Weekly Macro Note 11/23: Remaining 'TACO' Bullets, Portfolio Strategy Updates, Thanksgiving Macro Week Ahead, 99/07 Cracks Re-Appear, Technicals

In this Weekly Macro Note, we discuss the remaining 'TACO' ammunition the Administration retains, updates to Ozone Pro portfolio strategies, discuss data, the BoJ, and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers and Community,

Happy Pre-Thanksgiving Sunday, and it’s pretty incredible that the year has somehow landed up on November 23rd already. Because we published the Redeye Macro Note late last evening, with a longer-than-usual intro, we’ll keep this introduction shorter as a result.

This week will likely be quite light on volume (given both the full day off Thursday and the half-day on Friday), and the real traders & houses have already left their cities for the first ski trip of the season in Jackson, or down to Florida, Mexico, or the Caribbean to seek Turkey under warmer conditions. So far, we’re off to a pretty tepid start to the week with ES up about .25%, Bitcoin up a little more at about $87.5 (2.5%), and the NQ up about .45%. Given the wind-down in earnings as we highlighted last night, and a general lack of data this week, really until post-FOMC next month now, it’s more of a monitor the markets & Japan pattern now as we shift from November into December mode. As we head into winter, action should pick back up, though I expect more tepid conditions through both holiday weeks themselves. As highlighted below in the portfolio strategy updates section, I am beginning to look for an attractive entry zone on several names, and we will publish those updates out as they are made, intraday or in one of the Midweek Macro Notes.

After this 5-6% correction in the indices, in which breadth deteriorated, and market cap concentration became even more notable, while technicals have been stretched, a reset is what would make the said moves above much more attractive.

Let’s dive in.

Market Holiday Calendar

Wednesday (normal market operations)

Thursday (market full day closure)

Black Friday (early close)

Remaining ‘TACO’ Bullets

One of the things I wanted to cover this evening was the more ‘obvious’ remaining ‘TACO’ bullets. By bullets, I mean ammunition that the Administration has held onto to this point, after a year of massive fiscal intervention in the equity markets, both verbally and policy-wise. We’ve shifted towards a much more ‘Bushian’ administration in the last 2 months, and the rhetoric of earlier in the year has been tossed out the window, while as we highlighted yesterday evening, consumer confidence has hit near record lows.

The core ones that I think remain:

Supreme Court suspension of Trump’s IEEPA tariffs, Trump walking them back before the ruling

Acquisition of AI/data center company, or equity in one or a few, before summer

‘White swan’ announcement of additional economic stimulus or tax cut for the low-income cohort

The stimulus checks from tariffs are overstated, though politicians will warm up to them next year

‘Leaked’ headlines

Portfolio Strategy Updates

In this holiday lull, I am looking to make our first adjustments to the Global Macro Strategy Portfolio, at the right time. Our goal is to stay agile. I continue to await a pivot in policy from the BoJ to a more hawkish stance again, as the Yen has weakened dramatically (Bessent’s goal from the April lows) and the BoJ has shifted its tone towards being more open to one more hike. I expect that this will be the ‘said and done hike’ and we see no further following it until they ease.

Six has the latest updates for the MIRP strategy below.

Get all of our positioning updates, portfolio strategy, and more with 4-week access to Ozone Pro below:

Thanksgiving Macro Week Ahead

Thanksgiving week is usually a tepid one for US markets, with the Wednesday before Thanksgiving having a strong tendency for positive returns. Over the last 50 years, the S&P has returned roughly .54% for Thanksgiving, and has been positive about ⅔ instances over that period of time.

This week on Wednesday, we’ll get the CB Consumer Confidence reading, continuing claims, and PPI on Tuesday, along with retail sales (lagged release). The Chicago PMI will be released as well.

99/07 Cracks Re-Appear

The cracks in labor, and risk to equity/assets due to their extended valuations, have been noted by Fed members now several times over the past few weeks. This has been a notable shift in tone from the Powell ‘AI is profitable’ line of a few months ago…

