Weekly Macro Note: Geopolitical Update, Data Center Situation Part 2, Portfolio Strategy Updates, & More

In this Weekly Macro Note - we discuss the latest geopolitical developments, highlight the upcoming 'On the Ground' Data Center report series, discuss portfolio strategy updates, and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers and Community,

This evening - futures are off to an expected start - and largely in line with how weekend CFDs and other instruments like cryptocurrencies were trading when the news of a ‘no deal’ announcement was dropped by the Vice President. On top of that, the President announced this morning that the US Navy will begin enforcing a new blockade against all vessels that attempt to enter or exit the Strait of Hormuz. Given that the announcement was made for local time, which will take effect shortly, and we’ll have to see if that results in a further flare-up of tensions here as we begin a new week in the conflict. The Strait of Hormuz has now been closed for much longer than anyone expected, and traffic is at an absolute standstill - with no reported tankers leaving the Strait today since the announcement from Trump. The situation gets even more complicated on the insurance front, as insurance companies have no interest in writing policies given the current situation, so even if the Strait is ‘open’ at some point, it’s going to be up to the insurance providers to really decide when that is, and not yet governments on either side. Given that there will be a double blockade starting in the next few hours, I don’t think we need to worry about the insurance discussion yet.

Additionally, we saw the Houthis test the waters (literally) this morning, running out a skiff to spook a container ship, and the UKMTO issued a warning about this event. Overall, futures are sort of in the ‘sweet spot’ point for now, panic announcements from the Administration - with the key two metrics being oil prices and yields… You can view the past intervention points when the 10Y reached interim peaks over the last year (such as with the tariff announcement), though things are now different with oil as high as it is. The inevitable outcome in a situation that’s being largely driven by oil prices is demand destruction - and even though I’ve heard a few economists cite the 2011-2014 period as a ‘sustainably high price’ - the economic backdrop was extremely different that the point coming out of the worst economic situation in a century - rather than the backdrop we find ourselves in today with assets still at an all-time high, inflation still running hot (3.3% annualized in the March CPI - likely to tick up to 3.7-4.0%, and retail investors piling in weekly at rates that have never previously been seen.

The right tail scenario to get to those demand destruction levels remains largely in play - though I do expect there to be more constant questionable announcements throughout the week on all sides, especially as we head into a… double blockade of some sort. If we see military action resume, the next likely escalation step on the part of the Iranians is a closure of the Bab Al-Mandab Strait in the Red Sea through their Yemeni proxies, and the escalation ladder again seems quite defined. This evening we’re going to cover the following:

TREX, Partnering with MacroEdge Intelligence

Macro Week Ahead

Geopolitical Update - The Latest Details That Matter

Data Center Situation Pt. 2

Energy Portfolio Strategy Update

Not yet a MacroEdge Ozone subscriber? Upgrade below and get all of our research, reports, data, portfolio strategy, and much more below…:

TREX, Partnering with MacroEdge Intelligence

We’re pleased to partner with TREX to identify opportunities in the oil and gas arena. As an overlooked and oftentimes hated asset class, we’re firmly committed to a key sector that operates as the backbone of both the US & global economies.

More information will be available on this partnership and our plans on 4/24 in the Redeye Macro Note.

If it sounds like we’re doing about 12 different things - that is not an inaccurate statement - my goal is also to keep it organized for you all, and in a dedicated report this week or next, we’re going to put everything out there on the Macro Research side - including with our partnership with TREX to make it clear.

Macro Week Ahead

This week kicks off the official Q1 earnings season, and we’ll get more inflation data following the recent energy price spikes. On the macro data side of things, it’s relatively quiet outside of PPI, so I expect that war news, headlines, and actions will continue to dominate market action, alongside oil. Though we’ve seen some decoupling between the SPX & CL, it likely comes back into play if oil starts to creep back into the higher ceiling intervention range (around $113-$120/bbl) currently, as that will put upward pressure on yields.

Monday: Fedspeak, BoJ Ueda Speech

Tuesday: Producer Price Index (PPI)

Wednesday: Beige Book

Thursday: Claims

Friday: n/a

Earnings-wise >$500bn market cap

JP Morgan (Tuesday)

J&J (Tuesday)

Geopolitical Update - The Latest Details That Matter

The U.S. “Impartial Blockade” of Iranian Ports Following the collapse of 21-hour ceasefire talks in Pakistan, President Trump has ordered the U.S. Navy to begin a total naval blockade of all ships entering or leaving Iranian ports. CENTCOM confirmed the enforcement will begin on Monday, April 13, at 14:00 GMT. Crucially, the blockade targets vessels that have “paid an illegal toll to Iran,” marking a direct challenge to the IRGC’s $2 million-per-ship protection plan. It remains unknown if US assets are in the Strait to actually clear mines, though our best sources say that is not a process that was started (and/or) completed).

