Weekly Macro Note: Early Warning Signals, The Real Story for Oil, Shortages on the Horizon

In this Weekly Macro Note - we discuss early market warning signals in the technicals, take a look at the Global Bubble Index, highlight the real story for oil, cover shortages on the horizon, & more

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

This evening we’re back to wrap up May and head into June during this continuation of an ‘asset melt-up’ that is pushing retail past an ‘all-in’ mode that we last observed during the 2021 period. Jawboning and other government interventions have managed to keep WTI around the ~$90/bbl level, while financial conditions are being kept extremely loose alongside AI earnings tailwinds that are driving an all-out parabolic move in semiconductor equities. While signs of slowing continue to emerge in the real data - especially with things like the data center buildout - the timing instrument remains greatly elusive as we continue to see our Global Bubble Index push to new highs. The phenomenon is not limited to the United States, as Korean, Canadian, Spanish, Chinese, & other equity markets continue a vertical move upward. The reality is much more complex than this being a simple net positive signal that good things are happening in the economy, because under the surface, as we’ve analyzed for the better part of two years, we’re seeing GFC-style delinquency.

This is very much looking like the ‘all-in’ bubble in everything: consumer credit, private credit, student loans, equities, equity leverage, etc., and it does not look like it is going to stop in the interim until a shock event (potentially oil inventories hitting tank bottom?) actually shifts the mood on the matter. The pro-nominal price inflation regime, which is fully in charge of the current environment, knows very well that they cannot stop the party for the dot on the ‘i’ within our ‘i-shaped’ economy - even as the bifurcation grows more and more extreme.

