War Update: Latest Oil & Gas Market Developments, Hormuz Closure, Positioning for Upside

In this War Update - we discuss the latest oil & gas market developments, highlight the steep drop in tanker traffic and oil output with cuts in Iraq and Saudi Arabia, discuss opportunities, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Tuesday evening MacroEdge Readers & Community,

This evening, I am sharing a quick update on oil and gas markets with the latest developments in the Middle East. I was going to share this quick note early this morning, but there were rapid developments happening throughout the day that made it very difficult to piece together an entire article.

As the conflict continues to evolve - especially given our global macro focus, we can publish these as frequently as you would like - and as they help our clients position themselves for things like energy market volatility and opportunities.

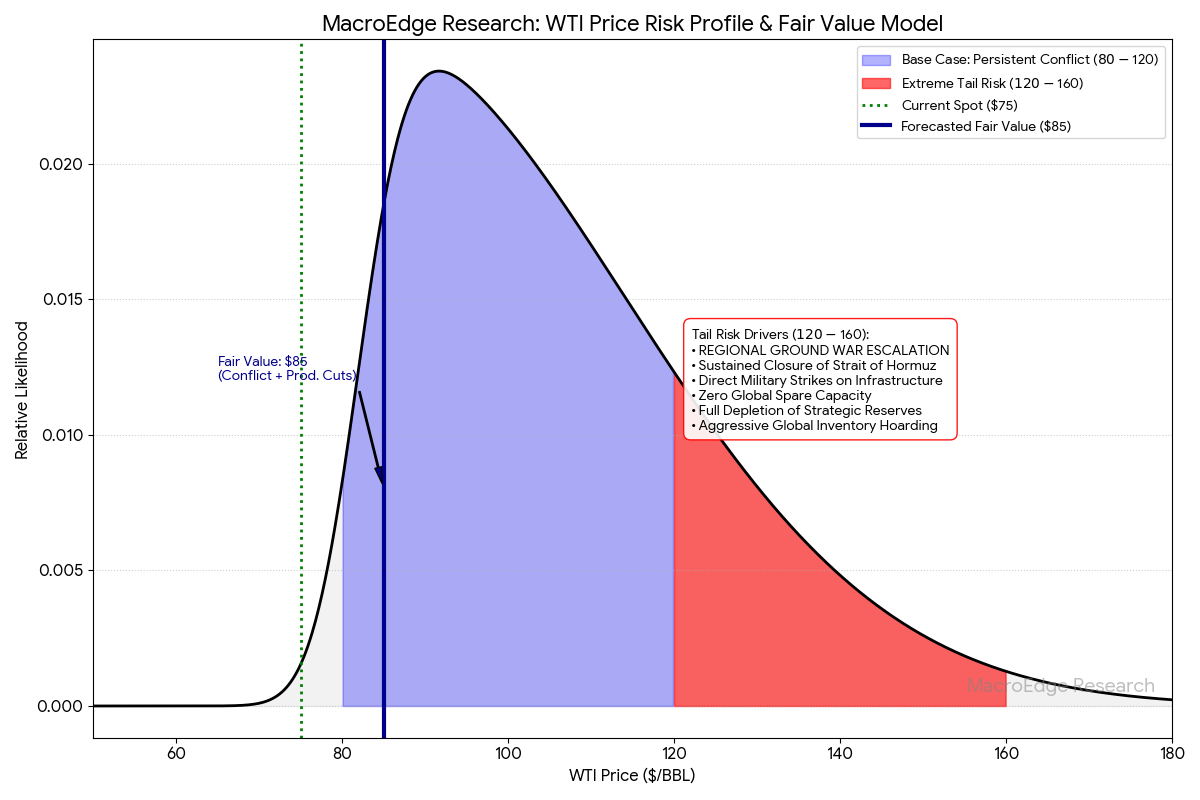

The right tail for oil is much higher, and I currently have a fair value (with no change in market conditions) in the mid-80s (baseline), on the right-tail scenario, this would land WTI between 120-160, likely for a very short period of time, as the impact would likely have a significant negative impact on the economy… remember the spike in 08?

We’ve gotten a lot correct about this conflict and positioning thus far, and I appreciate many of you highlighting our forecasts and comments on X. Getting things correct is one of the core reasons why many continue flocking to see an alternative view, and all of this will become part of our broader vision as we continue to expand our reach through the year.

