Weekly Macro Note: Golden Goose, Crash Up Continues, What About the EU?, Financial Conditions Continue to Loosen

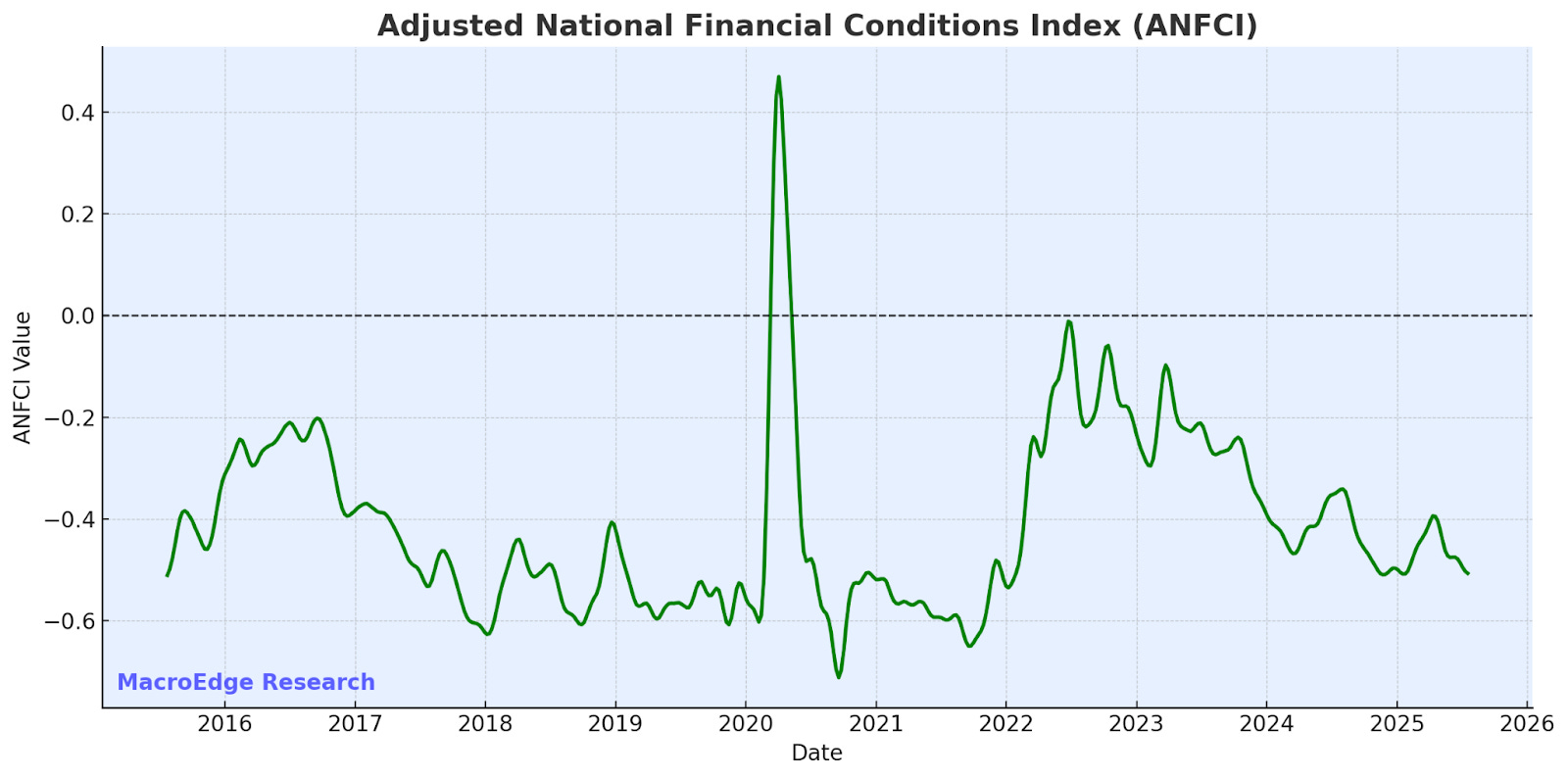

In this Weekly Macro Note, we discuss the continued loosening of financial conditions - back to their post-pandemic low levels, valuations, EU equities, the potential for rate cuts, and more.

