Saturday Macro Note: December Employment Review, No Rate Cut, Portfolio Opportunities

In this Saturday Macro Note, we dive into our comprehensive December employment report, discuss why there's very little chance of a rate cut this month (or thru March), and more.

Good Saturday afternoon MacroEdge Readers & Community,

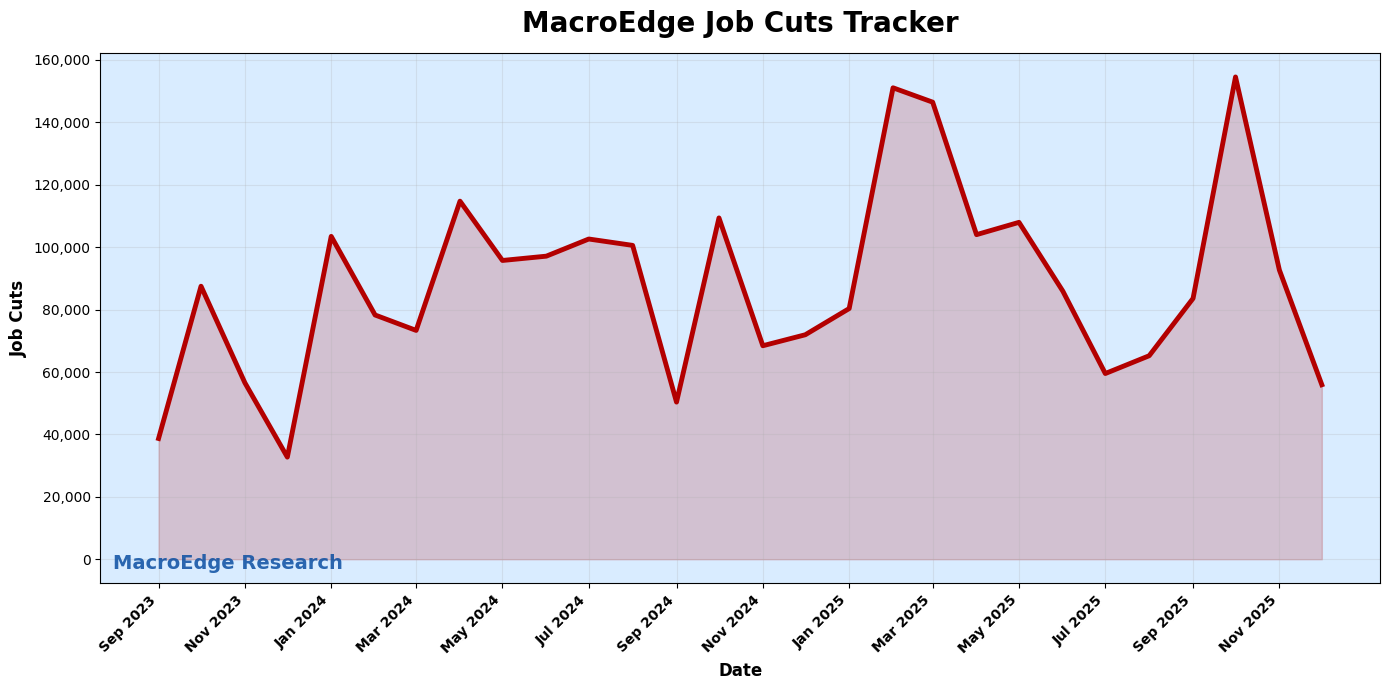

This afternoon we’re going to briefly dive into the employment trends as we wrap up & wind down focusing on 2025 data. For the most part - the report came in as we expected - with the one outlier variable being the small dip in the U3/U6 unemployment rates. The labor force participation rate also declined further. Notably, we’ve now had two consecutive months of net hiring across the government employment base - and foreign-born workers were responsible for all of the net job gains we saw in December - while native-born workers saw a steep drop in their total employment level in the household survey. Following up on the private sector data from December - the report was mostly in alignment with that data - and the one real bright spot in the labor data for the month was the steep drop in job cuts.

Subscribe to MacroEdge Ozone thru Substack -

Job cuts have continued to dip lower off of their October high - which was a significant month - and 2025 was still a very substantial year for job cuts, registering as the highest non-recessionary job cuts year since 2003.

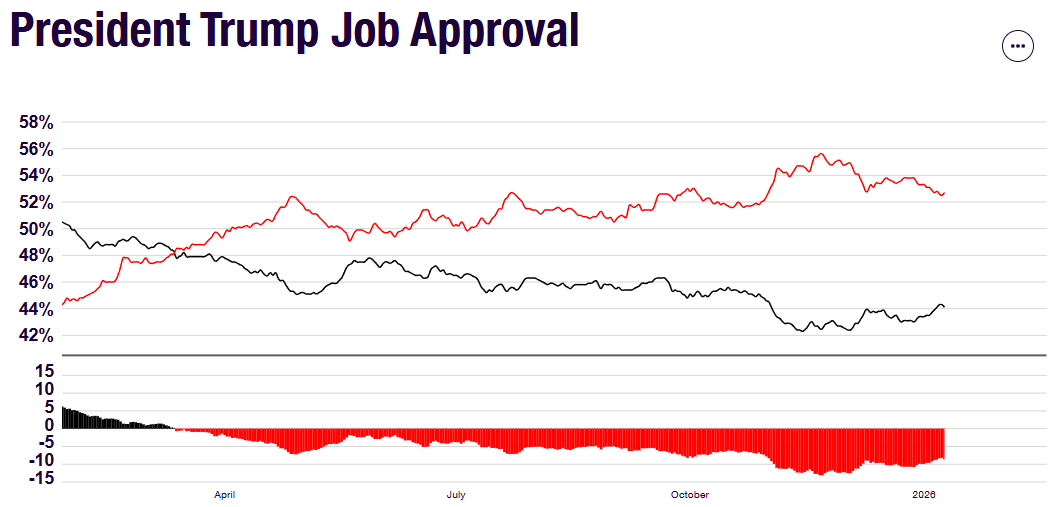

The Presidential approval rating spread has also narrowed from the October/November period - when job cuts were at their record high levels (government shutdown & corporate layoffs).

