Saturday Macro Note: Strait of Hormuz & Oil Supply Update, Fracking Activity, War Impact on Aviation and Hospitality

In this Saturday Macro Note we discuss the latest on the Strait of Hormuz and oil supply updates from the Middle East region, look at the latest fracking activity data, and highlight war impacts...

Don Johnson (@DonMiami3), Chief Economist

Good Saturday evening MacroEdge Readers & Community,

Today, we are delivering another update from the West Coast. On Monday, I will be departing for a few days and making my way over to northern Nevada, and then returning to the coast for a week. Beyond that, I will be in West Texas again before returning to Florida - this intensive travel schedule continues as we continue to expand our relationships and partnerships across the country, and develop and implement solutions across our Macro Research & Transform divisions.

We’re on day 14 of the ‘short’ excursion into Iran now, and the conflict shows few signs of abating for the time being. While there’s a lot of language being thrown around, the actual truth is in the energy supply impact, which is already impacting the global economy. With about 12-15% of the global oil supply currently frozen, and with little sign of this changing for the time being, many are wondering what’s going to happen next out of the region. For the time being, the United States, Iran, and Israel all seem at an impasse from a conflict resolution, though the President today was clearly voicing his angst over the Strait of Hormuz closure. In our modeling of the situation, pushing to the end of week three or into week four of a Strait closure would start to significantly impact the global economy beyond higher fuel/fertilizer/shipping prices. An actual price shock could start to materialize - more on the level of what we saw in the 70s - and this could be exacerbated by things like a domestic fuel export ban - if we start to push into a 4th or 5th week of oil exports being frozen at the level we’re currently seeing (12-15% of global supply).

The spike in energy and food costs across the board has tipped the scales for the midterm odds, with the Republican Party now behind in the US Senate odds:

States like Texas are likely to have historically close elections this year, as turnout for the party in power is set to be very low - and this will have ramifications for the economy if we end up with partisan gridlock from 2027-2029 (taking us through the end of the second Trump term).

While that’s way in the future, we’re going to continue to focus on what’s more immediately ahead of us as oil prices are in the driver’s seat now for the global economy (and equity markets), and we’re going to dive into many of the key topics below.

This evening we’re going to dive into:

A Taste of Trident

Strait of Hormuz and Oil Supply Update

No Signs of Weekend Resolution

Impact on Aviation and Hospitality

Weekly Macro Note Preview

A question some will find themselves pondering in the next several weeks, if this situation does not resolve itself: is this 2008 all over again, or are we looking at something more like 1973? The answer is likely to be a little more nuanced than that, either way.

Not yet a MacroEdge Ozone subscriber? Upgrade through Substack and get access to all of our research, data, portfolio strategy, equity research, and much more below:

A Taste of Trident*

Building on the cutting-edge macro research, equity research, and portfolio strategy we deliver at MacroEdge, we are opening the doors to register interest in the Trident I Global Macro Fund. This boutique vehicle is engineered to capture high absolute returns by identifying structural inflection points across global FX, rates, commodities, and equities. Modeled after unconstrained mandates, the Fund moves beyond traditional benchmarks to capitalize on mispriced macro fundamentals through a disciplined, thematic process. For accredited partners looking to move from analysis to execution, Trident offers a focused path into high-conviction global themes with a rigorous emphasis on downside control and liquidity.

Complete the form below to get in touch with our team & learn more about how we’re turning real-time data into real-time strategy:

