Weekly Macro Note: Nominal 'Crash Up' Continues, Physical Shortage Countdown, A Refreshed Look at Data Centers, Portfolio Strategy and Commentary

In this Weekly Macro Note we discuss the nominal crash up in assets continuing, a countdown to physical shortages as inventories of critical commodities continue to tighten, and more... #MacroEdge

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers and Community,

We’re continuing to spool things up after a packed week last week put us behind on the report front. There’s not a lot of information to report from last night to this evening, other than we’re going to hear from the President tomorrow on another potential Iran proposal being discussed. For the time being, it doesn’t look like it’s going to be much, though we’ll have to wait and actually watch the Strait of Hormuz data as it continues to come in. There’s been no change to tanker or ship traffic over the past 24 hours, and the situation continues to result in an accumulating shortage of critical commodities across the board. From oil to distillates, fertilizer, urea, crops, and more - this accumulation is only building and will operate with a lag, which is something that we outlined yesterday evening. Underlying price pressures continue to mount - and gauges like prices paid are going to continue to move higher. Barak had another fake headline from tonight - talking about some ‘concessions’ package which will be addressed by the President from the Situation Room tomorrow. Anything posted from that ‘source’ should be taken with a grain of salt, as it continues to look more likely that the US is likely to strike when Iran gives up ground or falls asleep.

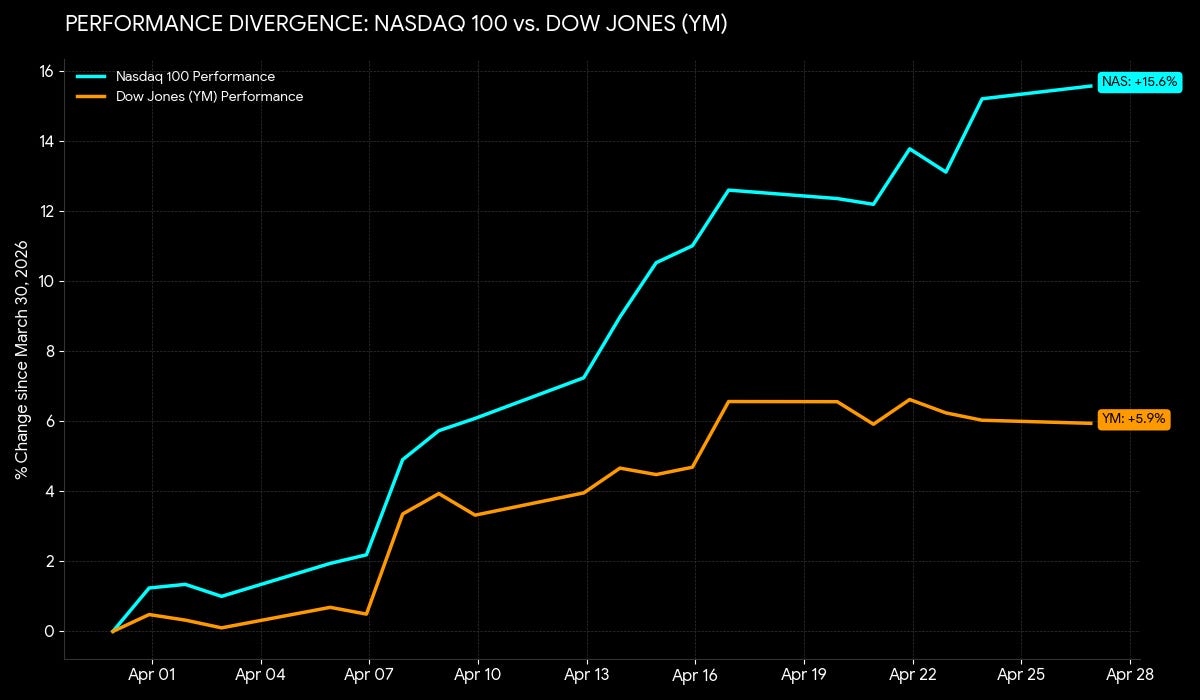

The Administration continues to lean into boosting nominal asset prices - and the climb that we’re seeing now is something out of 99, the KOSPI of a few months ago, and Japan in the late 80s. These unprecedented times are causing us to run out of instances and comparisons - and the rate at which things are climbing continues to accelerate. There are a lot of explanations being offered for why equity markets have essentially shifted to the ‘vertical only’ move, with the Nasdaq rising over 20% in a matter of weeks, and semiconductors over 40% MTD - a move only rivaled by 2000. The simplest explanation is that we continue to find ourselves in one of the most pro nominal asset price regimes that we’ve ever seen, which is unlikely to end until the Strait of Hormuz situation actually begins to cause demand destruction (if at all during the ‘big print’). For the time being, we have the Treasury close to a form of YCC to control the 10-30Y yields, and I do not think that Warsh is going to be hawkish in any way, shape, or form.

