War Note: War is Inflationary, Latest War Updates, Energy Markets Review, Asian Volatility is Accelerating

In the War Note we discuss the war being inflationary, highlight the latest war updates, discuss the latest energy market data, and look at Asian volatility #MacroEdge

Don Johnson (@DonMiami3), Chief Economist

Good Tuesday evening MacroEdge Readers & Community,

This evening we are resuming the War Note series to match the resumption in the US-Iran conflict. As airstrikes have escalated in recent days, the President notified that he expected the conflict to continue for at least 60 additional days, which I expect is due largely to the desire to continue letting inflation and nominal asset prices run at ‘hot’ levels until at least the midterms. The consumer economy in the lower 80% is softening now at a brisk pace - especially in real terms - and they want to mask that slowdown by turning back on the nominal wealth effect. It’s ugly, but it’s really the last lever they have to pull before midterms…

With oil having rebounded sharply over the last week (Brent neared $88/bbl and WTI >$80bbl) that will dampen some of the YoY energy disinflation celebrations that we saw on the networks today. I will discuss the inflationary nature of this war - especially in the context of nominal assets - below in ‘war is inflationary’ and we’ll take a look at the latest war updates. From there - we’ll dive into the latest on energy markets which have acted favorably from our calls over the last few weeks - with crude prices up sharply from the lows, and tier 1 energy names like CHRD moving higher. Energy prices have rebounded to pre-MOU levels, and I continue to think Iran & GCC nations want Brent around this $85 ‘magic’ level - because >$105 = trouble, and those that view oil in real chained terms miss the YoY base effects impact.

Brent is up $14bbl from the MOU lows:

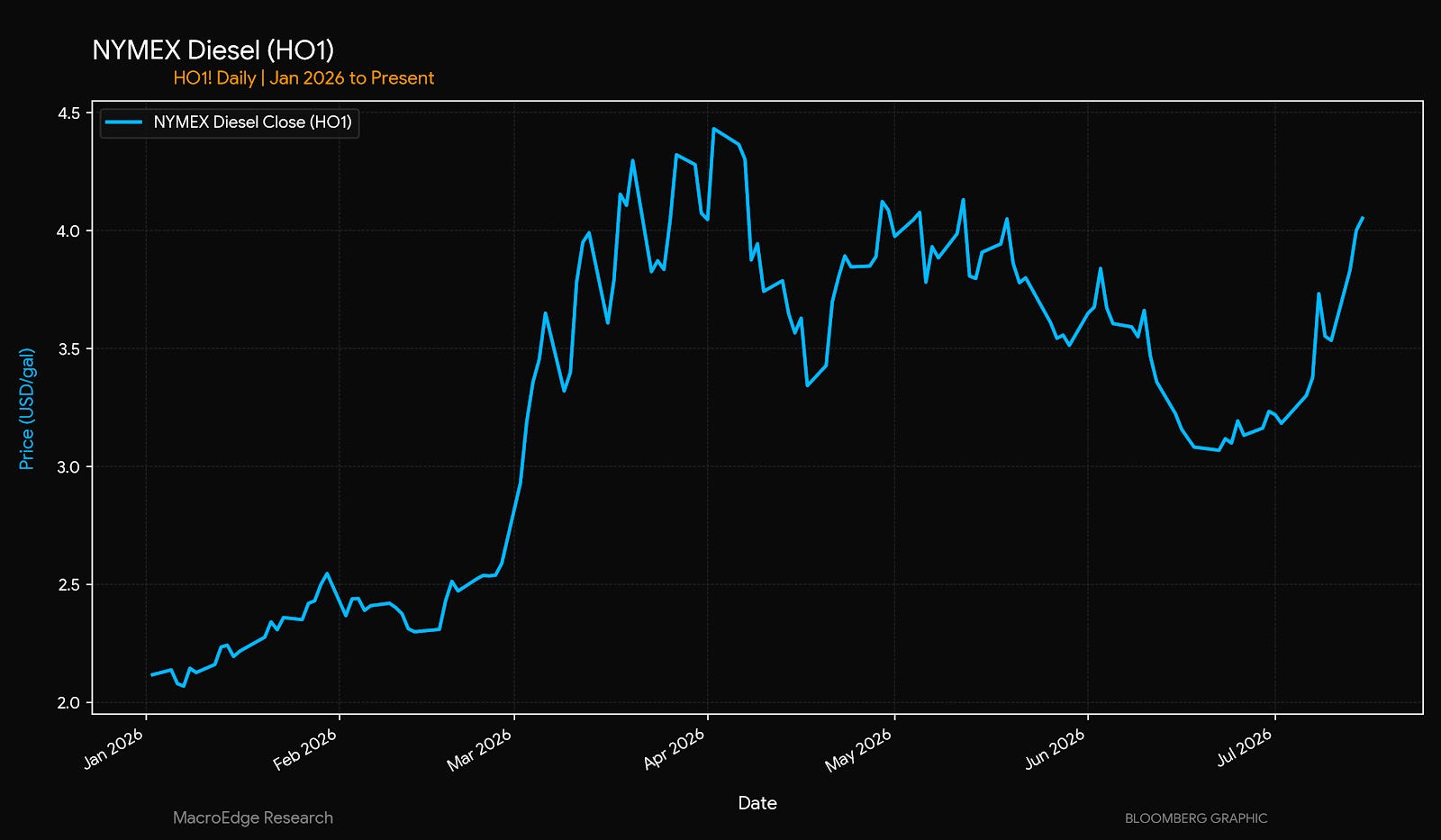

Diesel is back near cycle highs as Ukraine attacks on Russia accelerate, and the Strait remains effectively closed.

