Weekly Macro Note: Portfolio Strategy Update and Commentary, Geopolitical Update, Oil & Gas Quick Look, Credit Spread Movement, & More

In this Weekly Macro Note we provide the latest update on MacroEdge Portfolio Strategy, discuss the latest geopolitical developments from the Middle East, highlight oil/gas futures, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers and Community,

I am writing to you on my final evening in West Texas before making my way back to the office tomorrow for a very brief week off the road. From that point on, I will be on the road for another seven weeks or so as we continue to expand our capabilities and client base across North America and beyond. On weekends like this one, I am always blown away by the size of our community, as it approaches almost 150,000 across the different platforms we utilize… I am also consistently pleased to read some of the very intelligent comments that some of you send in or share, especially on weekends like this one (when I get to sit back and watch @RealJohnGaltFla) teach us all a few things about geopolitics and the Middle East.

As part of our commitment to continue improving everything this year across the MacroEdge spectrum, one of the newer shifts you will see over the next four weeks is an earlier release time for all Macro Notes. Right now, reports are published on a somewhat random timetable, and oftentimes very late into the evening - based on feedback we’ve received from several of you - it would be much preferred to get Macro Notes before 10pm EST. We’re committed to implementing these changes and staying on top of real-time data and updates in our Macro Notes so they remain actionable on this earlier timetable. We have nearly completed our wind-down of the legacy Ozone portal that was hosted on MacroEdge.net, and there are only a handful of accounts that have yet to have been migrated off.

On the geopolitical front, things are staying very volatile for the time being. The situation in Iran and the Middle East is very fluid, and we’re monitoring shifts as they continue to come in. The primary focus this week on our end will be the impact to energy and tanker markets, respectively, and it’s also notable that bonds are catching a continued bid on the strikes. Futures have nearly erased their dip in technology equities (NQ), and at the time of this writing, WTI is up about 7%. These gaps usually quickly resolve in today’s markets - and the broader distributive charts are quite sticky right now from a range standpoint. The 10Y is also at its lowest level since April of last year:

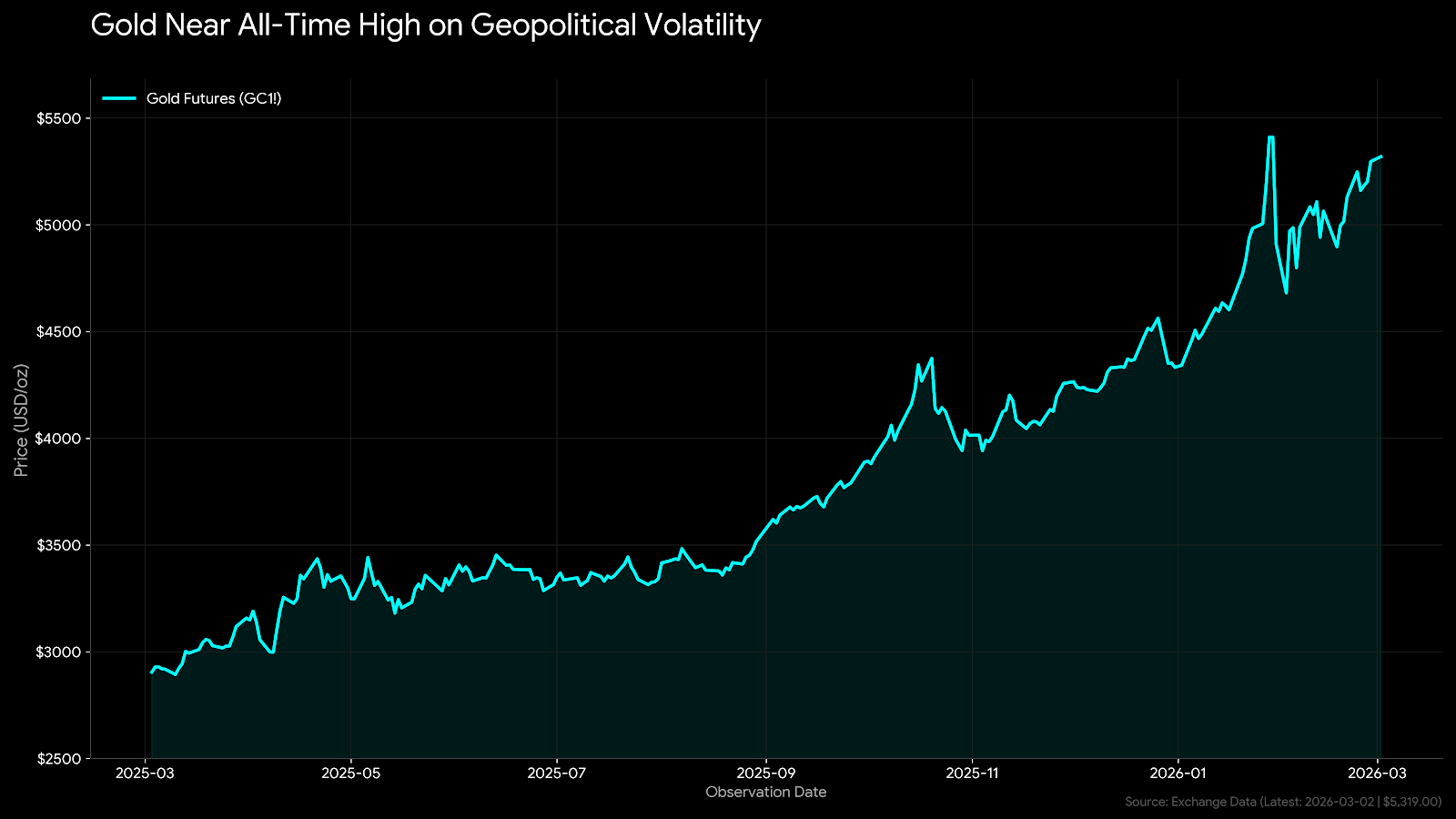

Though I expect that this could prove short lived as/if commodities continue their march higher. Gold is near an all-time high this evening:

Gasoline & Brent Futures are moving higher in the overnight hours:

This week will be very noisy with a lot of different dynamics and forces playing out at the same time - it’s hard in many cases to even know what’s real on social media, though the reality will be reflected largely in energy, bond, and commodity markets for the time being.

Don’t have MacroEdge Ozone? Get Ozone - now exclusively through Substack - below… Ozone is available to all new subscribers of MacroEdge for one week.

Macro Week Ahead

Monday: MacroEdge Job Cuts Tracker (USA), Tokyo CPI (JP), ISM Mfg PMI (USA)

Tuesday: API Crude Oil Stocks (USA)

Wednesday: ADP Employment Change (USA), ISM Services

Thursday: Trade Balance (February)... first trade report following Supreme Court ruling

Friday: NFP/Employment (February), Retail Sales

Geopolitical Update & Oil and Gas Quick Look

The next 24-48 hours will be very interesting. Oil gapped up (WTI $CL) as expected, and at the time of this update is up about 7%. This could moderate as we enter the morning hours as traders digest things like Strait of Hormuz traffic, operational expansions, or wind-downs, etc. For the time being, it appears that Iran’s (the IRGC) military capabilities (air defense, missile forces, and drones) are largely operational. Hezbollah has also gotten involved in the conflict from Lebanon, and Israel expanded strikes to include Hezbollah targets there.

