Weekly Macro Note: Macro Week Ahead, Crypto in Review Pt. 2, Bank of Japan Decision Review, Gold/Silver, & More

In this Weekly Macro Note -

(@DonMiami3, MacroEdge Chief Economist)

Good Sunday evening MacroEdge Readers & Community,

This evening we’re going to cover everything from the Macro Week Ahead, to a crypto in review part 2, discuss the Bank of Japan discussion, 3 technical charts, and more. As the constant debate continues to rage amongst our own team internally, and externally if we’re looking at a situation like 00, Hoover, or late 80s Japan when it comes to market action - it’s the constant questioning and refining of our processes that only enhances our own decision making and delivery to MacroEdge readers & clients across the globe.

In bubbles - that we find ourselves in - we increasingly see the trumpets get louder amongst the crowd that shifts their status rather quickly from ‘amateur’ to finding the need to post their portfolio screenshots on X/Instagram/Facebook, wherever they see fit. With the Onlyfans accounts now jumping into the options advice mix, I can say that I haven’t seen a bubble like this since 2000 from an equity/financial markets standpoint - and while real estate was undoubtedly crazy prior to the GFC when loans were being written for anything with a pulse - this is comparably insane. How long insane continues is something that becomes harder to quantify as the trumpets get louder & louder, though we can try to find signal from the noise through data - even in a complex and permanently shifted post-pandemic macro landscape.

Concentration risk is very high right now, and even though those playing left tail strategies (hello Universa and others) are navigating a more challenging low-vol landscape - this can shift on a moments notice - even in a world of ever-rising price levels, a Fed failure to hit it’s 2% mandated CPI target, and third-world like desires to prop asset prices up at the expense of the 80-90%. In markets like these, the drawdowns become quicker and more violent, and the bubbles they inflate through interventions do too…

Institutional Research and Ozone

On October 1st, we’ll be launching the first signup access for MacroEdge Institutional Research - our all-in-one suite for decision makers designed to put you in the driver’s seat for intelligent decision-making, portfolio strategy/construction, and so much more. Combining our cutting-edge data, critical domestic and international macro data, and our team’s efforts and internal portfolio strategies are about to unlock so much more for MacroEdge.

MacroEdge Institutional will become our flagship Macro Research division, delivering deep, actionable macroeconomic intelligence and data for investors, funds, CIOs, and executives who need conviction ahead of the market. Institutional reports cut through consensus, combining proprietary datasets with scenario modeling to frame risk and opportunity in real time. The MacroEdge IR Dashboard arms you with critical data, signals, and commentary to cut through a noisier-than-ever world.

MacroEdge Ozone will take a new role as our introductory MacroEdge offering - continuing in the same cadence, with limited dashboard access, reports and more. You can access Ozone below for 7-days below, and navigate the remainder of 2025 with success:

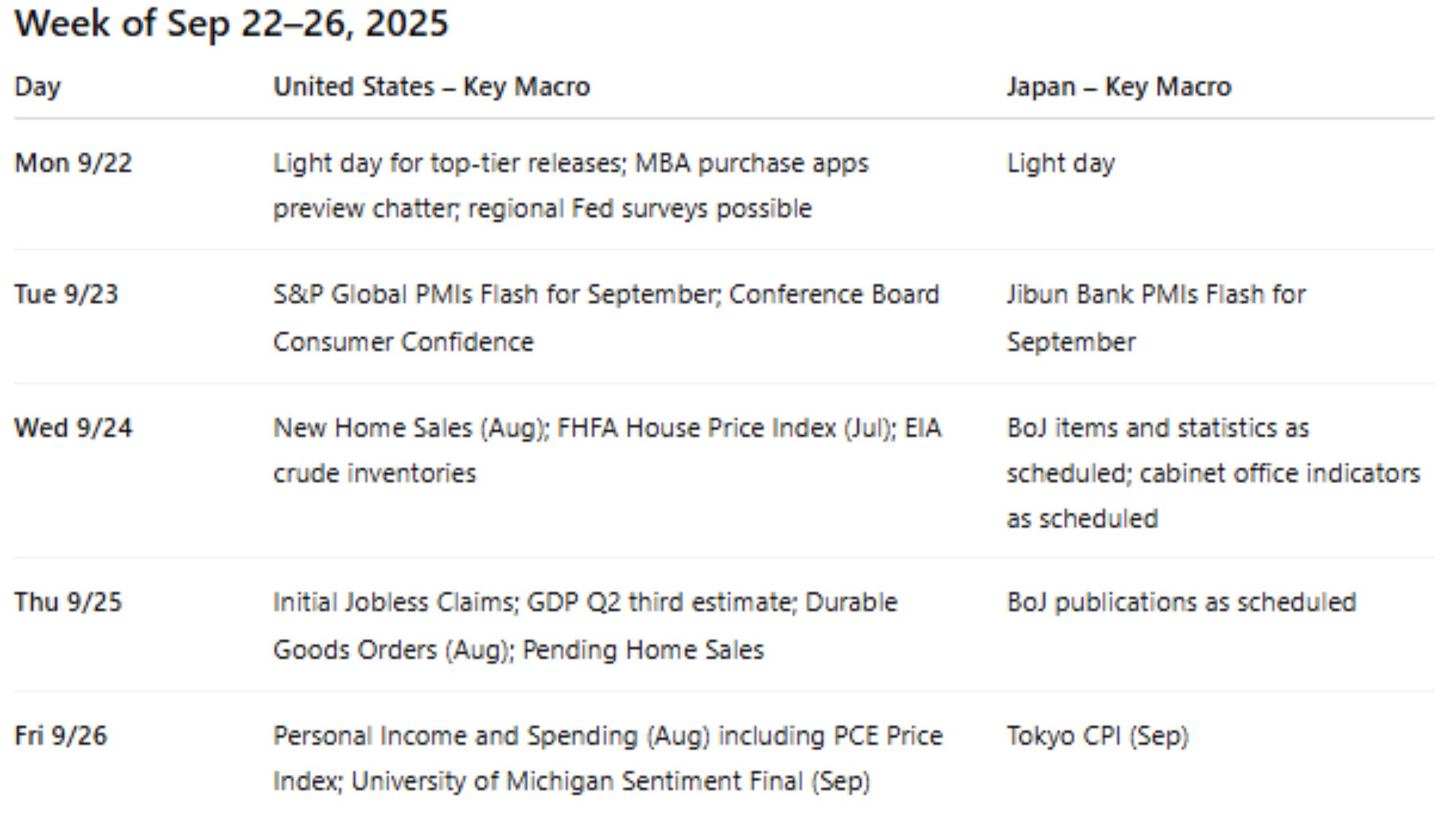

Macro Week Ahead

There are rising odds of a government shutdown (short-term odds currently sitting about 70%) and it could be a way for Schumer’s Senate coalition to stick it to the Trump Admin before midterms. This should have relatively little impact on the broader macro picture, though don’t rule out a 24-48 shutdown for political points before a deal is reached.

For earnings - Costco, Micron, and Accenture are our greater >100bn market cap names that will be reporting.

Crypto in Review Pt. 2

For Bitcoin - we noted in our Redeye Macro Note that historical warning signs in crypto are starting to fire - and we’re making those findings armed with some of the industry's newest and best live data around.

From a technical perspective - the resolution of this wedge would bring significant downside for the entire crypto sphere, and signals more robust financial conditions tightening ahead, barring any new market interventions.

