War Note 2: The Crude Reality of Middle East Wars, Oil & Gas Equities

In this 2nd edition of the 'War Note' - we talk about the crude reality of Middle East Wars, and oil and gas equities. We also discuss impacts to the Strait of Hormuz, total oil/gas disruption, & more

Don Johnson (@DonMiami3), Chief Economist

Good Wednesday evening MacroEdge Readers & Community,

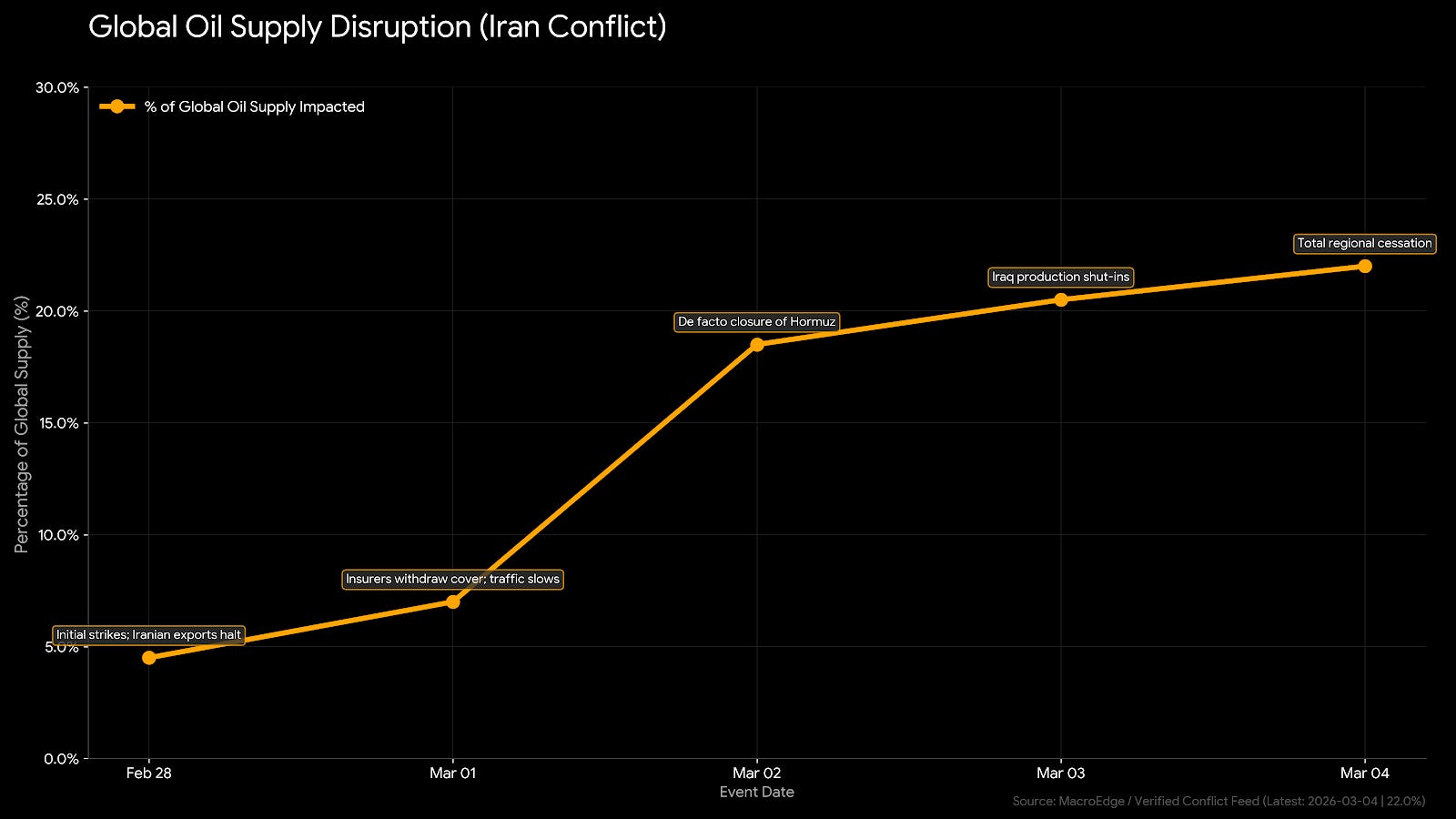

Due to community request, I am assembling another brief War Macro Note (#2) to cover the latest developments in energy and shipping. While US equity markets largely shrugged off the Middle East dynamics, I am shifting our focus to energy markets. With the Strait of Hormuz effectively closed, about 20% of the world’s energy supply is currently frozen/offline. This is a significant number that is going to have a much larger effect in days to come as the ‘off-ramp’ window shrinks. While the Administration and media are intervening in energy markets to a great degree through headlines, I am focused on the Friday off-ramp window as the signal for things to go much, much longer than anyone, including Wall Street, is currently expecting.

