Weekly Macro Note: 1973-Sized Energy Shock, War Updates, Technicals, & More

In this Weekly Macro Note - we discuss the latest from the Israel-Iran War, discuss the magnitude of the current energy shock, interventions, technicals, and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers and Community,

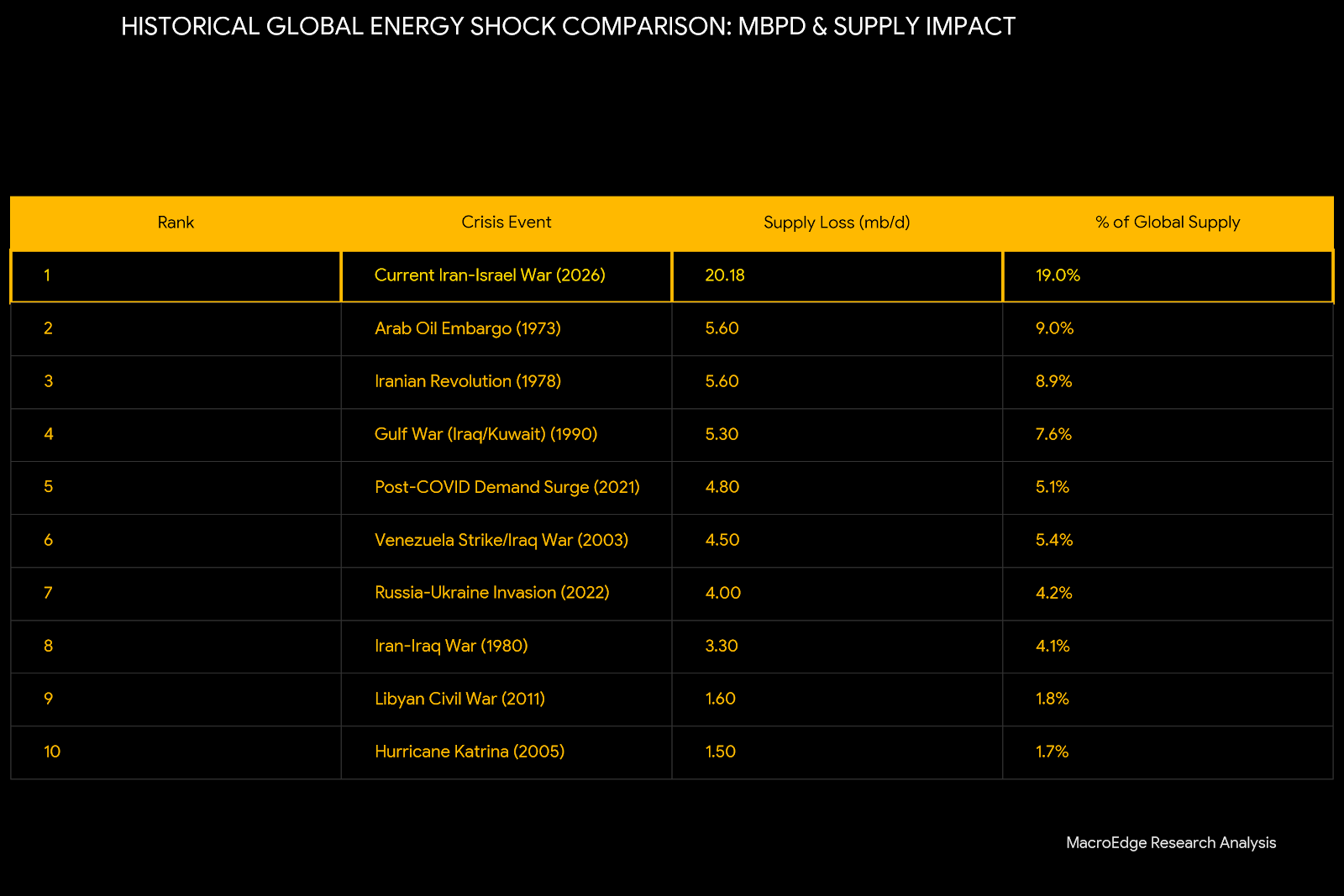

This evening we’ve got just one more macro note being delivered to you all from the West Coast before I embark back to Central Time on Wednesday. This weekend has seen further developments out of the Middle East as the Israel-Iran shows signals that off-ramp chances are narrowing, at least for the next 30 days. With the Strait of Hormuz still closed, our data arsenal has let us put an 8-18 day window of warning for governments to wind down the conflict before a broader energy shock starts to impact the global economy. Southeast