Weekly Macro Note: Jensen's Week, Tariff Update, February Cryptocurrency Report, Portfolio Strategy Update, & More

In this Weekly Macro Note - we discuss the importance of the Nvidia report this week, highlight our cryptocurrency updates, talk about the latest MacroEdge portfolio strategy moves, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers and Community

This week, we shift into a relatively quiet week from a data release standpoint in the United States and Japan - there’s some inflation data - but by-and-large, traders continue to watch for AI/data center bubble risk signals, and individual sectors have continually been rotated through. On top of that, for those ‘monitoring the situation’ - it’s been a constant standby mode for the Iran situation - and there’s been a lot of smoke signals from either side on progress on whether or not we’re actually going to see a deal or not.

Futures are reacting negatively to the 15% global minimum tariff rate enacted by the President - ironically, total tariffs collected (on an annualized basis) are still lower than under the previous tariff/deal framework - but the market clearly dislikes the uncertainty. I wouldn’t put too much weight into any futures reaction in this distributive regime for the time being, given what we’ve been over the past six months.

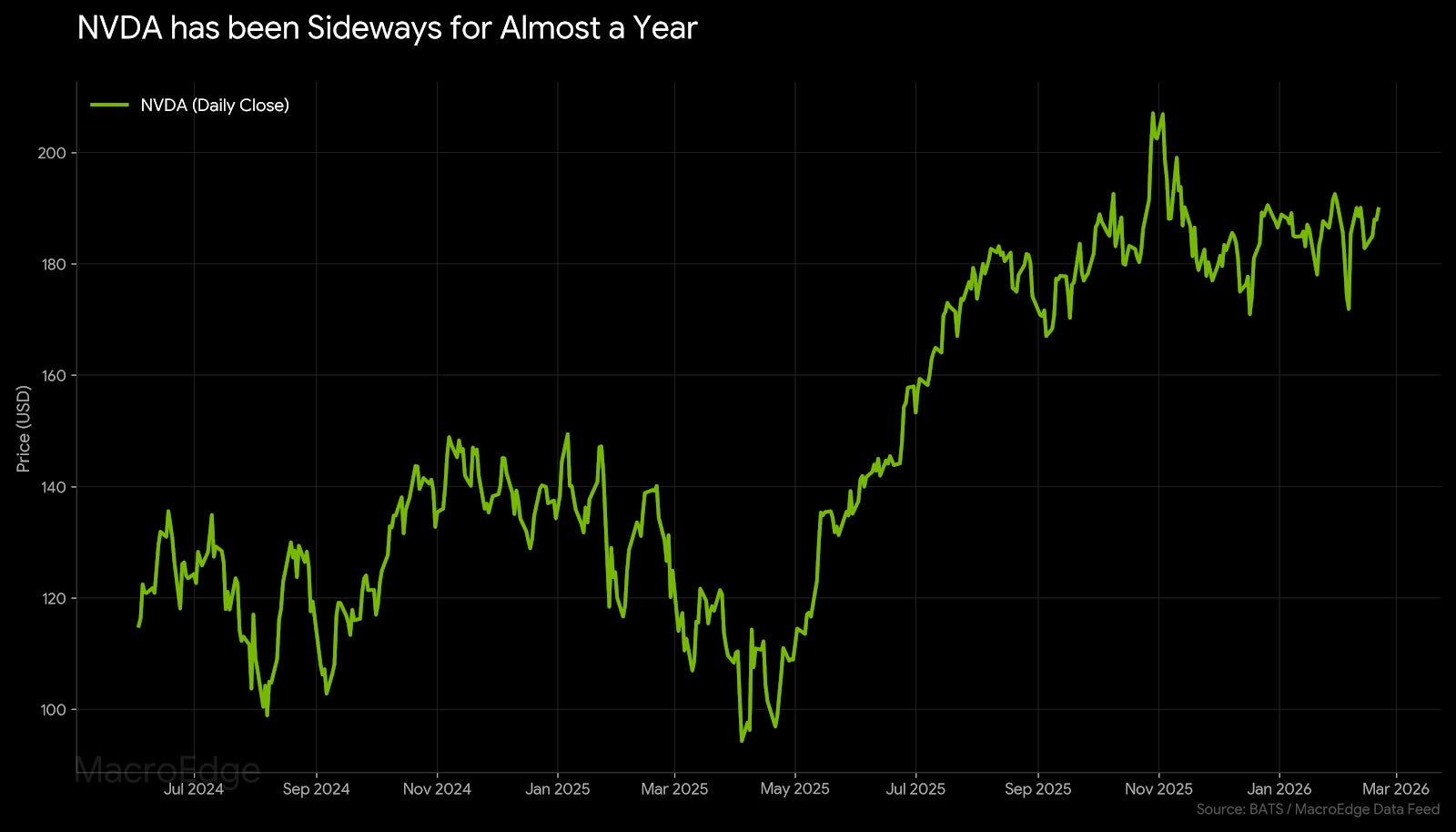

This week, Nvidia earnings are also going to be important (yes, I hate continually saying this), but Nvidia has been sideways for the better part of eight months now.

On top of that, we’ll get some additional GDP readings internationally, and I continue to utilize our global bubble framework for several key international markets as a signal for US markets - and for the entire AI/data center trade that continues to enjoy massive hype. When the Japanese and Korean markets finally wobble - the whole AI trade will be in the United States as well. On top of that, continue to watch the dollar for signs of the next move as the Administration (and Bessent) moved to stabilize the index over the last several weeks.

We’ve got a lot, lot, lot of reports and data in the pipeline:

Midweek Macro Note (Thursday Before Market Open)

Portfolio Strategy Note & Trident Note (Friday Evening)

Data Center and AI Update - February Data Release / AI Bubble Update with guest article from the Coastal Journal (Saturday Morning)

Weekly Macro Note (Sunday Evening) - March 1st

Which are repeated below again at the bottom of the report, but this useful macro data is critical in determining how a lot of these individual sectors are holding up. On the inflation front, this week we’ll get some additional data and color on where price levels stand, and it doesn’t look like we’re putting a dent in any price level yet from a CPI index standpoint (although that is quite rare). Consumers remain deeply unhappy about the economy - even though we continue to see real retail sales hold up at their 2021 indexed level - though the i-shaped economy is becoming more pronounced with every passing day. As things get more murky and complicated, I continue to wait for the key ‘macro trigger(s)’ as this distributive pattern continues.

With that being said, let’s dive into the macro calendar and have a great start to the week.

Macro Week Ahead

The week ahead is lighter than last week, though Nvidia earnings will take the spotlight for the week.

Monday: Waller Speech, Chicago Fed National Activity Index, Japan (Market Holiday)

Tuesday: CB Consumer Confidence, Factory Orders, Fed Governor Cook Speech

Wednesday: Nvidia Earnings, US Home Price Index

Thursday: Japan (national CPI), BoJ Takada Speech

Friday: US PPI, Canada GDP

If you aren’t yet a subscriber to MacroEdge Ozone on Substack, you’re missing our state-of-the-art data, research, portfolio strategy, and much more. We’ve shifted our entire Ozone infrastructure onto Substack - and we’re going to have more information over the next week on gatherings and our MacroStack group that is currently in development.

GDP Growth & Inflation Pulse

(Continued below: GDP Growth & Inflation Pulse, February Cryptocurrency Report, Supreme Court Ruling + New Tariffs Review, Technical Review for February, Energy Portfolio Strategy Basket, Portfolio Strategy Update & Commentary - Six)…