Tonight I won’t focus on things like KOSPI implosion (a core component of the MacroEdge Global Bubble Index), and we’ll review that in the next Midweek Macro Note. Below you’ll find the latest energy market developments from the day, positioning ideas for upside, and more in the commentary.

Not a MacroEdge Ozone subscriber? Don’t miss a beat on all of our research, data, portfolio strategy, and more, by joining Ozone below. Feel free to experience Ozone for a week, on us.

Latest Energy Market Developments (output cuts & more)

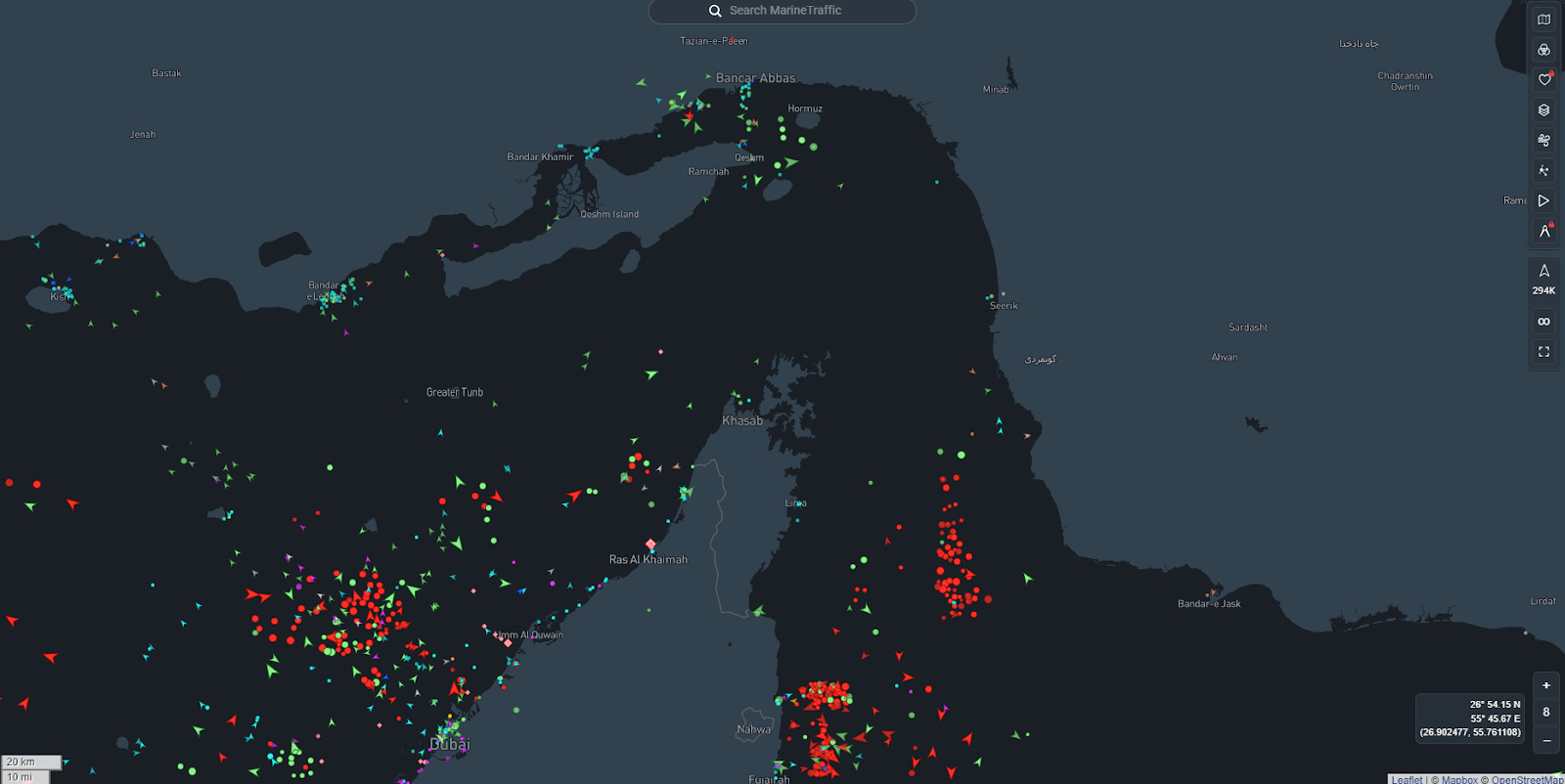

Oil traffic through the Strait dropped to the effective zero bound today, which is a positive tailwind for prices.

