Weekly Macro Note: Notes from Amarillo, Another 'No Deal' Sunday, a Crude Update

In this brief Weekly Macro Note - we discuss our recent 'On the Ground' developments from the High Plains, talk about another 'No Deal' Sunday, and provide an update on crude + gasoline...

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

It’s very late as I write this from the High Plains. Texas has treated both myself and Six thus far, and we’re excited to share much more over the course of the week with Part 1 of our agriculture data in our ‘On the Ground’ report. Monday evening (tonight) - we’re going to be releasing Part 1 of this extensive series - and we’re going to be focusing on the opportunity as we see it from a portfolio strategy standpoint. This leads into our broader launch of our portfolio strategy infrastructure come June and July, and we continue to focus on macro-intensive strategies that the mainstream is staying away from. As retail and speculators continue to pile into a more and more extremely concentrated asset bubble - which I call the ‘crash up’ - I continue to place high emphasis on seeking out assets that avoid this concentration risk - and we’ve been doing just that since the beginning of the year while continuing to put up strong performance figures.

Without a slowdown in our Global Bubble Index, this crash-up is one that is not one I have any interest in fading - especially during wartime posturing in a midterm election year with an Administration that cares most about nominal assets appreciating above all else. While again, we could go into the blatant and appalling examples of manipulation in oil markets the past several weeks - the jawboning is going to continue - so I’d rather position and profit (while calling it out) versus just calling it out and complaining online. The physical reality of the Hormuz closure is one that I still expect is going to catch up with the world in a major way, and taking off between 20-40% of critical commodities markets is not something that can be printed or papered over as we run down emergency reserves globally in oil markets, Asian countries warn of food shortages, and other critical materials and inputs are going to get increasingly more scarce as we head into the summer months. Oil at $100/bbl WTI spot this evening is a comfortable spot for companies in our portfolio strategy basket to continue enjoying, though the volatility and price action continues to be rather violent in this range. It’s tough to want to drill more, though I do think activity is going to increase, with this kind of rhetoric against oil prices to begin with.

Outside of that, equity prices are continuing to advance higher, with Korea entering a full-on parabolic move to the upside, Spain not showing signs of slowing, and NQ/ES relatively flat but now slightly up in the late evening hours. The music continues to play - but when the tunes finally slow - it’s not a party that I would want to stand at for long - hence why I am not playing in those ‘sexy & flashy’ baskets to begin with. One of the most effective strategies that I learned from a mentor several years ago was that we play our best ball when we bat knowing our own strikezone - and for me that might be different than Six - and for you, it’s probably different too. This week is going to be relatively light on the macro data side of things - though pay close attention to that April CPI reading. Some well respected analysts that I follow are forecasting prints as high as the low 4s, which likely shifts Fed policy even further after the latest employment data. I know we’re not diving into the employment data tonight - but with the On the Ground Report Part #1 coming tomorrow night, we will discuss the April employment data later in the week. Lastly, with cryptocurrencies (many of the ones that matter) retesting their 200dma’s or close, we’re likely at a turning point that warrants monitoring for the broader risk environment.

With that being said, it’s nice to be back, and I look forward to sharing many interesting findings with you all over the next week on the ag front.

Not yet a MacroEdge Ozone subscriber? Get access to all of our research, data, portfolio strategy, and much more below:

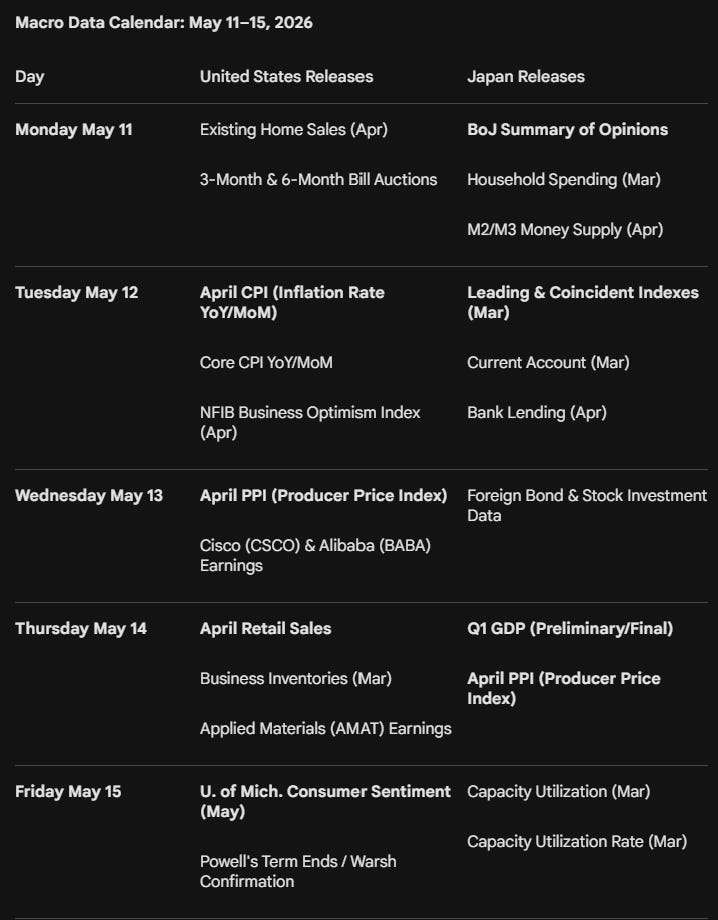

Macro Week Ahead

In the macro week ahead, we look to CPI and the end of the Powell term. While it’s unlikely that Powell cedes a position in the Fed, this final print will likely leave yet another stain on a term that was a complete and utter failure for the Fed’s stable prices mandate. Even in adjusted terms, Powell oversaw some of the worst inflation the US has ever seen, massive balance sheet expansion, etc… the list really goes on and on.

