Weekly Macro Note: Start of the 'Long Summer', Look at What's Ahead, Consumer Slowdown Risks

In this Weekly Macro Note - we discuss the start of the long summer, take a look at what's ahead for markets, and discuss consumer slowdown risks... #MacroEdge

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge readers and community,

It’s fantastic to be back from the 4th of July weekend and back in the driver’s seat of the ‘long summer’ ahead of us. From now until September - it’s a period to really accomplish a lot and buckle down across the board, so I know we’ll take advantage of that, and hope you do too.

From a market standpoint - I am having a little bit of a difficult time getting a read on the high-beta stuff as Bitcoin and other hyper-leveraged asset classes have bounced in recent days. While it’s certainly plausible that these classes bottom first, the technical setup in most things is becoming clearer as we head into mid-July, and directionally, things are going to move substantially based on where we’re sitting today. With the Korean and Japanese risks at new heights - I think it’s quite plausible that a downside impulse could play out in a ‘swan’ style fashion - catching a lot of the amateurs that joined the party very late (ie: last 4 months) off-guard, though with mid-terms now just a few months away - the administration is going to have to balance wanting to fight inflation & restoring affordability with keeping asset prices higher for their primary voting bloc/supporter base in non-presidential election years. With consumer confidence & sentiment readings at all-time lows, there’s a lot of apathy about how things are going right now (with the exclusion of the AI/semiconductor) trade that has driven record market concentration and pushed markets to new heights. The market setup as we head into the long summer is becoming more clear:

We may get some sort of initial trap with this setup and then move onto resolution. Given market concentration risks, negative divergences, internals, and now risks to future earnings in the AI space as CAPEX comes under investor scrutiny - it’s quite obvious the direction to which I think this will resolve itself, though I remain skeptical until we see any further directional confirmation for the crypto trade. Because of market concentration risk - this also doesn’t need to spread to a bunch of other areas in markets - but I think it will because the stock market is now the economy.

As discussed below, this is a very quiet week for corporate earnings (and macro data), and I expect to spend most of my time monitoring energy markets and the Asia situation, namely Korea and Japan, due to many of the risks that we’ve discussed over the last 6 weeks.

This is a very quiet week for corporate earnings. We start off the following week with bank earnings, and I expect that Q2/Q3 will mark a lot of tops for the semiconductor/AI names in terms of the earnings (yes, data centers too). Without taxpayer bailouts or a perpetual cash stream that they are trying to establish, whatever is left of our ‘profit-seeking’ system is going to sniff out what a mess we’re walking into in this trade.

Macro Week Ahead and Start of the ‘Long Summer’

No earnings of companies >500 billion market cap this week.

Monday: ISM Services PMI, Fed Speech

Tuesday: Export/Import Data, API Crude Stock Oil Change

Wednesday: FOMC Minutes, EIA Crude Inventory

Thursday: n/a

Friday: n/a

Not yet a MacroEdge Ozone subscriber? Upgrade to Ozone below and get all of our research, data, portfolio strategy, and much more below.

Report Schedule for the Week

As discussed in our previous Macro Note, one of our goals is to get the train back on the track, team and content wise, so that critical reports aren’t being missed and dispatched to you as our readers and clients, even when we are stretched thin and on the road with client work. Part of this effort involves expanding our network of contributors - and other items like briefer notes that have been discussed in the past. We’re going to continue to find the most optimal solution and look forward to the long summer ahead as a period to deliver the absolute highest quality and most actionable research possible, so that, namely, you all can be making the best decisions for your organizations and your portfolios.

Tuesday: June Employment Report, Energy Note

Thursday: New Partnerships and Offerings, Midweek Macro Note

Friday: MacroEdge Radio resumption - Episode #75, Redeye Macro Note

Sunday: Weekly Macro Note

Expanding Our Umbrella over the ‘Long Summer’

As we’ve discussed over the past 16 or so weeks, many opportunities have arisen for us as an organization - and we will be discussing these over the next 4 or so weeks. Several new partnership opportunities are ones that we will share and pass along, and I am excited to do so. Stay tuned for more on the Portfolio Strategy front as well.