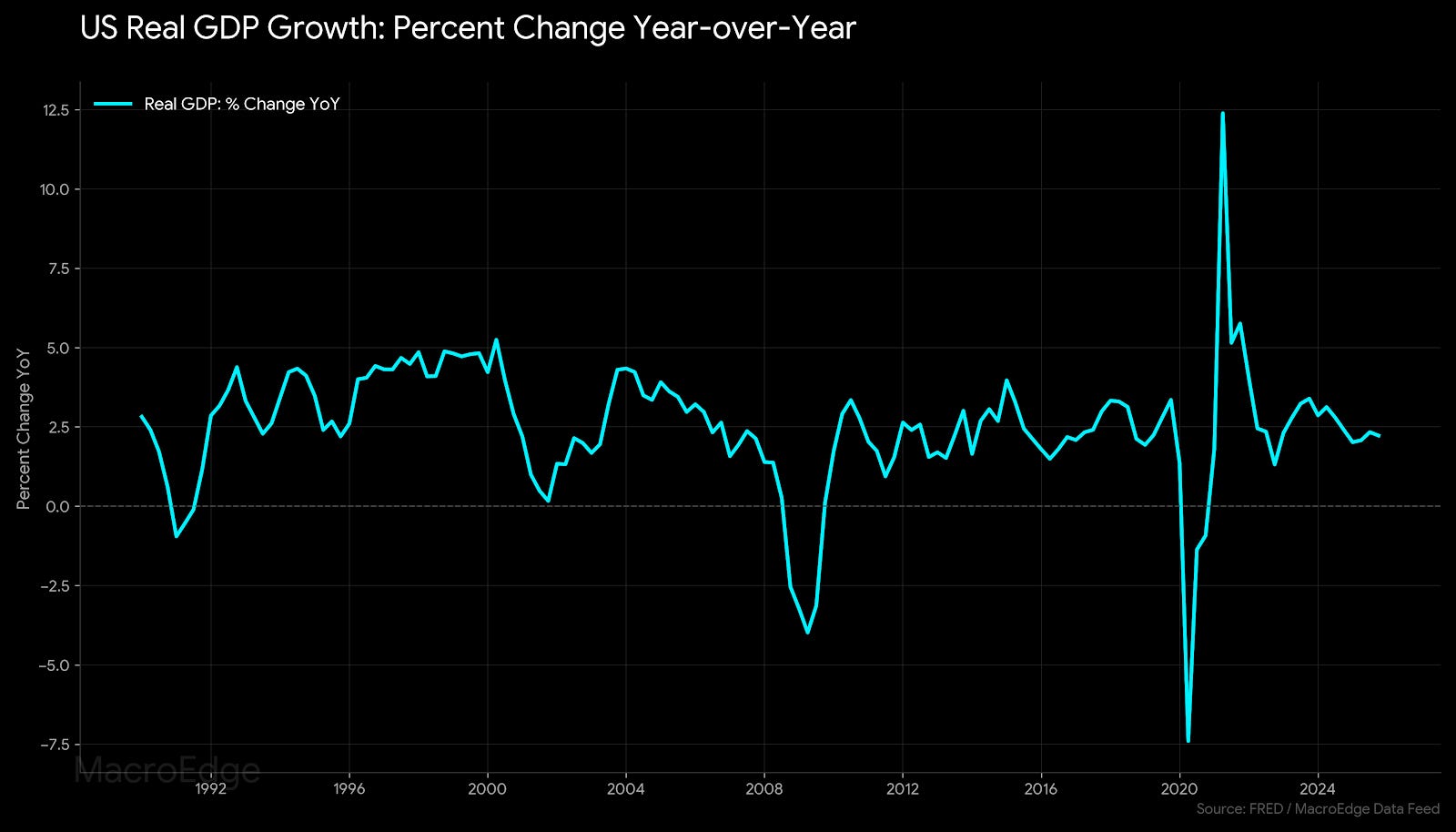

The GDP print was relatively soft for Q4, and inflation remains elevated & above trend. Despite political rhetoric suggesting a transition toward a “15% GDP print,” the underlying data in the latest reports continues to show a significant disconnect between political signaling and economic reality. Realized growth remains largely on-trend with previous presidential regimes, characterized by structural constraints and a lack of the “explosive” acceleration often cited in Trump admin briefings. Instead of a revolutionary breakout, the 2025-2026 trajectory is currently pacing toward a modest 2% year (assuming no major halt to data centers, AI, etc.). This performance aligns more closely with the long-term historical mean than with any transformative fiscal paradigm. Furthermore, the economy faces a concentrated risk if the massive capital outlays for data centers and artificial intelligence begin to soften. Should AI-driven demand reach a saturation point or investment cycles slow, it could remove one of the few remaining pillars of industrial support. This persistent “Gap” suggests that while market sentiment may be buoyed by optimism, the fundamental engine of the US economy is still operating within its traditional, range-bound growth parameters.

