Saturday Macro Note: Bombs Away, Energy Update, Data Center Layoffs & AI Update - for February

In this Saturday Macro Note - we talk about the explosion in geopolitical tensions in the Middle East, highlight the latest potential impacts for oil & gas, discuss data center layoffs, AI, and more

Don Johnson (@DonMiami3), Chief Economist

Good Saturday afternoon MacroEdge Readers & Community,

Today we’re seeing some realized geopolitical volatility in the Middle East. This morning, the US and Israel launched preemptive strikes against the Iranian regime, and Iran responded with missile attacks across much of the Middle East. The biggest impacts are the obvious potential impacts on the Strait of Hormuz - though an extended closure still remains on the furthest of the right tail in terms of risks for oil & gasoline prices. The President knows that an oil price spike will be very negatively received by consumers, and I consider prices at the pump to be top 3 in terms of what people interpret as *inflation* since gas prices directly pinch the already tight consumer budget in the US. The personal savings rates a % of disposable income is currently at one of its lowest recorded levels, and consumers are pinched by elevated inflation.

Update as of 3pm EST or so… There are mixed reports that the Iranian Supreme Leader was killed, right now - these reports from all sides are unconfirmed, and the US Envoy to Israel said that the US would continue to engage Iranian leadership without any further color. The most bullish scenario for crude in the short term would be a situation in which the regime is toppled without any immediate replacement, which could cause things like the Strait of Hormuz to close or be mined by whatever entity fills the potential power vacuum. For the time being, without a boots on the ground approach (which there are likely some from intelligence agencies), it will be quite difficult to remove a dug in regime.

On top of the conflict and its short-term implications on energy markets, we are going to briefly cover the data center & AI update for February below. The most notable developments came with the announcement of a deal between OpenAI and the Department of War, the escalation in postponements and cancellations across the board for data centers, and new investments into OpenAI to the tune of tens of billions from various firms. Equities have largely stopped reacting positively when firms are investing into OpenAI, and the Pentagon announcement (I think) is sort of foaming the runway for broader bailouts for an industry that has no moat to profitability in its current form.

Bombs Away

Timeline of Events: February 28, 2026

Launch of “Operation Epic Fury”: In the early morning hours, the U.S. and Israel initiated a massive joint strike campaign. Operationally known as Operation Epic Fury (U.S.) and Operation Roaring Lion (Israel), the assault targeted IRGC command centers, air defense networks, and nuclear-related infrastructure across Tehran, Isfahan, and other major cities.

Decapitation Strikes on Leadership: A primary focus of the first wave was the “decapitation” of Iranian leadership. Israeli Prime Minister Benjamin Netanyahu confirmed that strikes successfully hit the compound of Supreme Leader Ayatollah Ali Khamenei. Netanyahu has since stated there are “growing signs” that Khamenei was killed in the attack, though Iranian officials claim he is still alive.

Trump’s Call for Regime Change: President Donald Trump announced the launch of “major combat operations” via a video statement on Truth Social. He explicitly framed the mission as a “regime disruption” campaign and urged the Iranian people to “seize control of your destiny” by rising up against the Islamic leadership.

Massive Regional Retaliation: Within hours, Iran launched an “immediate” counterattack. Hundreds of ballistic missiles and drones were fired toward Israel and U.S. military bases in the Persian Gulf, with reported impacts in Bahrain (U.S. 5th Fleet HQ), Qatar (Al Udeid), Kuwait, and the United Arab Emirates.

Rising Civilian and Military Toll: Preliminary reports from the Iranian Red Crescent cite over 201 fatalities and 700+ injuries within the first 12 hours of the campaign. This includes reports of a high-casualty strike on a girls’ school in southern Iran, while Israel has closed its border crossings and raised its domestic alert level to the highest possible state.

