Weekly Macro Note: Life in a Market Managed by the Minute - Is There Any 'Real' Economy Left?, Oh My Gold... Let's Freak Out Again...

In this Weekly Macro Note - we discuss life in a market managed by the minute, a potential end to the ceasefire between Israel & Iran, technicals, employment data, gold, oil and natural gas, & more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

This evening we’ll keep the kickoff into the week quite brief as we continue to navigate ‘sillyland’ from a headline, algorithm, and markets standpoint. Late in the afternoon ET, we saw Iran launch 5 rounds of ballistic missiles towards Israel and drones toward the Kingdom of Jordan.

Sums up the entire risk environment:

The President stated that he’s in the driver’s seat and is trying to hold back from a retaliatory response from Israel, and it’s clear that Trump is getting very burnt out of the operation as we drag past month 3 and the Strait of Hormuz being closed for 100 days. While some are ‘surprised’ and ‘shocked’, we’re not yet living in some Mad Max-style-movie - the expectation was never that for the United States - given the size of our petroleum production and how much is being exported abroad (record levels right now). I still do not expect Iran to play ball on the Strait of Hormuz and uranium until at least the end of the month or past the 4th of July - and they know with midterms that the longer they can keep this level of pain going on the global economy, the larger the ramifications will be later in the year. With the level of intervention required to keep the market (which I consider to be the economy in the eyes of this Administration) afloat, it begs the question: is there any ‘real’ economy left? It seems quite counterintuitive, but the Gilded-era approach of simply pumping nominal values into the sky, higher and higher, continues to hollow out the productive economy as human capital and intelligence shift into things like government-backed capital incineration in projects we label ‘national security requirements’. If bailing out OpenAI and Altman is a national security requirement, I am going to go into retirement and start selling oceanfront property in Nevada, seriously…

We don’t need to go into my latest rantings on what a joke the whole bailout story that was released Friday & Saturday has become - and it’s clear that the AI companies are looking for their exit liquidity and puck save to be the US taxpayer. From outrageous capex suggestions like data centers in space and the whole token economy starting to atrophy corporate budgets, we’re starting to see additional pressures on the data center and ‘industrial revolution’ buildout. When this is all said and done, we’re likely going to be staring at a giant crater wondering what we just blew hundreds of billions of dollars on. When someone demonstrates an actual profit moat for these LLM companies - maybe, just maybe, I will be a little less jaded about it… but for now, I expect my early 2025 projections to come to fruition about taxpayer bailouts (acquisitions as they’ll call them) of some of these companies - especially the worst capital incinerators like Altman’s machine.

For futures (as of about 8pm) - oil is up modestly (~3%), the Nasdaq is flat, and Bitcoin is up about 2.5% on news that Trump is trying to restrain Netanyahu from retaliation. At one point in the weekend, CFDs - oil was up about 7%, and quickly we saw the maximum TACO approach to rein in the gain. Regardless, I expect Iran to sit in this ‘wait and see’ approach on what comes next, and I do not expect that Israel is simply going to let the retaliatory strikes slide. The ‘bear trap’ that are wars in Persia are gnarly ones, and the President finds himself in quicksand that he’s trying to use every tool and object to attempt to get out of the ‘pit’ of Persia.

This evening, we’ll cover the macro week ahead, discuss the employment report, talk about the Yen living above 160, highlight what’s next for oil and natgas, and wrap up with a technical look at the Nasdaq. It’ll be another headline-driven week, so buckle up and let’s have a great week as we speed toward the second half of the year (hard to believe!).

Not yet an Ozone subscriber? Upgrade below and get all of the latest data, research, and portfolio strategy right from the MacroEdge team.

Macro Week Ahead

This week, it is expected that the ECB will begin hiking their policy rate. This may be a one-off due to the Israel-Iran war, but sticky inflation pressures are spreading across the globe, and EU rates have been on the up and up.

Monday: NY Fed Consumer Expectations

Tuesday: Balance of Trade, Wholesale Inventories

Wednesday: May Consumer Price Index

Thursday: May Producer Price Index

Friday: UMich Sentiment Prelim (June)

Additionally, Oracle reports on Wednesday, and Adobe reports on Thursday.