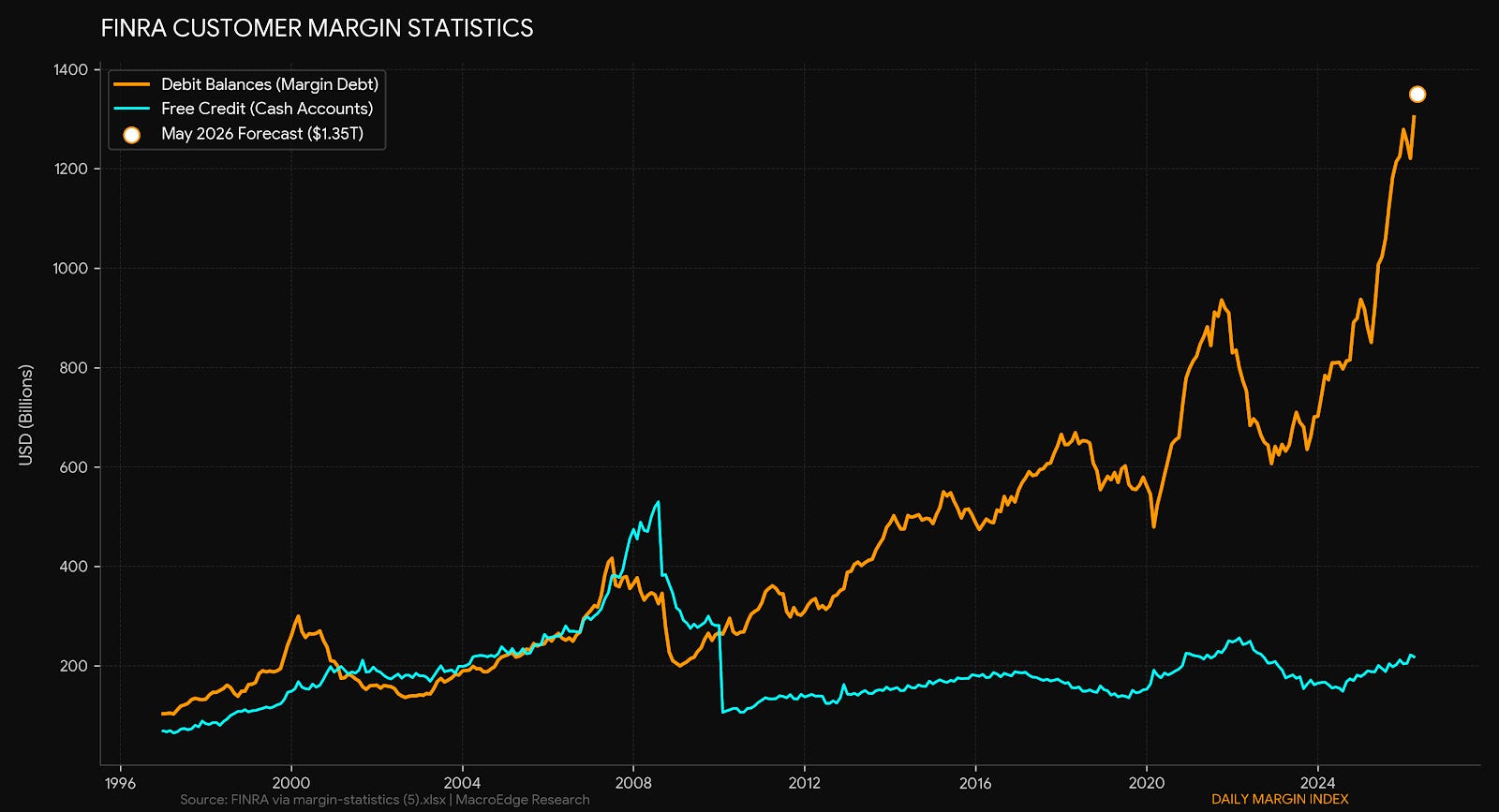

Just look at margin debt:

Again, not an indicator that matters until it actually rolls over, and that is not happening for the time being. There are excuses across X and the ‘Fintwit’ world right now why this environment is going to continue forever - and we’re quite close to the permanently high plateau period that Irving Fisher once outlined so eloquently during a previous period that shares many resemblances.

At the futures open - oil (spot WTI) is at about $92/bbl - equities are flat across the board, and crypto is down slightly today. The pain range for markets is a return >$100/bbl WTI for oil - and the setup as outlined below is really a constructive one if acute shortages begin hitting global economies from June onward. Iran is sitting with significant leverage right now as it pertains to global energy markets - and they know that the longer they can hold out and keep countries running down emergency supplies, the worse prices will get on a longer-term basis.

