Weekly Macro Note: Oil Market Update - A 'WTF' Weekend, Ignoring Headlines, On the Ground Part 2.2

In this Weekly Macro Note - we provide an oil market update after the "WTF" weekend as it pertains to headlines and 'deals', we discuss why trusting the technicals & fundmentals matters, and much more

Don Johnson (@DonMiami3), Chief Economist

Good Monday evening MacroEdge Readers & Community,

I hope you all have had a fantastic long weekend and Memorial Day. It certainly went by quickly, and this marks the end of my tenure in Texas after three weeks on the road in the Lone Star State. In the coming weeks, we will be making several key announcements regarding adjustments to our current base of operations, and I look forward to sharing these with you. I am a strong advocate for creating an environment that is conducive to broad success within our organization, down to the individual level, and we are adjusting to continue to meet that vision not only for the remainder of the year, but for years to come.

On the weekend headline front - Saturday and Sunday were packed with ‘trash’ headlines from the usual suspects. We are now shifting into a fundamental & technical only outlook with this noise, so these headlines - unless actually verified beyond the ‘source’ level - are going to get covered for the time being. On Saturday and Sunday, we heard of ‘deals’, ‘progress on deals’, ‘incredible deal’, all with no context and being sourced frequently from anonymous texts through Arabic news media outlets. When and if there’s actually a ‘deal’ - which has not yet happened - the Administration will be going on a grand parade of said deal - and we have seen none of that. While conflict restraint is in force, given the collapsing oil inventories in the US & abroad (US - domestic -1mmbpd drawdown), we’re going to see this jawboning continue during the war, given how effective it’s been to this point. I do expect that advisors are becoming more alarmed with the fact that we’re now through Memorial Day and heading into peak driving season with inventories plummeting across the board - but the strikes this evening show that they’re attempting to play both sides of the coin without letting front-month oil and gas get beyond their comfort levels… This also has to do with the bond market, as well, which staunchly rejected the war last week. I expect that the Administration will continue to be driven by rates & oil prices now, and inflation is going to run hot as long as the Strait remains closed (which is at least through June given announcements from the ‘sources’ today). I have a hard time saying that Iran is in a rush to give up their two major negotiation levers, being Hormuz & uranium, even if the Chinese are more heavily involved in the discussion now.

Futures are opening the short week to the upside in equities - with the Nasdaq up about .9% - and green across the board. This is largely due to the decline in price of crude, which is down about 4.9% at the time of this writing. The move off of the headline ‘sources’ has created a large downside gap above the $96 spot level. On Thursday, we will get the next EIA report, which is expected to show another large decline, though down w/w in terms of magnitude (last week was the largest inventory decline on record). Yields will start the week down slightly - and as reiterated many times - bonds and oil will be the driver of most (if not almost all) magical headlines for the foreseeable future. It’s actually net advantageous for the Administration that no deal gets made until we get an actual product shortage in crude/gasoline/distillates, which is extremely unlikely. They still have about another month to dilly dally around with the negotiation, and by July, I expect things to get considerably more serious if no final deal has been displayed or announced.

Not yet a MacroEdge subscriber? Upgrade below and get all of our research, data, portfolio strategy, and much more below:

Macro Week Ahead

This week is a short week. Continue to monitor WTI/yields & semiconductor/data center equities.

Tuesday:

9:00 AM ET: S&P CoreLogic Case-Shiller Home Price Index (March)

10:00 AM ET: Conference Board Consumer Confidence (May)

10:30 AM ET: Dallas Fed Manufacturing Survey (May)

Wednesday:

7:00 AM ET: MBA Mortgage Applications (Weekly)

10:00 AM ET: Richmond Fed Manufacturing Index (May)

Thursday:

8:30 AM ET: Core PCE Price Index (April) [Fed Preferred Inflation Gauge]

8:30 AM ET: Gross Domestic Product, Second Estimate (Q1 2026)

8:30 AM ET: Initial Jobless Claims (Weekly)

8:30 AM ET: Durable Goods Orders (April)

10:00 AM ET: New Home Sales (April)

Friday:

8:30 AM ET: Advance Wholesale and Retail Inventories (April)

9:45 AM ET: Chicago PMI (May)

This week, Costco and Salesforce are reporting as ‘notable’ earnings with mega-cap size.