Next up… airline bailouts! We’ll have more on this later in the week as Frontier, Avelo, and Spirit are now requesting to be nationalized.

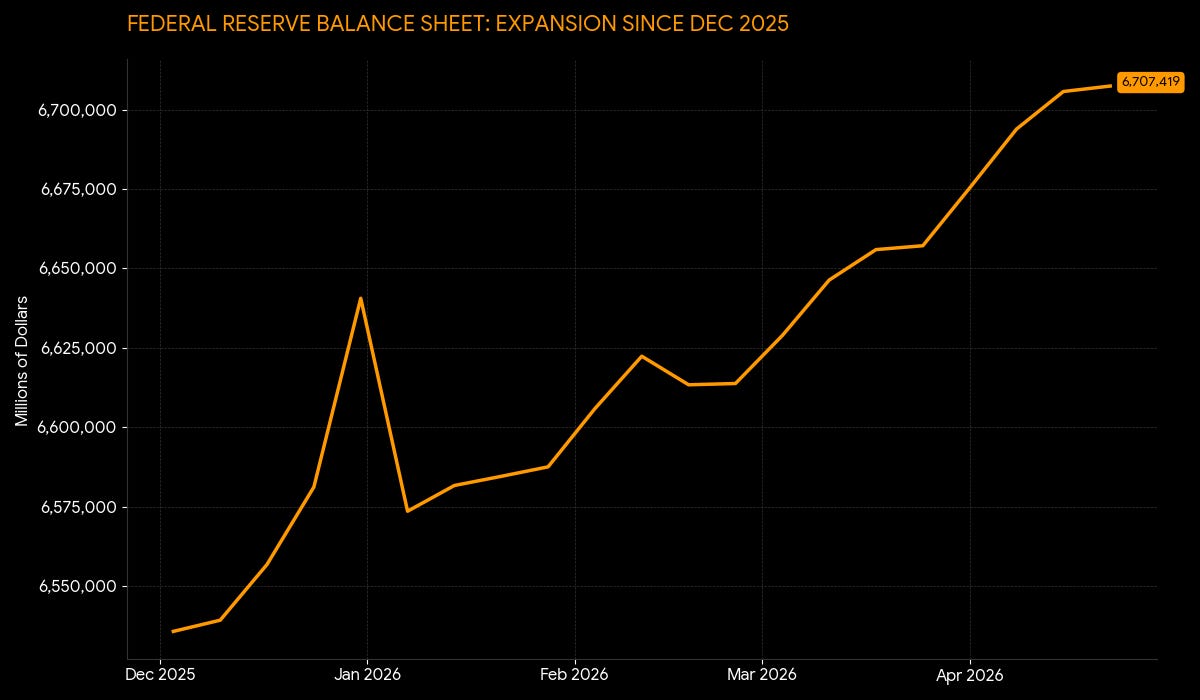

Just look at the current expansion of the balance sheet since December, even as the Fed failed to hit its 2.0% CPI mandated target. Inflation is now moving higher, and no one seems to care as nominal asset and price levels continue to ‘crash up’.

This situation is creating a perceived ‘mirage’ - as most individual investors (of which now there are more than there ever have been) assume that rising nominal asset prices are an inherently positive thing. In the case of a crisis in countries throughout history, we’ve seen retail investors pile into equities as a sign of panic over things like inflation, economic calamity - you name it, and the list goes on. While assets are indeed the place to shield one’s wealth and value from destruction by those spending and printing the currency, positive is not a word that I would always apply to the situation. Instances like the below are hardly wealth creation signals:

I noted on X that I continue to seek out real income-producing assets in lieu of high beta technology speculation, and I will let the speculators continue to seek out those opportunities in exchange for owning the real underlying assets and companies - especially those in niche sectors that we’re all reliant on in this ‘era of scarcity’ for commodities, etc. I mentioned this on X today, and it’s a theme that I strongly believe in over the next 5-10 years.

