just more of the same at this point, and a continuation of present themes.

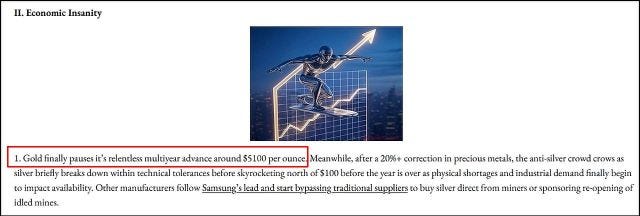

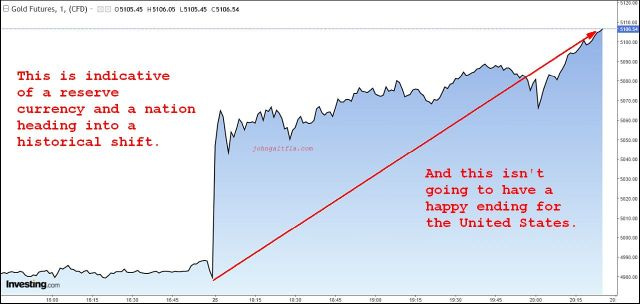

And It Looks Like Another 2026 Prediction Just Hit: Gold above $5100 per Ounce (@RealJohnGaltFla, MacroEdge Contributor)

Is this author happy about this?

Hell yeah.

Is this author terrified by this?

Hell yeah.

From the original JohnGaltFla’s Wild Predictions Thread for 2026:

I’m not bragging, but hell yeah, I’m bragging.

And I’m also scared as hell as to what is next. If this move verifies with the rally continuing, a peak higher than $5100 per ounce is a given.

Now we’re here:

This is the worst thing that could have possibly happened.

Why? It means that geopolitical and economic instability is moving towards new levels unforeseen by equity markets, political fools, and the masses.

I pray for everyone’s sake that they listened to this old guy and heeded these words:

If you can’t hold it, you don’t own it.

For more details, please refer to our Terms and Conditions.