‘On the Ground’ Research Part 2.2 - Another Discussion in the High Plains

The winter wheat harvest across the Texas High Plains is shaping up to be one of the most volatile and unusual seasons in modern agricultural history. To understand the dual pressures of severe domestic weather and unprecedented international geopolitical conflict, we sat down for an in-depth conversation with an ag-economist. This individual has been navigating ag cycles for longer than many of us have been alive. The following is a comprehensive synopsis of this discussion as of May 15, 2026 - focusing again on the wheat sector in our wheat, corn, and fertilizer deep-dive. Part 2.2 will be followed by Part 2.3 this week. Given commodity volatility due to the weekend announcements, we will continue to make any adjustments to our report schedule as needed.

The Ground Reality: A Devastated Dryland Crop

“If you drive through the Panhandle right now, the visual contrast is staggering,” the economist notes. “We are looking at a fundamentally broken winter wheat crop on the dryland side, while the irrigated acres are essentially acting as a life support system for the regional supply.”

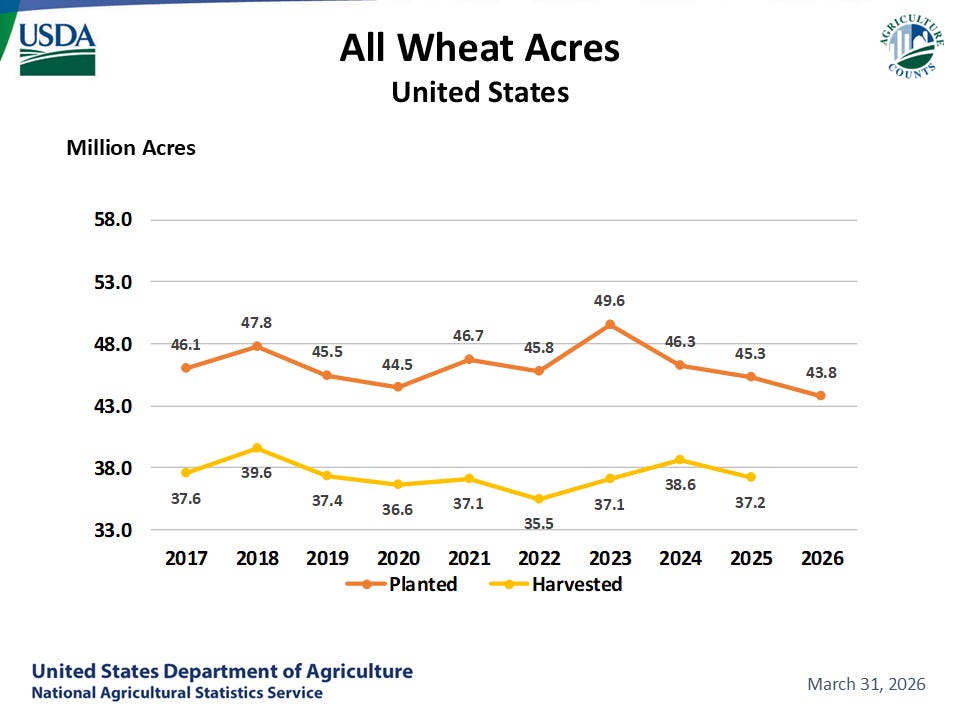

The localized crisis aligns directly with the sobering figures released in the May 12, 2026, USDA World Agricultural Supply and Demand Estimates (WASDE) report. The federal data confirms that the United States is facing its smallest winter wheat crop since 1965, with total production projected to collapse by 25 percent, down to just 1.048 billion bushels.

(WASDE - USDA)

Current wheat futures:

Down slightly from the cycle highs - but not nearly as much as CL/RB - reflecting the tightness we’re seeing in the data.

(Continued below: On the Ground Part 2.2 Continued, Oil Market Update - a ‘WTF’ weekend, War and Geopolitical Update, Report Schedule for the Week, Warsh/Rinse/Repeat - John Galt Note)

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.