Quote of the day…(maybe one for the KOSPI investors too)

Lastly, we’ll look at volatility and Asia and how that continues to signal trouble ahead in 2H as leverage, central bank issues, weak currencies, yields, and the worst speculation in Asian market history collide to cause problems. I do not expect that the party is yet over in Asia - and given how reliant South Korea and Japan now are on the wealth effect to offset a weak currency, they want to pump their markets higher just like the US does. We’ll take a look at the latest below in part 3 of our Asian market analysis updates…

Next Reports on Deck:

Midweek Macro Note & An Analysis of ‘Trump v Warsh’ - Project Argentina versus Project South Africa, Portfolio Strategy Commentary, and More

Redeye Macro Note - Friday: Reviewing the Close of the Week, Asian Review Pt. 4

Saturday Macro Note - Non-Op Oil and Gas Opportunities - Our Partnership for the Future

Sunday - Weekly Macro Note

Not yet a MacroEdge Ozone paid subscriber? Upgrade to paid Ozone below, and get all of the latest MacroEdge research, portfolio updates, strategy, and much more:

War Is Inflationary - It’s Just the Truth

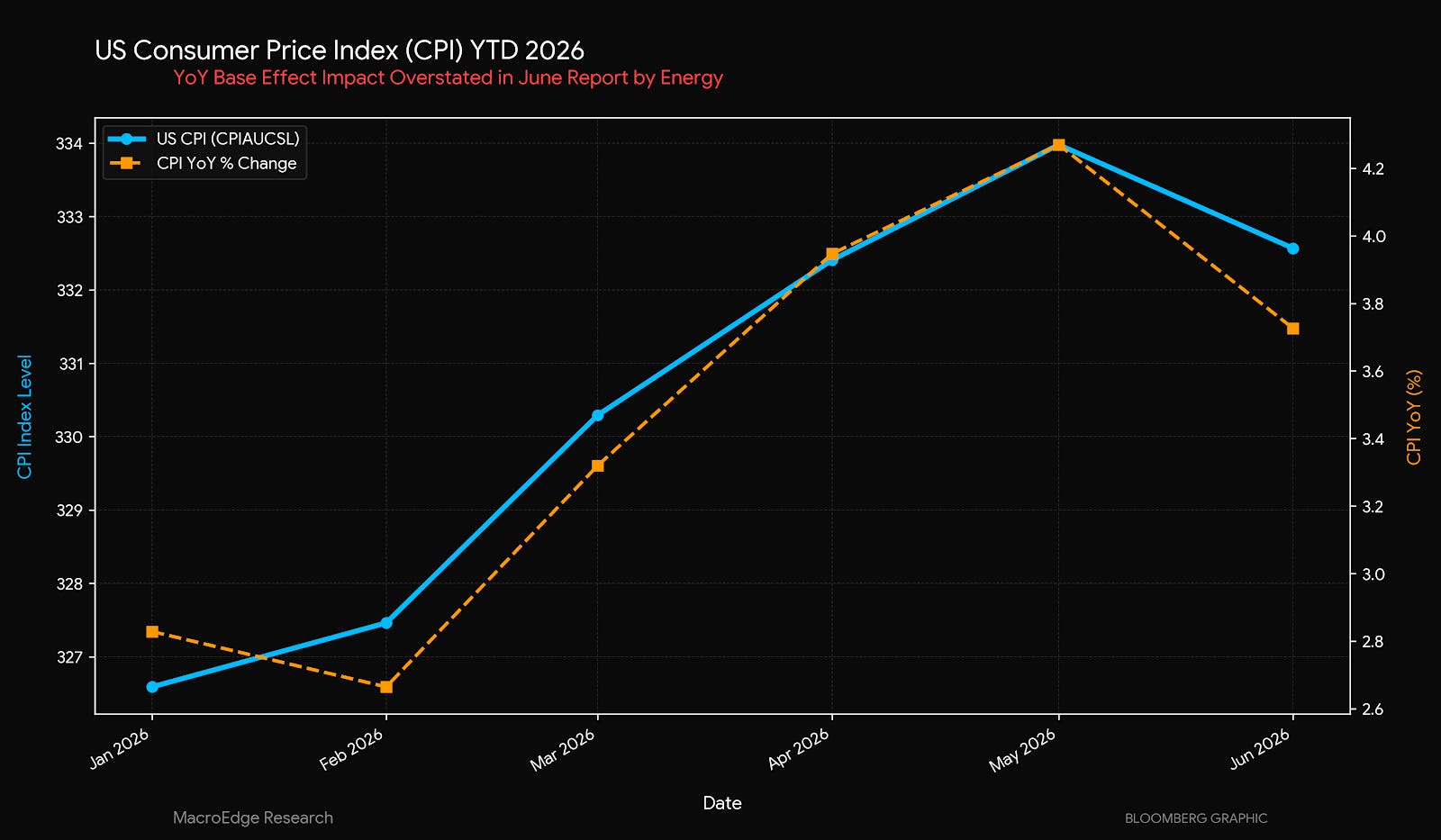

While John will discuss the inflation data (and report) from June more in-depth, I am in the camp that the risk of inflation is still much larger than disinflation. Yields are in no way, shape, or form providing us any valid signal on disinflation right now, and I think with the war picking up steam in recent days - the risks are that they turn the inflation machine on for the rest of the year to keep things masked past midterms. The economy in real terms is going to continue to slow now - especially as we lose momentum in the AI space with the data center buildouts, though that may be more of a 2027 than Q4 2026 story as I originally anticipated.

On the inflation review for June - I would be cautious in overstating the impact of this report - while it bought time to prevent a rate cut, yields certainly didn’t care a whole lot.

The path of least resistance will continue to be letting inflation run hot - and this one-off to prevent a necessary hike will not continue if oil, gasoline, and food prices rebound sharply in July/August.

The massive ‘blowoff’ occurred as the war worsened, and inflation ripped earlier in the year:

This time, if energy prices get to a high enough level - this will not be the same dynamic - though I do expect that we will see volatility increase across the globe. The chance for another melt-up leg higher is still there, but energy prices will get the final say in how short that may be.

Latest War Updates

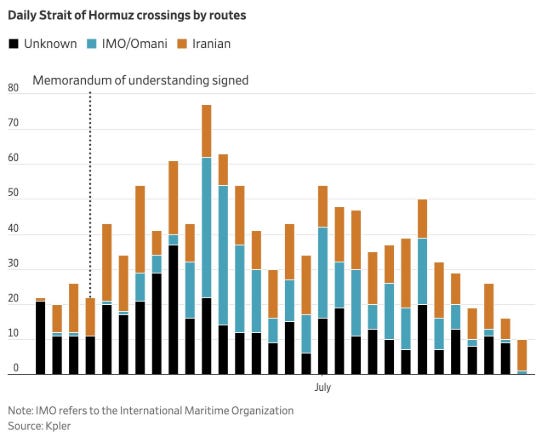