Strikes are resuming from the Iranian side as of about 4pm EST - and the ‘spray and pray’ approach appears to be a strategy designed to wear down air defense systems across the Middle East. There are many different opinions on the matter, but if the Iranian regime survives through a heavy Sunday campaign, things may get more volatile and complicated over the next several weeks. The scale and scope of US involvement appears to be much larger than last year’s spat, and there are a tremendous number of resources on the ground in the Middle East (and still currently in transit to the region).

Energy Update / Portfolio Strategy Update

I expect much of our energy basket to perform strongly this week - and am monitoring the open on Monday. We’ve written about oil and gas opportunities extensively over the last two weeks, and some of the benefits will be reaped this week.

(Continued below: Oil & Gas update, portfolio strategy note, data center and AI update + data center layoffs, Weekly Macro Note overview for tomorrow)…

Subscribe to MacroEdge Ozone below for one week access to all of our data, insights, strategy, research, and more.

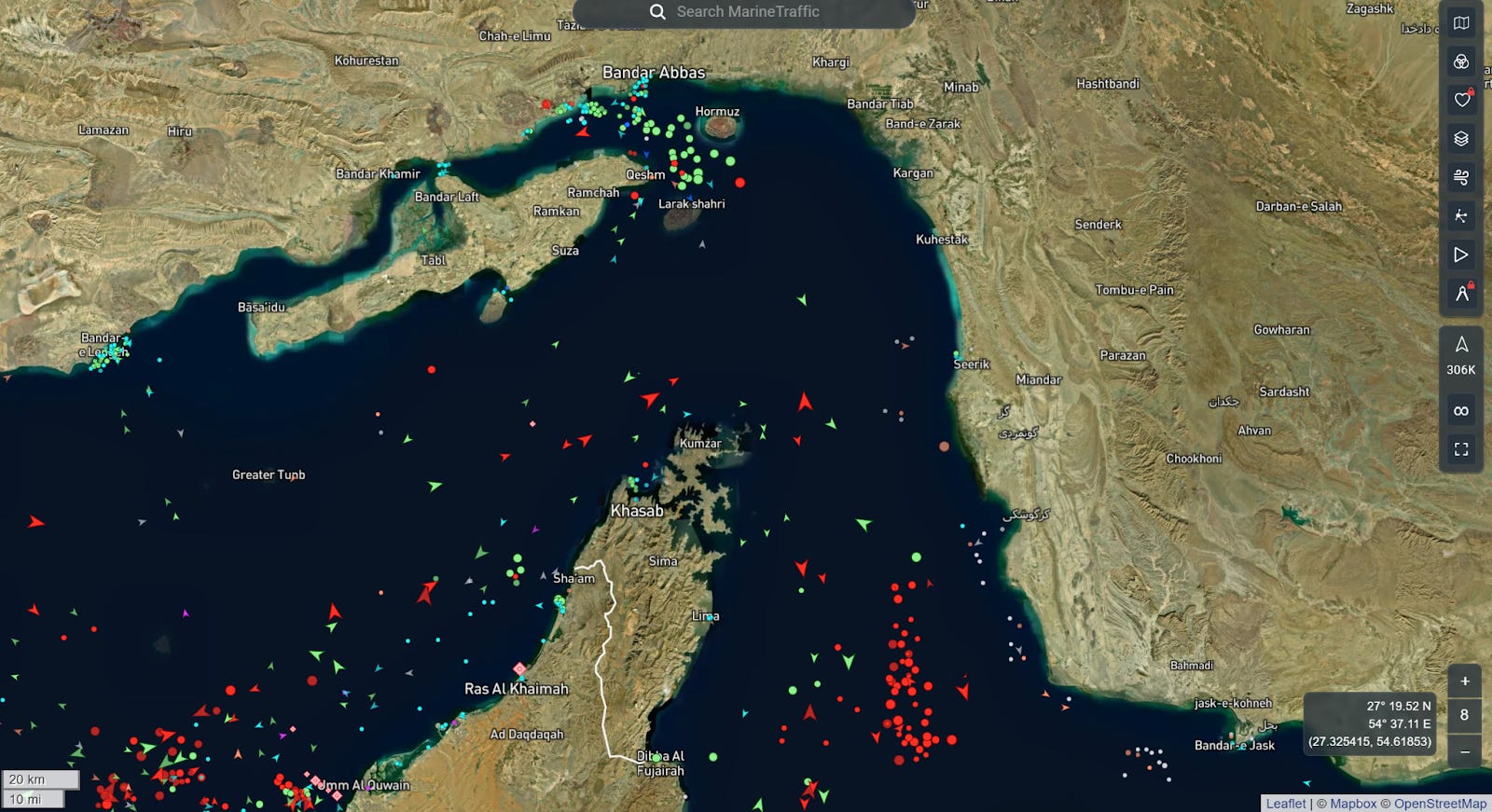

Traffic in the Strait of Hormuz has reduced to a near standstill, but is not completely shut. Threats from the Iranian Revolutionary Guard Corps to boats on the Strait haven’t been backed by anything yet, and I expect a Strait closure is a last resort measure Iran could use as a ‘panic button’ per se. (map below as of 4:36pm EST - MarineTraffic.com)

Weekend Wall Street, which offers a weekend crude futures contract, is up about 6% of the time of this writing, and the entire situation looks constructive for a gap up on Monday if tensions do not resolve over the course of the weekend. This gain is about half of what it was this morning, as traffic appears to be passing through the Strait, even with missile fire and airstrikes continuing.

