Weekly Macro Note 10/19: Sunday Night Negotiations, China Overview, Special CPI Report, Losing Steam...?

In the Weekly Macro Note - we discusses the latest tariff negotiations and upcoming deadline that will be moved, talk about the decline in government employment & migration, China, CPI, & more

(@DonMiami3, Chief Economist)

Good Sunday evening MacroEdge Readers & Community,

We’re heading into the second half of October towards a major earnings week - with over 300 companies reporting over the next 5 days. On Friday, we’ll also get the CPI report for September - which is a delayed, special release. This CPI release was required by law and not due to selective picking and choosing on data releases while the government is still closed. With a Social Security adjustment looming, this report was required for that calculation, there is no sneaky pre-Halloween delivery here, since I would call that out if it were really the case.

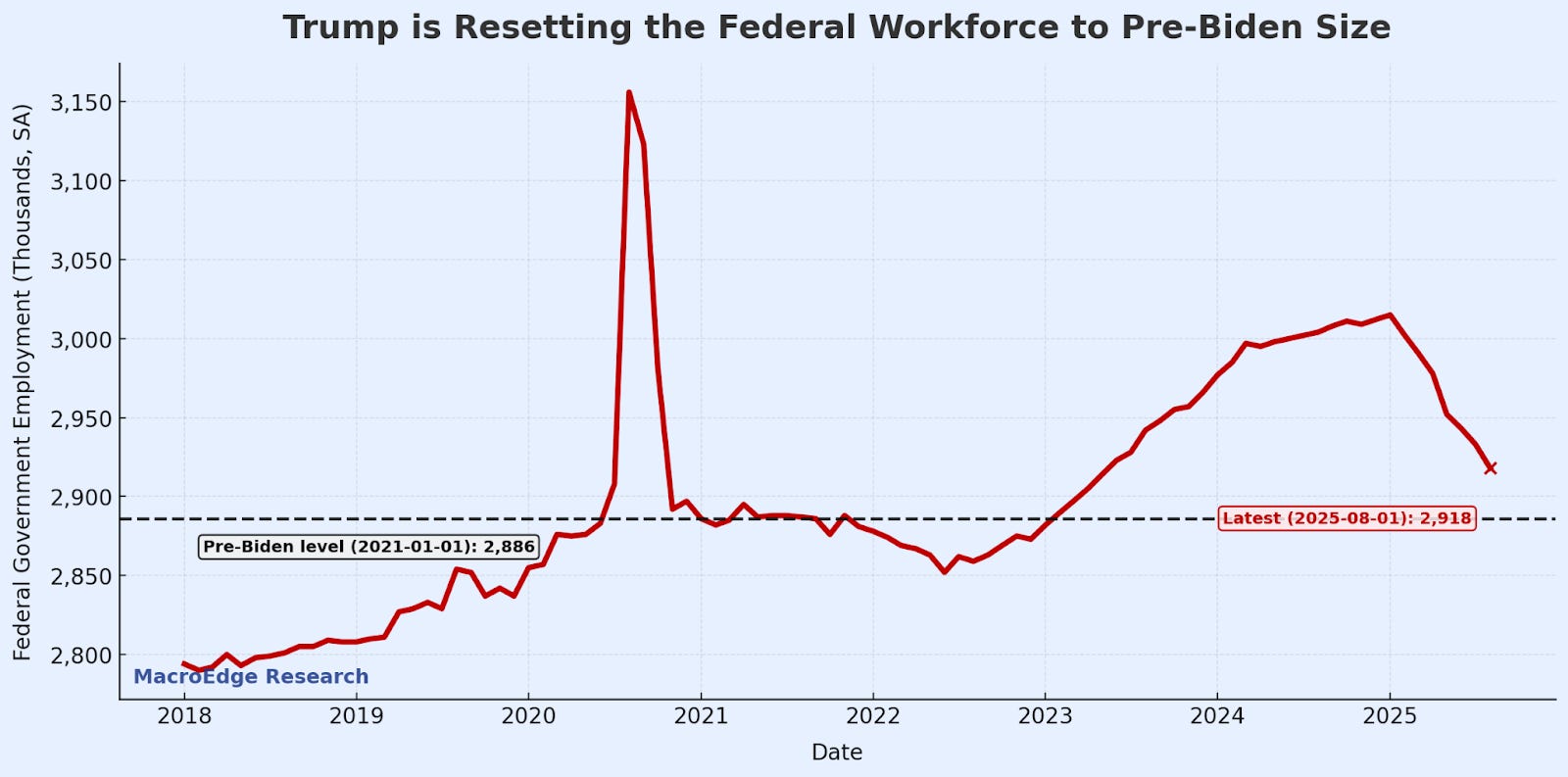

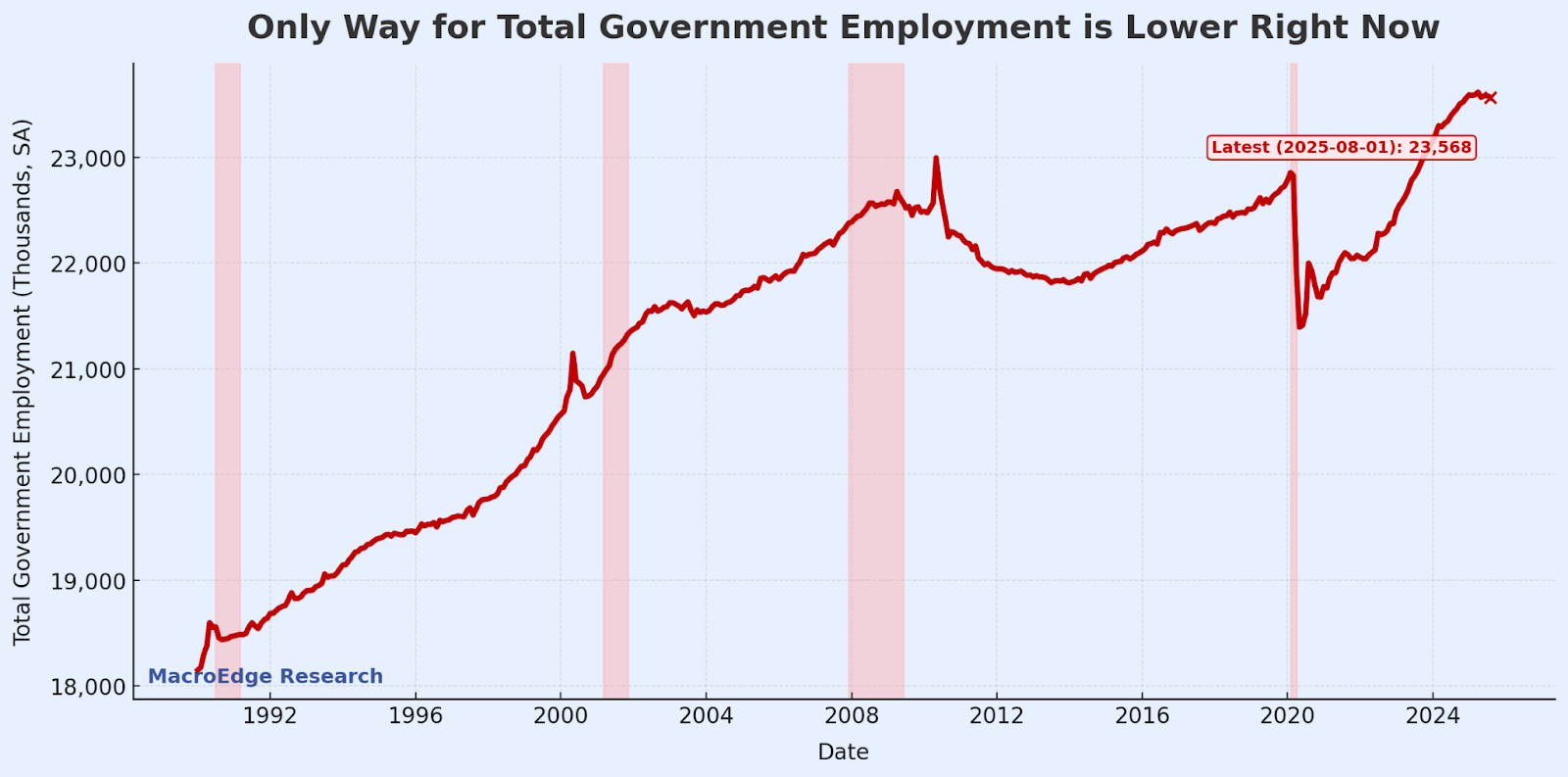

Right now, the expected government closure is pushing towards 45 days and it seems both sides have little care for impacts. Critical organizations and bodies like the DHS and military are still receiving for the time being, and it’s likely we see the next round of layoffs hit after the next paycheck lapse. The Administration is also using the shutdown to its advantage to continue trimming the Federal workforce. Back in December 2024 we noted and forecasted significant headcount changes coming to this Administration, and those have hit hard. The lever that has been pulled here is a significant one, and with the shutdown impacting payments to municipalities and states for the time being as well, expect that total government employment starts to take a hit soon, barring any new crisis or war.

For total government employment in the US (which stands at over 22 million still):

The market can’t really *react* to data that it doesn’t have, even though private sector providers like us can still paint the picture of what’s going on in the labor market. The October cut is about as guaranteed as they come right now, and a soft ADP headline print will seal the deal on both October & December.