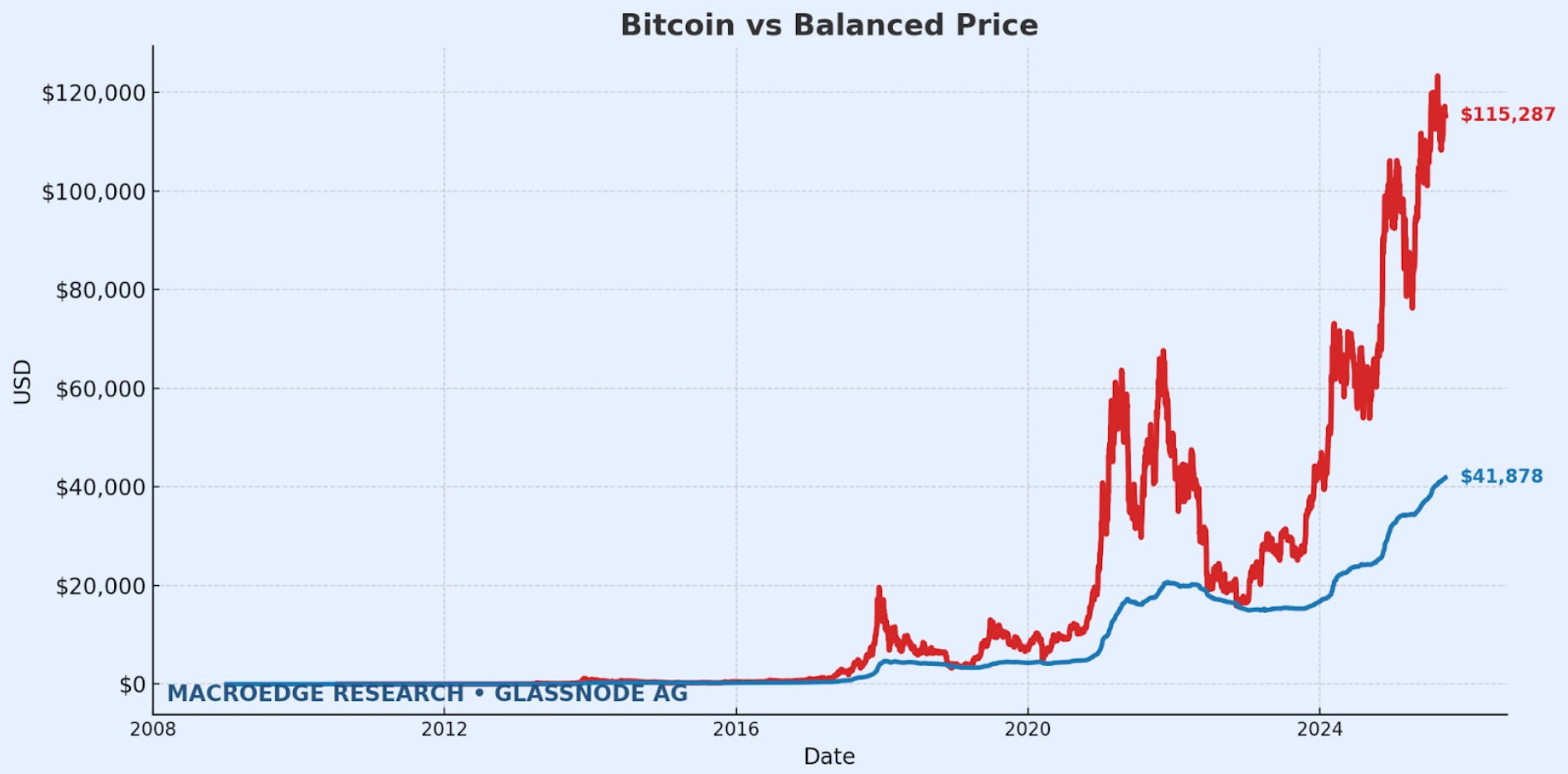

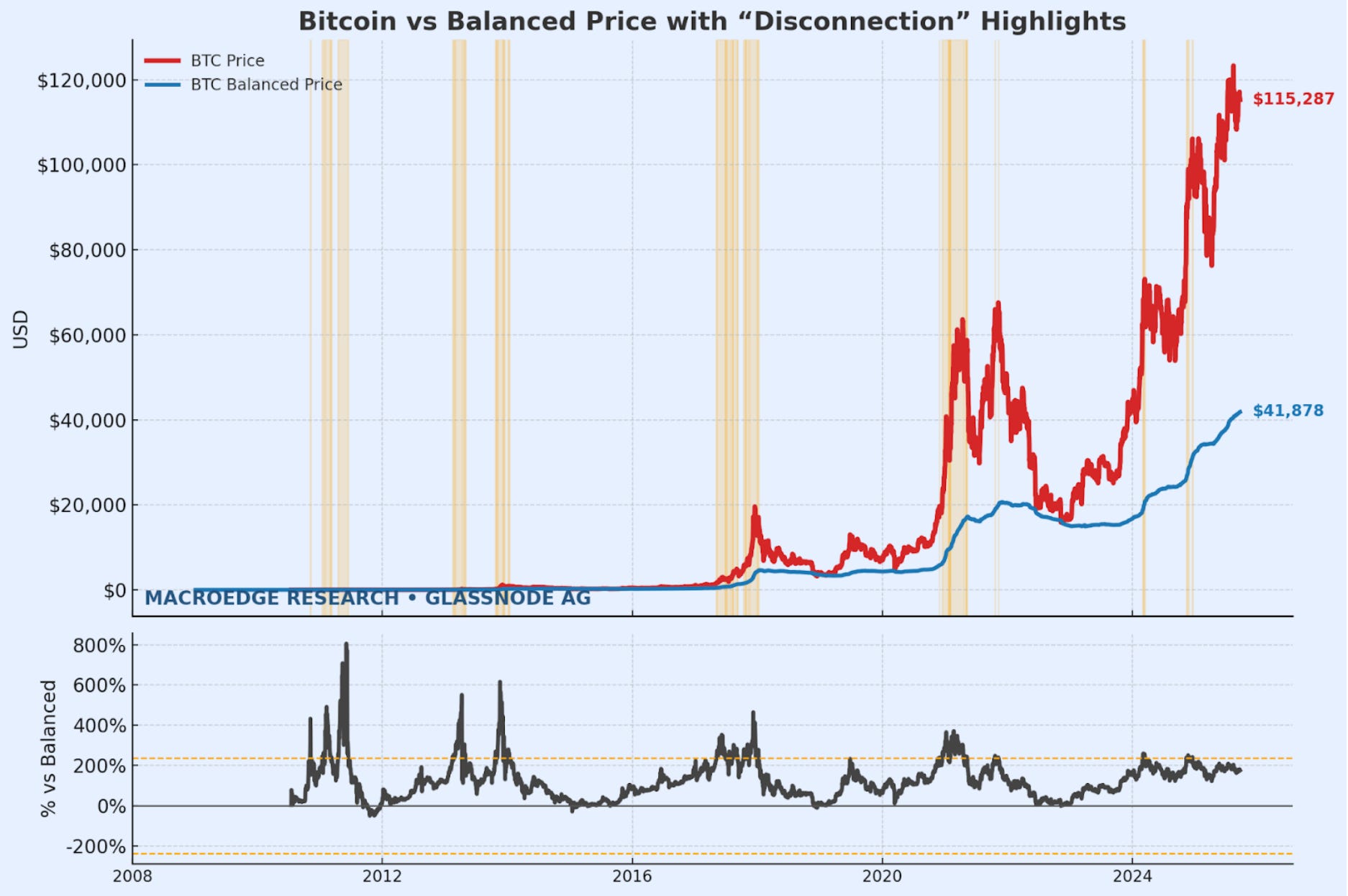

In our data deep dive from last evening - another interesting metric that caught my eye, Bitcoin v it’s balanced price:

&

Balanced Price is a Glassnode construct that blends realized cost bases to approximate the market’s “fair value” anchor for Bitcoin. It acts like gravity in the cycle: extended moves away from it often revert, while retests mark areas where risk-reward tends to improve.