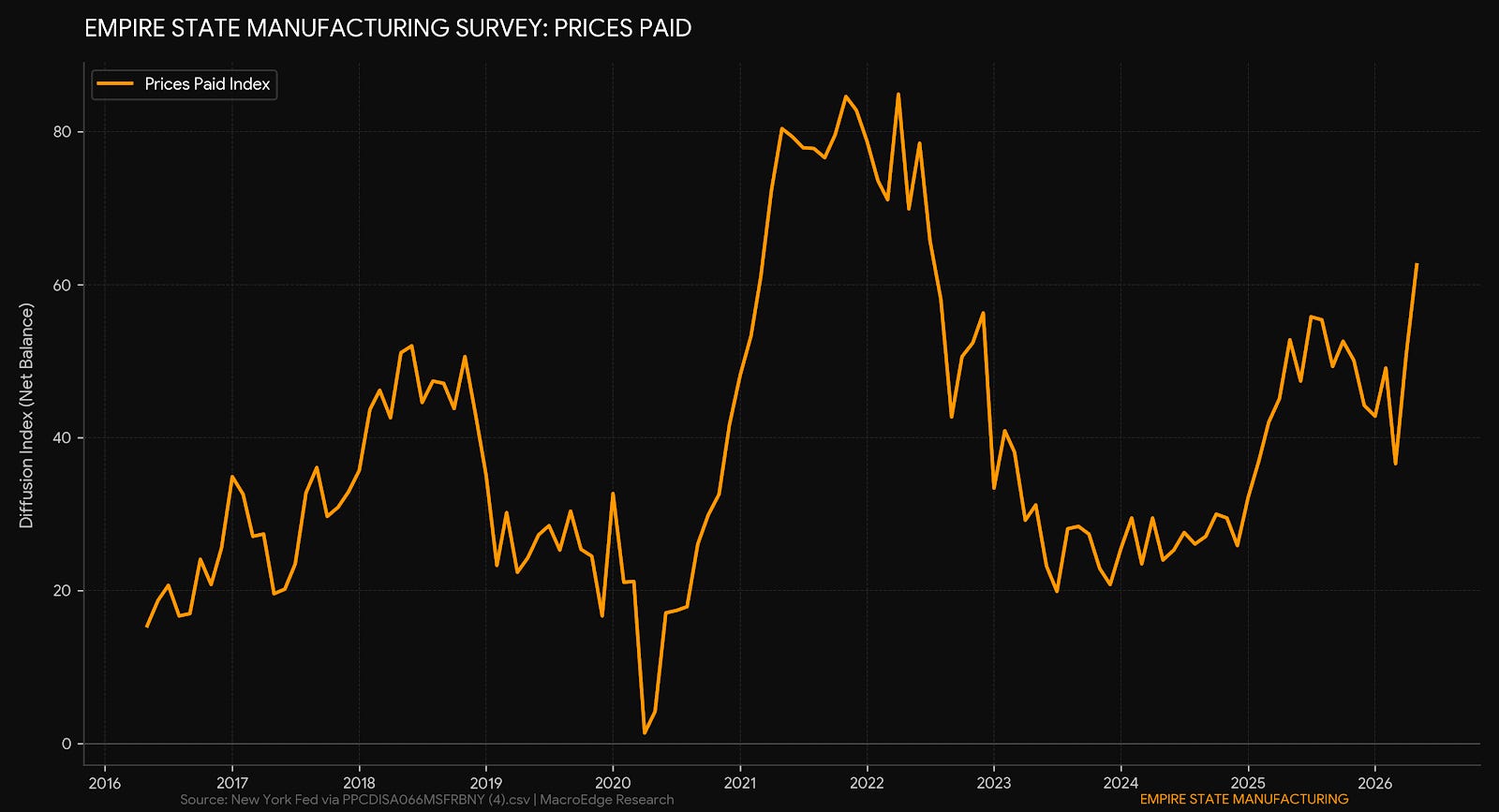

Prices paid are sending mixed signals, but directionally, we continue to move higher - especially for producers:

Not yet a MacoEdge Ozone subscriber? Upgrade below to get all of our research, data, portfolio strategy, and more:

Macro Week Ahead

This week is another mixed bag in terms of the importance and relevance of the macro data. Markets have largely enjoyed much higher inflation to this point - largely stemming from the Strait of Hormuz closure - but a long-term supply shock is not going to be a positive catalyst forever.

Monday:

Fed Chair Kevin Warsh statement

ISM Mfg PMI (May)

Tuesday:

JOLTS

Wednesday:

ADP Private Payrolls

ISM Services PMI

Federal Reserve Beige Book

Thursday:

Initial Claims

Friday:

May employment report

For earnings >500bn this week, AVGO is the lone name. I expect that it is not this week that we start to see things get worse yet, but over June and by late June, I expect that the acute shortage discussion becomes more relevant if the Strait remains closed, which is looking more likely.

A Preview of the Second Half of the Year

For us, an organization, I will provide a critical update on Wednesday regarding changes to our product offerings and mix for the second half of the year. Importantly, we will be expanding our footprint with a new location in Southlake, TX, which will enable us to continue and expand our service to our oil and gas customers across the state of Texas and beyond.

Stay tuned for that Wednesday update, and I am departing shortly to begin several days of discussions regarding changes to what we offer.

The Latest Geopolitical Developments

This weekend has been much of the same from a geopolitical standpoint - no real signs of a deal, more fake headlines and fake news (like news of a resignation from Iran’s President which turned out to be false), and the saga continues.

Trump Toughens Terms, Halting Near-Deal: Just as negotiators appeared to be approaching a formal memorandum of understanding (MOU), President Donald Trump announced he was in “no hurry” to strike a deal. Citing deep concerns over specific clauses that would unfreeze restricted Iranian assets, the White House significantly toughened Washington’s terms, causing the peace agreement to fail to materialize over the weekend.

Irreconcilable Disagreements on Nuclear Sequencing: The core structural roadblock remains a fundamental impasse over nuclear commitments. The U.S. demanded firm, upfront verification and the complete extraction of Iran’s Highly Enriched Uranium (HEU) stockpile. In contrast, Iranian officials flatly refused to transfer their HEU outside the country or lower enrichment limits, viewing zero-enrichment demands as an absolute red line while aggressively demanding upfront economic concessions.

