Weekly Macro Note: Rate Hike Analysis, Technical Overview... Ticking Risk Clock, Energy Portfolio Strategy Update, Portfolio Commentary, & More.

In this Weekly Macro Note - we discuss the potential for rate hike(s) this year, highlight the technical developments across US equities and commodities markets, talk about risks, energy, & much more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

I am writing to you this evening from Fort Worth, TX, as I embarked on a brief trip to catch up with my business partner and get things organized as we approach the second half of the year (crazy, yes - I know)... We’re continuing to be at the forefront of shaping key narratives in the macro landscape, and that will only accelerate in the second half of the year as Portfolio Strategy arrives to MacroEdge. While we continue to expand our Ozone efforts through the Substack (that you are reading this on), we are also making strategic adjustments in our organization to stay competitive in this fast moving world. Some of these adjustments involve shifting out of unfavorable industries and into things that we do best - and consolidating our resources & impact into the strike-zone, a term that I’ve been more frequently using of late. As a ‘lean & mean’ organization, we will continue to deliver great impact through our Macro Research, Transform, & ‘Other’ service areas - and look forward to doing things like resuming MacroEdge Radio in the weeks to come. Additionally, our partnership with TREX is only going to further our efforts in our key focus areas of the economy, and I am excited to build on the existing relationships and partnerships that we’ve developed over the past 3 years.

In the markets, futures are down slightly off of the Friday close as commodities continue to move higher. There’s very little tanker traffic in the Strait of Hormuz - and there’s the potential for a resumption of the war this week in the Middle East, given that fact. The tolling system is churning boats through far too slowly - and this continues to cause an accumulation of issues that will eventually resolve through massive cost increases, not only in the commodity-heavy import regions like Southeast Asia, but these same pressures will make it to the United States in the coming months as we continue to do things like run down the SPR at the fastest rate we’ve ever seen. At current drainage rates, we will be looking at pretty massive issues come July now on the fuel & distillate front, and we’re already hearing anecdotes from motor oil suppliers saying they’re being warned of looming difficulties in delivering said oils and products. I firmly expect that we’re going to see more manipulation from the media companies in the US to attempt to control WTI prices, but for the time being, people are growing more skeptical about the Trumpian approach to resolution in always saying that there’s a deal just moments away. Iran has little to gain by making a deal right now, and they have their largest leverage with the Strait of Hormuz, and second largest leverage point in high oil prices (with third being control over the Houthis in Yemen)... Iran’s goal of finding a sweet spot in WTI that causes max pain for US consumers while still being able to export product w/o demand destruction is their end goal, though inevitably it’s going to take shortages to resolve the demand side right now, which has shown no signs of abating to this point.

The economy remains in a very lopsided state, in its ‘i-shaped’ state, and directionally without assets and equities falling to any significant degree. This trend is going to continue for months and years to come, as the gap eventually gets so large that there’s little hope for mean reversion to past trendlines.

This evening we’re going to briefly cover Part 2 of the On the Ground series from Amarillo, in a preview form, look at the Macro Week Ahead, discuss the technicals in our ‘Technical Overview’, highlight the Energy Portfolio Strategy, & Six will have more in his Portfolio Strategy note…

Not yet a MacroEdge Ozone subscriber? Upgrade below to get all of our research, data, portfolio strategy, reports, access, and much more:

‘On the Ground’ Research Part 2

I continue to compile the last few discussions from Part 2 of our ‘On the Ground’ Research trip from Amarillo. Given that I’ve been on the road to meet my business partner here in the Dallas-area for a few days, two of the five discussions I am covering in Part 2 have yet to make it - so apologies for the delay on this component. At almost 30 pages thus far, the ‘On the Ground’ series is surely to be one that everyone will have enough to craft their own strategy and takeaways from - and I continue to be surprised at the sheer # of people on platforms like X discussing what a difficult year farming is facing to this point. Add in the wildfire element as well, and historic dust storms in Kansas, and this is already looking like it will be a memorable year.

Both wheat & corn are starting off the week on a positive note (from a commodity price standpoint), and I continue to expect that this will be the case as long as oil (WTI spot) lives above the 100-105 range.

Macro Week Ahead

This week is not that crazy from a data release standpoint, with the FOMC minutes coming out, as well as some key real estate data. Notably, April saw rents increase on a YoY basis for the first time since the major 2022 inflation wave, and this is something we should really keep an eye on for the next several days. On the earnings side, we have Nvidia, which means the resumption of a war will likely wait until then (or after), and that’s really all for the week.