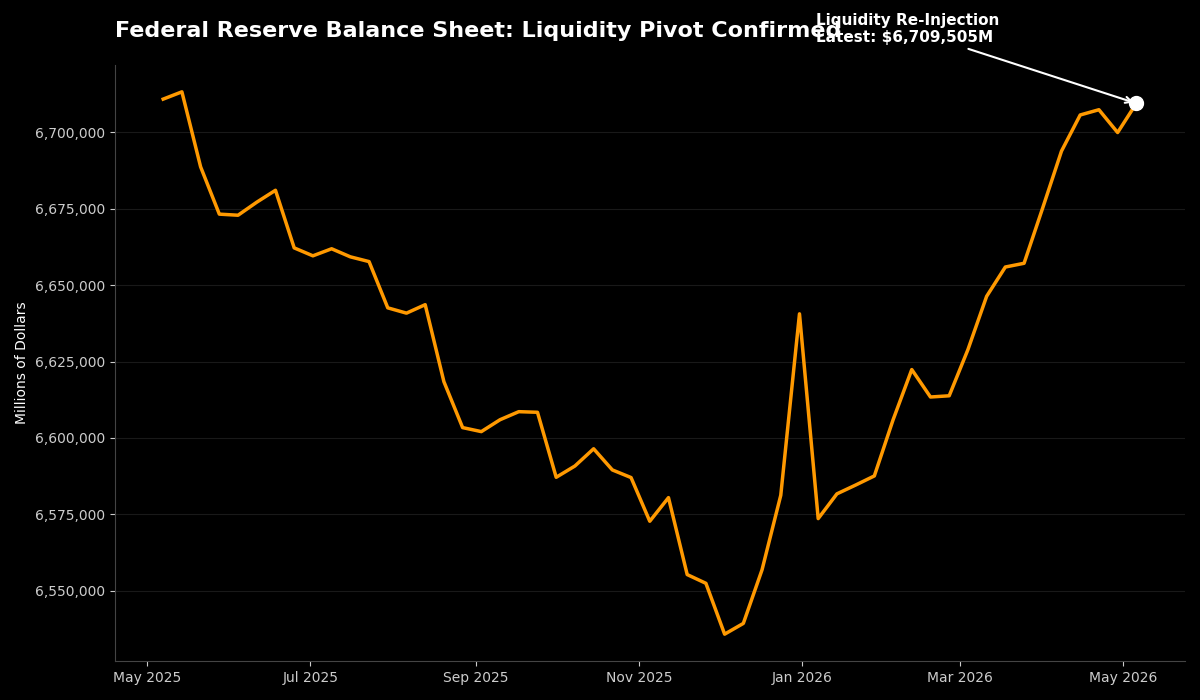

Something to keep an eye out for… the resumed expansion of the Fed balance sheet into a new Warsh term - who I do not think will be much of a ‘hawk’ at all…:

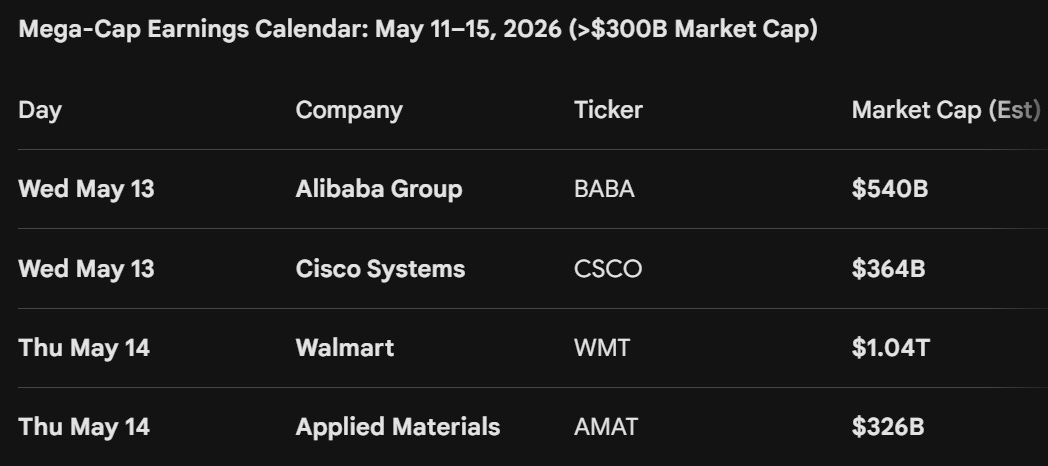

For earnings this week >300bn market cap:

Notes from Amarillo

Thus far, my time in Amarillo has been fruitful - and most of all interesting. We’ve had discussions with experts and business owners from across the ag-sphere the past few days, and the general consensus is that commodity prices for wheat and corn are not reflecting the coming upside price risk from a multitude of factors that are all currently swirling into a ‘perfect storm’ for higher prices… As the Strait remains closed, critical fertilizer exports remain greatly strained - and these markets are global, just as the oil markets are. While natural gas prices remain low in the United States, the same cannot be said for Europe & North America.

Corn & wheat - the primary focus for this trip - remain near the local low:

Wheat:

Tomorrow I will have more stories from my discussions, and photos, and I truly hope you enjoy the start to this new series.

Another ‘No Deal’ Sunday

The rejection of the latest ceasefire and de-escalation proposal from Iran marks a definitive pivot toward a “long-war” scenario for global energy markets. With the Strait of Hormuz now effectively closed for over 60 days, the market is moving out of the “temporary shock” phase and into a period of severe structural deficit as lag impacts begin to hit physical supply chains.

Below: The Breakdown of Negotiations (yet again…), A Crude Update, Gasoline Price Trends, and what’s next…