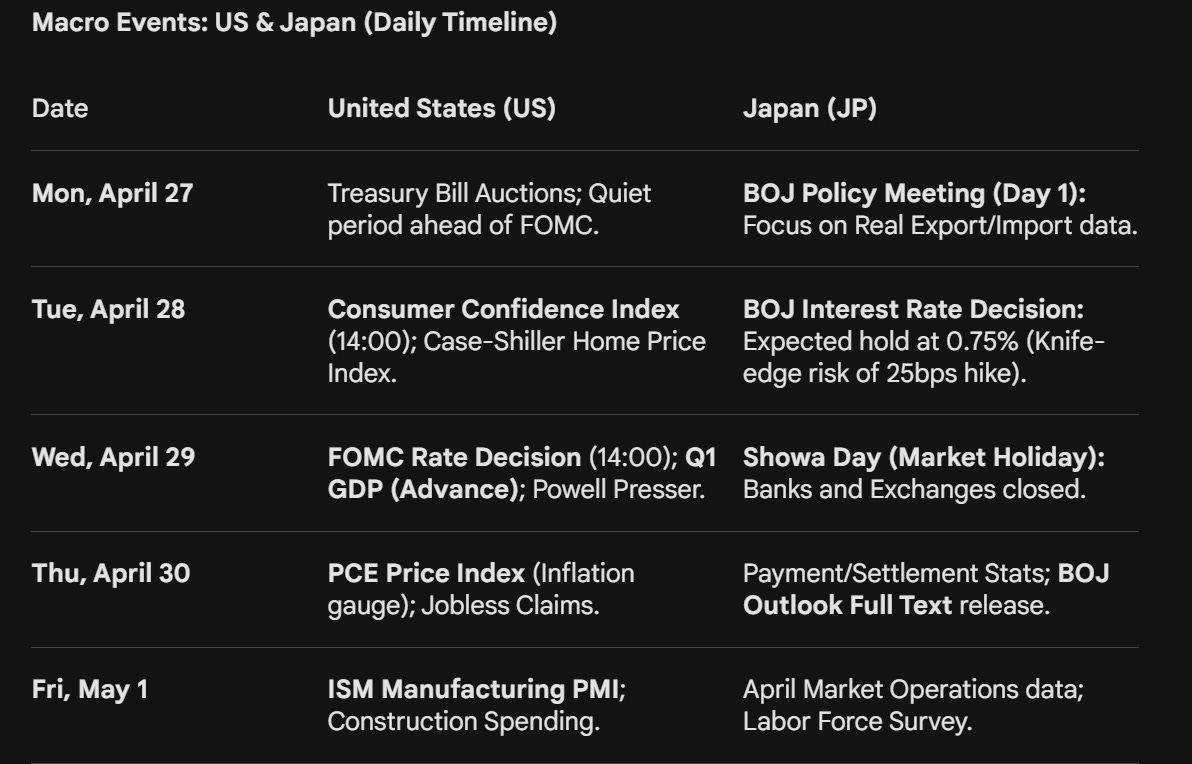

This evening we are going to dive into the futures preview for the week, which has started off relatively quietly, highlight the FOMC outlook, discuss the physical shortage countdown from the Strait of Hormuz, take a refreshed look at the data center bubble, and highlight notable macro data from the past week. We wrap up with our report schedule for the week - and if you’re not yet a MacroEdge Ozone subscriber, you can get all of our research, data, reports, and more below:

Futures Preview & FOMC Week Ahead

Futures are mostly green, with the Nasdaq leading, and the Dow lagging. The Nasdaq and Dow divergence is starting to become more noticeable - especially with the Transports & other sectors like real estate starting to lag the broader move in high-beta. Either the Industrials start to catch up, or this disconnect will widen and then correct in a violent way.

The events of the week:

On the FOMC front, it appears very unlikely that the Fed will reduce rates, with odds near zero. We’ll look for any signs of a hawkish pivot this week - but with the balance sheet expansion already underway, expect Powell to say something along the lines of ‘wait and see’ again. In Japan, we’re awaiting the next hike - though Bessent is clearly encouraging them to keep the Yen weak to allow global equity indices to continue surging through cheap borrowing of the yen.

… If anything, the Fed should be hiking right now, but we know that is not going to happen with the broader backdrop.

Not yet a MacroEdge Ozone subscriber? Upgrade below for the busy week ahead.

(Continued below → Physical Shortage Countdown, A Refreshed Look at the Data Center Bubble,

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.