This complicated dynamic pushes me to utilize real GDP as the preferred metric for measuring actual growth, and you can see the largely in-line print:

Supreme Court Tariff Ruling + New Tariffs & Analysis

The Supreme Court tariff largely came as a surprise to no one reading our research reports, and it had been expected for several weeks. The overturn pushed the Administration into enacting several new tariffs, and Trump has set the global minimum rate at 15%.

The Supreme Court ruling has shifted (not dramatically) the present trade landscape by striking down the administration’s use of the International Emergency Economic Powers Act (IEEPA) for broad-based universal tariffs. Before the ruling, the United States was operating under an aggressive high-tariff regime with an average effective rate of 18.5% and a projected annualized revenue stream of $465 billion. While the ruling provides immediate relief for global supply chains and importers, it introduces a new layer of policy uncertainty regarding the executive’s next move. A significant but highly unlikely risk is the potential invocation of Section 380 tariffs. This authority would represent a more severe and legally contentious approach to protectionism, potentially triggering a level of international retaliation far greater than the original IEEPA measures. Although this remains a tail risk with a low probability of implementation, its mere possibility continues to weigh on long-term capital expenditure plans for multinational corporations.

The post-SCOTUS ruling introduces new uncertainties - and the US will generate about $100bn less on an annualized basis from these new tariffs. It also remains to be seen whether they are challenged, or hold up going into midterms if the economy begins to flash additional warning signals. I expect the Administration to try and push the effective rate back toward the IEEPA levels, in as cautious a manner as possible.

