Weekly Macro Note: Global 'Crash Up' Index Update, Technicals Overview, Finding Opportunities in Inflation, Portfolio Strategy Update & Commentary

In this Weekly Macro Note - we dive into the latest 'crash up' index updates - discussing Korea, Spain, Canada, Japan, and US indices and their technicals, look at inflation opportunities, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

It’s nice to be back for another Weekly Macro Note, which will include the Macro Week Ahead, a discussion on our partnership with TREX, a technicals overview, and a look at our ‘Global Bubble Gauge’. We’ll also discuss how we continue to find opportunities in inflation as price pressures mount across the economy, and Six will provide a Portfolio Strategy Update.

MacroEdge Portfolio Strategy will be available in late June or July 2026, and will include all of our active portfolio strategies in one place.

On Wednesday, I depart for several locations in Texas for our first sector coverage in our ‘On the Ground’ series. Beyond excited to begin collecting findings in the agriculture sector, and our three focus areas for the trip should give us all (including me) a very interesting context and background to the entire ag situation. There are a lot, lot, lot of clickbait headlines and titles swirling around in the press and on X right now - so we’re going to actually discover what’s real, and what’s not. By connecting with farmers and people at the source directly, we hope to uncover portfolio strategy opportunities… the movement in the soft commodities (and fertilizer) in recent days gives us a nice place to pull the trigger from if the opportunity is actually there, and we’ll know much more after the coming week of discussions, data collection, and anecdotes. If we find horizontal trades not directly in the three major areas we’re targeting, equally as positive in my mind.

In the futures open, the markets remain largely muted, there were a few headlines - notably the launch of ‘Project Freedom’, which aims to help ships navigate the Strait of Hormuz amidst the latest targetings by IRGC assets. We’re approaching 2 months of the Strait of Hormuz being almost completely closed - and the ramifications from that are going to be enormous, even though we aren’t feeling the full force of the storm at the current moment. In the oil markets, spot WTI is roughly flat after an initial sell-off, and continues to look incredibly constructive. In the West, there are few signs of demand destruction at this price level, and I remain net bullish on the sector with WTI prices this high. At $100/bbl - the amount of FCF machines is immense, and the tailwinds continue to blow in the favor of these companies the longer prices stay higher. It’s going to take a couple of months at minimum just for traffic flows to get to half of their former levels in the Strait - and that’s not an event I anticipate occurring this week. Inflation for the time being remains net positive for speculation and equities - and there remains a relatively narrow choice palette for investors to hedge against inflation (especially as real estate price gains continue to slow).

This week, we’ve got markets closed in Japan for a few days, and in the US, more macro data that is going to continue to paint a very mixed picture. I continue to observe the energy data on both the inventory and frac front to see if there’s any additional activity happening there. Inventories are going to continue to plummet in the US as we’ve ramped exports up to all-time highs, and the SPR is likely to be at all-time low levels in the next 3 months. Earnings this week are reserved for the sub-$250 billion market cap companies, and we’re going to continue to see markets revolve largely around the oil/commodity/inflation picture & headline-induced volatility.

Oil working on the ‘right’ handle to the cup…

Expect the ‘crash up’ to continue as the Fed balance sheet expansion ramps up, and little is done to combat CPI from running at a 4-5% clip on a YoY basis.

Our team appreciates your support during our 24/7 coverage of the events in the Middle East and so much more. If you haven’t yet subscribed to Ozone, you are missing out on all of our research, data, portfolio strategy, (colorful) commentary, and so much more, upgrade below:

The Macro Week Ahead

This week is another major earnings week, and there’s some macro data we’ll also cover as the week progresses. Friday, we’ll get employment data, but I think the CPI data for April is going to be a lot more interesting than the employment data.

Monday: Factory Orders (US),

Tuesday: JOLTS (US), Bank of Australia Rate Decision

Wednesday: ADP Employment (US), EIA Oil Inventory (US)

Thursday: n/a

Friday: Average Cash Earnings (JP), Nonfarm Payrolls (US)

For earnings of companies >250 billion market cap: n/a

TREX Oil and Gas Partnership Discussion

On Tuesday evening, we’ll have an update on our exciting partnership that is developing with TREX.