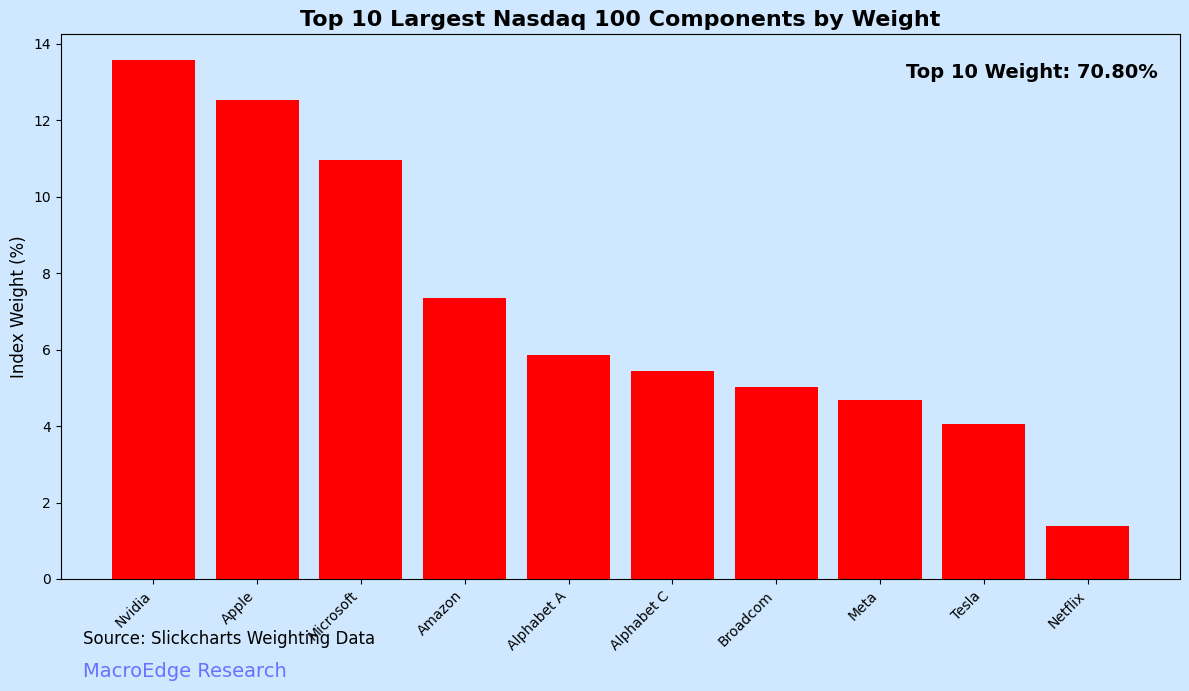

Concentration risk is as high as it has been - and the passive effect (covered by Michael Green) plays an extensive role in this feedback loop. For the S&P, it’s less but still very elevated by historical standards, with the top 10 names making up about a 40% weighting.

I continue to have very relevant concerns about the longevity of the data center trade, given what will become fierce opposition to them in the coming 2-3 years. While they had a limited window for success under the current Administration, and especially in red states, the pathway to profitability for the end users is still nowhere in sight. If I had to guess, opposition continues to mount here, and I get flashbacks to the fiber buildout days, in which we’ve way overbought, though under the current Administration, I could very well see us getting the government as a buyer-of-last-resort for stalled and empty data centers under the *national security* card.

The equity market, in particular, is the trophy for the Administration, and since late-August (we’ve moved it under the national security umbrella)... because even though the remark is somewhat sarcastic, I’m only being half sarcastic. On top of that, we’ve got the labor lag still in play from the 2 year hiking cycle that began in March ‘22, with U3 at an expected 4.5% for the month of October. I expect the Administration to begin tooling CPI lower for the November & December readings, and think that holiday shopping this year is going to be a very mixed picture depending on the economic cohort that someone belongs to.