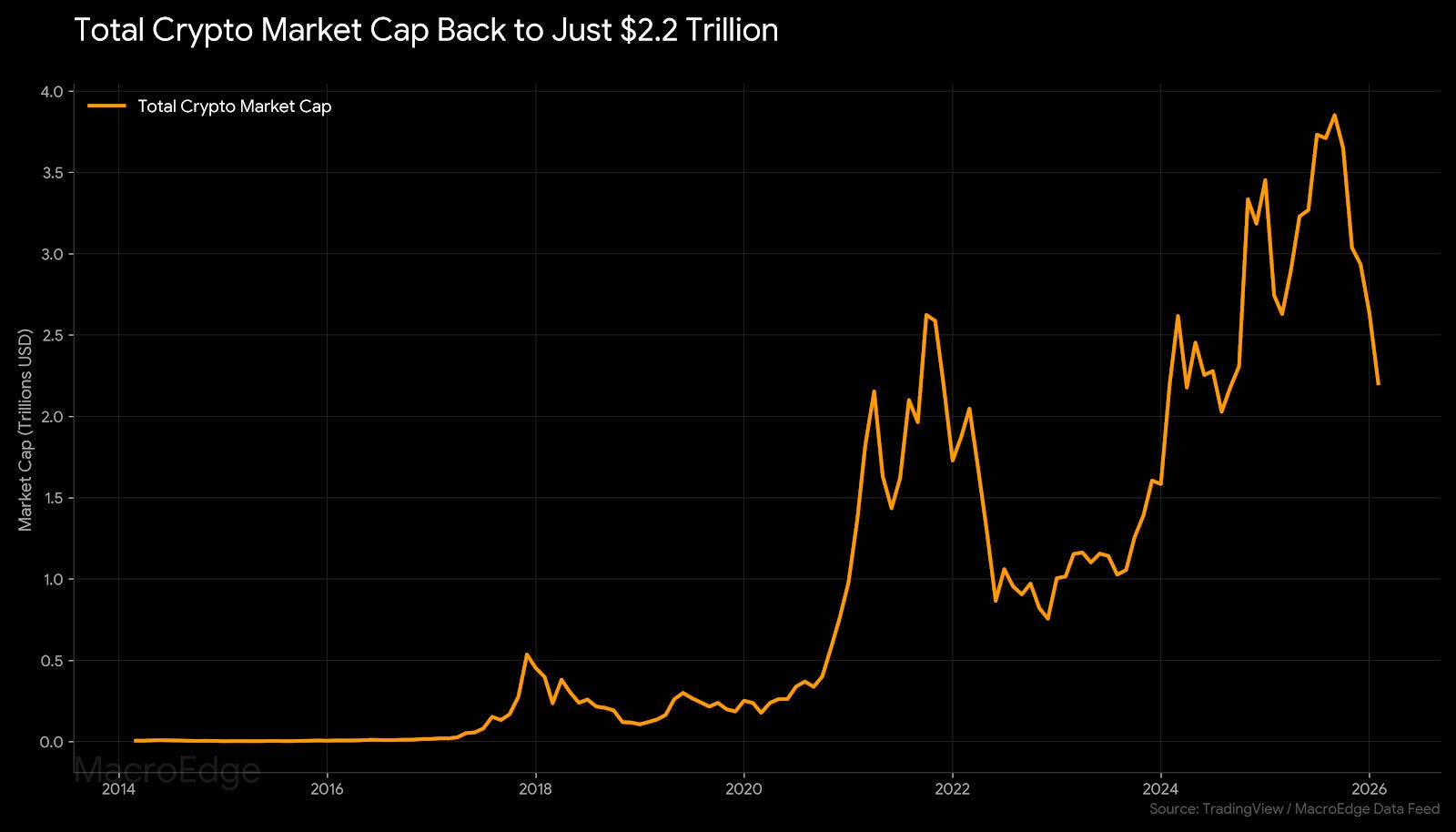

February Cryptocurrency Report

The cryptocurrency space has come under great pressure since September, when we published our first cryptocurrency related briefing.

Bitcoin is hovering around $64,500 at the time of this writing - and the balanced price level is somewhere in the mid-40s right now. Technicals have proven to be extremely useful (again) for this cycle, which makes sense, given that there are very few fundamentals behind the entire crypto space other than liquidity, speculation, and what we might label as ‘vibes’.

While oversold conditions are now present on the weekly, crypto often finds itself at oversold conditions for an extended period of time during these longer drawdowns. If Bitcoin approaches the mid-40s, I’d say that offers a much more attractive risk:reward ratio, especially if liquidity conditions are improving - but for the time being, things continue to look very ugly in the space, and there is still far too much leverage for my own comfort. With individuals being able to lever up 20/50/100x, this presents risk for further liquidations and downside if these sell programs continue.

Technically, a lot still needs to be resolved here for conditions to improve, and sellers are in the driver’s seat.