Good Sunday evening MacroEdge Readers, Clients, & Community,

This evening – new trade announcements are again sending markets ‘gapping up’ into Monday (they love their pre-futures Sunday announcements) – and we’ll dive into the details more below. With FOMC week finally in view, we know that we’re likely to see the Fed continue to hold rates this week and begin easing at the next meeting, as is currently priced, though a rate cut scenario can quickly be delayed, that’s become less likely as the heat gets turned up on the Fed to continue abetting a rapid debasement of the currency, along with a very pro-inflation regime. While there are some tariff impacts looming to offset here, the net effect continues to be one that’s very pro-asset class and assets (equities – in particular) themselves, with valuations shooting higher without any regard to fundamentals.

Monetary loosening may continue to pack the pipeline now, with the Big Beautiful Bill providing additional stimulative tailwinds to assets, and the ‘perfect scenario’ for a crash up in nominal asset prices has continued to play out as deals are made, the dollar is devalued, and rate cuts have been cued up.

In the week ahead - we’ll have more on Wednesday evening with earnings, updated FOMC data, and much more. It’s a major MAGS earnings well, along with FOMC, global volatility, and more, and we’re keeping an eye on it all as we continue to develop our first AlphaSights Report

New ‘Deal’ with the EU, China Pause to Continue

The United States and the European Union announced a new trade agreement aimed at avoiding a costly trade war and bringing more predictability to transatlantic commerce. The deal sets a 15% import tariff on most EU goods entering the U.S., a significant reduction from the originally threatened 30% rate. However, steel and aluminum imports will still face a 50% tariff, with the possibility of that being reduced in future negotiations. In a win for both sides, the agreement also establishes a zero-tariff policy on certain strategic sectors including aircraft, semiconductor equipment, specific chemicals, and raw materials.

As part of the deal, the European Union committed to investing $600 billion into the U.S. economy over an unspecified period. It also agreed to purchase $750 billion worth of U.S. energy products, spread over the remainder of President Trump’s term, averaging roughly $250 billion annually. Additional defense purchases are also included as part of the broader cooperation framework. The goal of the deal is to stabilize trade flows and avoid tit-for-tat escalations that could severely disrupt supply chains.

At the same time, the U.S. and China are maintaining a fragile tariff pause that began in May 2025. The initial agreement saw the U.S. roll back tariffs from a peak of 145% to 30%, while China reduced its retaliatory rates from 125% down to 10%. This truce is currently set to expire around August 12, 2025. However, negotiators from both countries are meeting in Stockholm tomorrow and are expected to extend the pause for another 90 days, pushing the freeze through mid-November.

While no comprehensive deal with China has been reached, both sides have shown a willingness to keep the situation from escalating further, at least in the near term. The pause gives businesses on both sides of the Pacific some breathing room but does little to resolve the core structural tensions between the two economies. The strategy, similar to the EU deal, reflects the Trump administration’s broader approach of using aggressive tariff threats to force strategic concessions while avoiding total breakdowns in trade relationships.