Portfolio Strategy - Arriving June/July 2026

MacroEdge Portfolio Strategy, led by Six, will be available late June or July 2026. We’re already experimenting with this offering through two core portfolio strategies you’ve likely been seeing the last few weeks - and this offering is only going to continue to take a more solid shape over the next couple of months:

Technicals Overview - Global Bubble Gauges

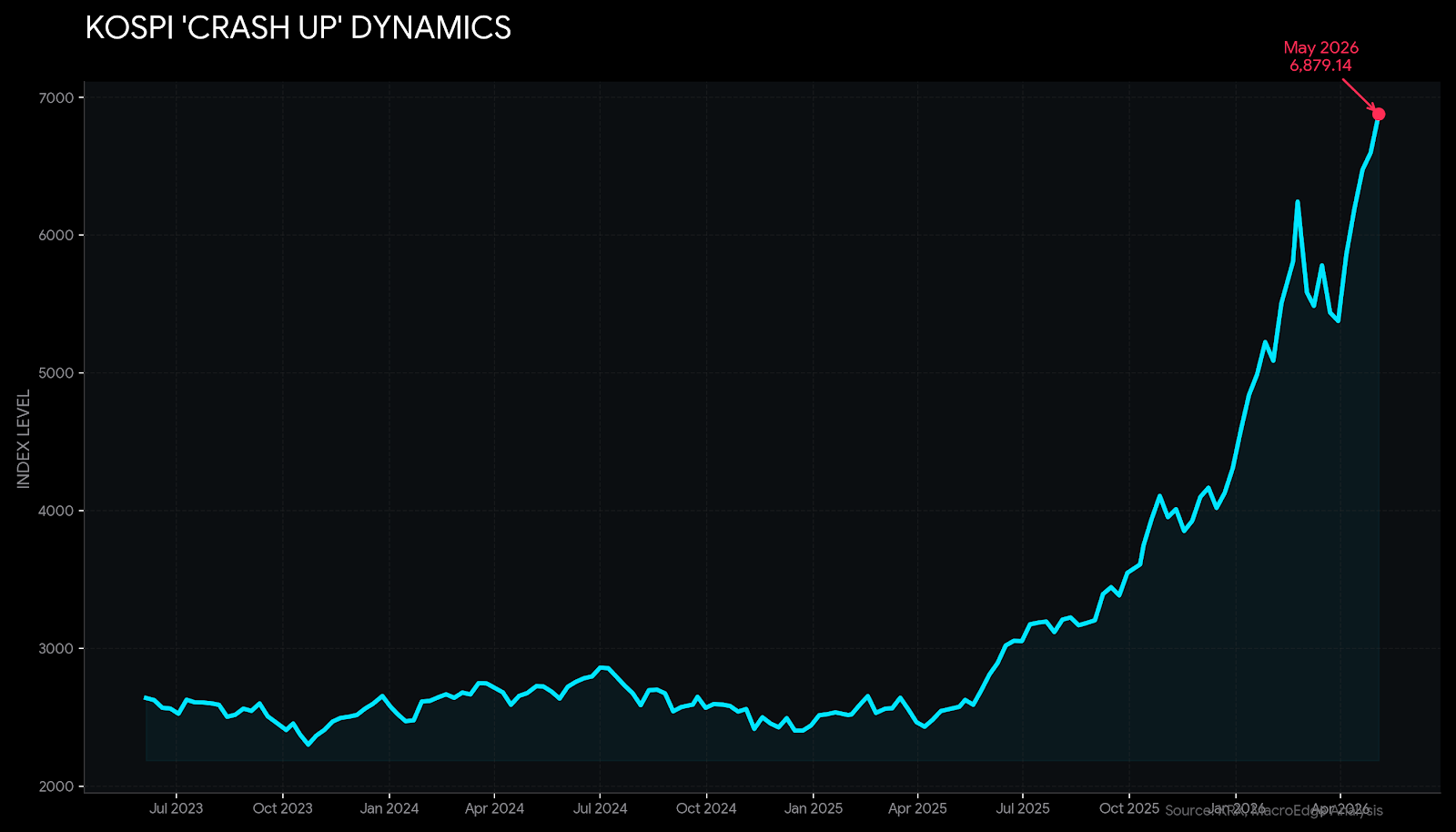

In looking at the latest update to our ‘Global Bubble Gauges’ - the pro-inflation and asset melt-up regime continues in this historic equity bubble. Our ‘Global Bubble Gauge’ consists of the Nikkei, KOSPI, IBEX, and TSX with a weighting by market cap in USD terms. None of the indices are signalling major red flags at the current time. At the individual index level, the TSX is lagging now, and in the crypto world (another good liquidity proxy - Bitcoin has ticked above $80,000 again). We’re likely witnessing a 200dma test, and nothing more for the time being.

In Japan, markers are on holiday for the first three days of the week.

For the TSX - we’ve yet to see the index make a new high since February:

Spain - still no new high - but not far from one (IBEX):

Korea’s KOSPI is up another 5% and continues a parabolic meltup as their currency weakens to near record levels vs the dollar.

The index has more than tripled since 2023.

While I prefer the IBEX as our best proxy and signal for the Nasdaq and other high-beta indices globally - our basket provides us with useful signal as to when we can expect things to finally roll over more broadly around the globe - and for the time being, the picture is mixed as Korea and Japan continue to ‘crash up’ while gains in Spain and Canada have slowed for the time being.