Strait of Hormuz & Oil Supply Update

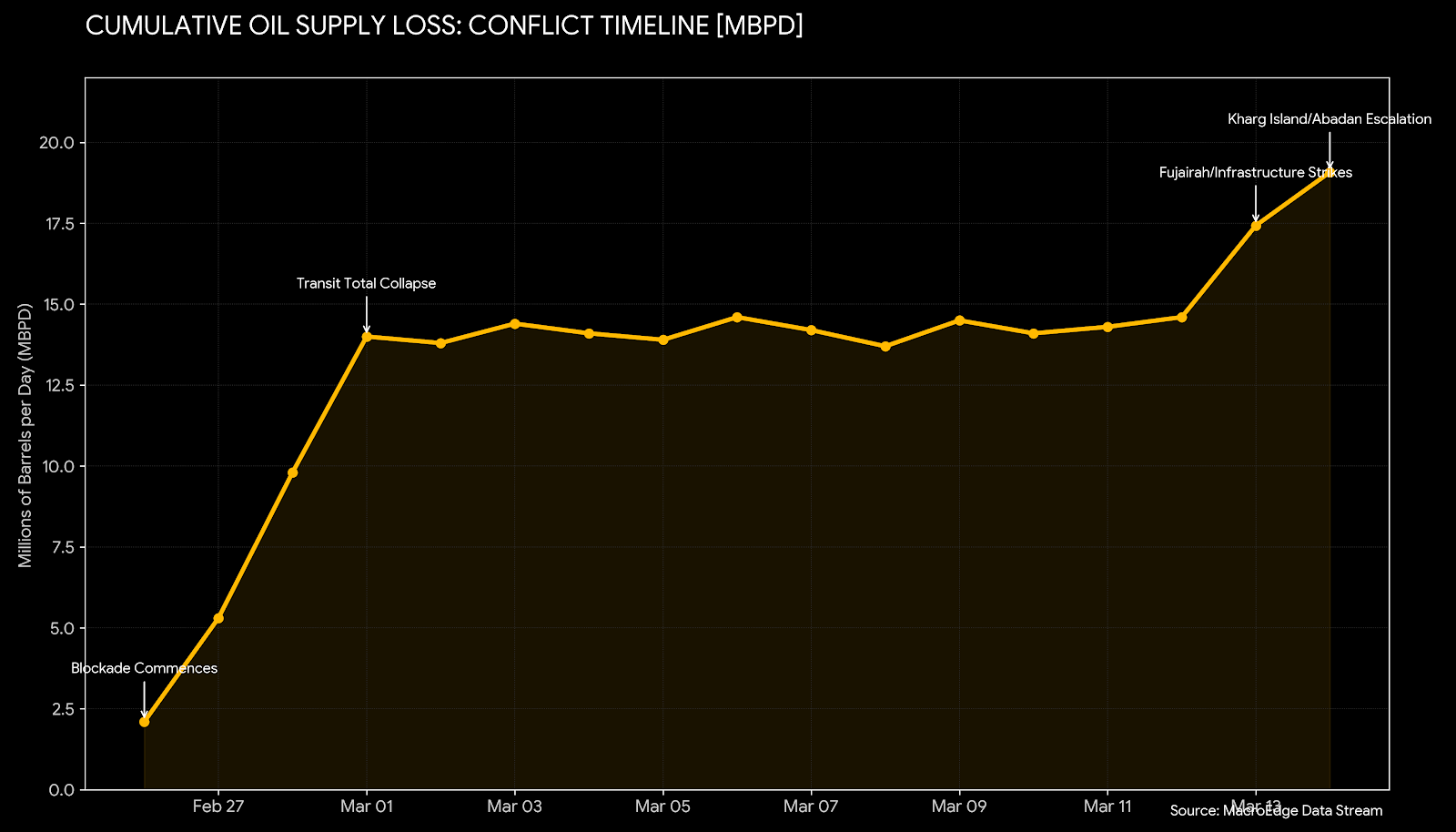

Goldman Sachs estimates that, based on current vessel flows and satellite data, flows have fallen “from about 19.5 million barrels per day to just .5 million barrels per day over the past few days. After accounting for pipelines redirecting some supply, the net disruption to Persian Gulf exports is estimated at about 17.2 million barrels per day.” No tankers crossed the Strait on March 12th, while on March 13th, it’s estimated that a single oil tanker crossed. We have a more conservative estimate on impacted supply for the time being - given the difficulties in tracking ship activity through the Strait - pegging the supply freeze at 14mpbd effective. We will likely see additional OPEC+ supply come offline over the next two weeks if the Strait closure continues - something I peg a 50/50 chance on right now if the US President shows no sign of trying to open up any broader off-ramp.