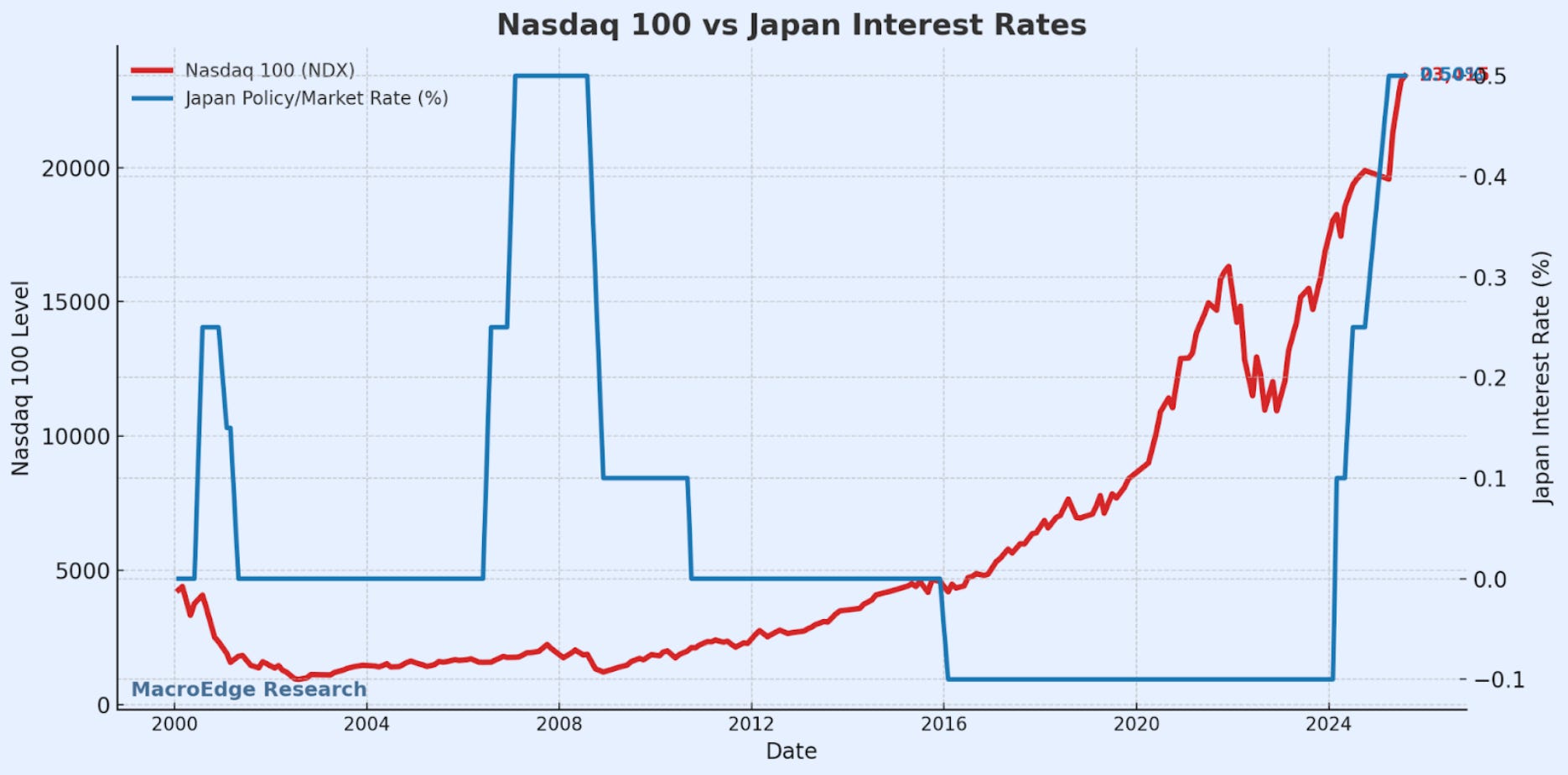

Bank of Japan Decision Review

The Bank of Japan kept its short-term policy rate unchanged at 0.5 percent, signaling patience as inflation runs above target. The board did announce it will begin reducing its balance sheet by selling portions of its ETF and REIT holdings, a clear signal that the era of unrestrained stimulus is being dismantled. Two members dissented, arguing for a hike to 0.75 percent, underscoring a rising internal divide and a willingness to press the case for earlier tightening.

This meeting reads as a hawkish hold. The rate is steady, but the balance sheet decision points toward a shift in posture. BOJ is telling markets it will not keep financing distortions forever. If wage growth and inflation stabilize, the pressure from dissenting voices will grow stronger. Investors should treat this as a turning point, where the risks are no longer about easing too slowly but about tightening too late.

… when Japan gets to cutting, it’s usually a bad signal for the world economy… and US markets - ie: NDX

Technical Tightropes

While general sentiment continues to be violently one-sided (one Schwab survey from an event this weekend noted respondents at >83% to be between ‘bullish to very bullish’) as discussed last night - things continue to look like they’re setting up for more volatility through the remainder of the year.