Brent Crude is currently sitting >$83/bbl.

Iraq Production Freefall: Iraq’s Oil Ministry has ordered massive shutdowns at southern fields, including Rumaila (-700k bpd), West Qurna 2 (-460k bpd), and Maysan (-325k bpd). Officials warn that the current 1.5 million bpd cut could widen to 3 million bpd within days as onshore storage reaches critical capacity.

(Continued below: latest energy market developments continued, Iran’s unconventional war strategy, current energy exposure and opportunities)

Strait of Hormuz Blockade: The Strait remains effectively closed for a fourth consecutive day. Total vessel traffic is down 94% since the start of the conflict. Major carriers (Maersk, MSC, Hapag-Lloyd) have suspended all transits, and war risk insurance has been canceled by major P&I clubs (Gard, Skuld, London P&I).

Aramco “Ras Tanura” Offline: Saudi Aramco shuttered its largest refinery, the 550,000 bpd Ras Tanura facility, following a retaliatory Iranian drone strike. While the fire was contained, the precautionary shutdown removes roughly 16% of Saudi Arabia’s total refining capacity from the global market.

Trump Administration Intervention: In a move signaling significant concern over $80+ WTI, President Trump announced that the Development Finance Corporation (DFC) will provide “at cost” political risk insurance for tankers. Furthermore, he has authorized the U.S. Navy to begin active tanker escorts through the Strait to maintain the “Free Flow of Energy.”

Regional Chokepoints: Beyond Hormuz, strikes have targeted shipping hubs in Abu Dhabi, Dubai, and Oman (Duqm), effectively paralyzing the export infrastructure of the lower Persian Gulf.

Daily Supply Disruption Timeline (Feb 25 – Mar 3)

Feb 28 (The Pivot): The Strait of Hormuz closure immediately stranded 2.8M bpd.

Mar 2 (Field Shutdowns): Iraq began shutting in major fields (Rumaila, West Qurna) as storage hit capacity.

Mar 3 (Current State): With Aramco’s Ras Tanura refinery offline and the blockade holding, the total global supply hole is now 8.55M bpd (~8.5% of global demand).

Iran’s Unconventional Strategy

Iran continues to wage a largely unconventional war on the defensive side, as expected. The goal of Iran is to utilize elements of terror and surprise, as well as guerrilla missile tactics, to keep the Arab states largely crippled - especially from an export and energy standpoint.

Iran’s unconventional military strategy is built on a “missile-and-drone first” doctrine that prioritizes survivability and regional paralysis over traditional air or naval superiority. By utilizing a vast network of “missile cities”, hardened underground bases excavated up to 500 meters deep within mountain ranges, Tehran can absorb significant aerial bombardment while maintaining the capacity to launch precision-guided volleys that hold the Strait of Hormuz and regional energy hubs hostage. This distributed architecture, combined with a “proxy-as-a-service” model, ensures that even if the central command is decapitated, as it has been to a degree, autonomous cells and regional allies can continue a war of attrition indefinitely. For the U.S., any pivot toward “boots on the ground” would likely be a dramatic miscalculation (especially from an energy price standpoint), as it would trade a high-tech standoff for a high-casualty, prolonged entanglement against a regime specifically dug in for a generational guerrilla-style defense on its own rugged terrain.