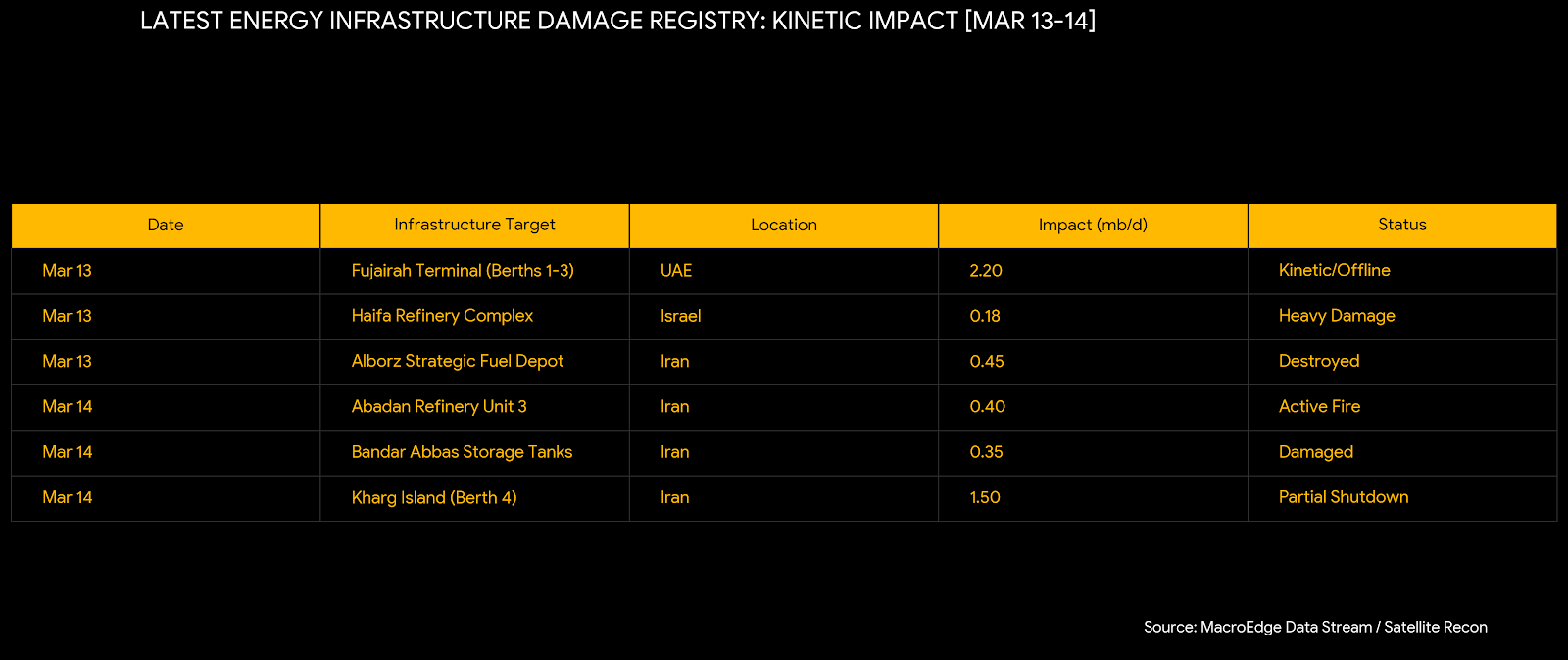

Below highlights the latest energy impacts from the weekend - significant impacts from the UAE, to Iran, and Israel. The largest impact being the UAE’s Fujairah Terminal - with ~2mbpd impacted (huge).

The ‘Goldman’ scenario highlights the 17-19mbpd outage:

(Continued below: Strait of Hormuz & Oil Supply Data/Charts, Fracking Activity Data, No Signs of Weekend Resolution, War Impact on Aviation & Hospitality)… & more with MacroEdge Ozone:

Even with flows to India and China occurring at some level, it is really not Iran that is facing the worst impact from an oil export standpoint - it’s the other GCC countries that currently can’t move any product through the Strait.