Data Center & AI Update

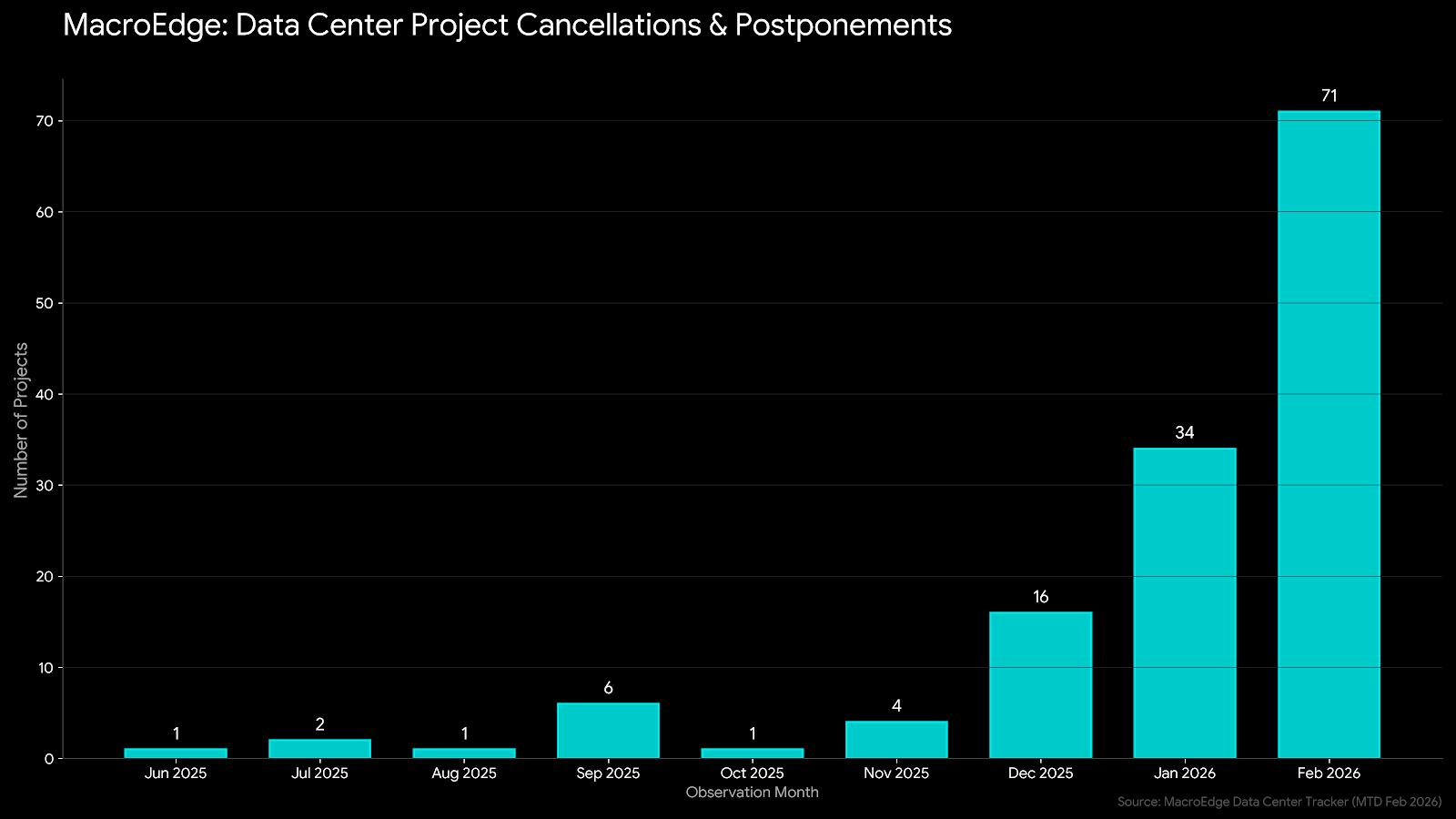

An expected 30 to 50% of large data center projects this year are slated to be delayed/postponed due to a combination of factors, including problems servicing them on the grid, water issues, and community opposition. The mounting ‘black swan’ risk for the sector is materializing to a degree, and this puts pressure on the whole economic growth narrative from AI we’ve seen over the last couple of years. Without such an extensive project pipeline (which is likely to peak next year from an active build standpoint) - though I expect it could peak by Q3 or Q4 of this year, GDP and other growth measures that have been inflated by the data center buildout are at risk.

As political pressure mounts on the data center buildout, I expect we will see developers get more desperate in how they attempt to ram their projects through. While some are now just being quietly cancelled, others are not - like we saw in San Marcos, TX, where there was over 24 hours of public hearings on the vote to torpedo construction of a >$1bn facility. A lot of municipalities are waking up to the reality that the provided tax credits and incentives for construction do not beat the increase in rents, electricity costs, water risks, and

Major developments for February:

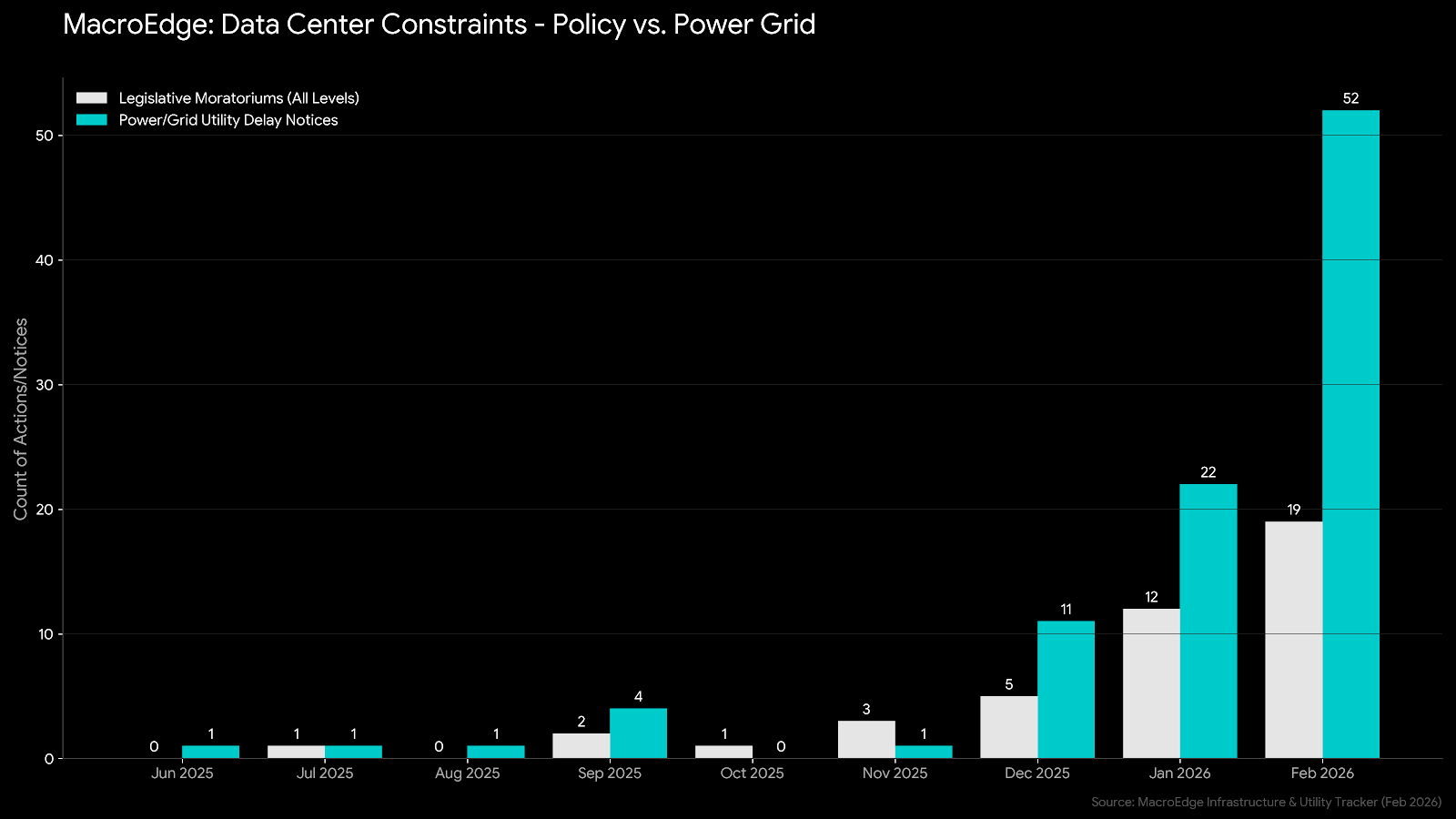

The GRID Act (Feb 11): This federal legislation created immediate financing uncertainty by proposing that data centers, not residential ratepayers, bear the full brunt of grid upgrade costs.

Sightline Climate Report (Feb 24): This widely circulated report confirmed that 30% to 50% of the 2026 data center pipeline is currently “un-powerable” under existing utility constraints.

Local Policy Shifts: February saw a coordinated surge in local “pause” votes across Minnesota, Georgia, and Colorado, suggesting that municipal opposition has moved from a fringe issue to a standard policy tool.

Tracked project cancellations and postponements in February jumped to 71, and the significant spike in cancellations will likely continue. I expect this to trend at about 70-100 a month for the remainder of the year, which aligns with the 30-50% projection of projects that will likely be cancelled or postponed this year.