The Sovereignty Battle Over the Strait of Hormuz: Reopening the critical maritime artery remains deadlocked due to conflicting sovereign demands. Iran insists it will only permit civilian shipping to resume under exclusive “Iranian arrangements” and regulatory traffic systems, which it views as its ultimate geopolitical leverage. The U.S. has explicitly rejected any framework involving an Iranian fee system or restricted navigation, maintaining that full freedom of navigation through the international waterway is non-negotiable.

Iran Exploiting the Truce to Reconstitute Military Sites: Adding to Washington’s resistance, freshly analyzed satellite imagery revealed over the weekend that Iran has been actively using the recent ceasefire windows to execute tactical military expansion. Significant reconstitution efforts were identified at the Yazd Missile Base, reinforcing intelligence assessments that Tehran is exploiting diplomatic pauses to shore up its operational capabilities.

Domestic Political Pressures on Both Sides: Domestic political dynamics crippled the closing stages of the talks. In Tehran, a powerful faction of hard-liners inside the Iranian parliament and the Supreme National Security Council launched aggressive public campaigns to undermine President Pezeshkian’s negotiating team, slamming any potential compromises with Washington. Concurrently, U.S. negotiators faced intense pressure from defense think tanks and hawkish congressional factions demanding nothing less than a complete, permanent ban on Iranian uranium enrichment and missile development.

The Global Bubble Index - Charging Higher Forever?

Our global bubble index (KOSPI + IBEX + TSX + Nikkei) is showing no signs of cracking yet. Until this shows signs of cracking/rolling over, I would be very careful fighting this trend… even with how ridiculous it has become.

For the KOSPI & Nikkei - still no signs of slowing, though breadth warning flags are becoming more apparent:

Spain is either setting up for another massive leg higher in this consolidation pattern, or for an impulse move lower - no real in-between on this setup:

Canada continues to move higher as well, even as its real economy suffers a recession:

For Bitcoin, the current price environment has completely separated from the equity action, which has been driven almost entirely by gains in AI/semiconductors.

Pretty decent chance that this divergence turns into a correction/downside over the next 30-60 days in the semiconductor space.

This global monetary environment is creating massive bifurcation, and I expect that the melt-up in everything continues as the everything bubble continues. This is going to surpass Dotcom and represent a combination of warning signals surpassing anything that we’ve seen across cycles in the past.

Semiconductor technicals are showing some early warning signals, but nothing to act on.

Look for a day that signals an environment change (crack), like a 5-7% downside move, which may signal a shift in sentiment that will spook out some of the retail insanity that we’ve seen the last few months.

What’s the Scoop for Oil and Gas?

The dynamic in oil and gas since the last move to the $107/bbl level or so has been quite ugly. As soon as that pushed bonds low enough for the Administration to start to ‘panic’ again, we’ve seen an unrelenting level of intervention in financial markets, primarily in oil, to push yields slightly lower for the time being.

(Continued below… what’s the scoop for oil and gas? - continued, the turn of the tide - Six, portfolio strategy… Marigold, LBJ, and Tehran - John Galt)…

Not yet a MacroEdge subscriber? Upgrade to Ozone below to get all of our research, data, portfolio strategy, and more, below:

The setup is mixed - there are really two key technical potentials now - though the one I think is most relevant is the Strait remaining closed through June for the time being. This area for WTI has acted as a huge demand zone over the last three months - and I do expect that if we were to break to the downside (which right now has very low odds), then WTI will sink further. The setup that looks more likely is a return to the upper end of this range band:

We made key adjustments to the energy portfolio strategy last week - cutting SND and KGEI for the time being - and reducing exposure in ACDC. I don’t like the fact that E&Ps are starting to even marginally get rig count higher given the current global war on oil prices by governments.

A return to the $110/bbl level is in order if the shortage narrative enters the news cycle (and people actually start paying attention to the data)... The fact that markets have been intervened in to this significant degree is concerning because real supply and demand signals have not been transmitted that would actually contribute to demand destruction. I guess right now the plan is to run the clock down to the very last second - which they likely know around when that is - and see if they cannot pull off some bargain or deal. Structurally, I am still bullish on the entire commodity sphere, regardless of developments in Hormuz, and with each passing hour, stories of normalization will only become more distant.