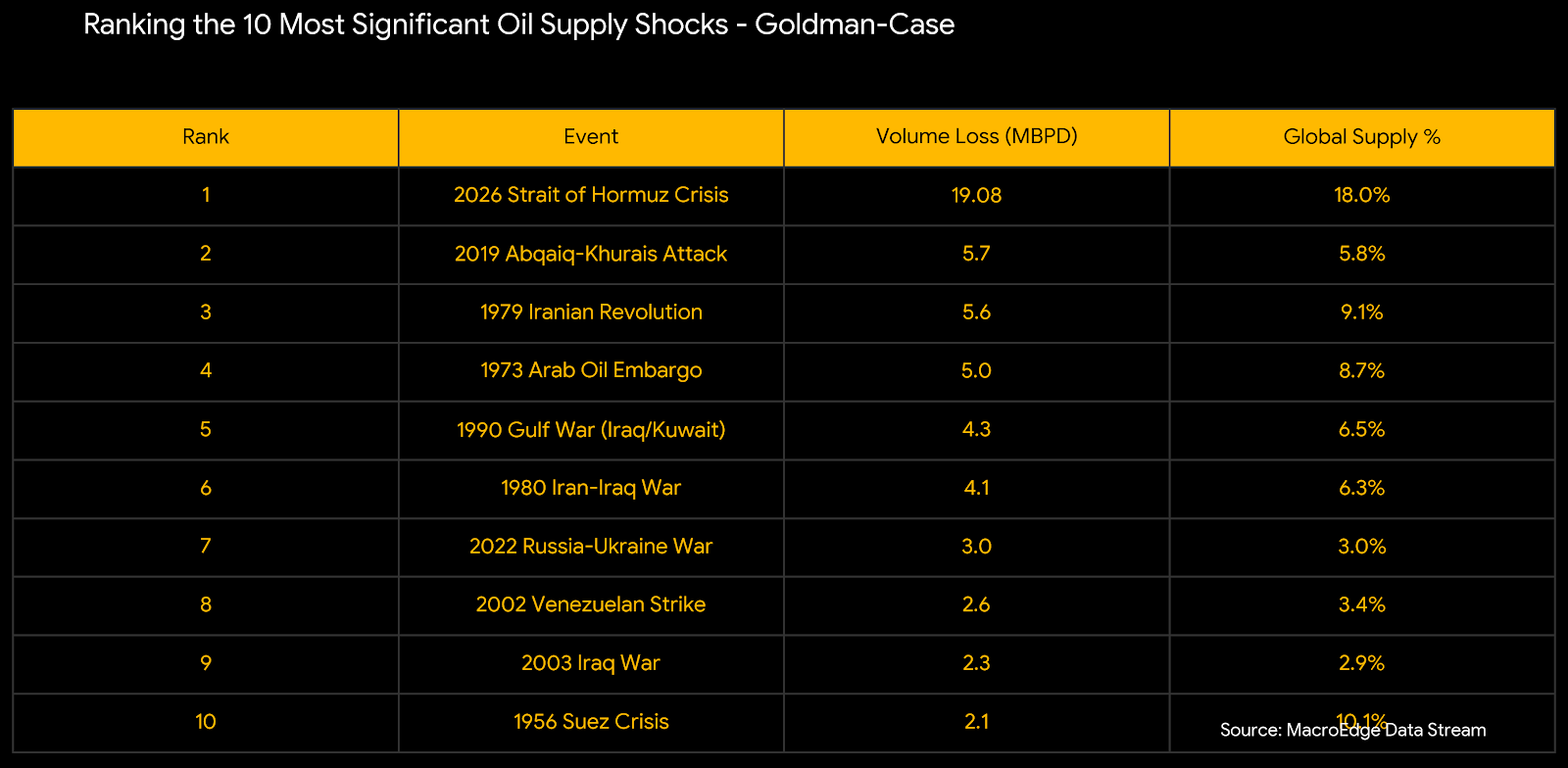

The Goldman scenario (or not, in our more conservative case) still puts this as the most significant output shock the world has ever seen:

The Australian government today noted that they were looking at just over two weeks of active fuel inventories, and east Asian countries like Japan and South Korea are going to start really feeling the pain & pressure if this situation continues through the remainder of March.

