Weekly Macro Note: A Brief Welcome to 'Summer', Yen/Won Weakness, and Geopolitical/Energy Update

In this Weekly Macro Note - we preview the week ahead, discuss the weakness in the Yen & KRW, highlight the latest on the geopolitical front from Switzerland, and discuss the energy markets.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

More of the same continues this evening from the war negotiations out of the Middle East - with Qatar stepping in this evening to intervene as soon as commodity prices began to move higher. Futures are flat across the board, with oil prices lower slightly after an early session pop on news that the Iran delegation was departing the peace talks. We now know that the peace talks will continue for the remainder of the week, which is the perfect jawboning tool for the entirety of the week, as inventories continue to draw down. The setup on oil and natural gas continues to look constructive now, and I expect that upside will materialize once we can actually work through all of the short-term headline noise of deals, MoUs, etc. A deal/ceasefire in Lebanon will mean that we can begin to shift headline focus to the actual inventory data - and that’s something that the market has refused to look at for the entirety of the move - really since the war first began.

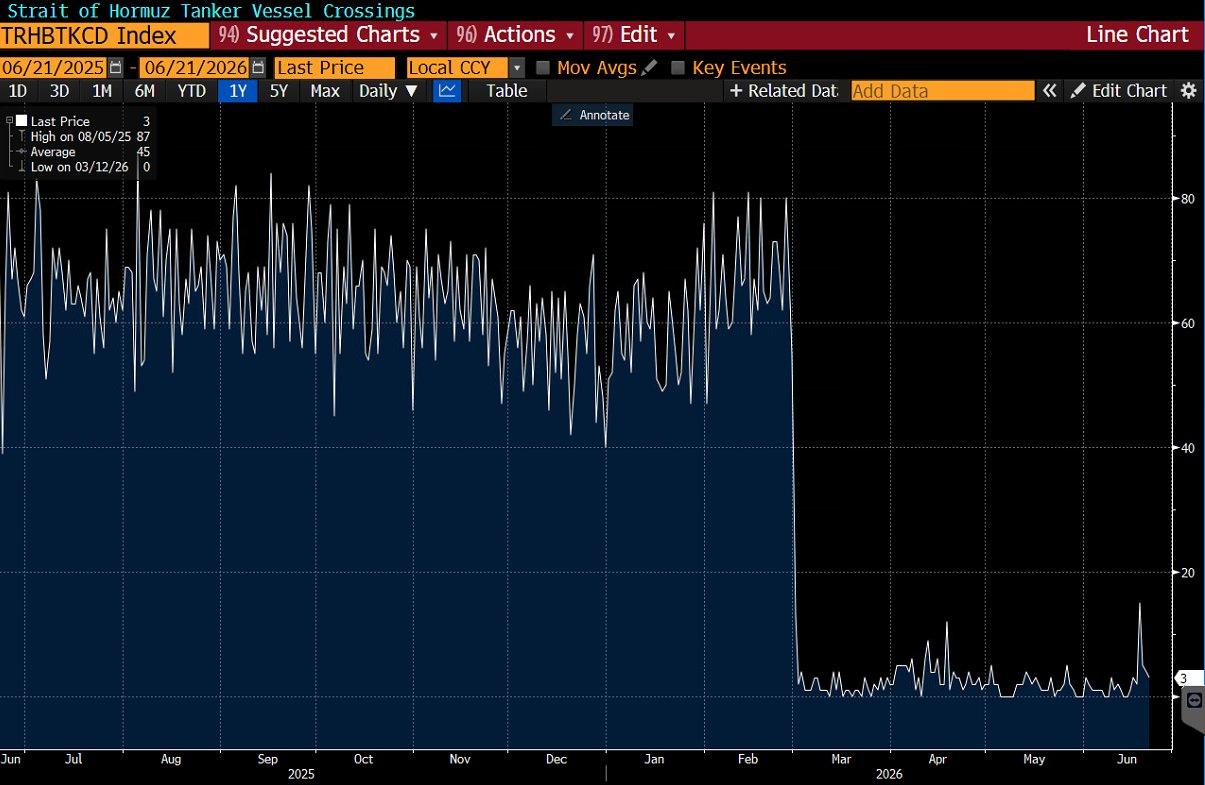

Traffic in the Strait of Hormuz remains nowhere near pre-war levels, and even as sanctions are lifted on Iran - it appears that Iranian tankers will be controlling a bulk of the exports out of the Persian Gulf for the time being. I expect that over the 60-day negotiation window, we don’t see Strait traffic get anywhere near prewar levels. The reality is that it’s not whether or not Iran/Oman want to permit boats through - they really would love to collect the tolls - it’s the insurance companies waiting to see if tankers are actually going to be allowed to cross without incident. Just 6 tankers have crossed in the last 24 hours (dark/sanctioned), and 3 ships with AIS on have gone through after Iran claimed the Strait was once again closed for business:

The goal now for policymakers is going to be to kick the oil market pressure as long as possible into the future - which gets it closer to a date where oil production can meaningfully move higher - which is also still months away (and may even be toward the end of the year). The dilemma continues to be the fact that inventory levels are collapsing at the same time that prices are not resulting in any sort of transmission to markets that we are short on supply - so the eventual outcome will likely at this point be localized shortages and a structurally higher floor on prices - even in the face of fake headlines and outright market manipulation by nations. If there is one thing that politicians hate more than anything else - it’s high oil and gasoline prices - and we’re seeing how quickly that can weigh on things like election outcomes, etc. With November now being just over 4 months away, it’s obvious that the pivot has to come now - and it doesn’t mean that the war won’t resume later. It’s also notable that neither Hezbollah nor Israel are taking part in the talks in Switzerland - even though the bulk of the focus today was about halting the conflict in Southern Lebanon.

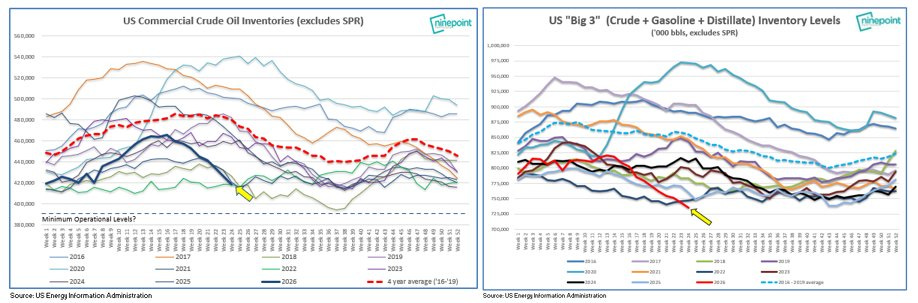

The real story in the macro data this week will be oil inventory levels. Expect that we hear from the EIA that Cushing in Oklahoma is hitting operating minimums - and that will impact PADD2/4 flows to refineries - which will not be able to purchase product from Cushing. While again, the impact won’t be most dramatic at home, this is what the early beginnings of a real summer pinch are going to look like - and the padding on the front-end is simply noise for an absolute rubber-band that’s going to hit as we physically (and in a literal sense) hit tank bottoms.

Not yet a MacroEdge Ozone subscriber? Get our portfolio strategy, commentary, research, data, and more below:

Macro Week Ahead

This week we will get our last of the hot PCE sequence readings from this energy price shock - and the remainder of the data isn’t particularly consequential. I would start to pay more attention to API and EIA data from here on out - as it’s likely that Cushing, OK, and other key oil storage facilities start hitting ‘tank bottom’ this week.

Monday: n/a

Tuesday: S&P Global Flash PMIs

Wednesday: n/a

Thursday: Final Q1 GDP, May PCE, Durable Goods, Tokyo CPI

Friday: UMich Consumer Sentiment - Final

On the geopolitical front - which I cover below, expect that things are going to continue to be really noisy this week with Axios & other sources running full bore on peace talks, deals, etc. in the headlines. Given the situation with oil inventories domestically - and around the globe - the US administration is doing everything possible to get out of the situation, as we will continue to run down oil inventories for the next 8-10 weeks.

Earnings this week:

FedEx (Tuesday)

Micron (Wednesday)

Geopolitical/Energy Update

This week we will get more of the same ‘bs’ jawbone action with the fact that the discussions are ongoing and they will use news outlets to control the narrative that there is *nothing to see here* while we begin to hit tank bottom at distribution facilities. Because there’s no way out now of the drawdowns - and politicians would much prefer to create the illusion that there is plenty of oil abundance

The setup on gasoline technically is now quite constructive - even though they slammed it back below the trendline this evening.