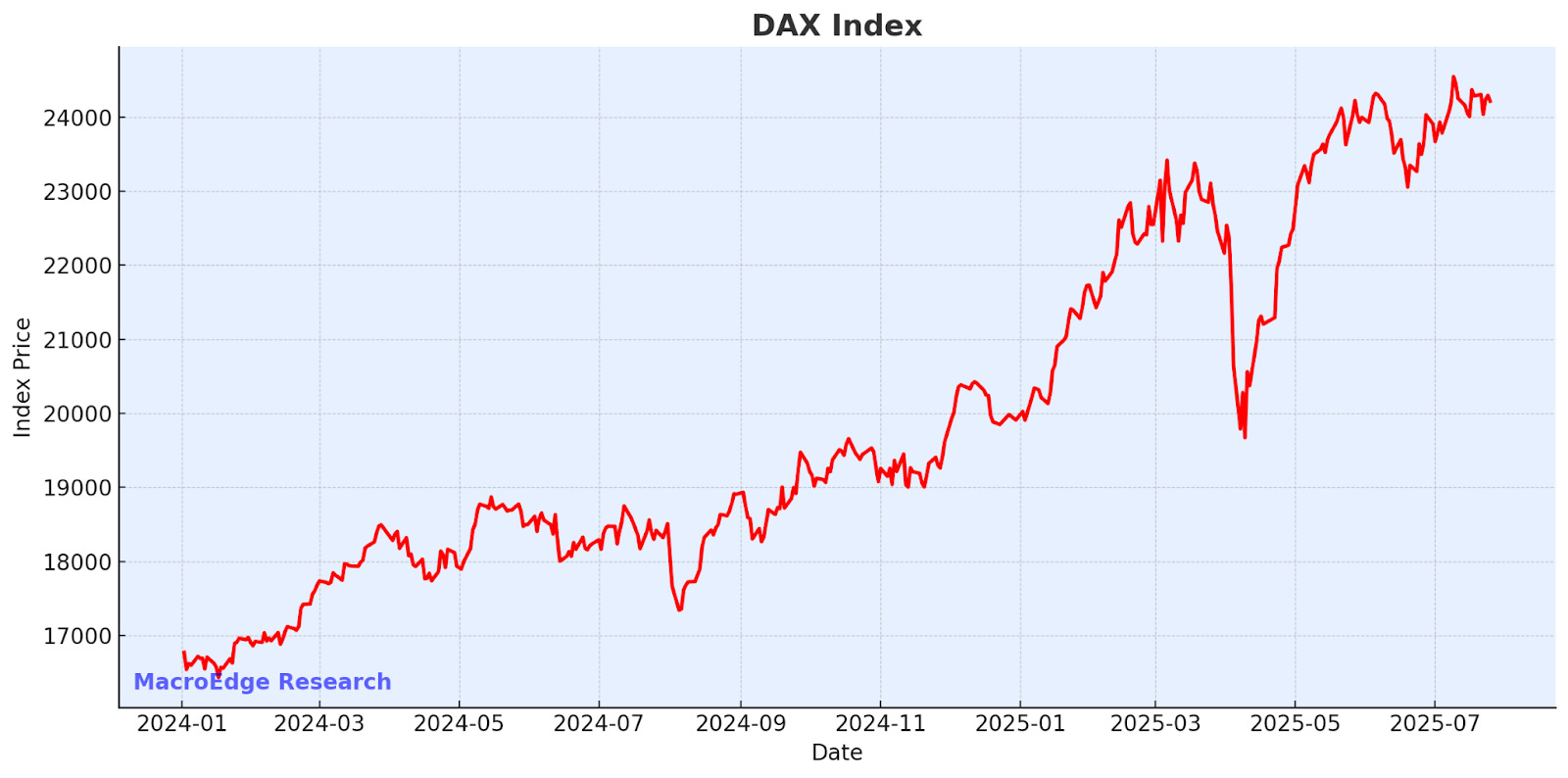

Note the US outperformance again widening on the latest batch of positive news - especially relative to European equities.

Asset Glory Continues

The assets to glory narrative continues - and has continued to accelerate with new deals in the pipeline and monetary tightness conditions loosening to their loosest levels since 2021. The Admin continues to prioritize accelerating asset prices, and that trend is unlikely to change until we see rate cuts - with stimuli to the economy set to accelerate further with Big Beautiful Bill impacts in the pipeline.

Rate cuts may provide the perfect storm for looser financial conditions… and that leads us to…

Real Estate Rage = Rate Cuts?

FHFA head Pulte has been eager to get cuts out of Powell, without success to this point - though that may soon be changing with the President taking note of the recessionary real estate conditions. One industry bogged down by rates has been (especially) the existing home sales market, and monitor for any signs of life there as the new home builders continue to increase now in anticipation of financial conditions being loosened further for rate cuts, which would ease mortgage access and availability as banks loosen their lending standards:

A homebuilder recovery may be in order if the Administration is set on looseneing lending standards, getting money flowing into mortgage markets, and selling activity surges. For now, the opposite conditions remain true, though the market provides us with a useful view at how participants expect the more cyclical sectors to perform in the coming months.

The Manufacturing Renaissance Myth (@RealJohnGaltFla, MacroEdge Contributor)

While there are many who celebrate all of the announcements of countries to invest and companies to reshore into the United States, there are some stark reminders that while the talk is nice, cute and somewhat absurd, the track record is somewhat poor based on past performance.

