Weekly Macro Note: An Explosive Upside Move in Oil, Energy Crisis Potential, Next Oil Stock I Like, Portfolio Strategy Update

In the Weekly Macro Note, we discuss the explosive upside move in oil, the potential downstream impacts of the energy price shock, a crisis potential, and deliver our next portfolio strategy update.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

As many of you know from the most recent readings, I am once again back on the road this week - currently on the West Coast and will be here for the next ten days or so. It’s going to be a very busy month as we continue to focus on building all offering portfolios of MacroEdge.

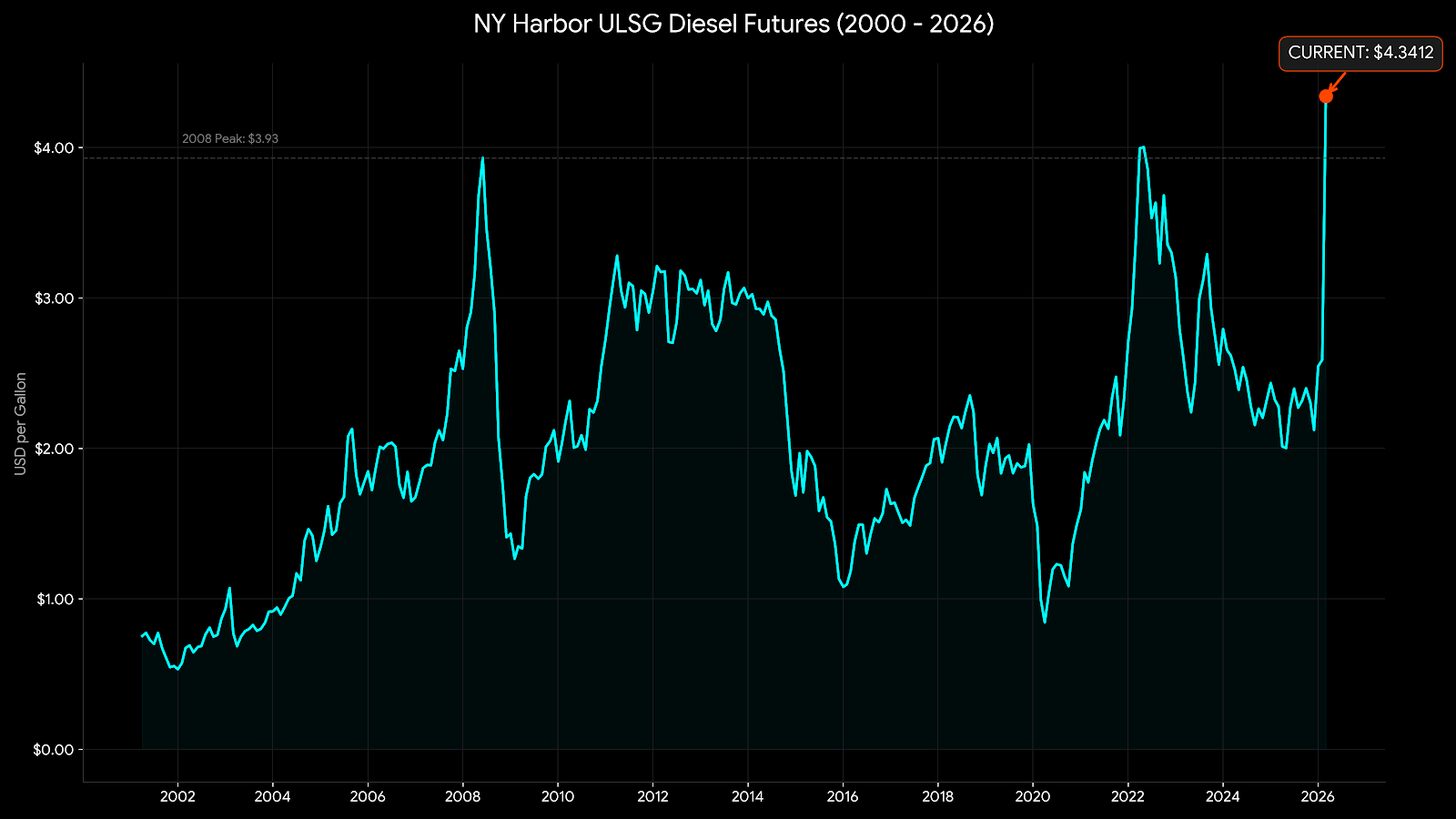

This is an unprecedented evening for the energy and commodity markets. I feel like I am watching the inverse of the COVID collapse that sent energy prices into the negatives. At the time of this writing, WTI oil is currently at $119/bbl, while diesel (ULSD futures) are just 20 cents from an all-time high… the last high for diesel was seen after the Ukraine-Russia war began. In terms of the historical context for the energy market moves, we don’t really have many to fall back on now - given that supply offline is effectively ~14-15mpdb - including backdooring exports away from the Strait of Hormuz.

We’re likely very close to a forced intervention on the part of the Trump Administration with the Strategic Petroleum Reserve (SPR) into markets, though they are likely waiting to see what other nations will pull the trigger first. Import-heavy nations like South Korea and Japan get absolutely wrecked with currencies as weak as they have, and a move this outsized happening in just a several-day period. Given all of the movements - and with how fast everything is evolving, I am going to continue keeping our reports more agile as the war evolves in the coming days - that keeps us from writing content that may get stale in just days (or hours, or minutes), and we’ll keep up-to-date information flowing out.

I will caution against energy moves like this in that they usually do not resolve in a happy way for many people. While in 2022, there was so much printing prior that the US avoided a ‘recession’ in name only, we’re at the level in which we’re going to see emergency levels pulled across the globe to combat energy prices (natural gas, oil, gasoline, etc). If the war doesn’t see a quick resolution with oil prices setting the tone, we will begin talking about very different outcome potentials over the next week. While the ‘off-ramp’ window closed that we had set to last Friday, I still think the Administration will double down in the coming week on thinking they can topple the Khamenei replacement (mistake)... Tomorrow we’re going to take a look at the technicals from the Nasdaq and technology names, continue with our war note series, and see how the day evolves.

