War Note: Operation Freedom Suspended, Energy Equities and Earnings, Frac Spreads, and More

In this 'War Note' we discuss the abrupt suspension of Operation Freedom, highlight the potential for conflict flare ups, discuss energy equities and their earnings thus far, frac data, and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Tuesday evening MacroEdge Readers and Community,

This evening, we’re going to briefly cover the latest developments of the week, with the latest geopolitical updates and coverage of some of the macro data and market action we’ve seen to start the week. Today marked another day of ‘crash up’ price action on the back of slightly lower WTI prices and yields. The 10Y is above Bessent’s danger zone - and looks set to continue higher - but investors remain in a crisis mode, flooding into equities across the globe - but most notably in the US, South Korea, and Japan - where technology (and semiconductor) equities continue a record-setting ‘crash up’. It is impossible for the time being to step in front of a freight train, and with debasement running at full throttle (with the Fed expanding its balance sheet), the signals have not aligned to signal downside for the time being in the beta equity basket.

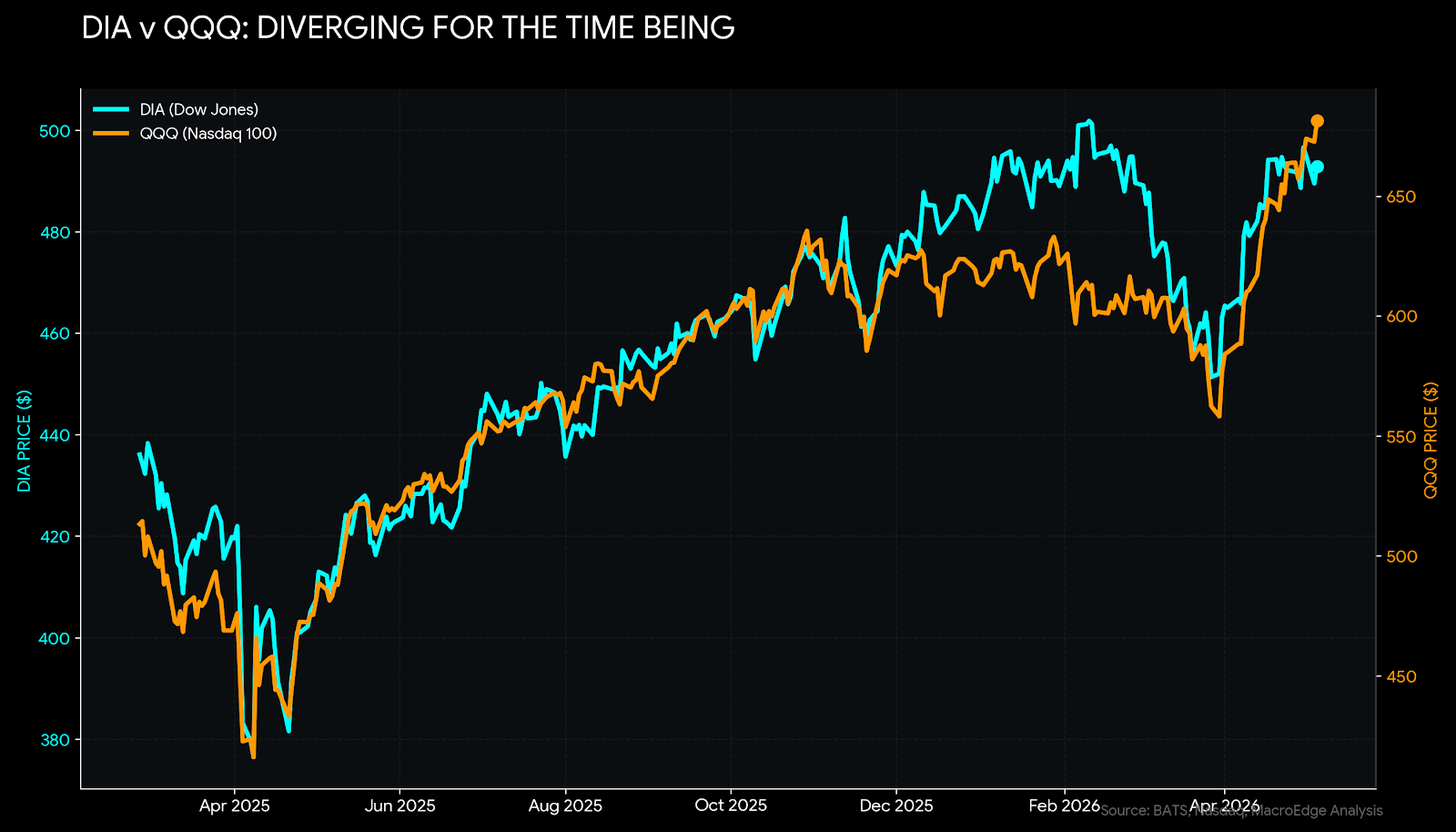

Needless to say, the Dow has continued to lag broader equity market acceleration - and inflation expectations continue to move higher - the investors… and especially the retail investor crowds… have their ears plugged to anything resembling reality right now as absolutely asinine figures are dropped daily in the AI capex-sphere. Regardless of whatever is happening in that space, our focus continues to be on the macro-heavy side of things in commodities and energy, more specifically. The situation is worsening by the week, and the API readings today were extreme in terms