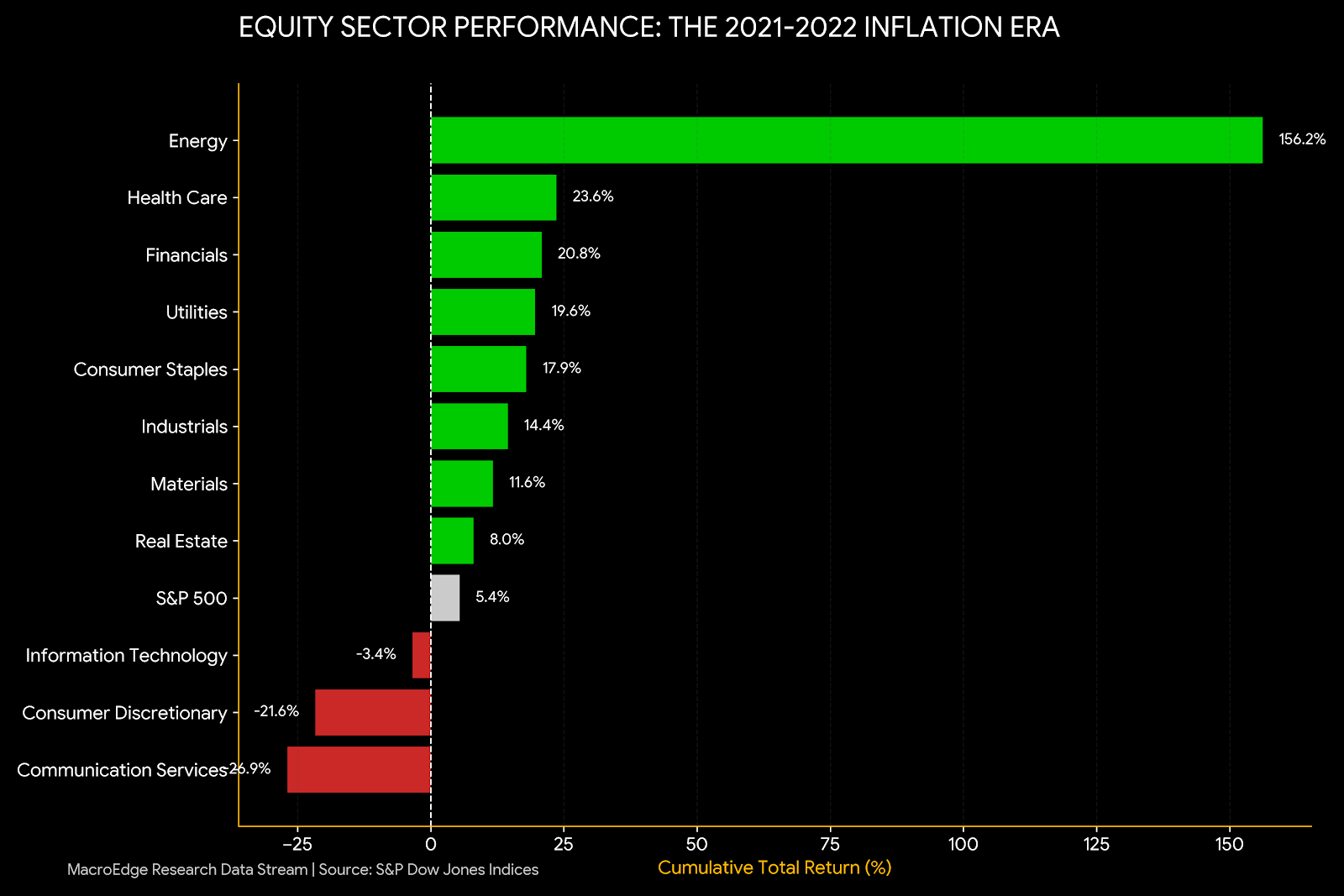

Finding Opportunities in Inflation

Historically, and specifically during the 2021-2022 cycle, the strongest equity opportunities are found in sectors with high pricing power and direct commodity exposure:

Energy (The Scarcity Hedge): Oil and gas firms are the primary beneficiaries of supply-side inflation. As energy prices drive the PPI higher, these firms see immediate revenue expansion.

Defensive Value (Consumer Staples & Utilities): Companies providing non-discretionary goods (food, power) can pass through cost increases to consumers with minimal demand destruction.

Materials: Miners and chemical producers benefit as the nominal value of hard industrial commodities (Copper, Aluminum) surges.

Short-Duration Cash Flows (Value over Growth): High inflation forces central banks to raise interest rates, which increases the discount rate on future earnings. This devalues “Growth” stocks (whose value is in the distant future) and favors “Value” stocks with current, stable cash flows.

Real Asset Exposure: Exposure to the underlying real assets like farmland, oil and gas assets, mines, and more, which are all beginning to outperform again

For commodity performance by type:

(Continued below: Finding Opportunities in Inflation Continued, Report Schedule for the Week, Portfolio Strategy Update and Commentary - Six)…

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.