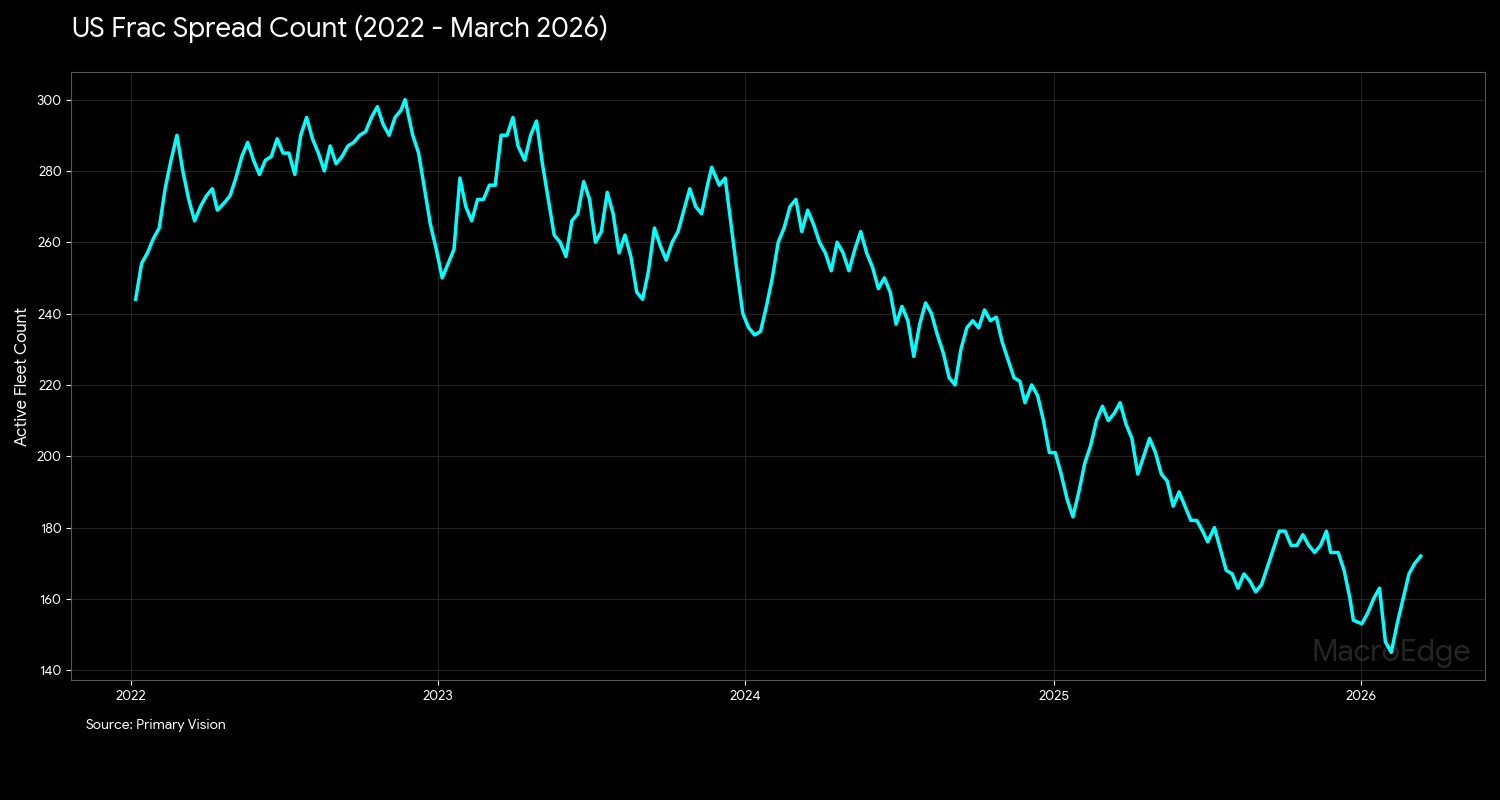

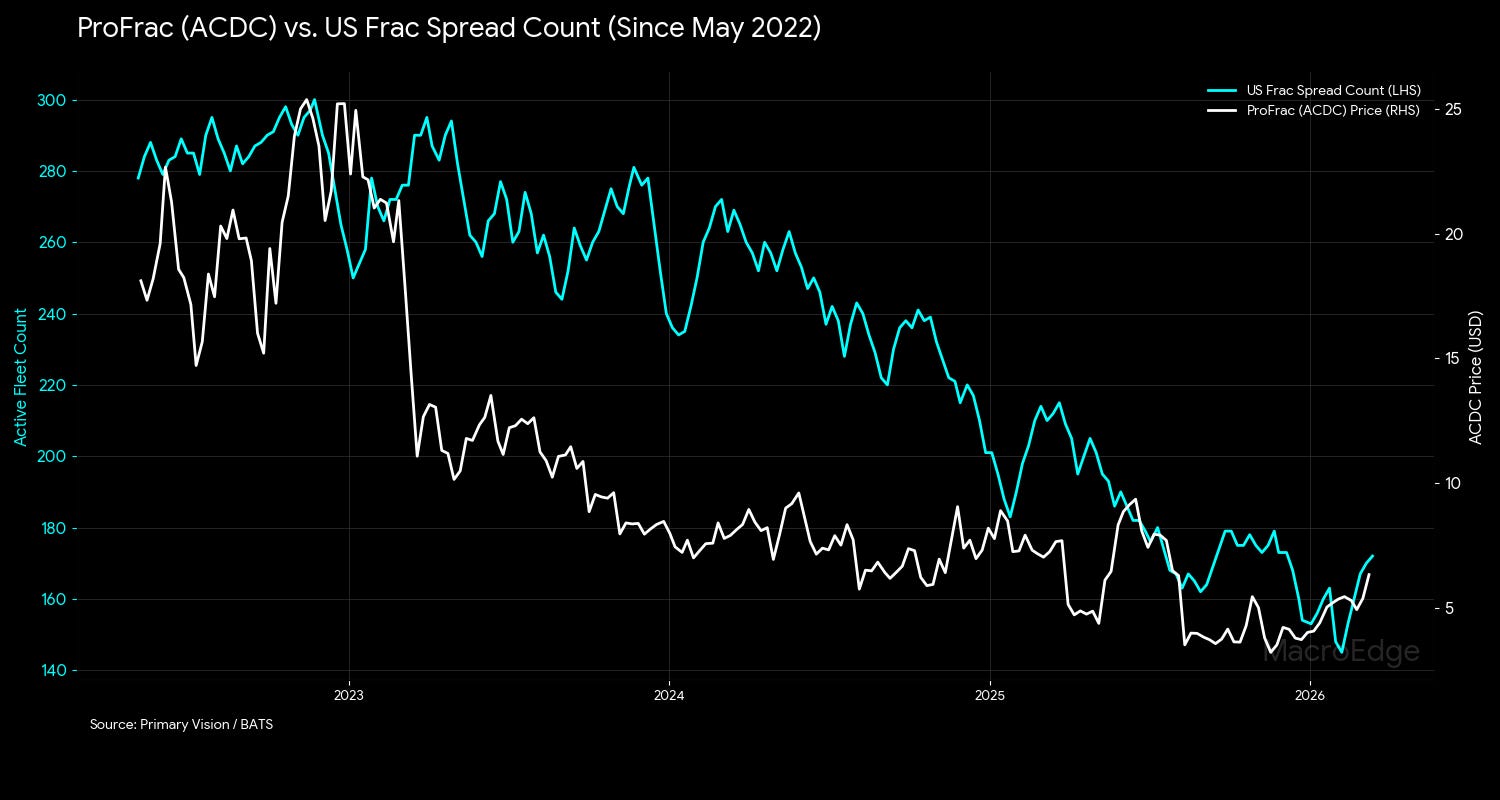

From an actual energy investment standpoint, some consolidation in price before another move higher, or a stabilization in the 80-100 WTI range would be best for the equities we’ve highlighted over the last few weeks. The higher prices stay for longer, the more likely we are to see things like frac spreads begin to finally move higher (something that they haven’t done now in years)... More on that tomorrow evening.

