Weekly Macro Note: No Rate Cut This Month, Japan Yields Surge, Record Cold Forecast for the South, Portfolio Strategy Update, and More

In this Weekly Macro Note - we discuss the low odds for a Fed rate cut this month, talk about record cold temperatures that may impact the South, provide a portfolio strategy update, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Monday evening MacroEdge Readers & Community,

Hopefully you have had a fantastic long weekend; it certainly went by quickly. As mentioned in our Saturday Redeye Macro Note, I am gearing up for a very travel-intensive MacroEdge work tour - putting me on the road for almost two months straight. On Thursday, I’ll be making my way over to Arizona, and we’ll be in Utah with a client for the weekend - then quickly turning around and going across the world for a major conference. I am excited to share some of these on the road moments, and if you follow me on X - there will be no shortage of travel photos or food that I will share in our Social Club on X. If you don’t yet subscribe to MacroEdge Ozone - you can now do so through Substack as we move our Ozone membership infrastructure fully to this platform. For the time being, it streamlines things, and make sure to catch our portfolio strategy notes from the last two reports - covering our core Ozone objectives for 2026:

Given that there haven’t been many developments since the Redeye Macro Note - I am keeping this Weekly Macro Note condensed to five key areas of focus: our usual ‘macro week ahead’, discuss the rate cut odds for the month being near zero, talk about the latest on Japan, highlight the potential for record cold to impact next weekend, and talk about the technical stall for technology & many of the 2025 leaders. Six will add portfolio color and commentary. There’s very little reason to expect cut odds to improve from current levels - barring an outlier PCE print this week. Geopolitical tensions are causing metals to rise further on additional tariff threats - and EU members have deployed several hundred troops to Greenland over the last several days. The Administration has been unable to break oil any lower from its current range - and this level has held for almost a year now.

As the distributive pattern continues in technology (+MAGS) and other leaders from 2025, we continue to wait for a macro trigger that may send them lower. For the time being, much of the fear - geopolitical, FX, inflation, employment, etc, has gone into assets, rather than out of assets. This is why we haven’t seen any broad correction drawdown anywhere. Couple that with intervention into the cyclicals like homebuilders and trucking, and we’ve seen some supportive moves in those key macro sectors from an employment standpoint.

Let’s dive in.

Macro Week Ahead

Tuesday: Weekly ADP Employment Change

Wednesday: Pending Home Sales (Dec), Construction Spending

Thursday: US GDP Growth Rate*, PCE November, Personal Income & Spending (Nov)

Friday: Japan Inflation Rate, US MoM Consumer Sentiment (Prelim)

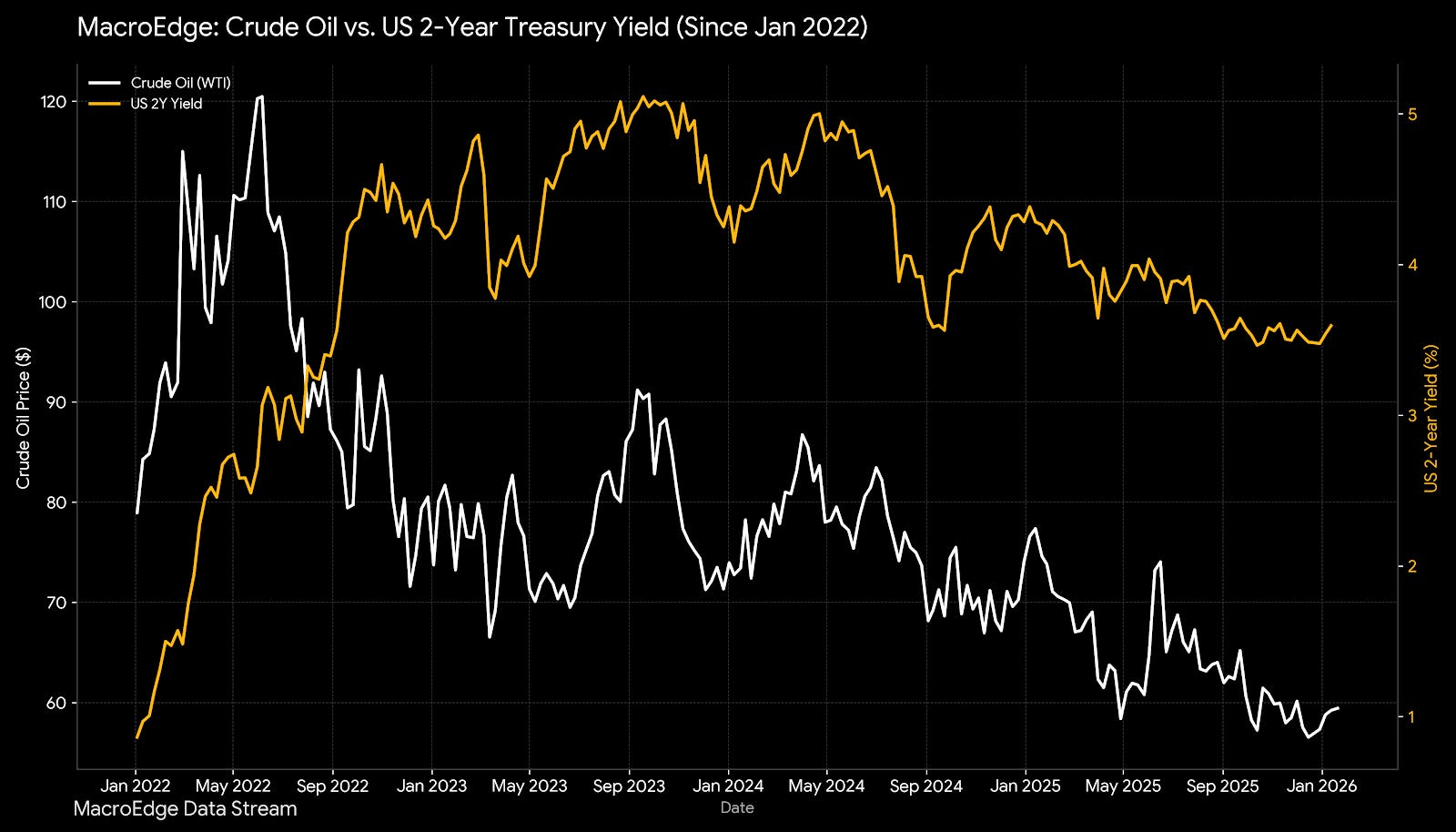

No Rate Cut This Month… & Why

As we started discussing in November/December, yields have not gone any lower - even though the fiscal side ramped up attempts to get them lower. The Greenland spat, talks about deficit reduction, etc - have the early legions of bond vigilantes finally arrived? Even oil has held the key $50-$54/bbl level since the spring tariff tantrum:

Continued below: (No Rate Cut This Month, Japan Yields Surge, Record Cold Forecast for the South, Portfoluo Strategy Update, and More)

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.