Current Energy Exposure

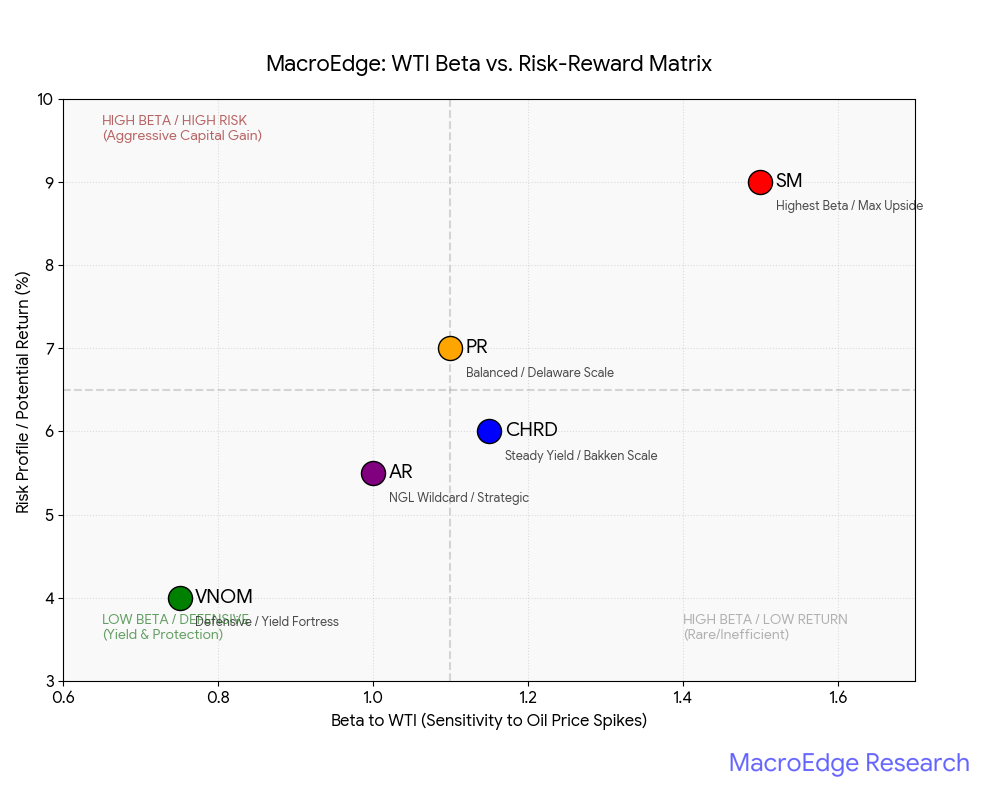

Our Portfolio Strategy currently has exposure to several E&P leaders that benefit from WTI upside, and direct exposure to the underlying commodity itself is also smart if equities lag (like they did to a degree today in the early morning spike). Energy equities - particularly E&Ps have been on a massive run in recent weeks, so a consolidation period may be warranted before a move higher to take out past all-time highs in many names.

In terms of my favorites, I continue to prefer SM, CHRD, VNOM, SM, and AR.

CHRD exhibits a high-convexity payoff profile relative to WTI due to its pure-play Williston Basin exposure and an oil-dominant production mix (approximately 57% crude). With a 10-year inventory of low-breakeven assets ($< $40/BBL), the enterprise operates as a high-margin cash flow engine with significant operating leverage.

$75 Scenario (Current): CHRD maintains a robust 16%+ FCF yield, supporting its $5.20/share base dividend while executing a maintenance-level CapEx program ($1.4B).

$85 Scenario (Fair Value): Incremental margins expand as 4-mile laterals reduce F&D costs by 21%, driving FCF toward the $1.2B+ range and accelerating opportunistic buybacks.

$100+ Scenario (Tail Risk): The “blue-sky” state triggers unhedged upside participation, where extreme cash flow generation shifts the focus from yield to significant NAV accretion and rapid debt extinguishment.

SM Energy (SM) * $75 Scenario: Generates steady FCF with a ~54% oil weighting, prioritizing its 80% FCF allocation to debt reduction following the Civitas integration.

$85 Scenario: Triggers a ~$600MM annual FCF tailwind (based on $300MM per $5/BBL sensitivity), accelerating the shift toward its 20% share repurchase allocation.

$100+ Scenario: Massive margin expansion on 2H26 production run-rates (420–430 MBoe/d) drives rapid deleveraging toward a <0.5x target.

Antero Resources (AR)

$75 Scenario: Focuses on Marcellus dry gas margins; leverage stays below 1.0x following the Utica divestiture and HG acquisition.

$85 Scenario: Indirect benefit via NGL price correlation (C3+ liquids); FCF accretion supports the $1B D&C maintenance program.

$100+ Scenario: Significant uplift in realized liquids pricing (213 MBbl/d) provides a “liquids kicker” that dramatically offsets any natural gas basis volatility.

Permian Resources (PR)

$75 Scenario: Maintains cost leadership ($675/ft D&C) and a 3.6% dividend yield; leverage tracks toward 0.7x.

$85 Scenario: 97–100% WTI realization captures the full risk premium; 5% YoY oil growth compounds the FCF per share accretion.

