Thursday Evening Redeye - Early Redeye Release + Vision Update

In this evening's 'Redeye' release Don provides an update on our first sentiment gauge data update tomorrow, a look at the 'Wynn speculators', and an update on Vision from Six.

Sentiment Updates, ‘Wynn Speculators’ and Economic Data (@DonMiami3)

Happy Thursday evening friends, MacroEdge Readers, and the world -

Of course tonight we have some interesting volatility occurring on ‘geopolitical news’ - we have an interesting and expanding combination of mixed economic data and concerning geopolitical news out of the Middle East… The news of Iran striking Israel caused a spike in oil that has now retreated slightly. After a drop in futures - Robinhood and Schwab/ToS have suspended 24-hour trading on their platforms which is a notable development. In my mind, it’s just another day and another sequence of events in our 24/7 casino society. Much of the ‘geopolitical’ market action we saw this week, today, and this evening is a mix of a sign of the times and hype.

The market’s obsession with news like this is a long-time occurrence, especially in the information era, but I wanted to let you know that our first update to all of our new Vision Equity Research tools in the Dashboard will see their first updates tomorrow evening. Much of what we focused on in the Redeye last weekend was the ‘Nirvana’ narratives present among speculators and many retail investors who would find a better home at the blackjack table at the Wynn:

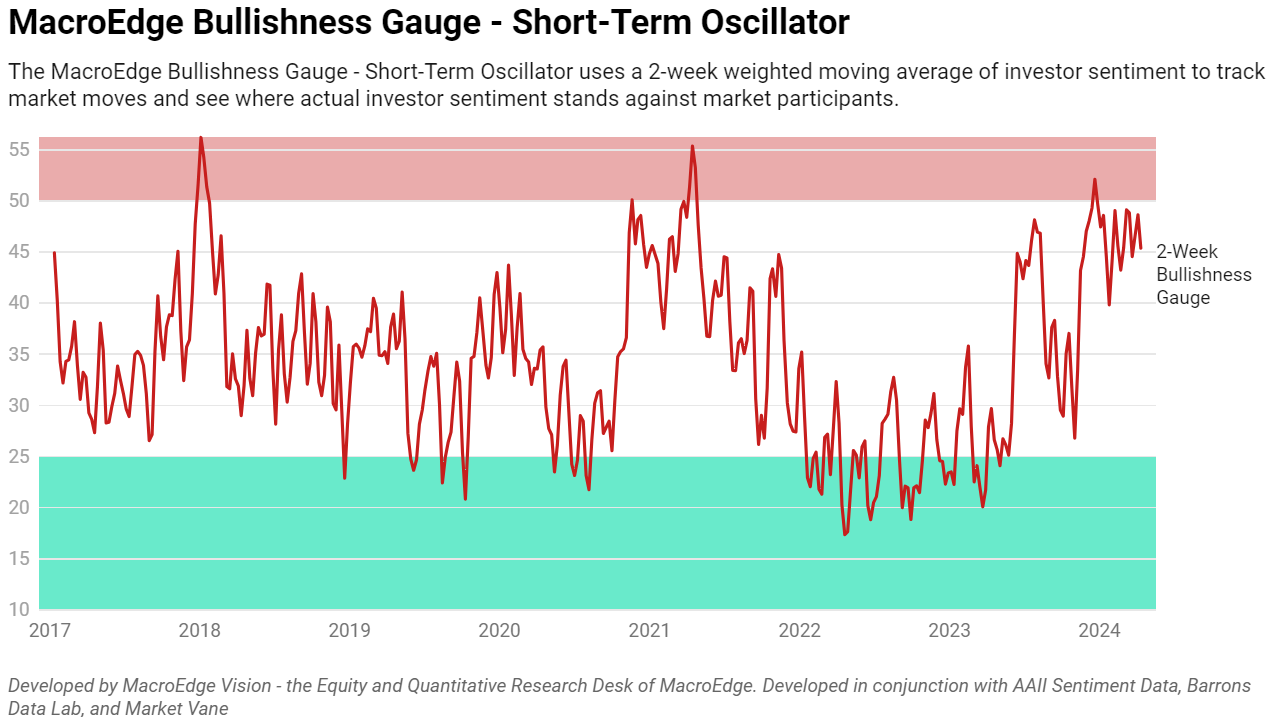

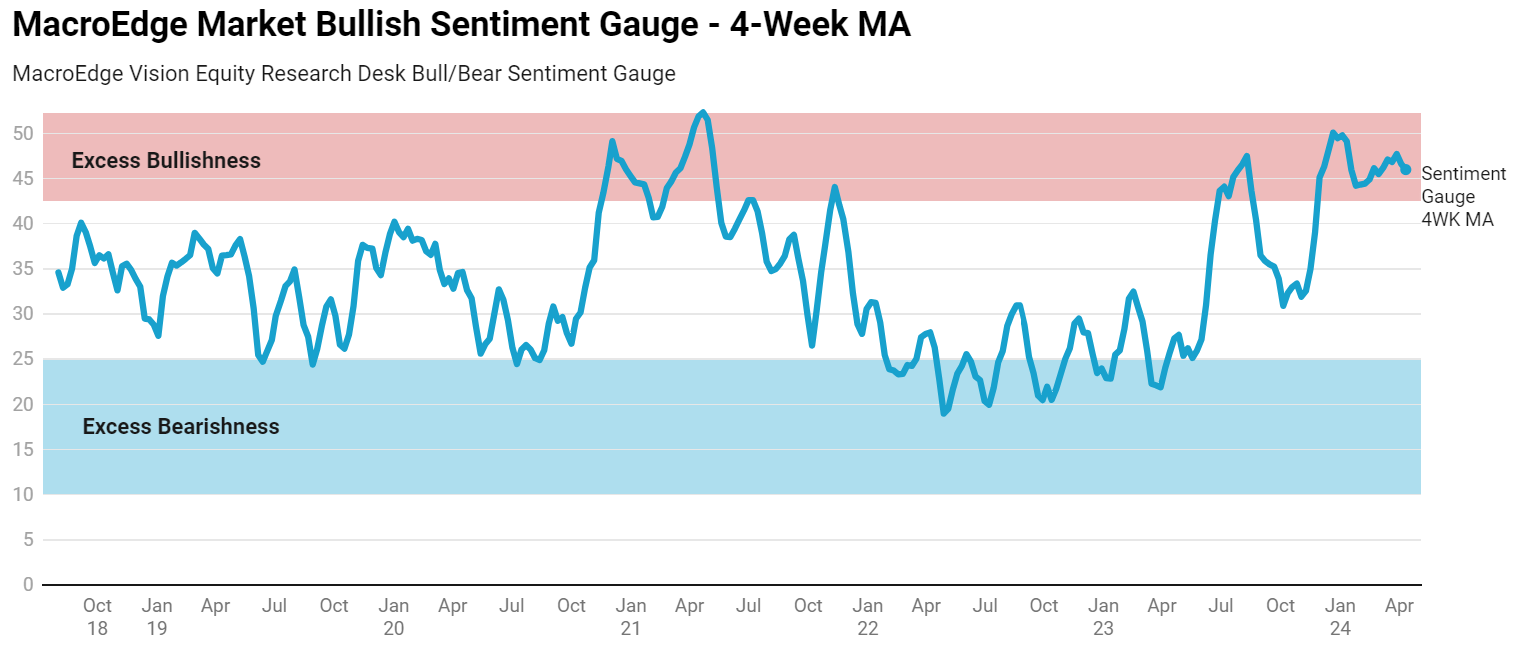

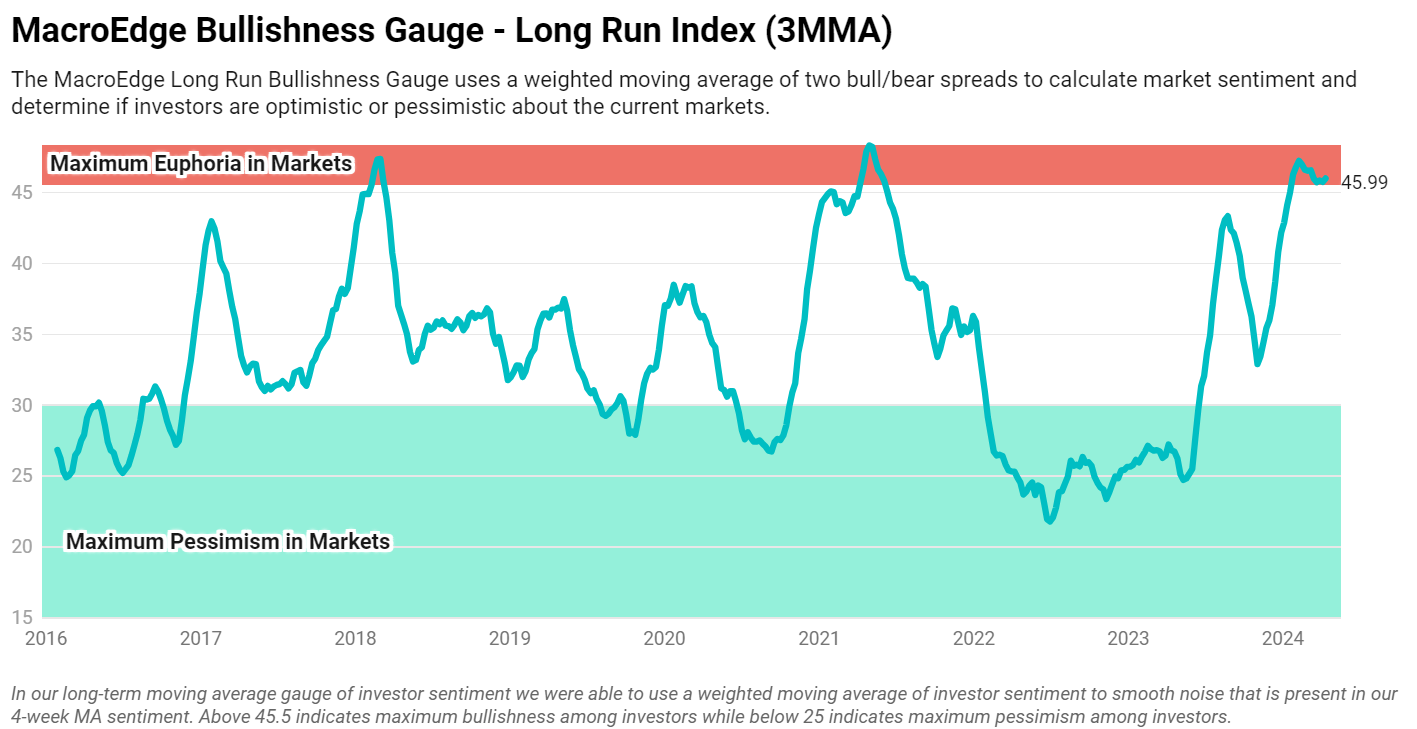

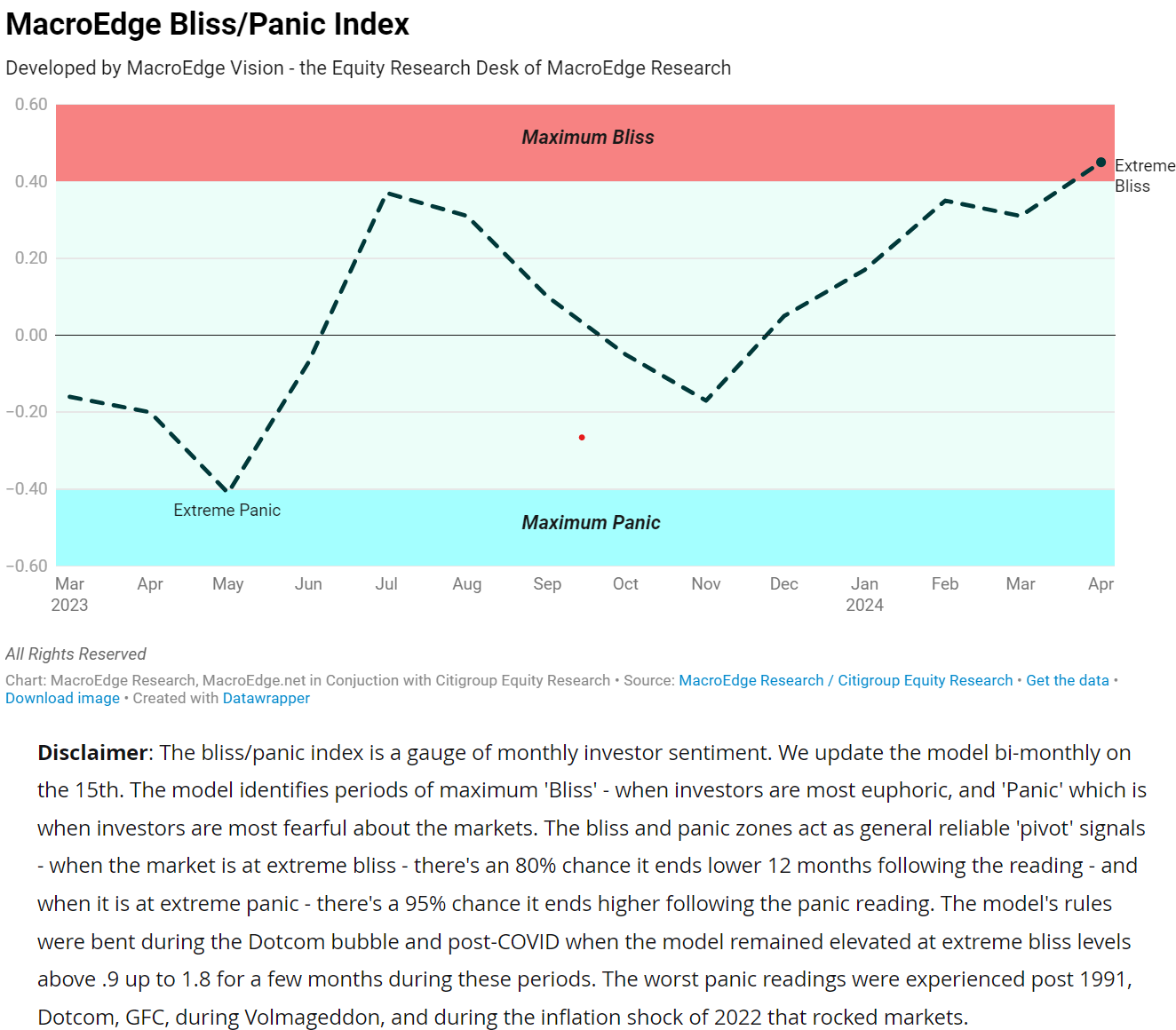

While the Wynn might be a little too classy for many, it’s where a lot of people’s heads were at coming into the week. Take a look at our four new sentiment/bullishness gauges:

(Our short-term bullishness gauge is available at: MacroEdge.net/data)

Our Bliss/Panic Index, Long-Term Bullishness Index, and Medium Term (4WK MA) indicators are now available through Vision below:

One thing I think is notable, and I track with a very smart PhD who wrote for us a very long while back, is that sentiment still seems mostly euphoric on the retail spectrum, so it’ll be interesting to see where things on our new indicators move this week… The market will of course and inevitably experience ‘bounces’ at certain points, but our new Equity Research tools provide us all with some new important market context that we can now take alongside all of our critical economic data both found in the dashboard and in our weekly Ozone reports.

A bounce will occur when sentiment on shorter time frames gets ‘panicky’, when our new indicators update that may be soon, but consolidation will likely be needed for continuation to the downside (even if it is a day/less), if this is not seen then the market is clearly leading in anticipation of broader labor/economic downturn (which is doesn’t usually do - it reacts). The statistical outlier risk our longer-run data outlook notes is something like a 1987 scenario, so all of these data points - even if outliers - warrant attention.