This upper trend line’s last shot to stop a ‘Caracas Crash-up’

The DAX has failed to go anywhere since March:

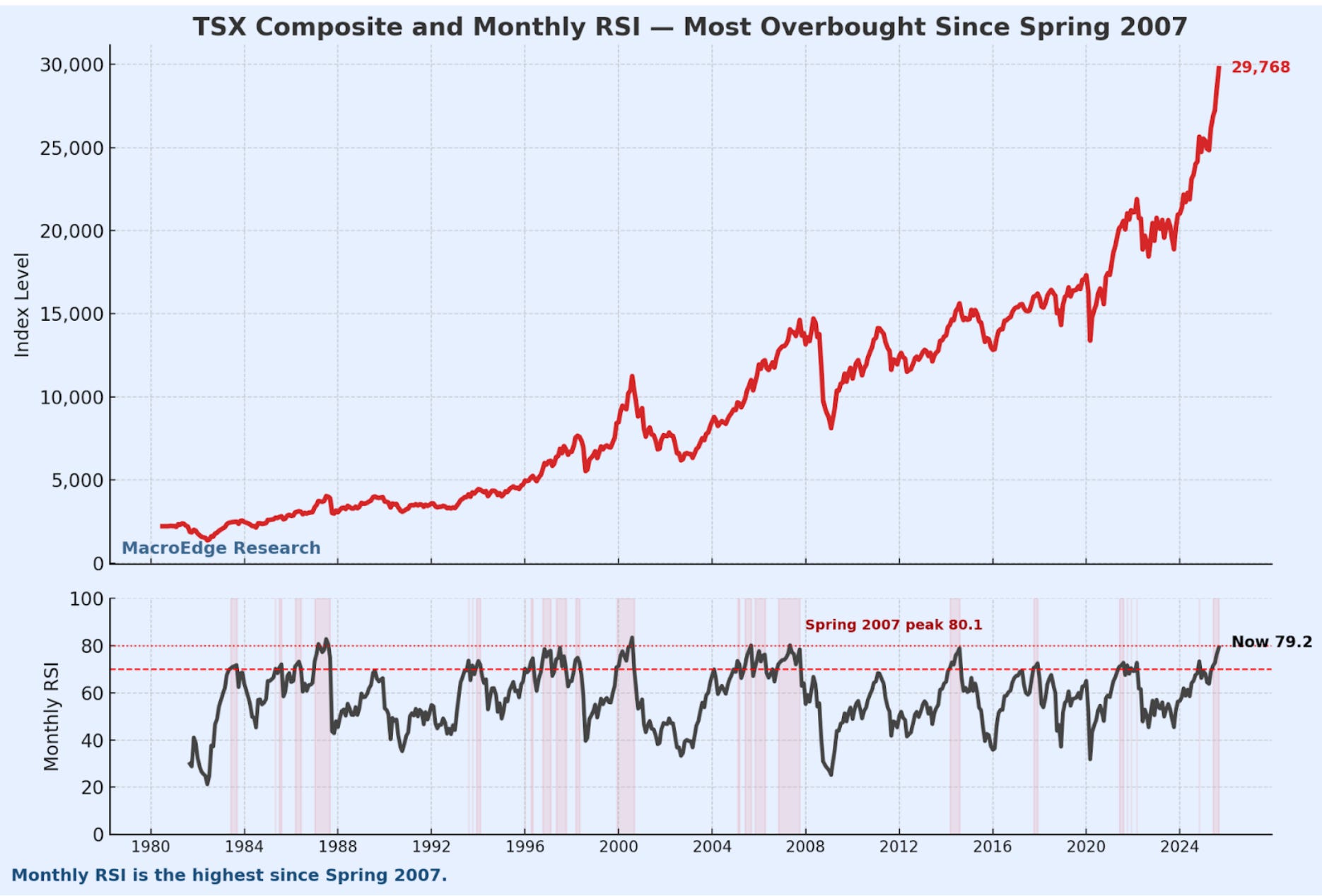

The TSX in Canada is its most overbought since Spring 07 on the monthly:

The macro situation in Canada is absolutely awful (employment and housing) so this is quite surprising, though the Bank of Canada continues to provide further support for assets… yes, note they aren’t bleeding into the economy beyond the assets due to other issues like immigration at play in Canada.

Globally, really strong r:r for left tail hedging, assuming we still don’t have ramp ups of QE/fiscal interventions immediately.