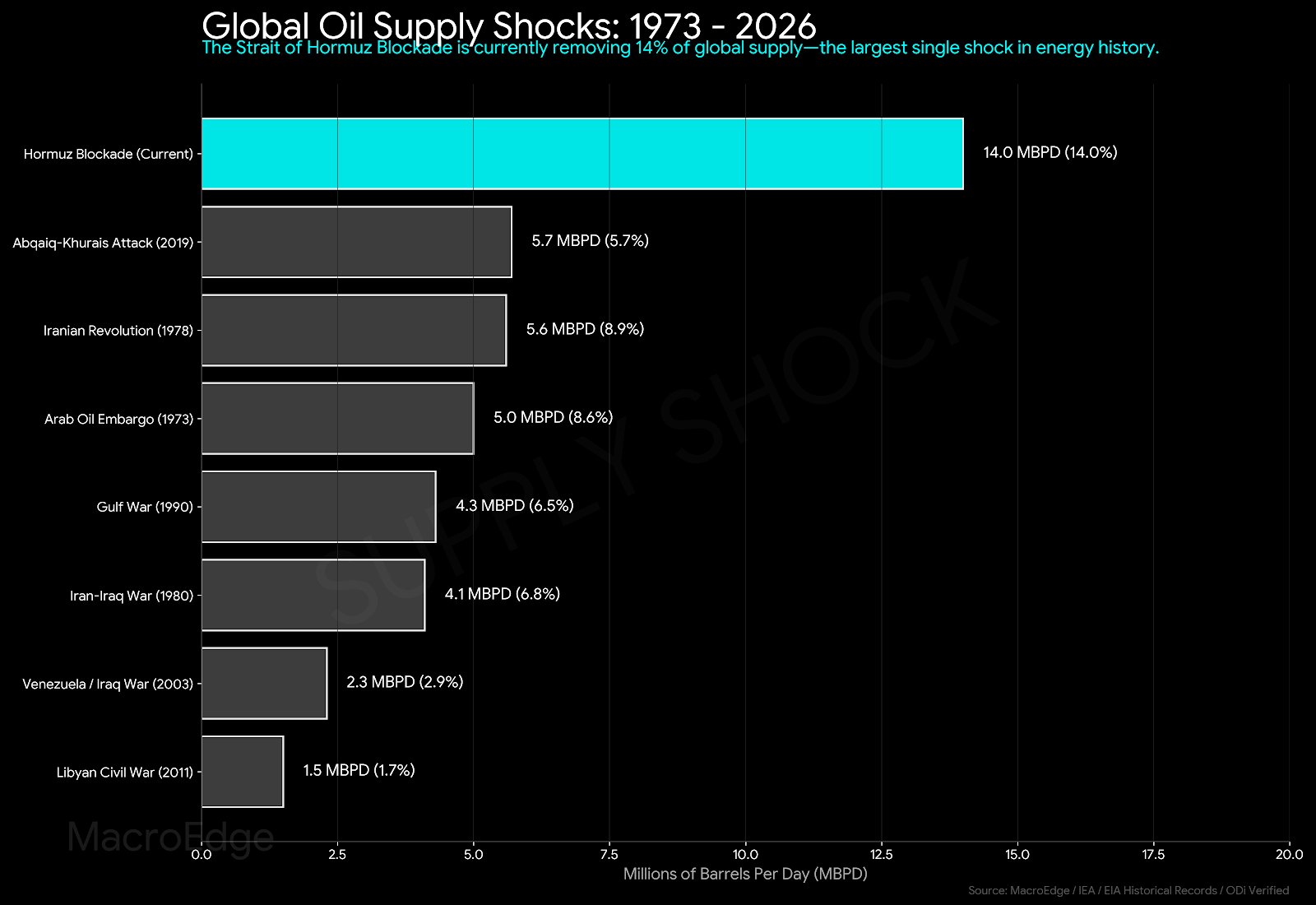

A note from my X that has been going viral today -> this is the largest single energy shock we’ve seen:

With 14 million barrels of oil impacted per day, this makes the Russia-Ukraine’s 1-3m b/d look like a walk in the park. As with any elevator, as highlighted above, the ride this is likely to put our economy on is not a pretty one, things are going to reprice over the next five days, and we’re going to be seeing evolutions every few minutes (seriously)... Another week of monitoring the situation closely, it will be.

Not a MacroEdge Ozone subscriber? You’re missing our data, research, equity research, portfolio strategy, and much more. Join below today, and see why we’re becoming a leader in the global macroeconomic landscape:

Macro Week Ahead

Monday:

Japan (GDP Estimate)

US Consumer Inflation Expectations

Tuesday:

Japan (Household Spending)

US - ADP Weekly Employment Data

US - Existing Home Sales

Wednesday:

US Consumer Price Index

Japan Producer Price Index

Thursday:

US Weekly Jobless Claims

US PPI

Japan: Machine Tool Orders

Friday:

Core Price Index (PCE)

US GDP Q2 Estimate

UMich Consumer Sentiment Data

The Oil Catalyst: With the Strait of Hormuz blocked, oil is the primary driver of all asset classes this week.

If this move in oil and gasoline prices is sustained for several months, we’re going to see it hit all input costs across the board - and that will impact food costs, trucking and transportation, flight costs, and everything in between.

Diesel prices, which are the backbone of the industrial economy input price reading are near an all-time high this evening:

An Explosive Move in Oil (and Gas)

The move in oil and gas prices is unprecedented by all standards - diesel is up 70% this month (we’re eight days in), and oil is up by almost the same amount. Moves of this magnitude end up being completely destructive in many cases, but that’s often with a lag. I find it fascinating that just a month ago that, we were writing about the historic asymmetric potential upside to oil prices, to now seeing what we’re seeing this evening, nearing $120 barrel for West Texas Intermediate.

Energy Crisis Potential

(Below: Energy Crisis Potential, Next Oil Stock I Like, Portfolio Strategy Update)

The potential for an energy crisis went from a far away scenario to a near reality. The diesel price shock is going to have a significant impact on the industrial economy - and if this lasts more than a week, things are going to get very painful, very fast in the economy. While the ‘normies’ - aka your average person not following anything going on in the world today - aren’t going to know what’s going to hit them until they fill up their tank this week or next - we’ve got our eyes wide open now.