In the larger economic picture, the train continues to roll down the tracks on economic weakness. The Federal Reserve members have all but pivoted to lets hold as long as we need (as ECB members move forward with a likely June cut) and the most important employment data will still follow that Fed cut in my eyes even though labor continues to weaken.

The CRE picture looks very weak and utilization of the Fed’s discount window ticked up to a high of year today at ~$8.6bn, which will be yet another thing we at MacroEdge will be attention to in the coming weeks.

On the employment data and data side of things, the labor market continues to weaken. Job cuts this month are on track for a new high for our Job Cuts Tracker:

Job openings are now back at April 2021 levels, and just 16% above pre-lockdown levels. The Philadelphia Federal Reserve updated their Employment Diffusion Index today (and I smoothed the noise with a 12-mma):

Overall, such interesting times we are living in, truly…

Let’s keep an eye on all of this data as it evolves and hopefully I will see you in the Ozone for the weekend report/all of our new data updates. I better get looking at these flights to Aruba in the meantime…

Your friend,

Don

Vision Update (@SixFinance,MacroEdge Head of Research)

MacroEdge Vision Equity Research is lead by our Head of Research, Six. Access can be found by joining MacroEdge Vision, which you can now do through Substack temporarily while we prepare our Substack roll-off:

It has been a very interesting last couple weeks since CPI. Unconfirmed reports tonight that Israel just hit Iran back. This is very bad from a humanitarian standpoint. For portfolio management purposes, we bought the dip today in 2yr Treasury futures /ZT. Vision book stands at around +329bps since inception on 4/3/24.