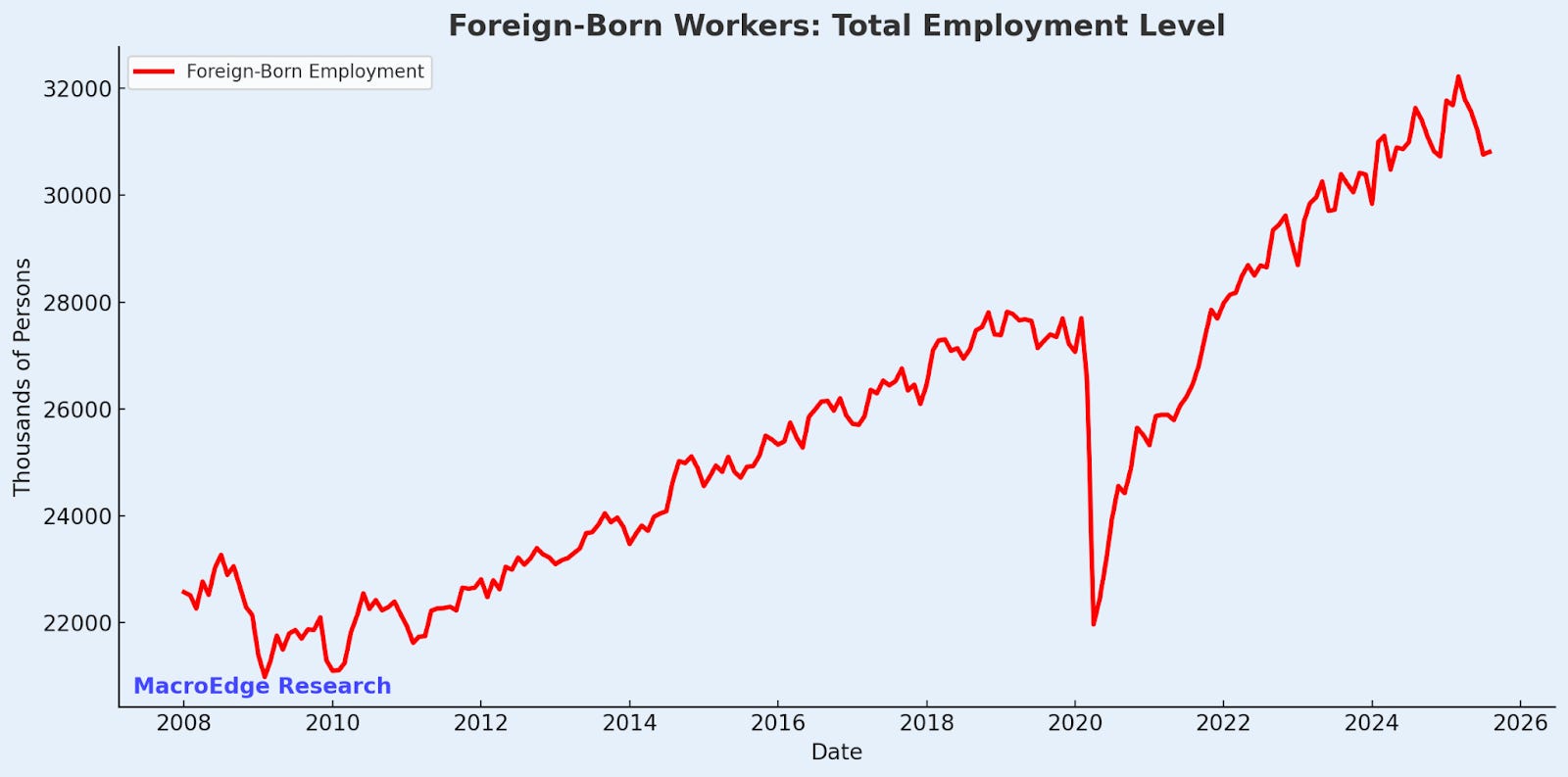

It cannot be understated that the ‘human stimulus’ effect was absolutely enormous from 2020-2024 under the previous Administration - which resulted in massive housing inflation, COL boosts, and papered over what was the *most obvious recession* in 2022. A small percentage of that has started reversing, with foreign born employment down 822K y/y:

For the time being, as discussed yesterday evening, the Administration remains hyper-focused on equity prices, though there are signs of cracks that we continue to watch as ‘fault lines’ for a broader pre-positioning, before potential larger moves that we seek to capture.

Included in tonight’s Weekly Macro Note:

Institutional Research Update

Weekly Macro Data & Earnings Review

Sunday Night Negotiations with Himself

China Overview

Special CPI Report

Losing Steam

Institutional Research Update

The MacroEdge Institutional Research Portfolio (MIRP) holdings and performance were updated yesterday evening.

MacroEdge Institutional Research is doing more than just delivering all of the data, research, and critical forward looking insights contained in Ozone – we’re turning research into positioning.

Learn more about Institutional Research below, and get 4-week access:

Weekly Macro Data & Earnings Review

A major earnings week

Lots of regional bank earnings releases

Megacap earnings

CPI on Friday

Sunday Night Negotiations with Himself

We’ve now pivoted into a unique time where the President & his Cabinet members are seemingly negotiating with themselves through social media posts. That was on display again tonight - as he negotiated soybean tariffs and the upcoming 100% tariff deadline with himself.

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.