Supply Chain Collapse & Food Hyper-Inflation: Diesel is the “blood” of the global supply chain; it powers the cargo ships, freight trains, and semi-trucks that move 90% of global goods. If ULSG Diesel remains above $4.30/gal (Futures), transport surcharges will be passed directly to the consumer. More critically, high energy prices increase the cost of natural gas-based fertilizers. This creates a “double-squeeze” on food: it becomes significantly more expensive to grow, and even more expensive to move, leading to rapid price hikes at the grocery shelf.

The “Forsaken” Recession: We are facing a classic Supply-Side Shock. Unlike a typical recession driven by low demand, this is driven by the soaring cost of inputs. When energy consumes a larger share of household and corporate budgets, “discretionary” spending evaporates. If these levels hold, the resulting contraction in consumer activity, combined with industrial shutdowns in energy-intensive sectors (like steel and chemicals), makes a global recession almost mathematically inevitable.

Destabilization & Civil Unrest: History shows a direct correlation between energy/food price spikes and social instability (e.g., the Arab Spring). When the cost of basic commuting and eating exceeds the median daily wage in developing and even middle-income nations, the “social contract” begins to fray. We are entering a window where sustained prices at these levels could trigger mass protests, strikes in the transport sector, and general civil unrest as the cost of living outpaces any possible wage growth.

Next Oil Stock I Like

While frac spreads are still near cycle lows, they’ve bottomed out a bit and tend to lag drilling activity. If we see drilling start to increase now as E&P companies attempt to capture this move (trust me, from my visit to Midland three weeks ago, they can’t believe what they’re dealing with) - I think that equipment and service providers offer asymmetric upside from here. One of those that I’ve explored deeply over the weekend is ACDC (ProFrac), and tomorrow, depending on how the day evolves, I will cover why the opportunity could be ripe given how fast some of these fracking heavy companies must get on the job and extract as much money as they possibly can to take advantage of a price environment like this.

Tomorrow’s Preview

War Note

Energy Price Update

Updating on our Energy Basket

ACDC - For those about to rock?

MacroEdge Portfolio Strategy Update - March 8, 2026 (@SixFinance, Head of Research)

The duration of closure of the Straight of Hormuz will be the primary driver of risk until this is resolved. Over twenty million barrels of oil flow through the Straight every day, and this is the largest supply shock (on a bpd basis) to the oil market in history. As long as the Straight remains closed, oil is likely to continue ramping higher.

This tactic, being utilized by the Islamic Revolutionary Guard Corps (IRGC), is the only meaningfully effective method to fight against total regime change in Iran. Time is on Iran’s side here, not ours. A prolonged Straight closure risks a global energy crisis, with genuinely profound economic consequences.

As long as the Iranian regime faces the existential threat of total destruction, it can be expected to do whatever it can to continue pulling on this extremely powerful lever.

Until oil starts moving through the Straight again, there is a large and rapidly increasing amount of tail risk to already expensive U.S. equities. By the same token, members of the administration know this, and the market may force them out of their regime change goals in Iran.

Crude oil futures are through $100 on the gap up. US equity futures are down relatively modestly all things considered. If the administration does not get the Straight of Hormuz open quickly, equities may continue to spiral. Managing risk here is paramount.

The /ES put spreads have been a great hedge through this chaos so far since Wednesday, and since we are through their bottom strike on ES and there is still a wide gap between market pricing and intrinsic value, I will leave them on for now, as there is still significant value to be attained.

Oil has risen so rapidly that the clock is ticking to avoid a recession now. The best case scenario, in which the Straight is reopened soon, would still likely see elevated crude prices for some time to come, not a straight line back to pre-war pricing, although certainly a premium would come out of the market.

I want to see where cash equities trade tomorrow before making any large changes.

Update to follow tomorrow night. I will be focusing on managing risk until then.

For more details, please refer to our Terms and Conditions.

Summer of discontent is definitely on the horizon.