On the latest for the war - the Strait of Hormuz is almost completely sealed off to commercial traffic again. We’re back at the sub-5 level for transits, and this is going to cause another commodity-driven inflation wave to bubble under the surface the longer this goes on. I really don’t anticipate that anyone can afford to have this last another 60 days given oil inventory levels (which continue to decline globally ex-China, and will begin declining in China soon) - and the US SPR is now nearing the 300 million barrel level (Congress has a min 254mb level).

The Strait is seeing traffic return to full war levels, and the blockade is now back on:

While inflation and assets may benefit from inflation in the Iran war - the lower 80% in the economy will suffer more the longer this conflict continues - that will be especially noticeable again in the global south, though it will be quite quiet and without significant media coverage.

An overview of the major updates over the last 12 hours:

Fourth Night of U.S. Strikes: U.S. Central Command completed a seven-hour wave of precision air strikes on Tuesday night, targeting Iranian coastal defense systems, missile and drone launch sites, and naval capabilities along Iran’s southern coast.

Retaliation in Bahrain and Kuwait: The Islamic Revolutionary Guard Corps launched retaliatory attacks against U.S. assets, using cruise missiles to strike and set fire to a major U.S. military logistics center at Mina Abdullah in Kuwait, while also targeting U.S. Fifth Fleet facilities in Bahrain.

Interceptions in Jordan: Jordan’s air defenses intercepted and shot down three Iranian ballistic missiles that entered the kingdom’s airspace, which followed an Iranian drone strike aimed at Jordan’s Al-Azraq airbase.

Threats to Global Energy Corridors: Asserting a “for everyone or for no one” stance on regional oil, the Guard Corps threatened to block all alternative energy export routes in the region if the U.S. naval blockade of Iranian ports persists.

Trump Escalation Warnings: U.S. President Donald Trump warned that air campaigns will intensify next week to target civilian infrastructure, specifically power plants and bridges, if Tehran refuses to negotiate a deal. (We’ve seen this before, and he will walk it back just as the Hormuz tolls got walked back)... brinkmanship is how he ultimately ends up getting back at the negotiating table, which is really just the ceasefire table…

Energy Markets Review

Thus far in July, there has been fewer than 4 million barrels of oil are exiting the Strait of Hormuz per day (an 8mb reduction from normal levels).

Ukraine attacks on Russian energy infrastructure and tankers continue to worsen - this is being reflected in gasoline and diesel spreads - which are at all-time highs.

Gasoline markets are near record-tight levels, and prices by the end of the week are going to be back above $4/gal or so on average in the United States.