Technical Deep Dive for February

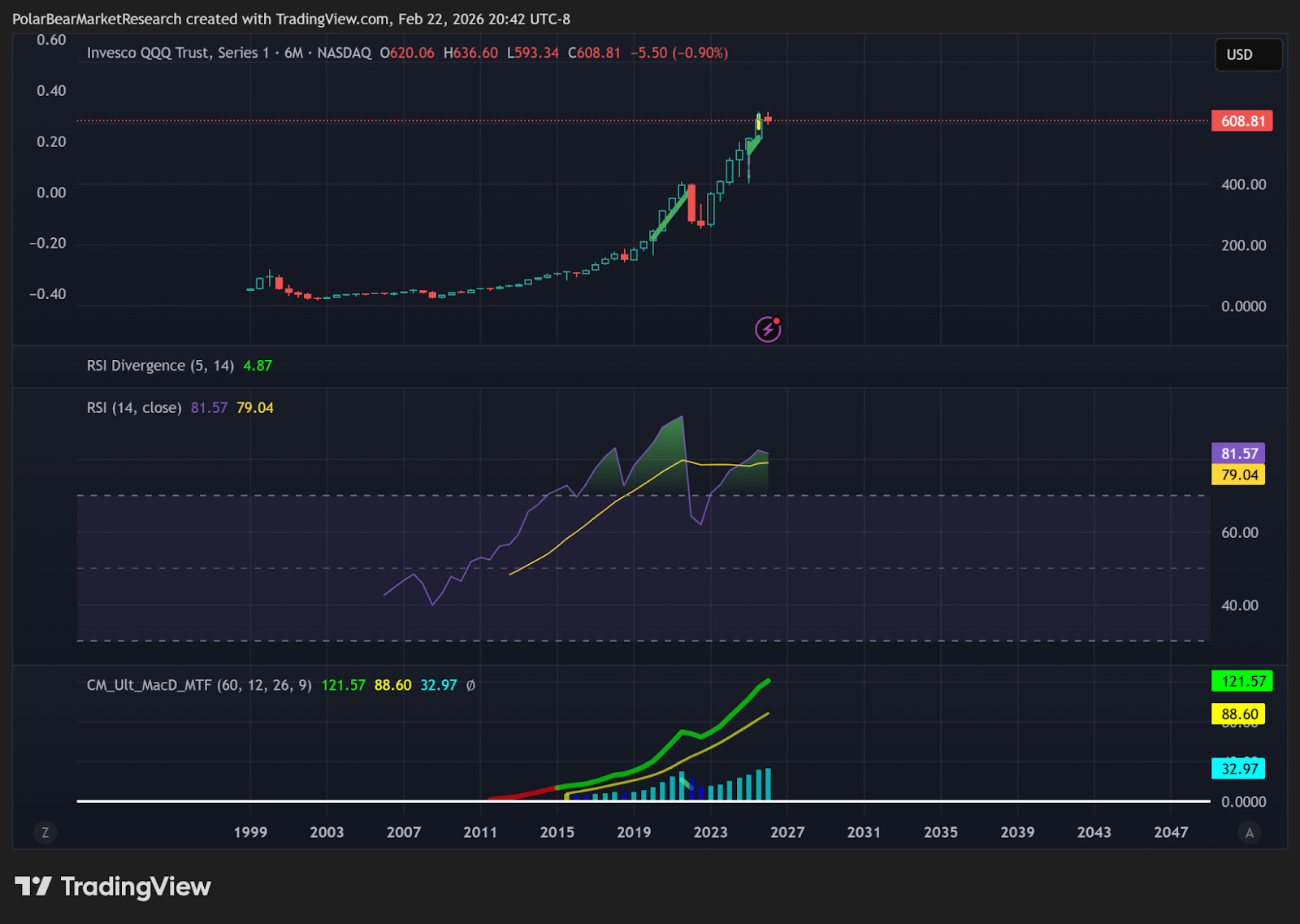

Technically, the next important thing for the technology sector is the Nvidia earnings on Wednesday. I am cautious on interpreting after hours action on the equity, but I still expect bigger problems for the MAGS name to emerge late in the 2nd half of the year versus in the present/last quarter. As data center & AI problems materialize, investors are now looking to the future to see if they’re going to get a return - and a lot are questioning if this is ever going to happen with Nvidia at these levels (and a $5 trillion market cap). For the Nasdaq, we’re starting to see the sideways action in very long-term timeframes like the 6-month, and negative divergences on timeframes this long are very notable if they materialize:

While cyclicals have improved to a degree to start the year, I think these are being wrongly re-interpreted as ‘macro-reacceleration’ when they are likely to turn out as another complicated fakeout - of which we’ve seen many over the past three years.

Oil prices are in a standby pattern waiting to see if the US moves on Iran, and how inventories shift over the next several weeks:

Technically, the look is extremely constructive in many different names (and even nation indices like KSA - for Saudi Arabia - look quite positive). The same goes for gasoline prices, which look quite constructive as well. Any geopol turmoil and a combination of different structural factors could finally get the wheels turning here. The key with any energy trade is not pulling the cord too early if things look a little wobbly, because we know that politically it is extremely unpopular (and risky) to let energy prices rise.

For the Nikkei (and our global bubble indices - which we’ll have an update again in the next week or two) the parabolic price action has once again briefly stalled.

For the IBEX - I continue to use this as the most reliable signal for the US cycle - and for the AI/data center cycle (AIS), the Nikkei continues to run a nearly 1:1 correlation, as we’ve talked about many times in the past several months.