Macro Data Releases:

Monday: Empire State Mfg Index, Industrial Production

Tuesday: Housing Starts & Permits, Fed Barr

Wednesday: FOMC Minutes, Fed Waller

Thursday: S&P Flash PMIs, Philly Fed Mfg and Price Data

Friday: Existing Home Sales, KC Fed Mfg Data

Earnings >$500bn MC:

Alibaba (Wed)

Nvidia (Wed)

Nvidia is going to get a horse-race-like obsession given the speculative mania in the entire AI-space, though I will not pay much attention to it. We will likely have an update from Six in the Thursday Midweek Macro Note to recap earnings and see what lies ahead in this very fast-moving market environment. The question remains if we just completed a leg up and a ‘blow-off top’, or if inflation will run so hot to the point that assets and equities directionally are locked in to accelerating to the upside.

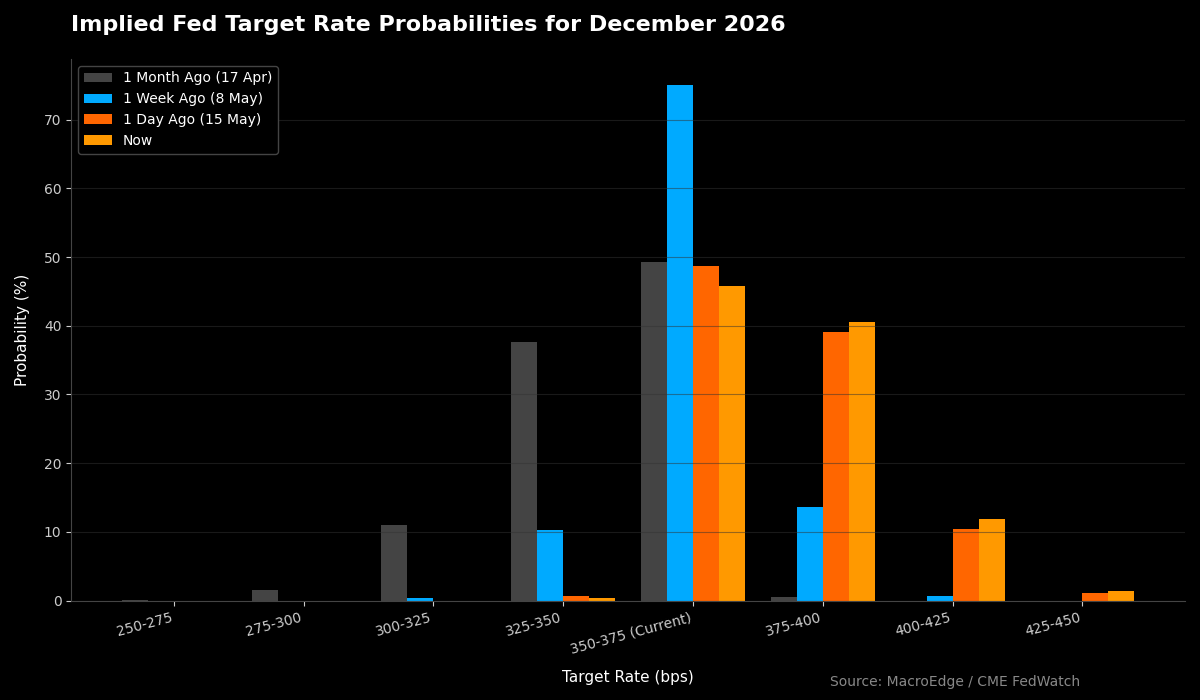

Continue to watch inflation data in the weeks & months to come as the odds of hike(s) before the end of the year are now being meaningfully priced in. WITHOUT demand destruction (which we are not close to those price levels for the time being in the liquid and soft commodities space), expect that hike odds will continue to be priced in. Navigating the summer is going to directionally tell us if this is a massive fakeout in bonds, or if we have another, much more significant wave of inflation ahead of us (like 73)...

Technical Overview… A Ticking Risk Clock

(Continued below: ‘Technical Overview… A Ticking Risk Click, Energy Portfolio Strategy Update - In Watch & Observe Mode, Report Schedule for the Week, Portfolio Strategy Update and Commentary from Six, and more…)

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.