I really think until there are actual shortages and people have to pay consequences - very few will care - thinking that commodities simply fall out of the sky on a day-to-day basis (at the pump, grocery store) or wherever, so keep that in mind… On the semiconductor insanity front - look for signs of an intermediate topping process if we get one - that will mark a shift in the forward outlook for the sector - there are plenty of reasons under the hood for why we may begin to see that.

The Turn of The Tide (@SixFinance, Head of Research)

The Speculative Regime is Intact and Broadening.

The environment remains ripe for speculation, and the character of that speculation is changing in a way worth front-running. The thesis I want to lead with, because it is the one most likely to be wrong, is that this is late-cycle melt-up behavior, and chasing laggard rotations into a tape that has already re-rated the leaders is precisely how you buy the top. I do not believe that the top is in, and fundamentals may later inflect should economic conditions improve and inflation recede. I am ready to be proven wrong, and will revisit the thesis the moment that breadth deteriorates rather than improves.

The laggard basket I led with weeks ago - ORCL, NOW, QCOM - is inflecting on schedule. QCOM saw the meatiest move and in my view has now largely discounted its fundamental inflection before the fact. When this happens, and the good news is pre-emptively priced, the easy money in that name is behind you, and the marginal speculative dollar starts hunting for the next “not yet discounted” home. I have high conviction in QCOM’s fundamental inflection, but only moderate conviction that QCOM has significant upside from here.

DELL

Dell is a perfect example of the current market regime. A blowout quarter reported tonight led to a 30%+ gap higher in overnight trading. This move structurally resembles ORCL’s late 2025 surge, the one that later more than fully retraced. The takeaway is not “short DELL”, but that the speculative engine is running hot enough to gap an already up triple digits on the year name over 30% higher after hours, and that energy will not stay contained in the names that have already moved. This is a bridge to the real trade, and the hot money flowing into the market, as evidenced further by NBA players increasingly taking to Twitter to share their investment theses on AI and robotics.

Beyond Tech

After going long CAI recently, the move I am watching is the spread of speculative capital out of the mega-cap AI complex and into sectors that have been left for dead. The single most compressed, most hated, most un-owned major sector in the index right now is healthcare. And the catalyst that could un-stick it is the one thing the market has spent two years pricing exclusively into semiconductors and hyperscalers: artificial intelligence.

The market has paid up enormously for AI as a cost-and-compute story, or the “picks and shovels”. It has paid almost nothing for AI as a therapeutic output story, which actually discovers and commercializes the drugs the compute is supposed to produce. When those two narratives reconnect, the re-rating likely accrues to the cheap side of the trade.

On a relative forward PE basis, the S&P 500 Healthcare sector is near its lowest relative valuation to SPX in three decades. This de-rating was driven by multiple overhangs, including Medicare price negotiation, pharmaceutical tariffs, “most favored nation” fears, patent-cliff anxiety, and a multi-year capital rotation into AI and tech that have starved the sector of marginal flows.

Core Thesis: AI Arrives in Therapeutics and Genomics

Healthcare is far from my personal edge, and my positioning reflects that. The structural argument however, does not require me to pick molecules; rather only that the market begins to re-rate the sector’s innovation premium as AI compresses the discovery timeline. This is the same innovation premium that has been bleeding out of the relative multiple for years.

Catalyst Stack

DeepMind’s Isomorphic Labs raised a $2.1B round in May 2026 and now guides its first AI-designed drugs entering clinical trials by end of the year.

Nvidia and Eli Lilly stood up a $1B AI lab with dedicated infrastructure aimed squarely at drug discovery foundation models. The picks and shovels vendor is co-investing into the output layer. The output layer is likely to be re-rated.

Insilico Medicine pushed a fully generative AI-originated molecule into Phase 2 trials. The proof-of-concept risk in “can AI molecules reach trials” is now largely retired. The open question now is hit rate and final approvals, a massive step forward.

The counterpoint to the argued points is that although AI may accelerate the discovery phase, it is unlikely to compress the years of clinical validation required in drug trials. The fundamental payoff is therefore longer dated, but luckily, equities are a long duration instrument. Therefore, at this stage, this is a trade on the re-rating of the sector, not the FDA process.