$100+ Scenario: Operational “high-side” where capital efficiency and scale in the Delaware Basin generate outsized returns, likely triggering special dividends or accelerated M&A.

Viper Energy (VNOM)

$75 Scenario: Pure-play royalty model (zero CapEx) provides a high-margin yield; base dividend remains fully covered even below $30 WTI.

$85 Scenario: Revenue scales linearly with price; integration of Sitio assets drives FCF toward the $1.3B+ consensus estimate.

$100+ Scenario: Maximum cash-conversion state; with no inflation-sensitive D&C costs, nearly 100% of the price spike is distributed as cash available for distribution.

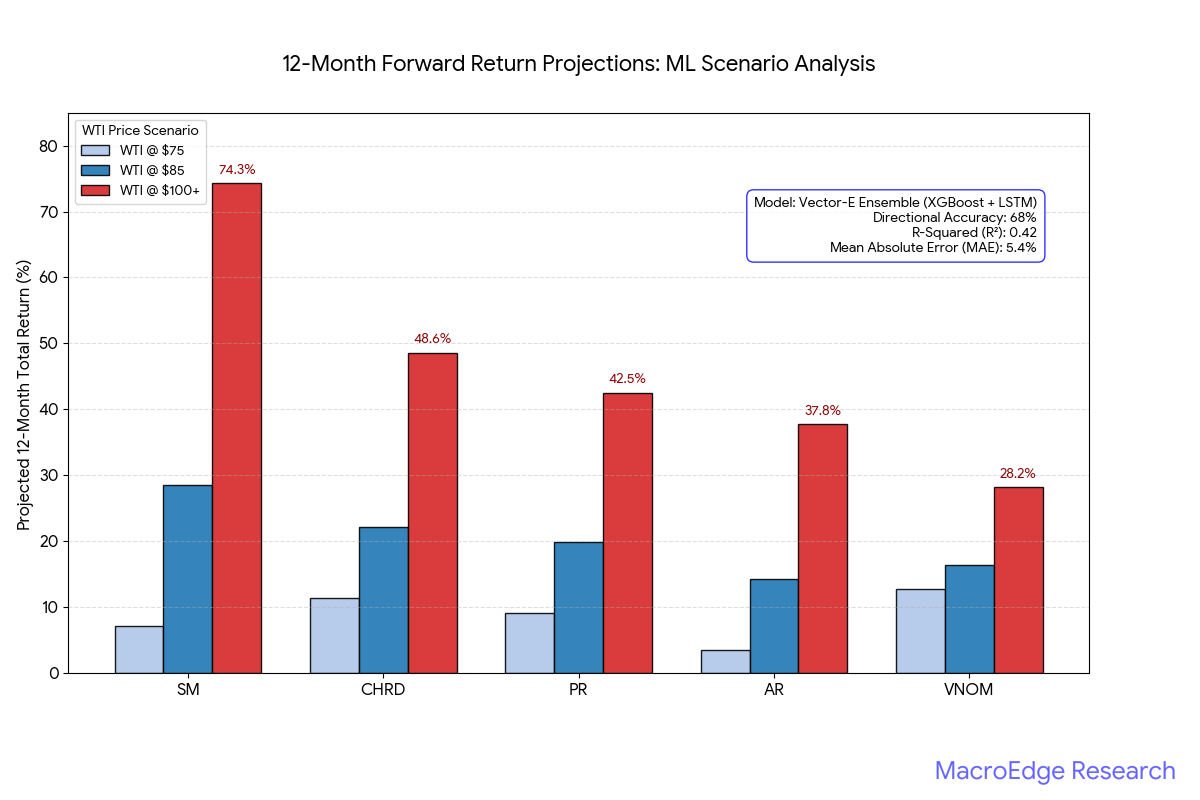

MacroEdge ML Model Details

Model Architecture: The Vector-E Ensemble combines gradient-boosted decision trees (XGBoost) for structural feature extraction with Long Short-Term Memory (LSTM) layers to capture temporal and geopolitical risk patterns.

Accuracy Metrics: * Directional Accuracy: $68\%$ (High-confidence directional bias)

R-Squared ($R^2$): $0.42$ (Significant explanatory power for volatile commodity equities)

Mean Absolute Error (MAE): $5.4\%$ (Tight error variance for 12-month returns)

For more details, please refer to our Terms and Conditions.