I wanted to do a quick update tonight on market structure. Following the CPI we have seen a change in market regime. Every rip is getting distributed into and sold. Small odds of hikes are now being priced in. Net Interest Income on the big banks are all disappointing. MacroEdge job cuts tracker now shows us on track to outpace January as the largest month for cuts this year if the trend continues. Powell’s comments on Tuesday were extremely bearish and cuts are being increasingly priced out.

It seems many market participants do not realize the regime change that is occurring. While it is very important not to short in the hole here, selling rips is proving profitable at the moment. With the Steepener that has occurred, along with the drastic repricing in rate expectations versus how we begun the year with 6-7 expected cuts, I am much more interested in selling rips than I am in buying dips.

Our leveraged real estate short DRV (3x inverse real estate select sector) is now up roughly 24% since we put it on and I was considering trimming the position today but have not made any changes yet. Will have to see how the rates rally overnight plays out before making any changes.

ECB and BOE have all but confirmed June cuts, crude oil is obviously rallying again, things are moving very rapidly now. Will post any new positions through MacroEdge Vision twitter/x account tomorrow for the day only because of rapid developments, as well as in the Vision private group. Being VERY careful about shorting into the hole here, as overall bullish market structure while currently looking very bearish, is not yet broken.

Have a ton of data and will be moving a lot of the book out of cash (1-3m treasuries) into allocations this coming week. The iron is hot and it is time to strike. Don’t miss the next weekend report.

*Excuse typos