Because this is outside my circle of competence at the single name level, I am expressing it through two thematic vehicles rather than concentrated stock bets, and sizing up the exposure while deliberately diversifying away the idiosyncratic biotech risk I have no edge on.

Those vehicles are:

IDNA - Tracks an index of global developed and emerging market companies positioned to benefit from long-term innovation in genomics, immunology, and bioengineering. It is a passively managed product, following a Factset index.

ARKG - This is the higher octane vehicle and, in my view, the best speculative beta to the theme. Actively concentrated in DNA sequencing, gene editing, and AI-enabled diagnostics with a much smaller average market cap than IDNA. In a genuine sector re-rating, it has the highest leverage to this theme. The problem, bluntly, is the manager. Cathie Wood has a chronic and well-documented inability to get out of her own way. A structural tendency to buy high into momentum and sell low into drawdowns. She habitually buys when she should be selling and sells when she should be buying. It is the right basket (which can be copied if desired), but with a heavy behavioral tax attached. An inflection of the magnitude I foresee in this sector is a rising tide that lifts all boats. If the relative multiple mean-reverts toward its historical average off a multi decade base, the rising tide should account for that in this vehicle, which again can be recreated as a basket of single names. The ETFs are for simplicity’s sake.

What flips the thesis:

A regulatory shock (one that could come if the democrats retake political control).

Failed or stagnated progress in AI healthcare innovation.

An equity market breadth rollover.

As of today, I see this as the best sector thematic trade on the board, and one with a multi-year runway ahead of it. I hope to hold this position for years, and am proud to invest in and hopeful that the technology that we are pouring trillions of dollars into globally actually allows for major medical breakthroughs.

Marigolds, LBJ, and Tehran (@RealJohnGaltFla, MacroEdge Contributor)

The number of Americans who have a clue about this title probably is under 100 out of 350 million.

What the hell does a common garden flower, an egotistical maniac President, and the capital of Iran have to do with anything then or now?

Everything, as history is one’s guide to understanding the present.

I. The Current Situation

As of tonight, Trump has rejected the super secret Iranian position that has been leaked all over social media then imposed new demands on the regime in Tehran. Of course, none of the demands that Trump presented are acceptable nor are the new sanctions against any nation or entity paying the ‘environmental toll’ that Iran imposed so basically the ceasefire is status quo. Unless of course one is an IRGC missile crew being killed by “defensive” US military strikes or a US soldier killed or wounded in Kuwait after an Iranian missile strike.

If any of this seems redundant it should.

The Persians have survived being conquered by Alexander the Great, defeating the Roman Empire in battle, the Sunni attempt to extinguish the Shi’ite Sect and rewrite the history of Ali, Genghis Khan’s genocidal destruction, and a period under the British Empire.

For some reason I do not think another US President who is only interested in his own personal economic glory intimidates nor will force Tehran into a rushed agreement to satisfy Trump’s poll numbers before the midterm elections.

This brings the entire point of this analysis back to history, a point in time where an arrogant ass as a US President thought he could intimidate what he perceived as a third world power that should have been vanquished under colonial ru

II. How a Common Garden Flower Can Teach Everyone About the Iran-US War

The simplistic beauty of the Marigold. Easy to grow most of the time, easy to maintain, and having absolutely nothing to do with the alleged negotiations via Pakistan between the US and Iran.

Unless one starts to open a history book and review the history of Operation Marigold, a peace negotiation which realistically could have ended the Vietnam War in 1966 and then draw the parallels to what happens when the Generals who were warmongers along with a President whose arrogance created a false bravado which would be exposed by 1968.

The North Vietnamese Premier Pham Van Dong made the first proposal to push for a ceasefire with a return to the conditions of the 1954 Geneva Accords plus the following four demands:

1. Recognition of the basic national rights of the Vietnamese people – peace, independence, sovereignty, unity, and territorial integrity… The U.S. government must withdraw from South Vietnam U.S. troops, military personnel, and weapons of all kinds, dismantle all U.S. military bases there, and cancel its military alliance with South Vietnam. It must end its policy of intervention and aggression in South Vietnam…

2. Pending the peaceful reunification of Vietnam, while Vietnam is still temporarily divided into two zones, the military provisions of the 1954 Geneva agreements on Vietnam must be strictly respected…

3. The internal affairs of South Vietnam must be settled by the South Vietnamese people themselves, in accordance with the program of the NLF, without any foreign interference.