A Look at the Employment Report

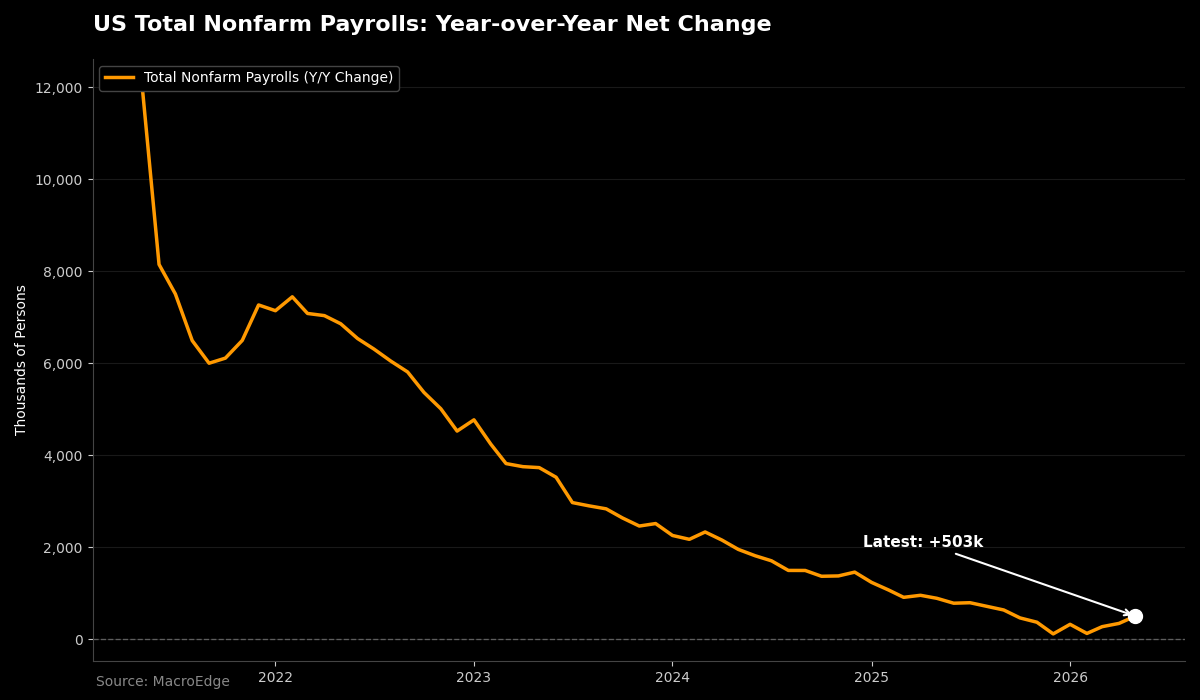

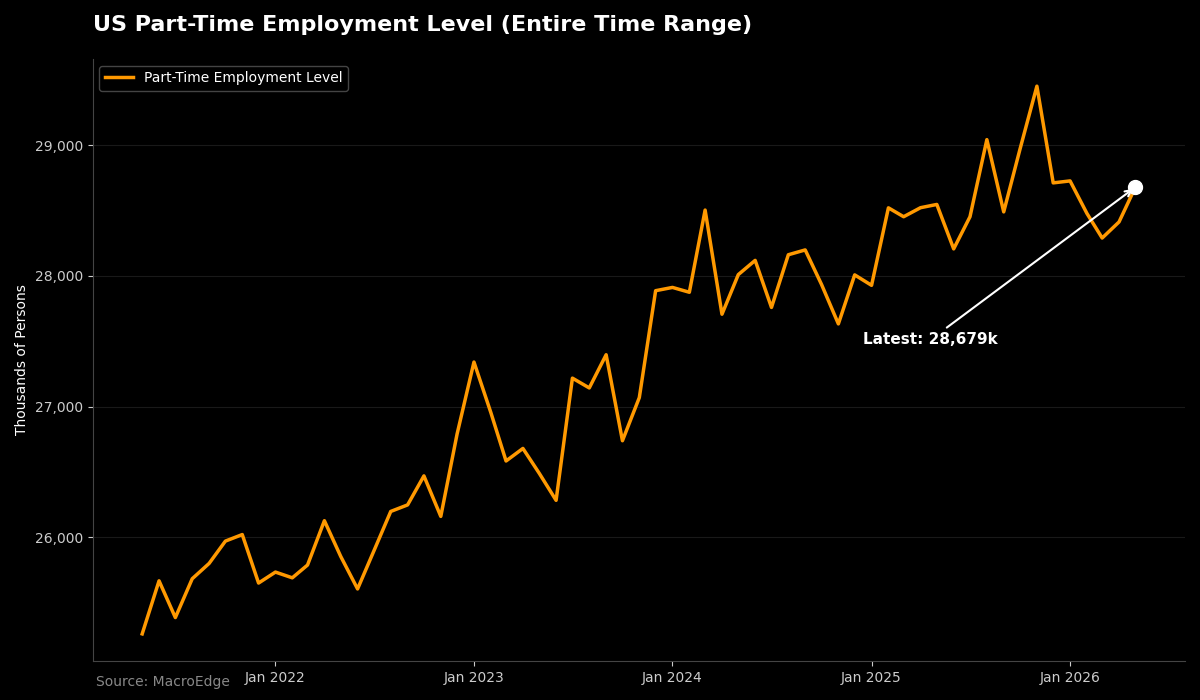

The payroll report presented another mixed picture. While the weakest prints are in the rearview mirror for the time being, the report came in line with our expectations. On a population-adjusted basis, these reports are barely above break-even, and job growth was driven almost entirely by a brief spike in part-time jobs.

Nonfarms came in with a positive YoY read:

The unemployment level remained largely unchanged for the month.

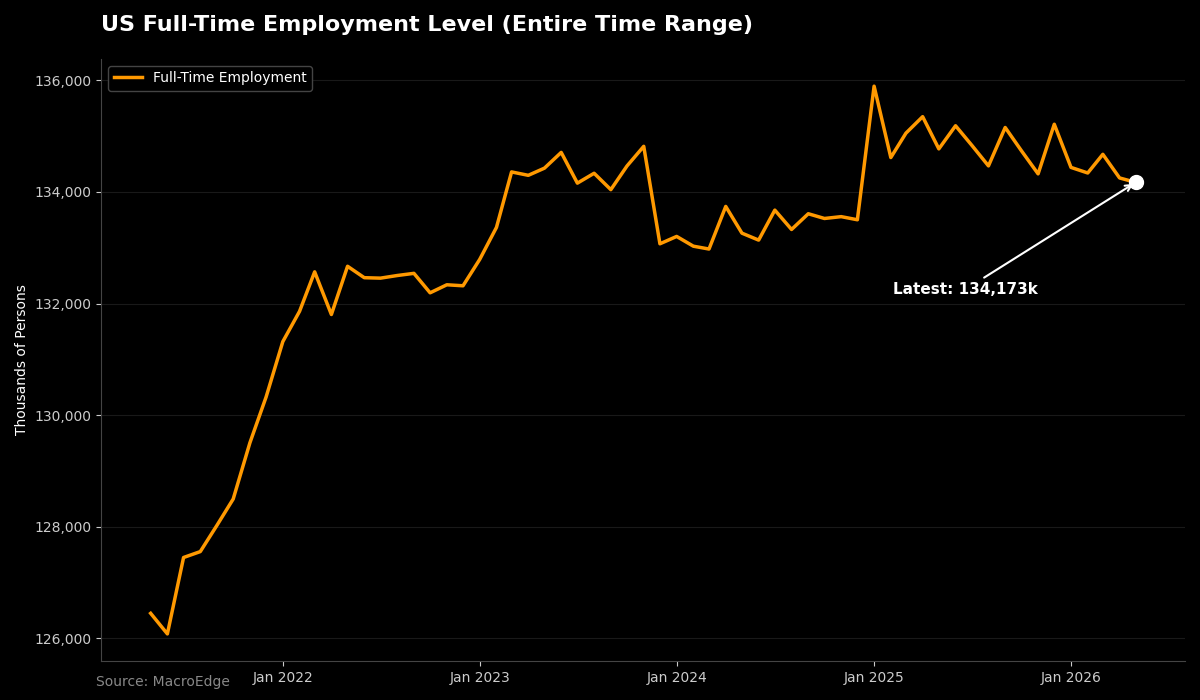

Full-time employment hasn’t changed for the better part of three years, and there are some very alarming underlying trends, like zero growth in male employment, while retirements continue to surge:

The ‘nice-looking’ headline figure is likely due to a combination of FIFA-related hiring for the past month, and a rebound in corporate hiring, though layoffs are still elevated. It’s just a bizarre employment environment - and low immigration along with worsening demographics are making the labor market look better in the data than it actually is.

Expect this mixed picture to continue through the June and July data.

The Yen is Not AI’s Friend

The Yen is back in ‘critical’ territory, weakening and staying above the 160-threshold. It’s near levels that have previously forced the BoJ to hike - and we’re once again, close to that with the BoJ potentially hiking this month.

Time to hike Bank of Japan? Likely once more…