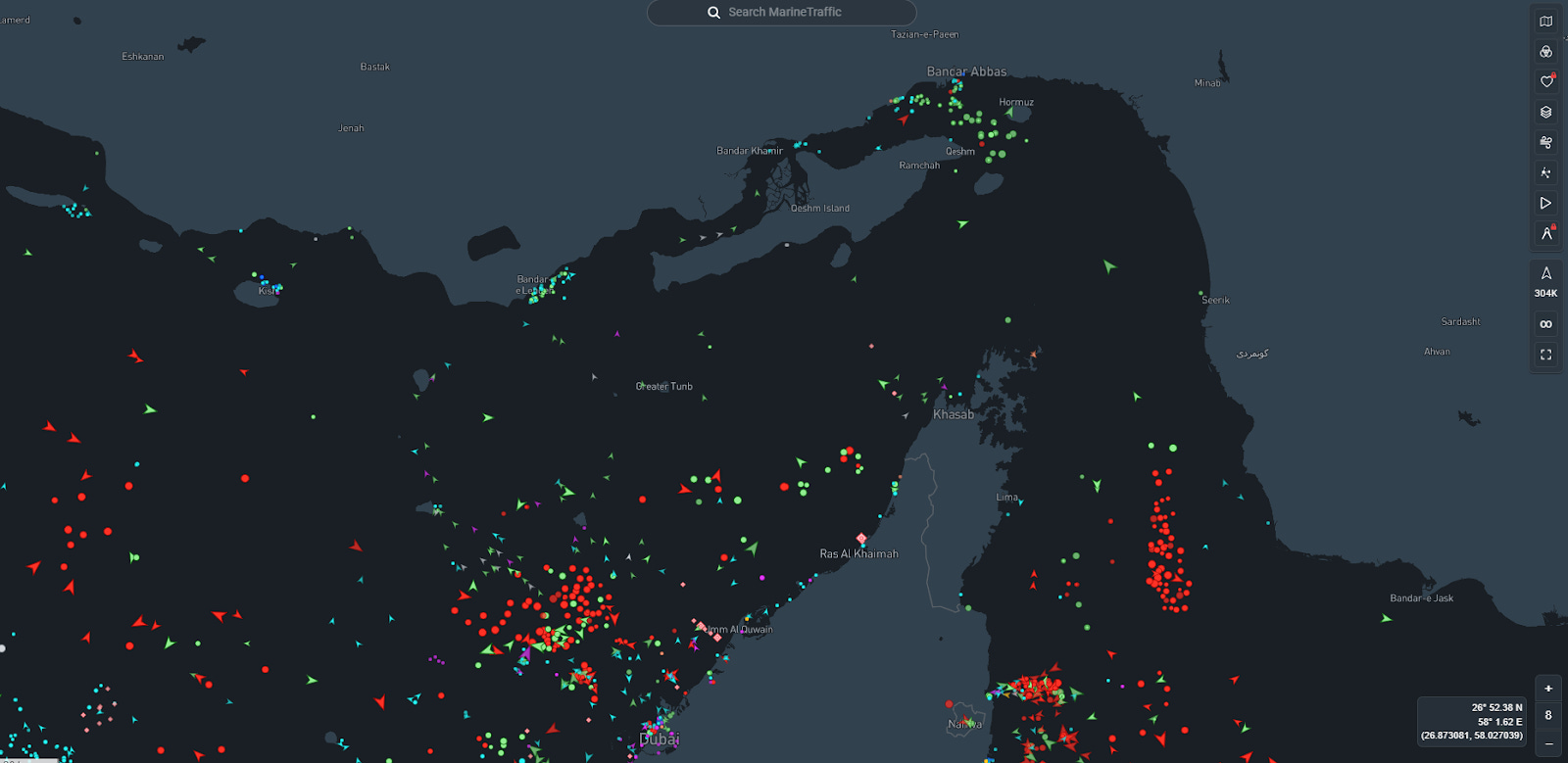

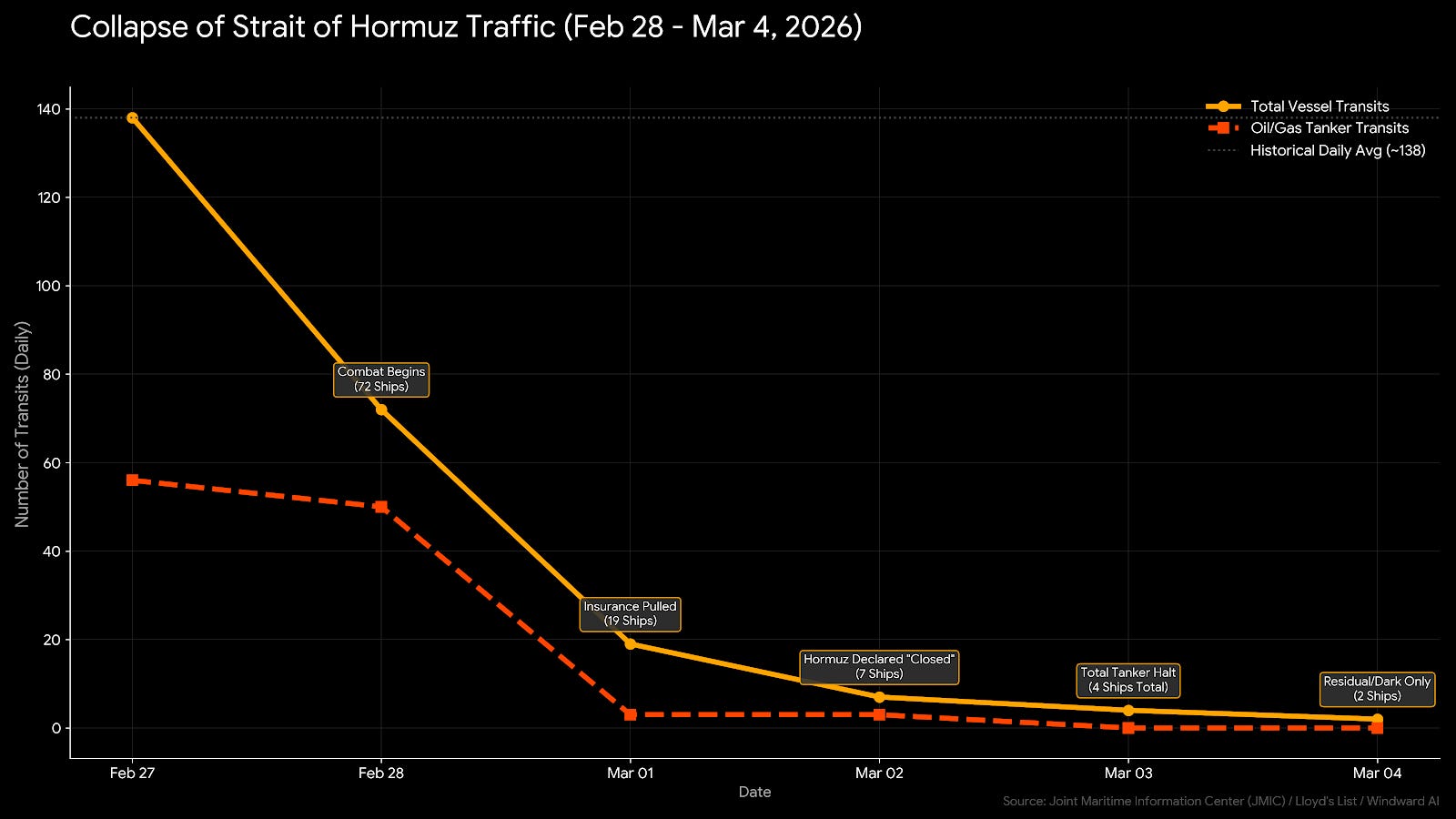

The Strait of Hormuz is effectively closed, as of this evening EST:

Just a few Iranian vessels made it through the entire day, operationally, and it’s a very difficult spot to put US warships.