Energy Portfolio Strategy Basket

We have a very exciting energy portfolio strategy basket being constructed, and I am currently working on finalizing the details with Six. In a special report this week, we will publish the basket under our portfolio strategy report - as well as include key portfolio strategy items like allocation, risk, etc. Stay tuned for that following the Midweek Macro Note… and Six will have more on it below.

Remaining Reports for February

Midweek Macro Note (Thursday Before Market Open)

Portfolio Strategy Note & Trident Note (Friday Evening)

Data Center and AI Update - February Data Release / AI Bubble Update with guest article from the Coastal Journal (Saturday Morning)

Weekly Macro Note (Sunday Evening) - March 1st

Have a fantastic start to your week, and I will hand it over to Six.

MacroEdge Portfolio Strategy Update - February 22, 2026 (@SixFinance, Head of Research)

Friday’s Supreme Court decision and Trump’s following response in taking global tariffs to 10% across the board, and then later on Saturday, increasing to 15% in a Truth Social post, takes trade policy into a further state of uncertainty. It’s no surprise that the tariffs done under IEEPA were deemed illegal; that was widely expected. It’s also no surprise that Trump immediately fired back with new levies; he and his cabinet have been saying for months that they will do so. Trump could have used the Supreme Court verdict to pivot, and instead chose to dig his heels in and has shown pure hubris and emotionality in raising from 10% to 15% less than 24 hours after his initial response.