4. The peaceful reunification of Vietnam is to be settled by the Vietnamese people in both zones, without any foreign interference.

Sound familiar?

So where does “Operation Marigold” come into all this?

The New York Times on February 3, 1966 published a story about the proposed peace negotiations from North Vietnam with this key excerpt:

In the view of United States officials, acceptance of Hanoi’s terms would mean surrender to the Vietcong in South Vietnam and agreement to eventual unification of Vietnam under Hanoi’s control.

The negotiations were top secret as the US intelligence community believed that the initiative was the work of the Eastern Bloc nation of Poland facilitating false negotiations on behalf of the USSR to embarrass the US militarily in Vietnam. In the end, as discussed by Wallace J. Thies, in When Governments Collide: Coercion and Diplomacy in the Vietnam Conflict, 1964-1968, the truth might even be more painful:

Perhaps the most thorough scholarly analysis of all the secret diplomatic probing efforts during this period to open Vietnam peace talks, written after the declassification of a substantial portion of the U.S. record, concluded in 1980 that, “With the benefit of hindsight, it appears that the MARIGOLD contact offered the best opportunity for the Johnson Administration to negotiate a settlement of the conflict.”

Many of the details of these negotiations were still denied by LBJ after he left office, as the blunders committed by his administration lead to an increase in US involvement, more unnecessary deaths on both sides, and worse for the Democrats in power at the time, a massive power shift to their mortal enemy Richard Nixon and the Republican Party of that era.

Does this sound familiar?

Over this past weekend it was believed a serious negotiation was underway once again using the intermediaries in Oman and Pakistan to codify the ceasefire and begin the de-escalation phase of the conflict. Suddenly, on May 30th, Trump once again changes his mind (or had a third party convince him) that it’s time to take a harder line with Iran and he posted this nonsense on his dying social media platform:

The unique position of strength North Vietnam attempted to negotiate from parallels the positions Tehran has adopted now. Both nations were then, and are now, technologically inferior to the United States yet displayed strategic defiance knowing the economic and political tolerances for a major conflict favored their approach of attrition, delay, and tactical military victories designed to reduce the geopolitical effectiveness of the hegemonic behemoth.

LBJ would pay for the price of his blind presumptuousness with his loss of power and the election of Nixon. While Trump does not face this same risk, the ability of the opposition party, including some from within his own party, could create an extremely untenable political situation for Trump and the Republicans in 2027.

III. Paranoid Parallels and Economic Consequences

As a historian and avowed Federal Reserve bashing agent, one does not have to look far in my social media history or articles to understand my disdain for erroneous central bank policies but worse, political incompetence be it George W. Bush and Greenspan instigating the housing disaster or Barack Obama and his corrupt group of merrymakers setting the standard for Executive Branch corruption and graft; only to be out done by President Trump, I might add.

The inability to end the geopolitical uncertainty regarding petroleum supplies and the byproducts from the region only further engenders the mistrust of the US government by its citizenry. In fact the data, economic propaganda, and denial of reality for the poorest in American society has become the standard policy of the past two administrations, a decision which will have consequences a the Republic begins to splinter.

A prime example is the headline from the May 26th Financial Times displayed below which was dismissed out of hand by the Trump administration economic team over the weekend. The pain for the average lower middle to lower class American is not going to change not matter how many times Bessent or Hassett appear on Sunday morning talking head television to pump Wall Street algorithms or investor confidence.

If anyone inside the administration continues to feed the belief that Tehran is not aware of this issue, then history truly has failed to provide a necessary lesson.

Should this conflict and the closure of the Strait of Hormuz continue through June or worse, July, the impacts on the energy markets will hit Asia and Europe first and slam into the American heartland by early September. The reality is that it is the economy stupid, and to refuse to take a moment to smell the marigolds along with finding an avenue for a lasting peace might well have complications far beyond an economic slowdown and shifting of the geopolitical axis away from the West.

Just as ignoring the flowers created a decade of instability in the United States from 1966 to 1976, all in the name of Presidential ego and a refusal to understand the historical roots of the crisis our government helped create.

For more details, please refer to our Terms and Conditions.