(Continued below: geopolitical update & oil and gas quick look, Friday PPI Report Rundown, Credit Spreads Once Again Dancing, Portfolio Strategy Update and Commentary…)

The Iran-Israel war has hit a tipping point after the confirmed death of Supreme Leader Ayatollah Ali Khamenei in a joint U.S.-Israeli strike. This mission, named “Operation Epic Fury,” has pulled more than 15 nations into the conflict. Regional players like Jordan, Saudi Arabia, and the UAE are now actively shooting down Iranian drones and missiles. The fighting has also spilled into Europe’s backyard following a drone strike on the RAF Akrotiri base in Cyprus, which serves as a critical hub for Western military operations. Combined with the effective shutdown of the Strait of Hormuz, where 150 tankers are currently sitting idle due to IRGC threats and a total freeze in the insurance markets, 20% of the world’s oil supply (and LNG supply) is now temporarily offline.

President Trump has made it clear that while he initially suggested a four-week window, the conflict could continue well beyond that timeframe, and told the public to expect more service members to be lost. In a video address following the deaths of three U.S. service members in Kuwait, the President vowed vengeance but warned that more casualties are likely before the mission ends. He emphasized that combat operations will continue in full force until all strategic objectives are achieved, regardless of the duration. This shift in rhetoric suggests the administration is bracing for a sustained campaign rather than a short-term surgical strike.

Summarized:

Timeline and Casualties: Trump stated the operation could last four weeks or as long as it takes. He explicitly warned that more American service members will likely be lost, calling it a necessary burden for future security.

Expanded Geography: The hit on Cyprus proves that European territory is no longer safe from this escalation. Attacking a primary Western staging ground in the Mediterranean changes the stakes for the entire NATO alliance.

Maritime Blockade: The Strait of Hormuz is nearly impassable for commercial ships.

Nations Involved: Over 15 countries are now involved, as well as several Iran-backed groups in countries like Lebanon. A coalition group is focused on ballistic missile defense and trying to keep shipping lanes open while publicly condemning Iranian strikes on neighboring sovereign states.