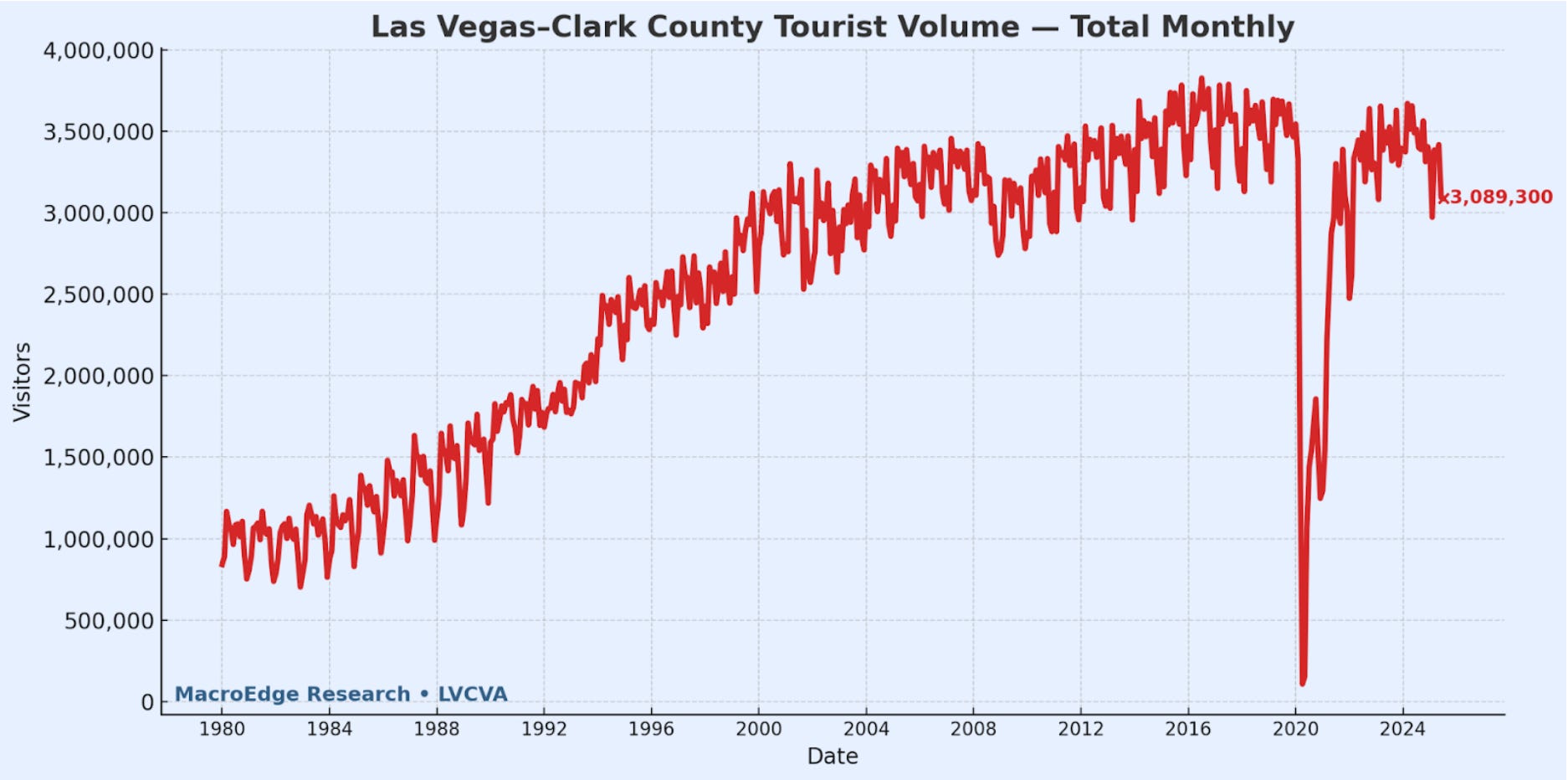

Silver State Troubles

One of the more important ‘bellwethers’ that we’ve discussed over the last 18 months is seeing some signs of accelerating softness. A) In travel data B) In residential construction employment and C) in home prices -

Nevada employment flipped negative y/y for the first time since the lockdowns (and MGM just cut 800 middle-management jobs):

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.