Traffic is essentially zero, and insurance won’t be issued even though politicians may demand it:

Yesterday evening, you’ll recall we discussed the right tail risk for crude, and with each passing day that the Strait remains ‘closed’ - no need for word semantics… WTI, gasoline prices, food prices, and everything down the chain will move higher. In the interim, oil and gasoline prices will be most directly affected - and I’ve marked Friday as a critical 1st peg in a point of no return in the US being involved in this war with Israel.

Today, I was very excited to see that we landed as #70 on the Top Rising in Finance list on Substack - my goal, of course, is for us to land on the permanent list in short order - but we’re committed to improving things dramatically here, our home for Ozone, over the course of 2026.

If you haven’t yet upgraded to Ozone, you can do so below and try Ozone for a week:

Tomorrow evening we’re going to talk about Friday’s ‘D-Day’ deadline line for an offramp, and why I think it will serve as a critical inflection point in the war, with thoughts on what we can expect in the coming days.

Latest Updates for Energy & Trade Today

QatarEnergy Force Majeure: Following drone and missile strikes on the Ras Laffan and Mesaieed industrial complexes, QatarEnergy has declared force majeure on LNG deliveries. This is the first time in history that Qatari gas exports have been completely paralyzed by conflict.

Strait of Hormuz “Total Closure”: The Iranian Revolutionary Guard Corps (IRGC) has declared the Strait of Hormuz effectively closed, stating any vessel attempting transit will be set “ablaze.” Insurance coverage for the region has been widely withdrawn, stranding over 150 ships.

Iraq Production Cuts: Due to the closure of export routes and storage reaching capacity, Iraq has been forced to shut in 1.5 million barrels per day (bpd), with warnings that another 3 million bpd could go offline within 72 hours.

(Continued below: Latest Updates for Energy & Trade Today… The Crude Reality (Upside for Oil & Gas Equities)...

European Gas Shock: The Dutch TTF (European benchmark) has surged by over 50% today alone, as the loss of Qatari LNG threatens European energy storage levels ahead of the next winter cycle.

Diplomatic Channels: Reports from the New York Times suggest Iranian operatives have signaled an openness to Oman-mediated talks with the U.S. to prevent a total regional collapse, though combat operations continue.

22% of the global oil supply is currently trapped, or offline:

The Crude Reality - Upside for Oil & Gas Equities

The Administration has bit off more than it can chew currently in terms of potential energy impacts, which is why we’re seeing such frequent interventions in the energy market through headlines. The Venezuela supply hasn’t made a dent in the global picture because it’s so small, and once the market realizes the severity of the situation (if it continues for 3-4 weeks), I am expecting for oil and gasoline to reprice to much higher levels. With our broad global macro focus, events like these are our sweet spot from a strategy standpoint, and I won’t beat a dead horse on the names we discussed yesterday evening.

RBOB gasoline futures - highest now since May 2024:

A move of this magnitude will greatly impact the Fed’s ability to cut rates, especially with base effects rolling off harder in the months to come.

For WTI, $77.5 is the next critical pivot point, and a move above could reprice oil into the mid-80s, with a likely short term correction on the next intervention announcement (like SPR). Gasoline prices are set to be up for most Americans this week to the tune of 30-50 cents, depending on your location, and that will be a feedback loop into the popularity of the war/conflict.

(Above: WTI 10m)

WTI is still not at a critical point in terms of inflation to really get alarmed about, but we’ll talk more about those levels tomorrow evening in the Midweek Macro Note.

Midweek Macro Note Tomorrow:

Geopolitical Update

Trident Note

Portfolio Strategy Note

Employment Data Forecast (NFP)

Rate Cut Odds

And More

For more details, please refer to our Terms and Conditions.