Friday PPI Report Rundown

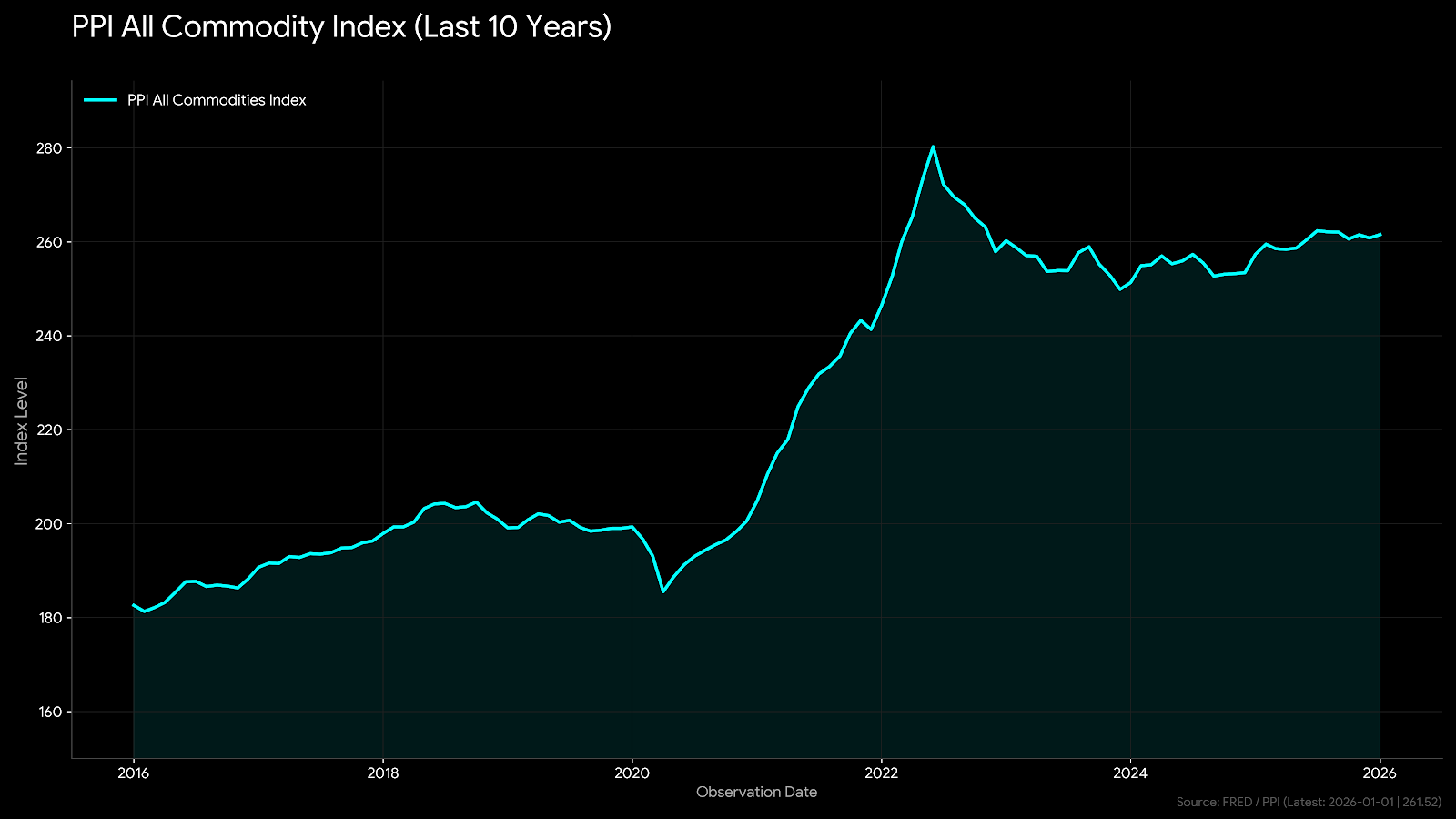

The January PPI report showed wholesale inflation rising by 0.5% for the month, which was higher than the expected 0.3% increase. While headline annual inflation was pegged to 2.9%, core PPI jumped to 3.6% and exceeded the 3.0% forecast. This surge was driven primarily by an 0.8% increase in service costs and trade margins. These numbers suggest that while energy and goods prices have dipped, underlying inflationary pressures remain stubborn in the production pipeline. This data reinforces the likelihood of the Federal Reserve maintaining its current interest rate stance in March…

The commodity index is nearing all-time highs again, so we’ll see where this goes with oil moving higher again:

Global Bubble Gauges

In terms of the global markets we track as part of our ‘global bubble’ basket, things remain at/near all-time highs and pushed higher last week. In our basket, I utilize the IBEX/Nikkei/KOSPI/TSX:

The TSX melt-up continues:

Japan (Nikkei) / Korea (KOSPI) are key correlations with the US AI bubble, and thus far have not displayed signs of cracking.

Nikkei:

While a bearish divergence has formed on the daily, Japan continues to utilize a variety of market mechanisms to propel their equities higher. The concentration risk here is very high, though until the BoJ signals easing, a weaker Yen is also helping the bubble go higher.

KOSPI… one of the wildest global market ‘melt–ups’ we’ve seen in the last two years:

The Spanish circus continues… and remains my top Nasdaq signal for the time being… when Spain breaks, US tech will be in a much worse position.

Credit Spreads Once Again Dancing

Credit spreads have widened some as bonds have also begun to move higher. With the 10Y hitting a 1-year low this evening - something to keep an eye on with geopolitical volatility and as AI/tech company CDS’ have pushed dramatically higher.

The higher this goes, the more pressure we’ll see on equity markets.

Report Sequence for the Week

This week, we will be expanding our report coverage by an additional Macro Note due to the geopolitical volatility and our coverage of all things energy sector.