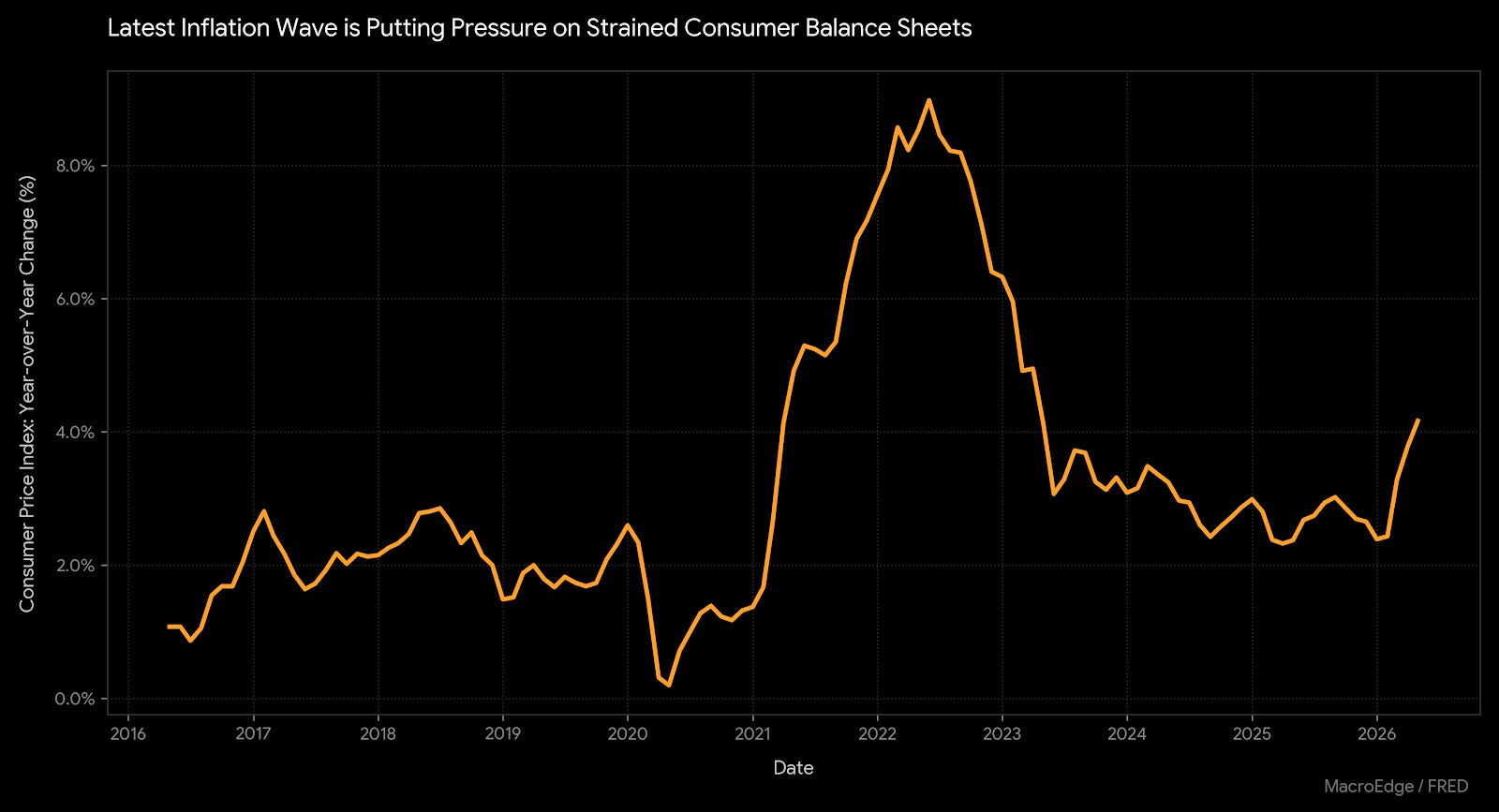

Consumer Slowdown Risks

One of the things I’ve been highlighting is the risk of a consumer slowdown in the second half of 2026 if asset prices fail to continue their ‘melt-up’ that began with the start of the Iran war and during an enormous federal deficit that is rendering the Fed Funds Rate essentially useless in most sectors outside of things like housing (yes - it’s important) but with demographic changes, etc, there are reasons why this cycle has/is taking much longer to play out than anticipated.

The latest wave in higher prices - especially in food, airfare, etc is putting a lot of strain on consumer balance sheets.

The Iran war was a huge mistake on the ‘price war’ side of things as 1) wars are almost always inflationary and 2) going to war with a massive oil exporter usually results in an inflation shock.

Continued below: Consumer Slowdown Risks, KOSPI Timebomb Part 3, American Housing Questions the Media Never Asks - John Galt).