Asian and East Asian economies are particularly vulnerable, and I am monitoring Australia as an energy-bellwether for fuel shortages.

Yields are also moving higher, with the 10Y back above 4.4%. This evening’s report will be shorter than, usual given the high-frequency development of market data right now, and futures are moving lower as oil prices again push back toward the critical $100 level. Oil and gas prices are now firmly driving just about everything in the macro-narrative, and will remain our core focus while the largest supply shock in world history continues to materialize.

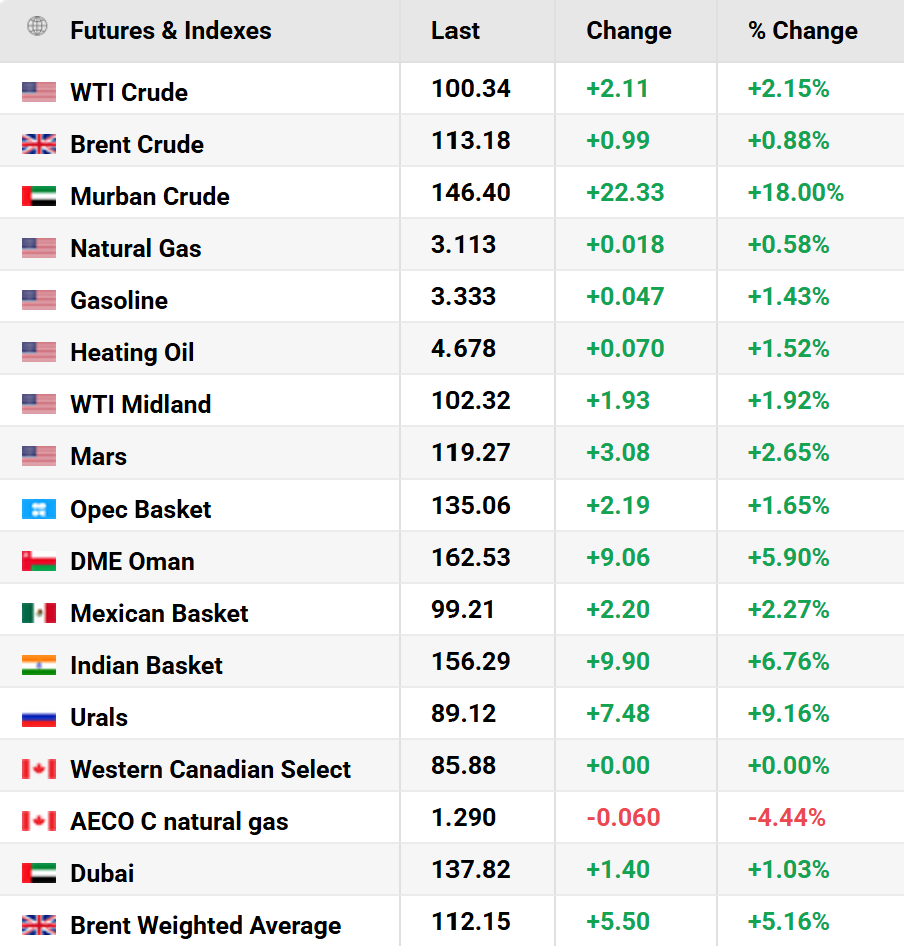

The latest in oil and natural gas basket pricings:

Notice the significant spread between WTI, Mars, Oman, India, Dubai, and Brent. WTI remains price suppressed relative to the basket, and opportunities are going to arrive from this situation.