Midweek Macro Note, Geopolitical Updates, & NFP Forecast (Wednesday)

Redeye Macro Note - Geopolitical Updates, NFP Review (Friday)

Equity Market Discussion (Saturday)

Weekly Macro Note (Sunday)

MacroEdge Portfolio Strategy Update - March 1, 2026 (@SixFinance, Head of Research)

“... to the great, proud people of Iran, I say tonight that the hour of your freedom is at hand. Stay sheltered. Don’t leave your home. It’s very dangerous outside. Bombs will be dropping everywhere. When we are finished, take over your government. It will be yours to take. This will be, probably, your only chance for generations. For many years, you have asked for America’s help, but you never got it. Now you have a president who is giving you what you want, so let’s see how you respond. Now is the time to seize control of your destiny and to unleash the prosperous and glorious future that is close within your reach.” - POTUS

The Iranian regime is on the ropes. The supreme leader is dead, and the command structure is fragmented. The remnants of the regime continue to launch strikes into neighboring countries and strike ships in the Strait of Hormuz. While it is unclear what the last dying breaths of the Iranian Islamic regime are going to sound like, or whether they mine the Strait, it is clear that conditions are as ripe as they are ever going to be for the Iranian people celebrating in the streets to rise up and topple the regime.

Plagued by crippling sanctions and extreme inflation, Iran’s economy could be set to boom if the leadership that comes next is cooperative with Western powers. The Vienna Institute for International Economic Studies estimated in a February 2026 study that removal of EU sanctions alone could boost long-run Iranian GDP by over 80%. Should sanctions be removed and progressive leadership be appointed, the rebuilding of Iran’s economy could become a preeminent global investment frontier for years to come, as foreign direct investment explodes, and SWIFT system re-entry allows for a stabilization of the Iranian Rial, and a moderation of inflation.

While investing directly into Iran is currently challenging for a number of reasons, there are a number of ways to position for an Iranian economic renaissance ahead of direct access. First, one Western avenue with direct exposure is Hikma Pharmaceuticals, which already has Iranian production facilities in the country. I view this exposure similarly to that of the oil services companies we highlighted that were already located and licensed in Venezuela when the Maduro operation occurred, with WFRD already appreciating by ~25% since January.

Tupras on the Turkish exchange offers another avenue, as heavier Iranian crude flows locally to the refiner. The story here would likely be significant margin expansion as proximity and sanction removals allow the refiner direct pipeline access to the heavy Iranian crude that Tupras built infrastructure around, but sanctions have brought this business to a screeching halt. Iranian heavy crude flowing to Tupras would be an instant boon to Tupras.

As we wait for the dust to settle in this regional conflict and continue to hold long positions in US domestic oil E&P’s, with oil obviously expected to gap higher, the next trade here is far more structural and long duration. If regime change does occur, and new leadership is Western-aligned, it will be the beginning of a structural bull market in Iran.

ORCL

As I press software longs interested in a squeeze of lopsided positioning, the new developments between the US Government and Anthropic (whose new product headlines have been immediate catalysts for downward re-rating across software and other sectors for weeks) creates asymmetry for Oracle. As Oracle has sold off since its OpenAI forward revenue guidance, and its software designation surely adds to selling pressure, catalysts align for a substantial tactical reversal. As OpenAI is the dominant counterparty risk in Oracle’s levered bet on AI infrastructure, a pivot from the Department of War from Anthropic to OpenAI is a huge catalyst for selling relief in the name.

When the government announced all use of Anthropic must stop, and Anthropic will be designated a supply-chain risk(unprecedented for US firms), we can also assume that a deal between OpenAI and the government implies that OpenAI systems, when heavily integrated into US government workflows, will now be critical military infrastructure. While the long term LLM winner remains unclear, the military making OpenAI their primary vendor tells the market that Oracle’s infrastructure buildout, admittedly in a very roundabout way, is now de-facto military infrastructure, shifting the risk profile. While I question Oracle’s strategy on a long term basis, recent newsflow necessitates a tactical long in ORCL in my view, and I plan to add both common shares and call spreads.

For more details, please refer to our Terms and Conditions.