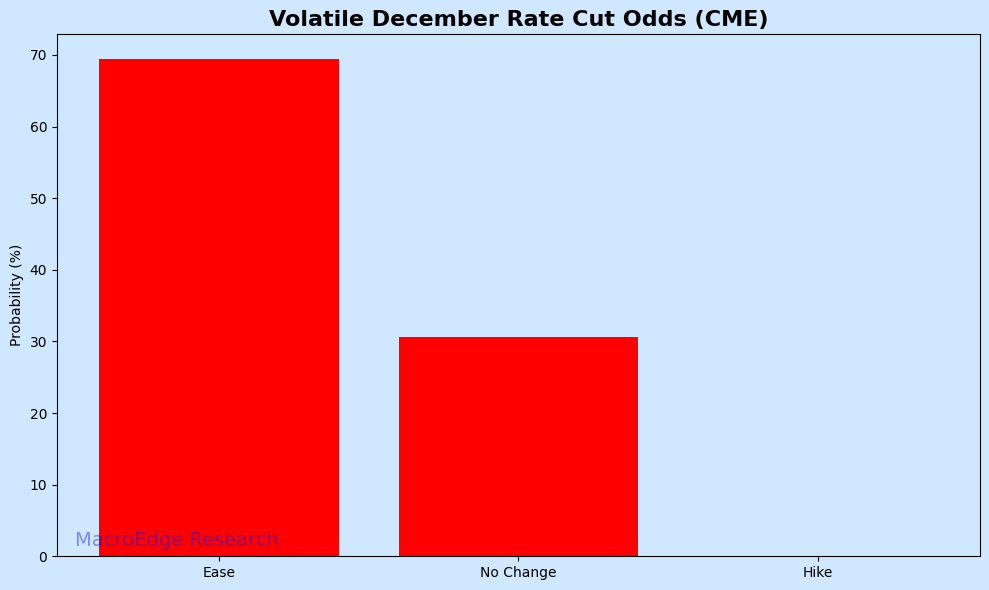

Because the wealth effect is in play, I expect to see the Administration defend equity markets through the holiday season, and window dressing becomes more difficult to defend after the December FOMC and pre-Christmas rate cut we’re now expecting.

The equity bubble similarities in tech of the late 90s, with valuations stretched to record-tying bubble levels of then, coupled with the employment and real estate downturn, give us a lot of similarities to continue analyzing from previous cycles. Interest rate lags are still in effect both ways, even at our record levels of deficit spending & out-of-control fiscal boosters from both parties.

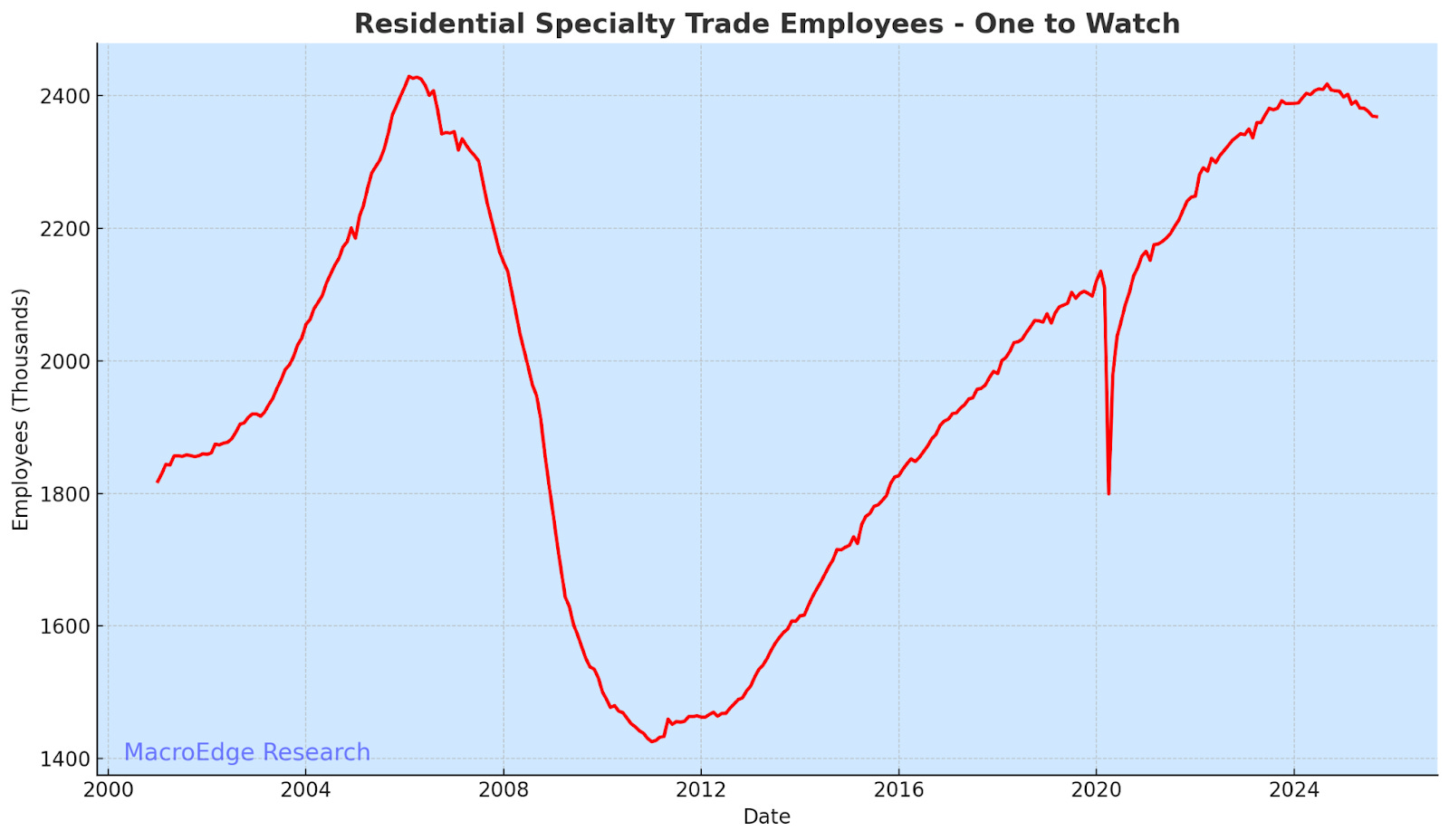

One to watch for residential construction building:

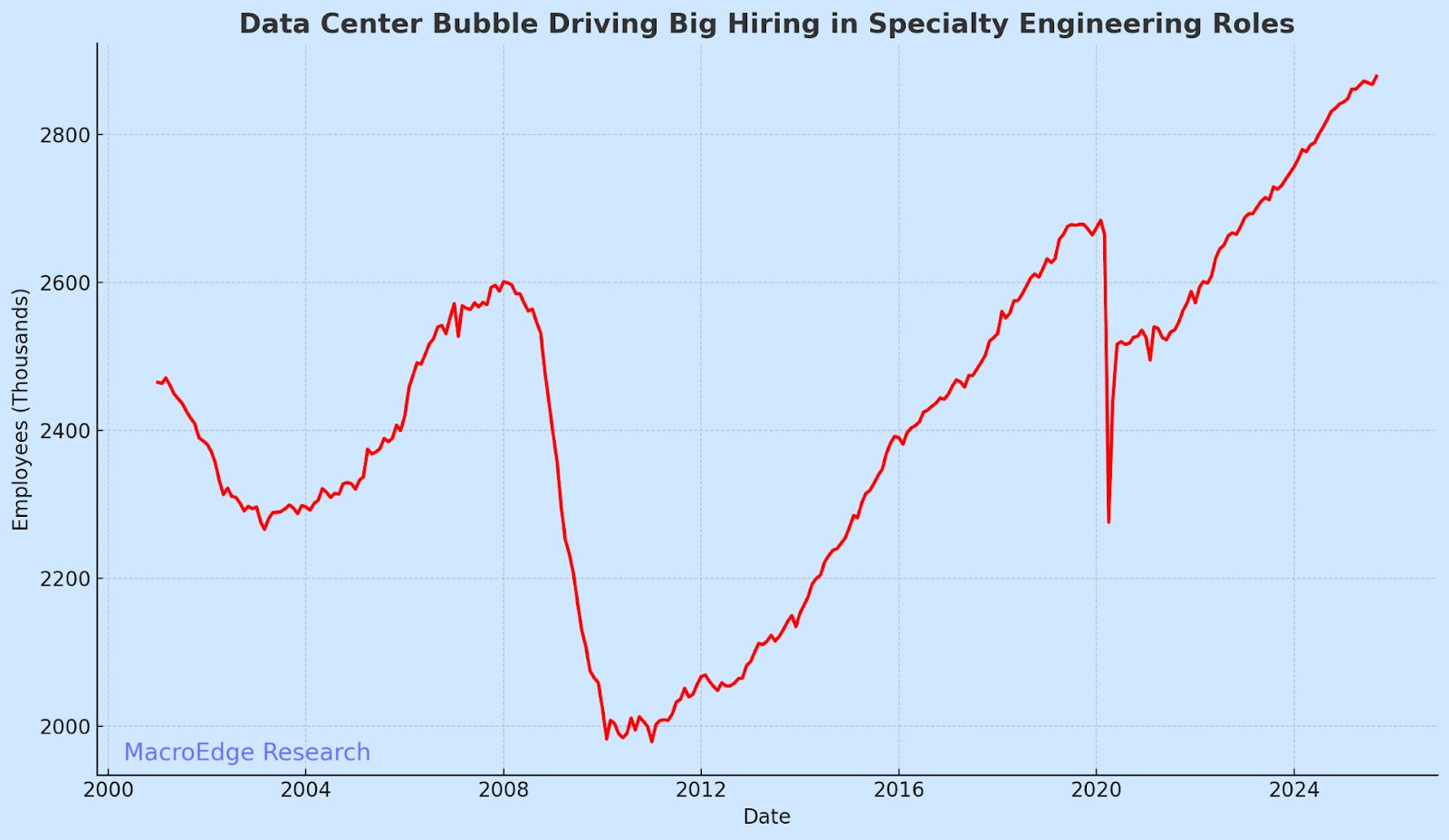

And for data center construction:

Notice in the previous cycle (above) the lag that non-res had to res.

Continued below (technicals, portfolio strategy updates, NVDA update, Ozone Pro commentary, and more):

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.