Weekly Macro Note: Global Speculative Mania, Air Travel Continues to Soften, Volatility Lurks, Portfolio Strategy Update

In this Weekly Macro Note - we discuss developments in the global speculative mania - from Japan, to Korea, Spain, and more - talk about air travel trends, vol upside potential, strategy, & more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

It’s great to be back for our third consecutive day in a row as we wrap-up the ‘catch up’ streak from a very busy week on the road for us. My three month long sales rally continues, and I wrap-up my time in the desert over the next few days and be en route to the Midwest. We are evaluating new candidates for the establishment of our first headquarters location - and are focusing on places with very pro-business environments and low cost of living environments that allow us to begin growing our team from. While the current situation has been fantastic as a starting point, we can do better, which is the purpose for the next trip. I am excited to report back with more in next week’s Weekly Macro Note as we evaluate all of these options.

This weekend has been a major political weekend globally - with elections in the United States, Japan, Portugal, and elsewhere. There have been many interesting political shifts occurring - especially in Europe - where right-leaning parties are surging, but haven’t garnered enough power to overcome coalitions. That has resulted in results like we saw today in Portugal, though in Japan, the LDP secured an earth-shaking landslide in their victory. The Japanese are clearly passing up a mandate on a return to a zero immigration hardline policy, and societally, they have a whole lot to fix. While I’ve taken a break from our broader ‘Project South Africa’ report thematics for the time being, I think that we’ll likely bring some of that back as we head towards midterm season in the United States. From a macro standpoint, there’s little improvement occurring for the bottom 80% of the ‘i’ in the i-shaped economy, and I am watching tensions ratchet up in real-time in behaviors and sentiment that are making it past the online sphere now and into the real world.

In this evening’s Weekly Macro Note - we’re going to dive into the macro data ahead for the week, discuss the latest on the softening air travel trends, highlight the potential for higher vol in the coming weeks and months with the current state of the Nasdaq & SPY, and take a look at the four MacroEdge global bubble gauges. There’s a lot to cover, and the schedule this week will shift slightly with the labor data report dropping on Wednesday, and our continued travel schedule in effect for the time being. There are many exciting things happening for MacroEdge - so stay tuned for all of them as we continue to expand. With MacroEdge Ozone now fully migrated into the Substack ecosystem, you can get all our reports, research, data, portfolio strategy, and much more without the need for two logins and separate membership management… the feedback to this transition has been quite positive thus far, and you can experience Ozone through Substack for a week below:

Macro Data Ahead

Tuesday: NFIB Survey, Retail Sales

Wednesday: January Jobs Report (delayed release), Japan Market Holiday

Thursday: Existing Home Sales, Japan PPI

Friday: CPI, Japan Q4 GDP

Earnings >$500bn that are reporting:

KO

AZN

CVS

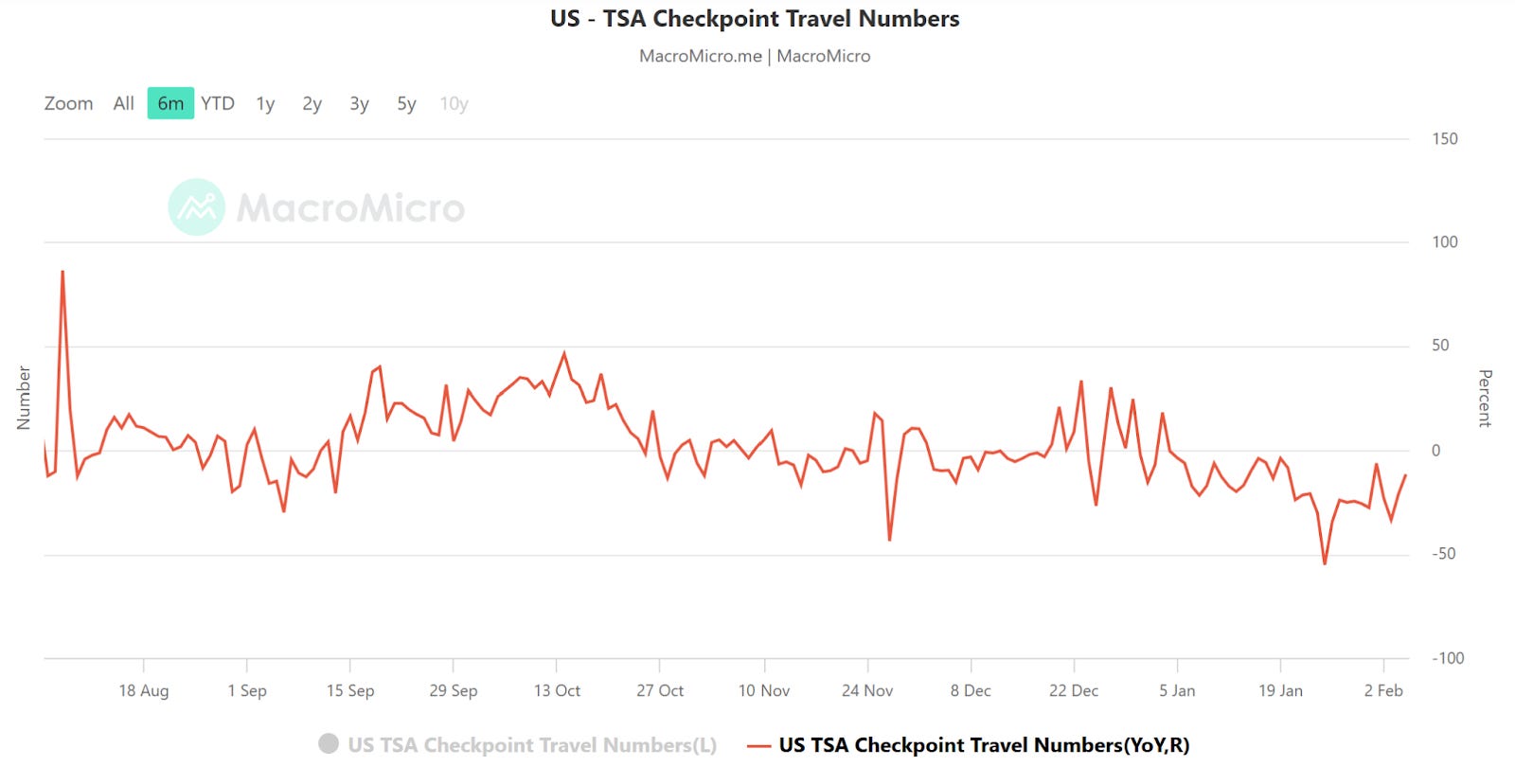

Air Travel Continues to Soften

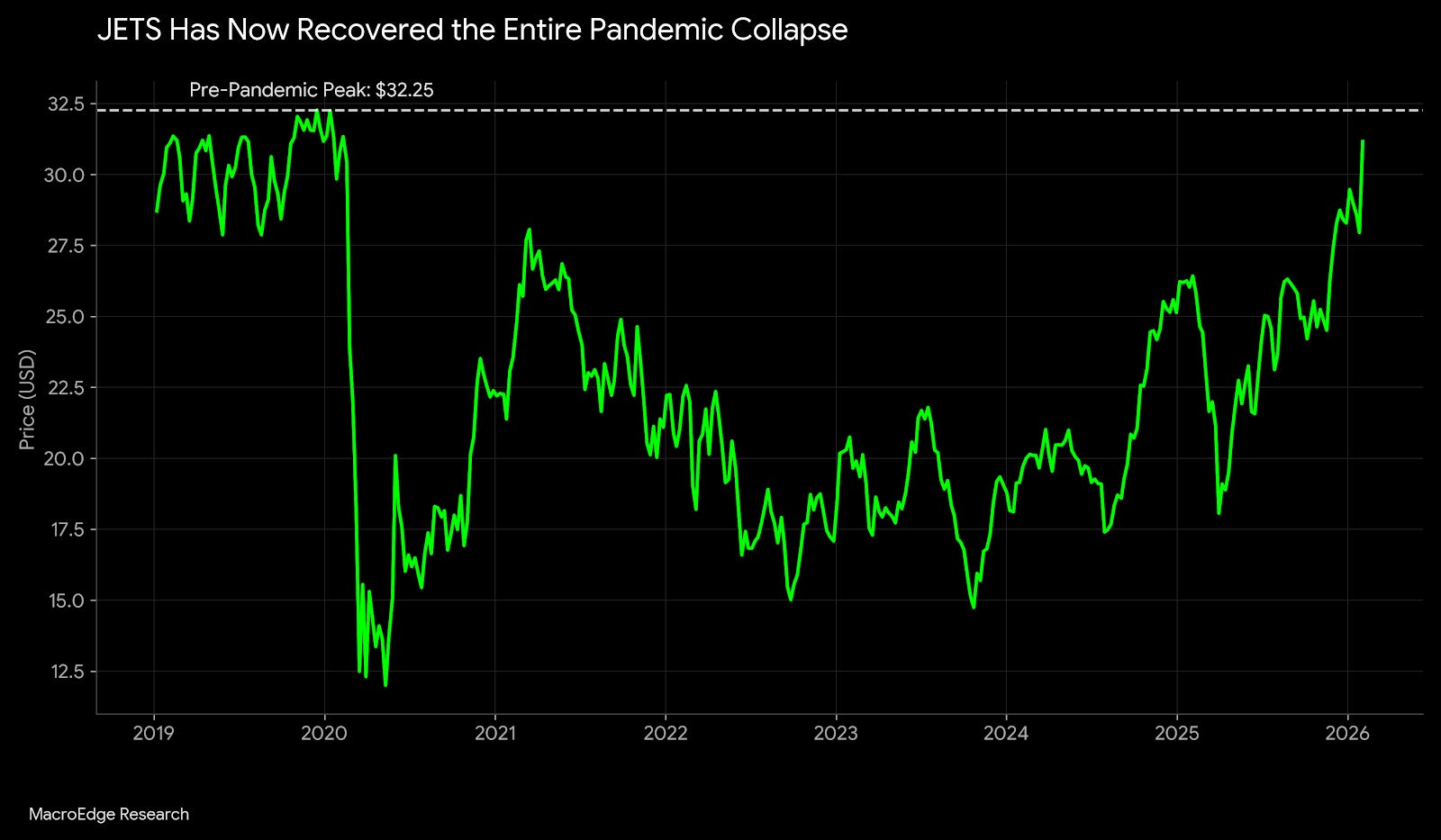

Following up on the hotel thematic in yesterday’s Macro Note - I am continuing to track air travel data closely as we head further into the 1st quarter. Thus far, a softer year continues to be realized, and air travel has been negative y/y for the entirety of the year so far. The decline hasn’t been hugely dramatic (outside of the ice storm related airport closures and delays), though we’re off about 11%.

The real-time data is not being looked at in the equity markets, and JETS made a significant move higher to end the week last week.

One or the other is in the wrong here, though stabilization at record high air travel levels isn’t a negative thing. A meaningful decline in passengers (yes, back to that i-shaped economy thing again) would likely result in this move in JETS and all of the carriers being reversed quite quickly. For the time being, the regional carriers (like RJET and SKYW) are also participating in the upside acceleration, and the most profitable carriers like DAL are benefiting greatly from the current environment. Even mediocre operations like AAL are seeing benefits from low fuel cost, high travel demand, expensive ticket prices, and positive tailwinds from rewards programs keeping people coming back to travel more via the skies.

Look at RJET:

And SKYW as two examples:

Volatility - Here There & Everywhere

This week has the potential for elevated vol again as we head into a jobs report, CPI, and much more. We got some volatility out of the very lackluster JOLTs report, and with Japanese yields acting up again, we are setting the foundation for another movement higher for vol. There remains plenty of catalysts to ‘light the candle’ though macro triggers thus far have not been enough for any material downside. They have been enough, however, to put us in a quicksand range for almost six months now.

(Continued below: Volatility - Here There & Everywhere, A Look at our Global Bubble Gauges, Report Schedule for the Week, Portfolio Strategy and Commentary Update, & more)…

Until/unless we start to see broadening in technology, this range is going to remain tricky - and the same goes for the S&P, which is forming somewhat of a rounded top on a zoomed out view:

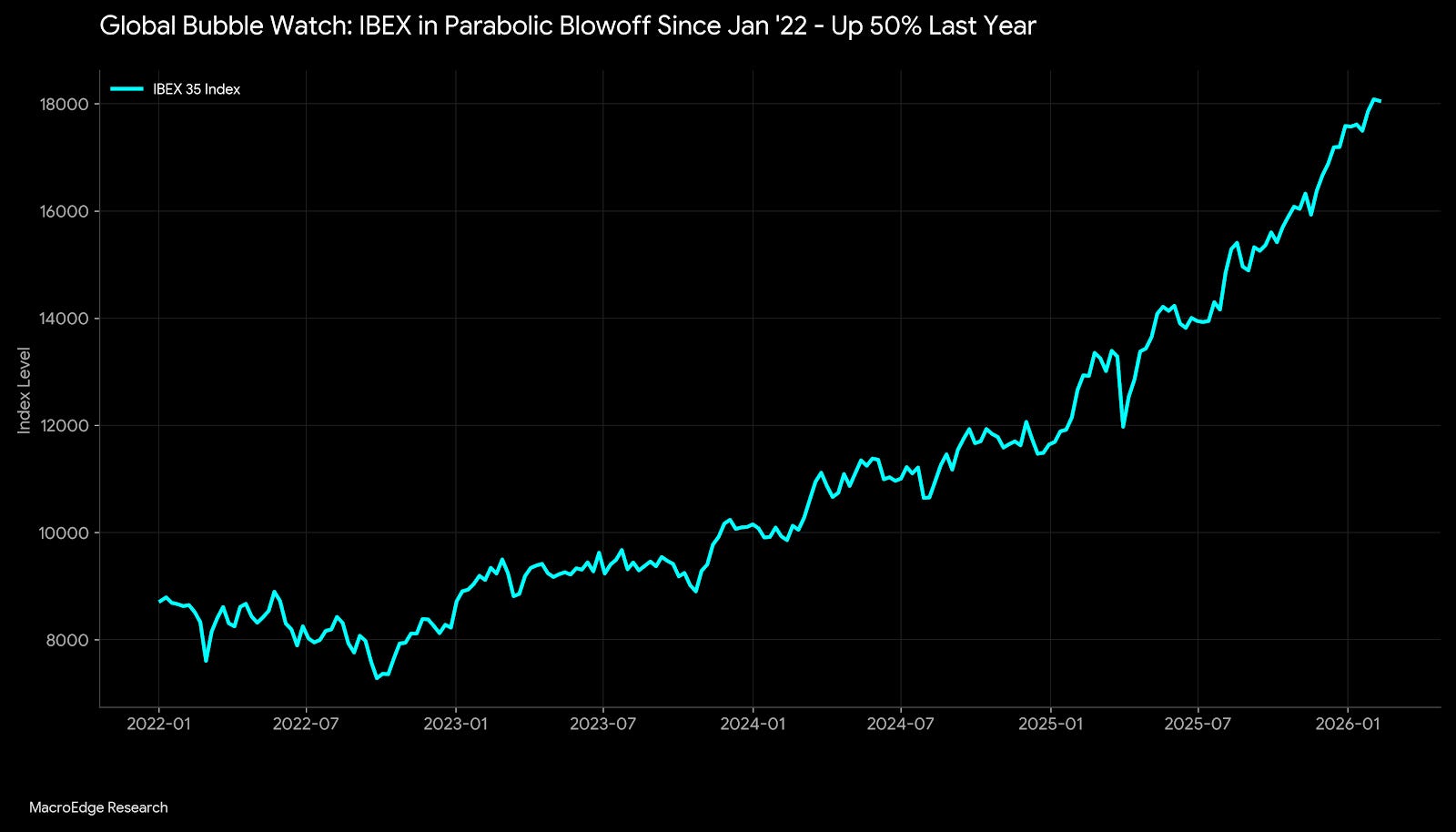

When the AI trade (AIS) finally fades, we will see meaningful downside in the Qs and SPY, but for the time being, it remains the name of the ‘game’ or ‘casino’ - whichever fits the current classification label better. Below, our update to the 4 current MacroEdge bubble gauges: the TSX, Nikkei, KOSPI, and IBEX, also adds color to this global bubble in risk assets. While we could turn elsewhere to places like South America and other East Asian countries that have seen historic rallies in recent months, these four demonstrate the close correlation of the ‘all-one trade’ thematic that continues to tighten around things like AI, the yen carry trade, liquidity/financial conditions, & much more.

A Look at our Global Bubble Gauges

The TSX, Nikkei, KOSPI, and IBEX comprise our ‘4-market global bubble gauge’ - highlighting extreme excess with little fundamental support to the moves, record high closes, and extreme overbought conditions across the board. While some of this is due to other factors like monetary debasement taking place - 2/4 of these countries are already facing demographic collapse.

Looking at the TSX, overbought conditions are near record-levels though the brief dip was already reduced to a blip on the radar. The TSX is not my favored gauge for when we’re likely to see these conditions globally roll-over, I hand that over to Korea, Japan, and Spain for the time-being even though the Canadian blowoff is impressive.

The candle print on the Nikkei from the initial election celebration is something right out of a circus.