Trident - The Future of Macro-Driven Asset Management*

Learn more about the Trident I Global Macro Fund and TREX Fund by submitting the contact form below.

Geopolitical Updates

On the little geopolitical front, we only saw signs of escalation this weekend. We are in a very precarious position with this war, and an extension of the conflict with the Strait of Hormuz closure is looking more likely. Without a concrete plan to reopen the Strait, European and Asian nations are in a very precarious position. While things like a fuel export ban may be popular from a policy standpoint, they could all contribute to a feedback loop in higher prices across the board.

To summarize some of the most major developments over the weekend:

Iran utilized a new medium-range ballistic missile (MRBM) to target Diego Garcia, a military base from which the US launches long-range attacks from.

Israel escalated the conflict overnight with strikes on critical Iranian infrastructure - including energy and power plant infrastructure.

The Strait of Hormuz remains effectively closed, with traffic down over 95% on a rolling week/week basis from the start of the war.

The US President highlighted that more significant attacks may begin against Iran in the coming days, and highlighted that ‘total destruction’ may be the only possible route if the Strait of Hormuz isn’t reopened.

Off-ramp routes are narrowing as attacks on both sides continue to escalate, and this week is critical in determining if any off-ramp will be possible in the next 30 days.

Oil & Gas in the Driver’s Seat

Oil and natural gas prices are firmly in the driver’s seat now for all short-term market trends. That will eventually become ‘intermediate term’ macro trends as and if an energy price shock materializes, which appears to already be underway. If natural gas prices join that move higher in the United States (Henry Hub / NG1), things are going to get quite painful. The pain will start to trickle into input costs across the board - from logistics, to food prices, raw materials, and more - which will eventually contribute to demand destruction (yields are doing some work here too, with things like mortgages).