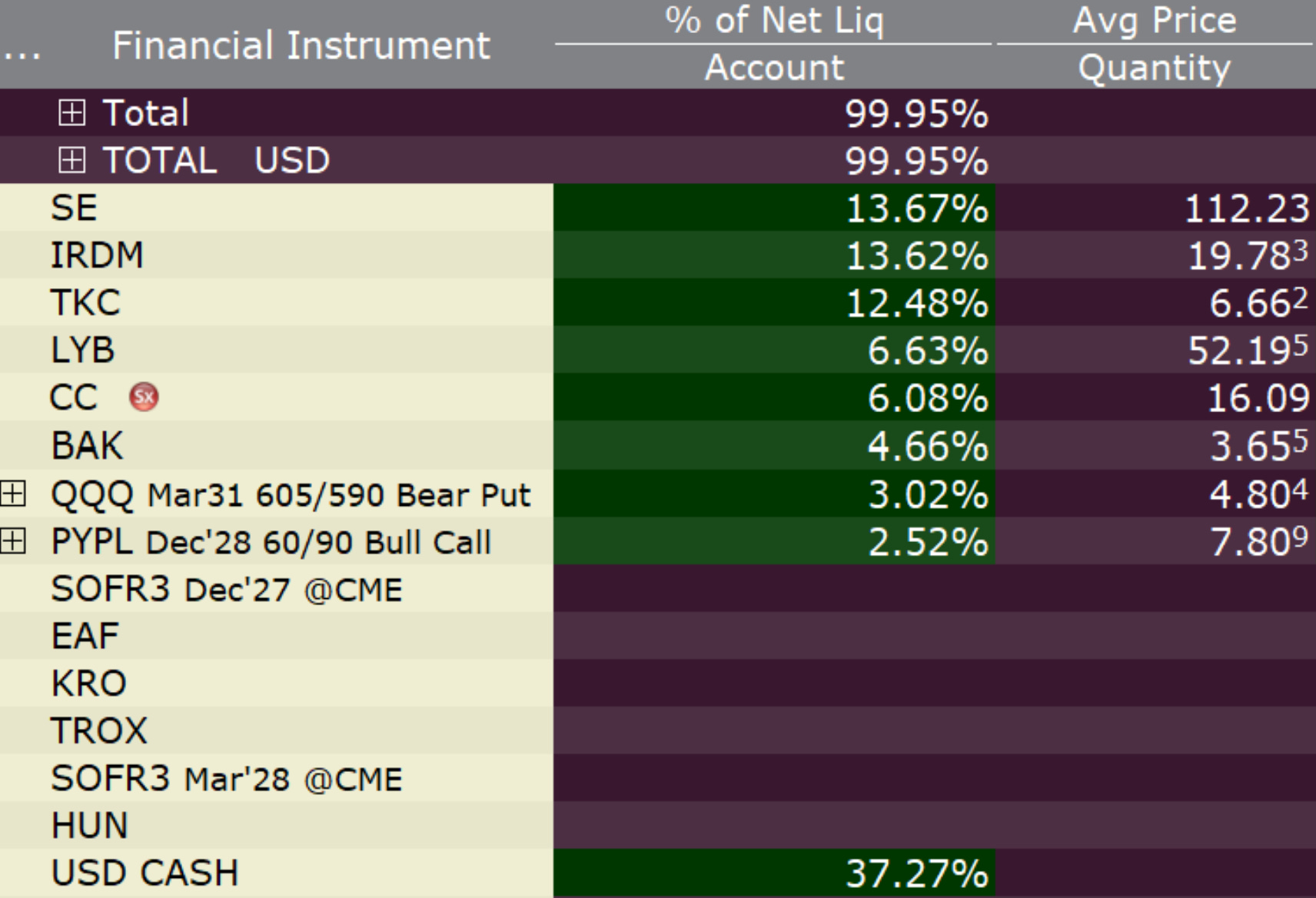

Within the portfolio, I have taken my US equity exposure way down, as I am unsure if the market will be optimistic as to a lower effective tariff rate than existed before yesterday, or if the continuation of policy volatility as POTUS doubles down on trade will be negative for US beta in the short term as import costs swing.

I have exited the SOFR futures entirely and captured profits on those, as the hot Core PCE and cold GDP print on Friday was not what I expected. I have also reduced my exposure to the manufacturing sector following a weaker-than-expected Manufacturing PMI, and my general lack of substantial conviction across the board required to run larger risk positions. I have hedged my remaining equity exposure with a 3% position in narrow put spreads expiring at the end of March, seen in the table above.

I still believe that deglobalization remains the predominant factor shaping global macroeconomics today. Countries around the world are taking action to diversify their supply chains and defense posture. The global effective tariff rate is rising, even when tariffs imposed on or by the United States are stripped from consideration, from ~2.5% to 3.5% thus far, with additional tariffs and trade barriers being floated in many countries around the world.

Unless Trump’s team can find a way to isolate China in their levies, the new flat-rate model will disproportionately benefit China given its existing position in the supply chain. Countries like Vietnam, who have enjoyed a surge in activity over the last year, will see a reversal in the rerouting of trade through their country.

The policy structure on China will be the most telling. We are in an economic cold war with China, and it is largely bipartisan within Congress. While relations are relatively tame at the moment, we know that can change as soon as China finishes stockpiling oil and gold, and the US alternative critical mineral supply comes fully online. Global defense spending, averaging a CAGR of 3-4% over the last two decades, is now forecast to grow in excess of 8% through 2030, as the world enters a rearmament era. The US-China relationship will continue to drive deeply liquid, large-scale capital allocation over the coming years.

Oil looks ready to breakout here, but is also certainly enjoying a geopolitical risk premium as the US has amassed an armada on Iran’s doorstep. The newly issued tariff ruling from the Supreme Court and the new flat tariff rates call into question the counterparties on all US trade deals. If OPEC countries feel they no longer must keep oil production high as a backdoor cost to favorable trade and access to the AI supply chain, production hikes may not resume as planned this year.

In addition to the names Don is looking at, I am becoming very interested in Saudi Arabia, whose stock market has been trading mostly sideways for a matter of years now, while global equities have broadly melted up over the last year. Saudi Arabia has, as of February 1st, 2026, removed the Qualified Foreign Investor restriction within their equity market. This previously allowed only large financial institutions to invest in their shares. Now, Saudi Arabia is moving to diversify away from being solely an oil economy, and simultaneously aggressively pursuing foreign deposits and investment. If the Iranian regime falls, the peace dividend in the Middle East could be enormous and structural. The KSA ETF is the vehicle I will be using to capture that broad exposure.

US-led procyclical policy has spilled over into Japan, Germany, India, Poland, Vietnam, and other countries. The policy drivers are aligning on a global basis to be very constructive for commodity prices. The Australian Dollar also looks good on this basis.

For more details, please refer to our Terms and Conditions.