We saw a continued uptick in the UMich Consumer Confidence indices yesterday - which are recovering off of record low levels. All of this is occurring amidst a stock market that seemingly has priced out any and all macro/geopolitical risk for the time being. More on that tomorrow, that aligns with our ‘Year of Differentiation’ theme for the 2026 year.

Tomorrow evening - we’ll discuss more from a portfolio opportunity standpoint - looking more into the trends in South America - discuss macro data ahead - and talk about continued geopolitical volatility that’s been observed from across the globe (some of which is now even being seen in the United States). The Administration looks set to continue pushing forward with a major global realignment this midterm year - with Greenland and Cuba seemingly next (along with Iran) in the crosshairs. There are also interesting discussions taking place surrounding Mexico & the cartels - and it’s a non-zero chance that the US strikes cartels within Mexico over the next several months.

For tomorrow: housing data review/preview, portfolio opportunities - South America & more, macro data ahead, geopolitical volatility, Fed balance sheet expansion, Yen, Trump midterm shifts, & more.

December Employment Review - Mostly Soft, Again

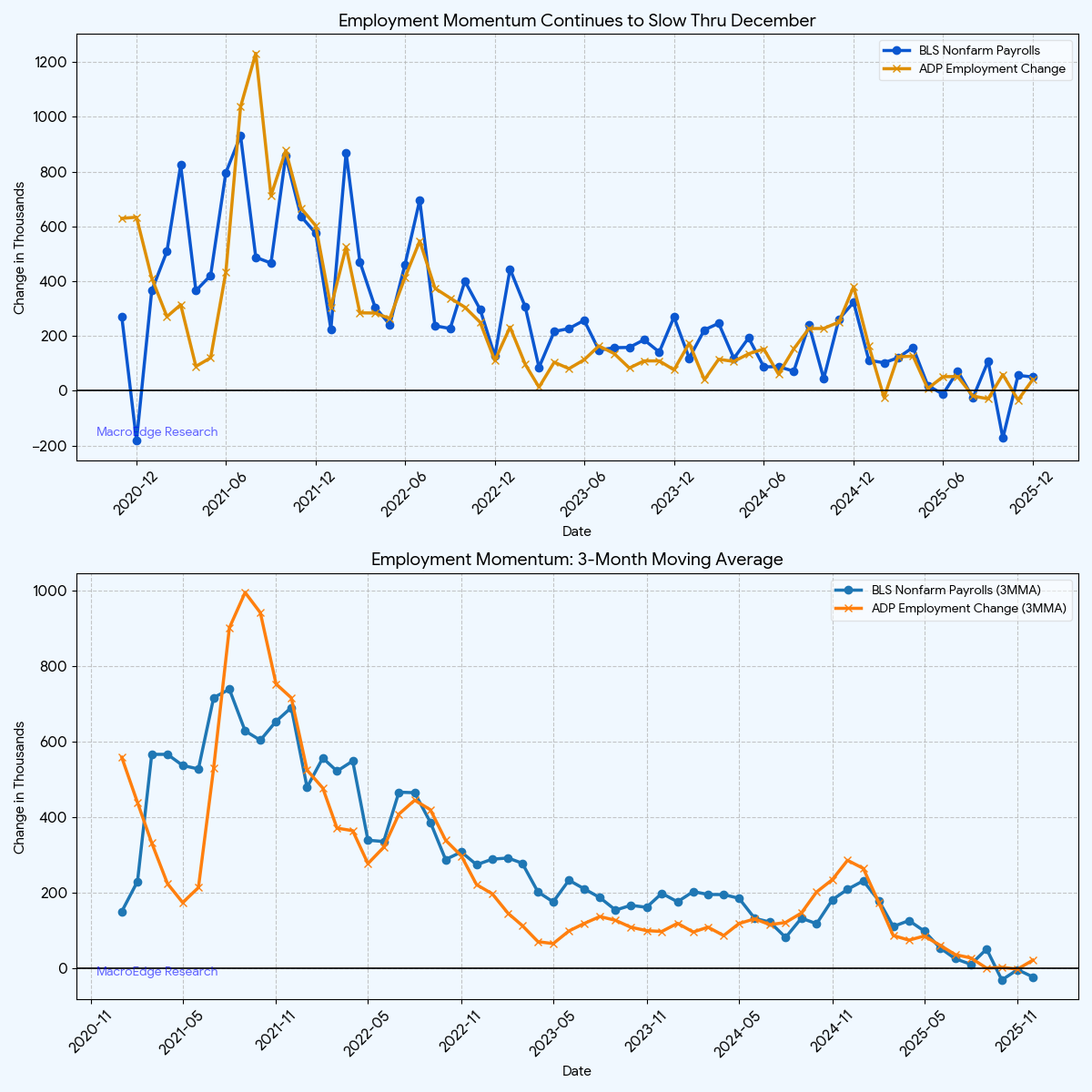

Nonfarm & ADP momentum continue to slow →

With these final figures - total payroll employment for 2025 (including revisions) was just +584,000 - which is the weakest hiring rate outside of recession since 2003 (similarly to job cuts being their highest since 2003 outside of recession…).

continue reading below with MacroEdge Ozone - Comprehensive December Employment Report (cont.), No Rate Cut for January, Portfolio Opportunities…

subscribe below…

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.