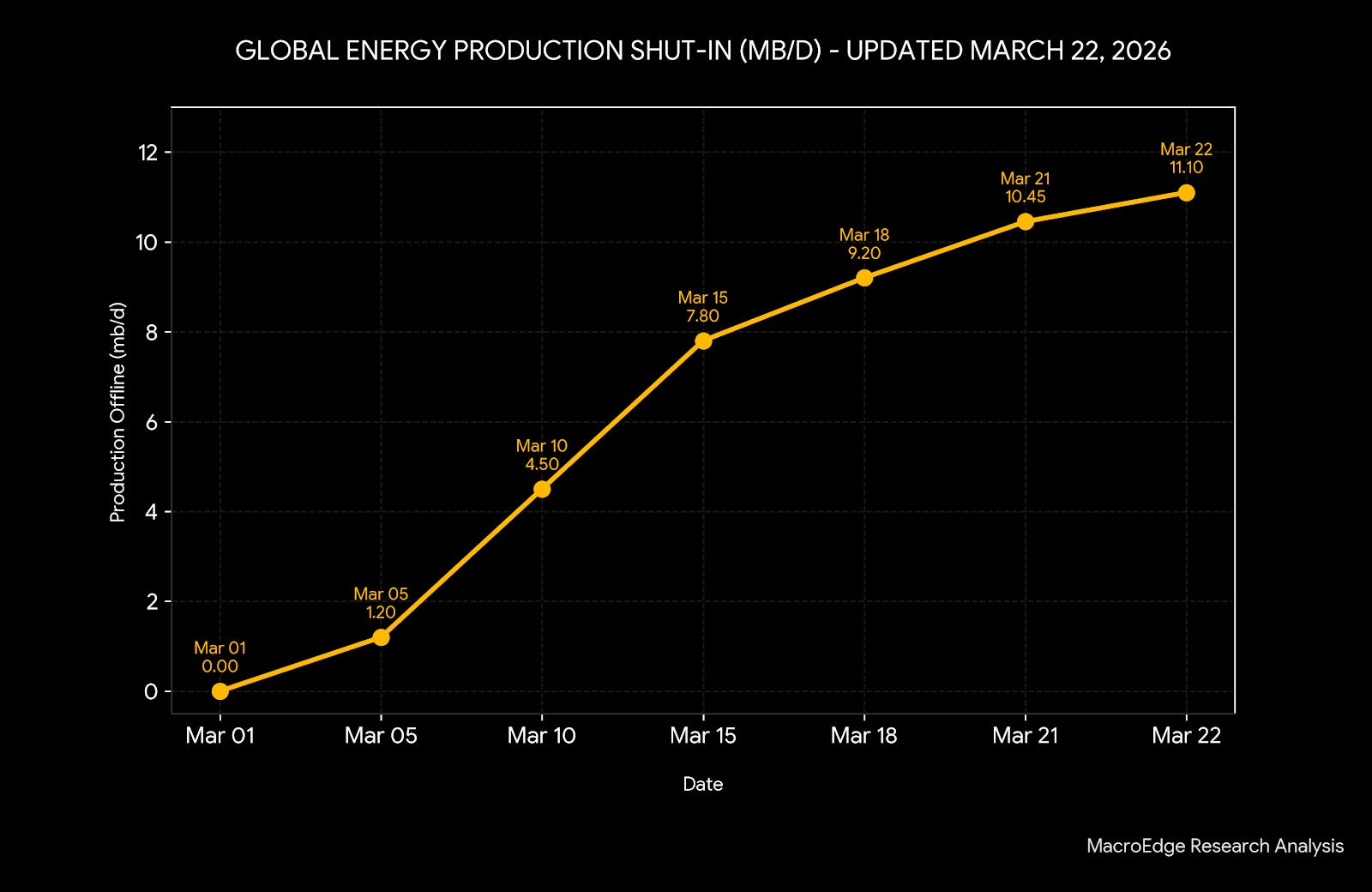

The latest update to our global oil production shut-in tracking:

Through 3/22 - about 11.1mbpd is offline - which makes this the largest production shock on record by orders of magnitude. This event is just about half of the overall supply shock as well.

Interventions in Oil Markets Continue

While it’s speculation to a degree, it appears that the Treasury and government have set an intervention mark at the $100 WTI mark. Over the past two weeks, every time the price of WTI has crept towards $100, it’s been kicked back lower. This has pushed spreads against Brent, Murban, and the OPEC basket to the widest levels we’ve ever seen. While the US is in a better place from an oil stock standpoint, this policy positioning could be setting up oil prices for one of their most explosive ‘squeeze’ style moves we’ve ever seen:

When WTI breaks above the $100 WTI market and holds this level for several days, look for further pushback, but an eventual ‘dam break’ moment where prices push toward much higher lows.

Technically, in Trouble

Equity indices in the US are still undergoing a very lengthy distribution process - with institutions selling into retail euphoria. Notably, in February, margin leverage dipped lower - and this is a key signal to watch over the next six months. If we see margin begin to unwind, we are going to see liquidations, which can eventually trigger forced selling of US equities.

Report Schedule for the Week

Tuesday: Geopolitical & Energy Update, How Oil Prices Impact the Broader Macro Picture

Thursday: A Midweek Macro Note from Midland, Margin Update

Friday: Redeye Macro Note

Saturday: Saturday Macro Note

Sunday: Weekly Macro Note

*Important Disclosure: This post is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any interests in Trident I Global Macro Fund, LP. Any such offering will be made only by the Private Placement Memorandum (PPM) and Subscription Agreement. Rule 506(c) offerings are limited to Accredited Investors only. Investing in private funds involves high risk and is not suitable for all investors.

For more details, please refer to our Terms and Conditions.