As these pages wrote about and reminded everyone in March of this year, Foxconn was supposed to start building components for Apple iPhones and other devices. How did that work out for the United States and President Trump after the promises started flying in 2017?

From the Milwaukee Journal-Sentinel in 2023:

What has Foxconn built since expanding to Wisconsin?

Not what it originally promised. The facility has changed from a Generation 10.5 to a Generation 6, which normally makes screens for phones, tablets and TVs. But so far, no screens have been made.

In fact it gets worse. Another major company, this one run by a Chinese billionaire promised to build a factory in Moraine, OH, and indeed he did. From Fortune Magazine, December 22, 2016 after Trump’s first election:

His company, Fuyao Glass, has invested over $1 billion stateside, according to the Post, the most significant move of which is opening its U.S. factory in the Ohio town of Moraine, a suburb of Dayton, back in October. The glass maker is re-purposing the town’s former General Motors assembly that had been standing empty since late 2008, as the Dayton Daily News reports.

So how did that turn out several years later? From the Dayton Daily News, April 3, 2025:

The 74-page complaint describes a law enforcement investigation that began in December 2019, saying multiple “business owners originally from China” who, on moving to Ohio, “became intricately involved with one another” created roughly 40 business entities that facilitated the “harboring, transportation, and employment of illegal aliens at various factories, and have developed a sophisticated money laundering organization.”

Promises made, promises, uh, kept.

Why does this author keep such a skeptical eye towards all of these paper promises and commitments produced by the Trump administration on an almost daily basis?

That is simple. During President Trump’s first term, as outlined in my earlier article from March linked above, his promises were for all types of investment and corporations to relocate to the US and spend billions upon billions reshoring and investing in the US worker.

However, the same government bureaucrats that measured economic activity during his first term in office are still doing so today and the myth that manufacturing is going to return to the United States and boom is just that; a fallacy, a false promise, or better yet if one would like, a golden unicorn.

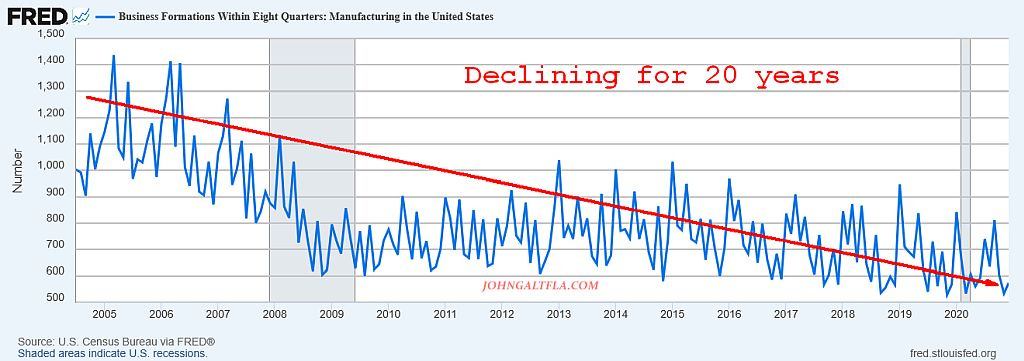

The data does not lie as manufacturing business creation has been in a 20 year decline but instead of analyzing why, the average American has followed the lead of team MAGA by blaming illegals and unfair trade practices.

To be honest, this author had no idea the numbers were truly that bad but they are now lower than during the lowest ebb of the Great Financial Crisis and bouncing off pandemic lows. If the manufacturing business formation is that low, the next obvious step is to verify that against manufacturing employment levels.

And that data is even more depressing:

Even though new manufacturing techniques have improved, to see numbers like that is breathtaking. The sector has barely recovered from the outsourcing surge under President Obama and worse, is at levels unseen since just before World War II. Yikes indeed.

As the layoffs intensify in the American tech sector as the H1B insourcing accelerates along with the promises to build in America fall by the wayside due to costs, red tape, and expense, do not say one was not warned. The track record during Trump v1.0 from 2016-2020 should have provided a guide that companies and nations will say or promise anything to create the short term political satisfaction with the administration while pumping up equity prices on Wall Street.

May we live in fraudulent times, indeed.

For more details, please refer to our Terms and Conditions.