Weekly Macro Note 10/5: Japanese Election Optimism, Gold Highs Continue, Continued Reason for Caution

In this Macro Note - we cover the continued euphoria in everything from Bitcoin to equities, the Nikkei; discuss the new highs in gold and other metals, and highlight continued reasons for caution...

Good Sunday evening MacroEdge Readers and Community,

I am writing this latest rendition of the Weekly Macro Note from California, where we have several client meetings this week. It’s certainly a great place to visit - especially this time of year - but the only downside I always find in these longer trips out west is being thrown off into PST for our Macro Notes. As discussed last week, we’ve really simplified our offering approach, which I anticipate will give us great fuel into the remainder of the year.

This evening, we’ll dive into the optimism out of Japan on the selection of Sanae Takaichi to serve as the next Prime Minister for the nation, discuss the continuing highs in gold and other metals, and explore some of the macro-driven reasons for caution – that we’ve discussed continually for the last several weeks.

Investor optimism continues to be off the charts (breaking some of our dual-axis charts now) though that has only fueled continued speculation higher for equities in the US… namely in the high beta semiconductor and AI names.

This evening we’ll keep things brief from a macro coverage standpoint, as well as forecasting, as I expect the government to remain closed until the 15th or 16, at the very earliest. Both parties are figuring out how to use the shutdown for political leverage, and though no mass layoffs have originated from the shutdown, I expect 50-70K more federal employees, on top of the DOGE cuts and 100,000 ‘retired’ employees, to be axed this week.

MacroEdge Institutional Research Update

Report #03 coming on 10/7 in the evening

MacroEdge Dashboard

Invites are still delayed pending Dashboard being moved to alpha stage, you will receive an email with a registration link when the dashboard is available

Link to register for IR will be available on the MacroEdge website at the end of the week

Our six new macro data points will be available over the next week – MacroEdge Monthly Inflation Composite Index (Ex & Inc-Energy and Food), MacroEdge Jobless Claims Estimate, MacroEdge Recession Indicator, MacroEdge Employment Momentum Index, MacroEdge Market Valuation Signal.

Macro Week Ahead

This week from a macro data standpoint hinges on the BLS releasing (or not) the latest data regarding employment and inflation. With little sign of progress on the shutdown, we’ll continue to rely on private sector data, including our own, for the time being - and earnings this week are also light. We just have Pepsi & Delta to look at for any level of importance at the macro level.

Monday, October 6

Japan releases August household spending, a key measure of consumer momentum heading into the final quarter, alongside foreign exchange reserve data. In the U.S., short-term bill auctions set the tone for Treasury funding. A prolonged data blackout from Washington remains possible, with several statistical agencies on standby.

Tuesday, October 7

The U.S. trade balance for August will be the week’s first major macro print, offering a fresh view of import demand and export softness. Japan publishes its leading and coincident indices for August, an early gauge of business cycle direction.

Wednesday, October 8

The FOMC Minutes dominate the mid-week focus, offering a deeper look at the September rate-cut debate. Japan’s Reuters Tankan survey arrives the same day, capturing sentiment shifts among manufacturers following yen volatility.

Thursday, October 9

The U.S. jobless claims series remains the primary real-time labor indicator, though its release could be delayed if BLS operations are suspended. Japan’s producer price index for September will update cost-push inflation dynamics in manufacturing and energy.

Friday, October 10

The University of Michigan’s preliminary October sentiment survey provides the first read on post-cut consumer expectations for inflation and spending. The U.S. monthly budget statement for September will close the fiscal year with a focus on deficit trajectories.

In short, Japan’s calendar centers on household and producer inflation, while the U.S. week hinges on whether BLS and BEA data streams continue uninterrupted. If the shutdown persists, private and high-frequency indicators will temporarily substitute for official labor and inflation releases.