Frac spread count since 2022:

Fracking equities & fracking activity are closely correlated:

No Signs of Weekend Resolution

The conflict between Israel, the United States, and Iran shows almost zero sign of de-escalation, with all parties appearing to “dig in” for a sustained war of attrition. Israel has officially declared the conflict is entering a “decisive phase,” while the Iranian leadership, now under Mojtaba Khamenei, has rejected diplomatic backchannels, signaling that they will not capitulate despite the elimination of their primary military and political leadership. This hardening of positions is punctuated by the deployment of additional US Marines to the region and the expansion of Israeli target lists into northern Iranian industrial zones like Tabriz.

The tactical focus has shifted aggressively toward the systematic dismantling of high-value energy and military infrastructure. Over the past 48 hours, Israeli and US strikes have pounded the Taleghan 2 nuclear site at Parchin and multiple fuel depots in the Tehran and Alborz provinces, sending massive plumes of toxic smoke over the capital. Iran has retaliated in kind by targeting regional energy arteries, most notably striking the Fujairah oil terminal in the UAE and the Haifa refinery in Israel. The most critical flashpoint remains Kharg Island and the Strait of Hormuz; while the US has currently spared Iran’s primary oil export infrastructure, the threat of its total “obliteration” remains the final lever of escalation.

If WTI surpasses $120/bbl again - which the government will be desperate to avoid - we will begin to see global economic activity begin to shut down, and we will also likely see civil unrest start to kick off as well. The current situation paints a picture in which it could be quite likely that we see an all-time high in oil prices.

Impact on Aviation & Hospitality

The war between Israel and Iran is already having a significant impact on the hospitality and aviation sectors. For aviation, the impact is even more outsized in the short term across the spectrum, with JetA costs doubling since January, and Middle East commercial air traffic is running just 40% of its pre-war levels. The *Peace in the Middle East* work that had been done over the last ten years has largely been undone now, and we’re on the brink again of the entire region being at war - with all targets being fair game over the last two weeks. As infrastructure attacks have accelerated, the impact to air traffic globally has become more pronounced, as seen in data from FlightRadar24. While nowhere as significant as a ‘pandemic-level’ event like we saw in 2020 - a 10% drop in daily flights will have a significant impact on many airlines, and if JetA prices continue to rise (downstream of oil) - we’re going to see some airlines begin to cancel flights and cut available route supply to keep planes full and optimized in a much higher price environment. The EIA’s Gulf Jet Fuel Price Index made a sharp move last week, and JetA prices continued to move higher over the weekend. I called out on X that I spotted almost $11/gallon prices at Santa Monica Airport when clicking around the price data for the Southern California region!

The JETS ETF is down over 15% this month amid higher JetA prices and lower traffic volume:

The bearish divergence on the monthly timeframe is typically a significantly bearish development, and monthly trends take time to play out.

Impacts to individual airline equities are more pronounced, and I expect regional carriers in the United States to get punished of oil prices remain elevated. RJET - Republic Airways (down almost 25% MTD):

Skywest is experiencing a sizeable drawdown as well:

The airline picture for carriers both in the United States & abroad will be very ugly if fuel costs remain at these levels or go any higher.

Tomorrow’s Outlook

Tomorrow evening, we’ll deliver the latest after the futures open.

Food and Fertilizer Price Impacts

Oil & Prices Paid Relationship

Additional Energy Equity Research, Strategy Update

Geopolitical Update

The Technical Trainwreck

Private Credit Warning Signs

The Latest 30,000-Foot Employment Signals

*Important Disclosure: This post is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any interests in Trident I Global Macro Fund, LP. Any such offering will be made only by the Private Placement Memorandum (PPM) and Subscription Agreement. Rule 506(c) offerings are limited to Accredited Investors only. Investing in private funds involves high risk and is not suitable for all investors.

For more details, please refer to our Terms and Conditions.