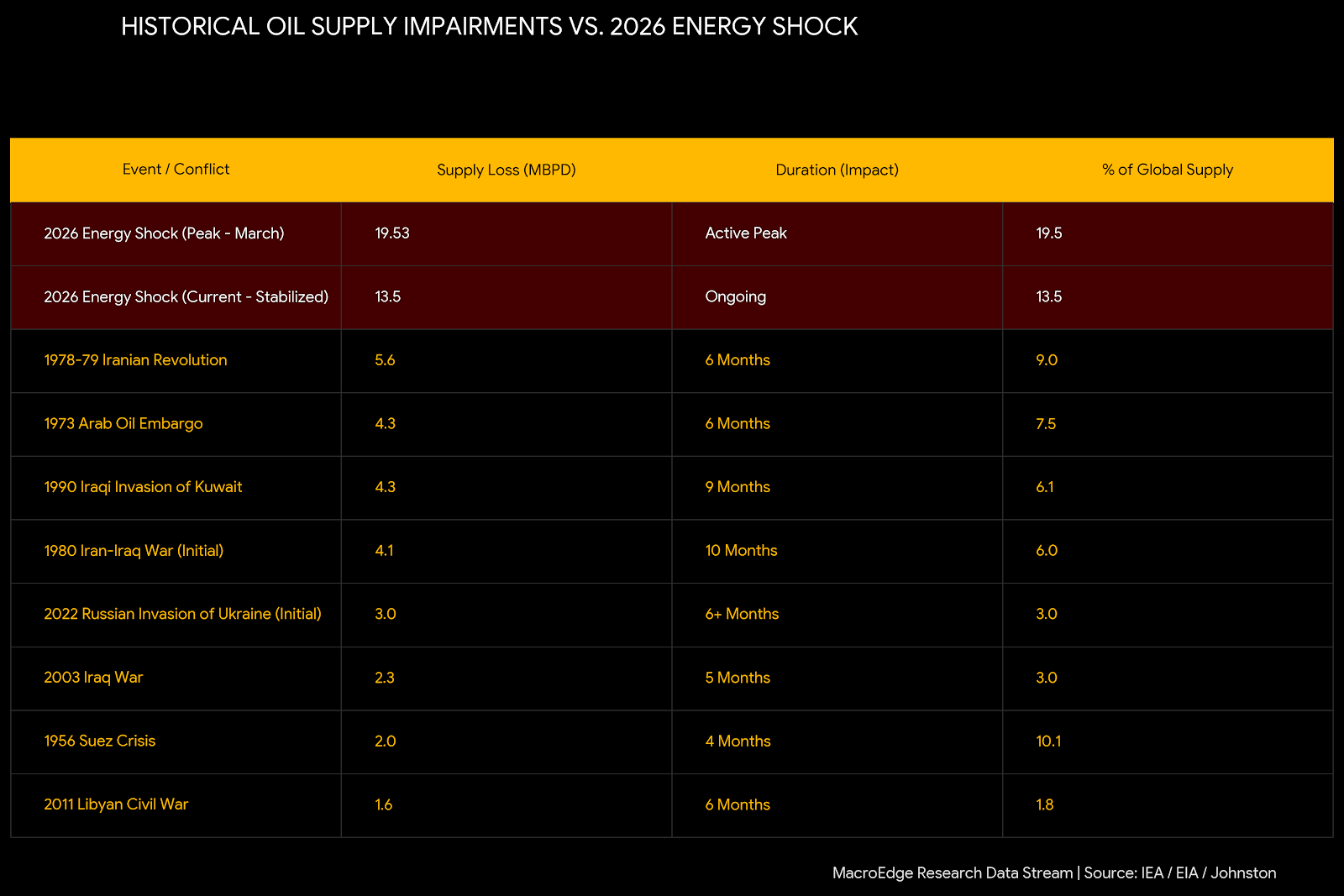

Strait of Hormuz: The “Controlled System” Fails The Strait remains under “smart management” by the IRGC, effectively closed to all but “Iranian-approved” vessels. As of April 12, only one commercial vessel successfully transited without Iranian coordination by skirting the southern edge of the hazardous area. While the 10–15 ship window was intended to drain floating storage, HFI Research and Johnston indicate that the corridor has not returned to normal commercial routing. 13.5 MBPD remains effectively offline as Gulf producers (Saudi, Iraq, UAE) await predictable, un-tolled access.

Red Sea Escalation: The Bab el-Mandeb Threat with the Islamabad talks failing, Iran has signaled a potential “horizontal escalation” by instructing Houthi allies to shutter the Bab el-Mandeb Strait. This effectively weaponizes both major maritime chokepoints simultaneously. Major carriers (Maersk, CMA CGM) have moved back to “Red Alert,” canceling planned returns to the Suez Canal and rerouting via the Cape of Good Hope. This diversion is absorbing approximately 2.5 million TEU of global capacity, ensuring that freight rates remain decoupled from historic norms through Q4 2026.

The latest table below highlights the continuing impairment - even with offsets from the Saudi East West Pipeline, Iran’s Northbound pipeline to China, & more…

Not yet a MacroEdge Ozone subscriber? Get access to Ozone:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.