of the inventory draw. We’ll get the latest EIA data tomorrow, along with the latest update on SPR levels, but the oil market remains extremely mispriced relative to the fundamentals of 13.5-14mbpd remaining offline. Even though US firms like Diamondback are pledging to boost output slightly in their earnings calls, it doesn’t even come close to what is required to resolve the physical shortages and drawdowns.

Continue to pay close attention to this performance divergence here - though for the time being it is not a major red flag for the technology sector as the ‘crash up’ continues:

Tomorrow we will get the latest Fed balance sheet readings, which will show another w/w increase, and the Treasury is heavily involved in global market stabilization as the conflict continues in the Middle East. As discussed below, the Fed is letting inflation run ‘hotter for longer’ though don’t expect them to play ball forever as other central banks continue to move their policy rates higher, like Australia, which hiked for a third meeting in a row. As stated over the past 12-16 months, it is not until Japan begins easing and we see the MacroEdge Global Bubble Index roll-over before we start to see any sort of pain in US equities. With leverage and max risk-on for a variety of reasons, the insanity will continue, so I am continuing to play ball in the niches we know and understand best while the crowds flock to risk.

I look forward to providing our next updates over the coming week from Texas as I depart tomorrow midday towards the Panhandle of Texas. We’re meeting with stakeholders in the ag-space for our ‘On the Ground’ series Part 1.

Not yet a MacroEdge Ozone subscriber? You’re missing all of our research, data, portfolio strategy, and much more, along with future product updates with things like Portfolio Strategy & TREX. Upgrade below:

War Update: Operation Freedom Suspended

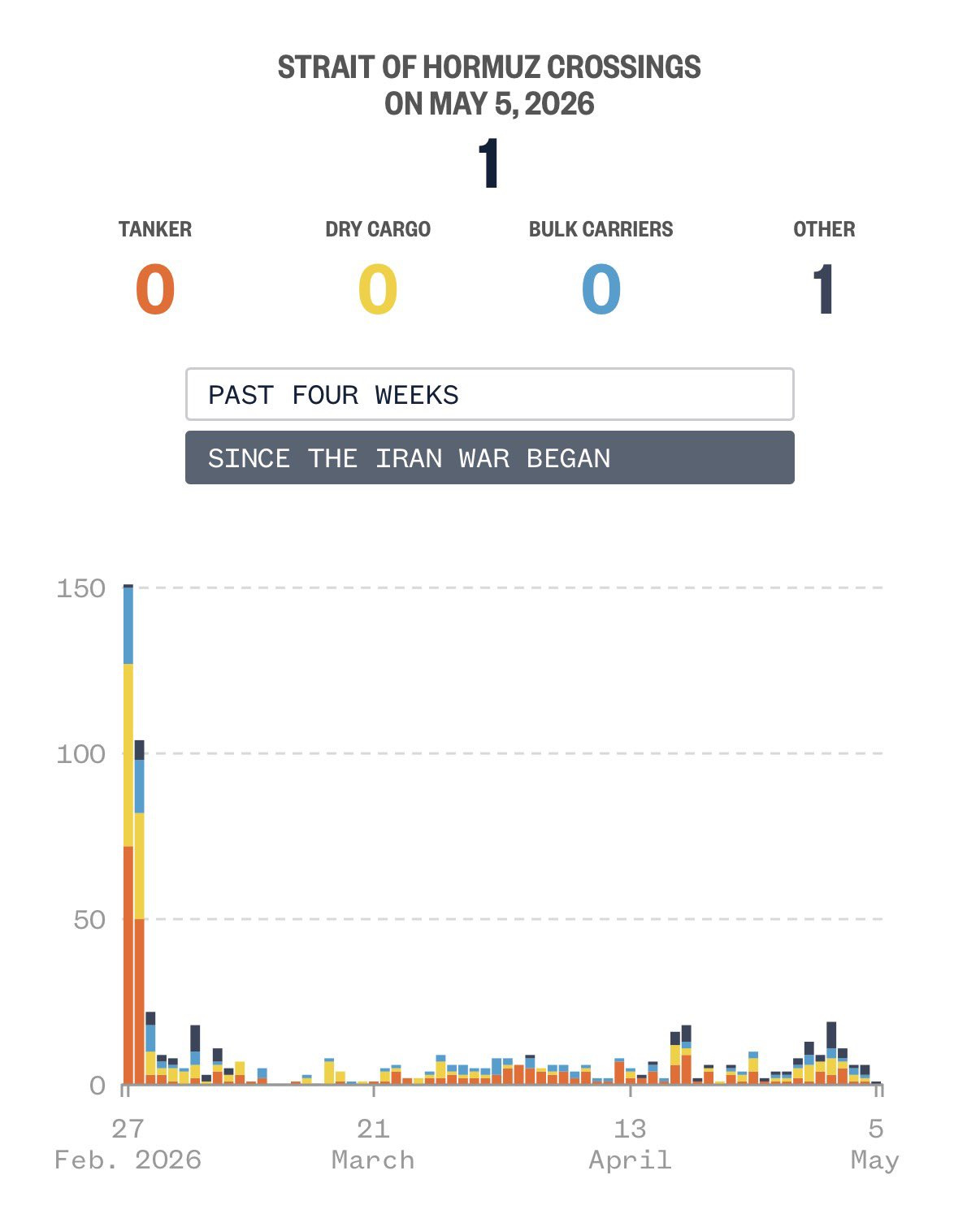

This evening, after market close, the President announced the immediate suspension of Operation Freedom. This came on the heels of the news of the API draw (discussed below) and the Strait of Hormuz traffic update, which highlighted just 1 ship crossing the Strait in 24 hours.

(Source: JaguarAnalytics on X)

While we continue to reside in total fantasy land for the time being, this is absolutely going to catch up at some point - regardless of printing or not. Operation Freedom was yet another botched idea to actually get traffic moving through the Strait - and it’s going to take more for the Iranians in terms of concessions to restore things on the traffic front. I expect that the situation in the Strait will likely not return to *normal* now before late summer or fall right now in terms of traffic levels - especially with the stated goals of the IRGC in maintaining long-term control of the Strait as a revenue stream (of course the power factor is relevant, too), though don’t expect GCC countries to want to play ball with that for any long period of time. The infrastructure is simply not there in the Middle East for the closure to not impact things on a much larger scale in the coming months, and it would take years for the GCC to build out and up workarounds to the Strait if that was something they actually wanted to pursue.

Expect that these wild jawbones will continue while they still work, though the EIA data tomorrow could be another wake up call for the Administration that they better find a way out of the situation quickly, or things are going to get much, much, much tighter on the oil front over the summer.

Latest API Crude Stock Reading… Yikes

The API reading was another wake up call for inventory level doubters today - with total products falling by about 24 million barrels.

(Continued below: Latest API Crude Stock Reading… Yikes (EIA Tomorrow), Energy Equities… Blowout Earnings for the Most Part Thus Far, and Commentary), available with Ozone…

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.