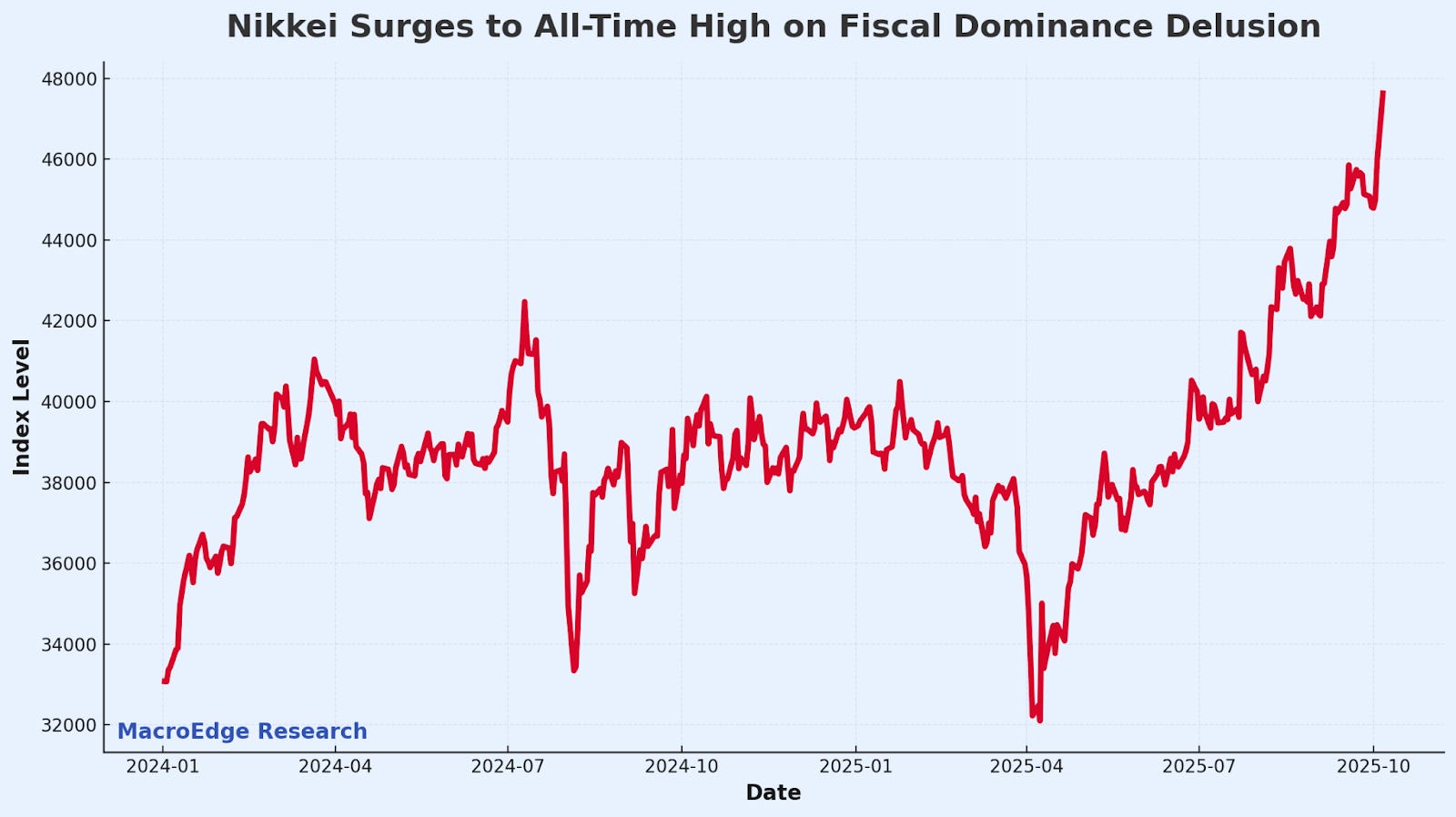

Japanese Election Optimism

The Nikkei surged tonight due to the selection of a new ‘Abe-esque’ Prime Minister - while the optimism is similar to that of Trump back in November 2024 it’s likely that this optimism tapers off through the end of the year. Soon-to-be PM Takaichi (LDP) has promised similar fiscal spending & programs in the form of Abenomics, and that’s resulted in the Yen weakening to the 150 level this evening (US-time) along with a surge in the Nikkei, while bonds have stumbled.

The Nikkei is at a new all-time high, and the biggest event out of Japan will be the next hike from the BoJ, or an initiation of cuts (that look very unlikely right now) if the economy begins to falter and the BoJ goes even more aggressive on its pro-easing policy stance.

Gold Highs Continue

Gold has continued to surge to new highs this evening – and the broaders metals market continues to send warning signals to us about something (that may or may not be the most obvious signal of all-time time).