At these record high levels supported by a weak yen, fiscal stimulus, and a spineless Bank of Japan - Japanese policymakers are terrified to do anything other - including tighten financial conditions. There are many reasons for that - but the Japanese, more than many others, are scarred by their ‘Lost Decade(s)’ periods which originally stemmed from massive speculation and then monetary tightening to quell said speculation. I think we’re in a similar situation today in the United States today as we saw Japan in the late 80s entering the 90s - though we have the quicker ability to turn on the ‘human QE’ migrant spigot - even though domestic pushback against this has continued to mount. It’s a very complicated dilemma we find ourselves in today…

Spain’s IBEX has gone full ‘bananas’ this year with a parabolic blowoff. This rally pushed the index up almost 50… yes, 50% on the year for 2025. Performance to start the year has been strong as well, and the IBEX is currently my #1 global speculative gauge for where things stand. When we see the IBEX roll over, I have a feeling we’re likely to see other things crack as well:

Viewed in non-technical terms:

It gets even dumber in Korea, which has more than doubled from January 2025.

Report Schedule for the Week

Tuesday: Midweek Macro Note & Employment Report Outlook (January)

Friday: Redeye Macro Note

Sunday: Weekly Macro Note and Portfolio Commentary

Below, Six will continue with the portfolio strategy commentary & update for the week, and I look forward to seeing you all Tuesday evening for our next

MacroEdge Portfolio Strategy Update - February 8, 2026 (@SixFinance, Head of Research)

TREASURY SECRETARY BESSENT: We are at the beginning of a manufacturing boom.

Green chutes are meaningfully emerging in cyclical equity prices. A deeper dive into ex-hyperscaler capex reveals no meaningful surge for 2026, and Trump’s $18 trillion investment declarations, when broken down, seem to hold no substantiation whatsoever. The largest counterparty economies of this investment “pledge” have “pledged” a multiple of their annual GDP. Manufacturing PMI respondents’ survey was downbeat, as has persisted for several years, despite the January headline number and the new orders surge. The US goods economy has broadly been downtrodden since rate hikes took the wind out of the markets’ sails.

Yet real economy stocks have surged. Cyclical equity prices appear to have troughed and are moving broadly north. Surprise indices of growth are surging. Freight volumes are breaking out to the upside.

This is a pivotal year for the administration heading into midterms, as Bessent looks to substantiate the reshoring of manufacturing proclamations that have been made for the last year. Without a durable boost to the manufacturing sector, the administration’s entire economic agenda is at risk as credibility is lost, not just with the public, but across financial markets. The OBBBA tailwinds, coupled with the administration’s attempts to start a reflexive manufacturing boom, usher in the potential for a durable boost.

The mechanism of action:

Forward guidance: Bessent signals to the markets that a manufacturing boom is beginning. Hyperscaler AI capex has kicked off the initial boost in pockets of the market, somewhat substantiating the claim.

OBBBA as the key policy lever: OBBBA structure provides substantial benefits to companies increasing their manufacturing capacity, with a key caveat - the production facilities must be completed and placed into service by the end of 2030.

Tariffs as a “pre-commitment” signal: The manufacturing boom heavily relies on global markets, believing that tariffs are durable and will remain in place.

Real GDP reacceleration: increase in GDP growth rate further reinforces the domestic “boom” narrative, driving increased capacity build through capex.

In order to grow our way out of debt, consistent with the administration’s stated mandate, they are attempting to use forward guidance and policy incentives to create a domestic investment boom in both the real and financial economy. The financial economy has responded positively well in advance, but the harder part of the process is yet to come: the real economy needs to respond now. Price action in cyclicals tilts towards an early-days reacceleration in the domestic real economy, also indicated by Q4 GDP numbers. The labor market remains weak, and the alchemy of economics being conducted by the administration against a large US debt load is a fragile balance. However, Bessent thoroughly understands, perhaps better than any Treasury Secretary the US has ever seen, the effects of forward guidance and policy levers on the economy and financial markets.

At the portfolio level, I will continue to run a large allocation in the chemicals sector. I believe that from current levels, many chemical companies deep in cyclical troughs offer the most upside to this theme as it continues to play out. To stay involved, I need to see the manufacturing data continue to improve. January data was positive, and inventories are very low, indicating a large restocking cycle ahead.

SWK is another name that appears to be beginning to inflect to the upside, also from a deep cyclical trough. This will likely be a key enabler to any meaningful industrial cycle, and one that I will be adding to the portfolio, as I look to then submit the overall thesis to the test of time.

For more details, please refer to our Terms and Conditions.

2025: Poland - 50%, Romania - 50%, Lithuania - 100+%