Policy Problems (and Power Grid Connection issues) are also surging:

For AIS (US AI ETF), there is a significant negative divergence on the daily technical chart:

There is also the potential for one on the weekly chart:

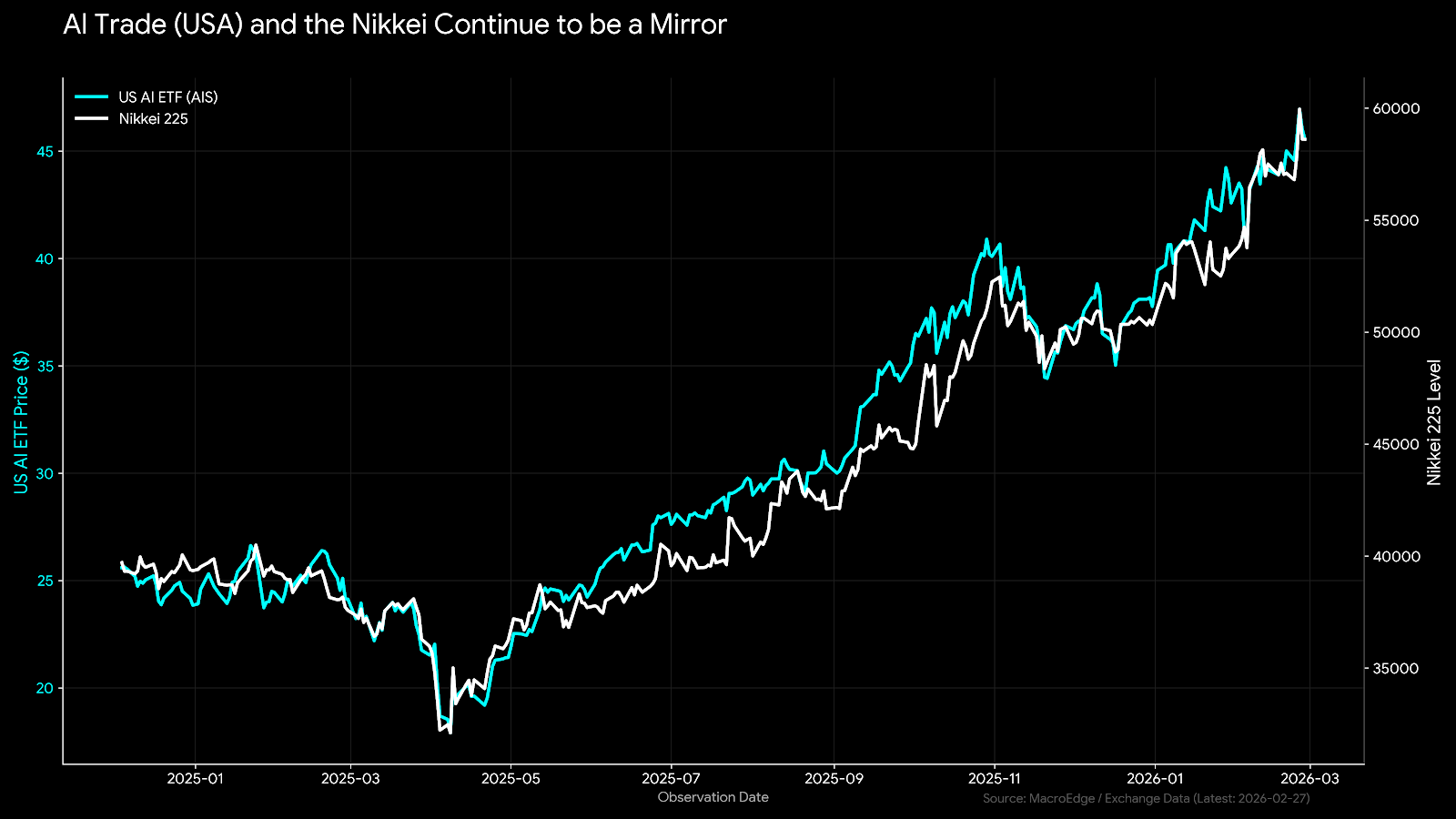

The AI trade and the Japanese bubble (N225) continue to run an almost 1:1 relationship:

Some signs of data center troubles… Data center layoffs leave workers ‘stunned’ in Racine County:

Diving into the Weekly Macro Note —>

Geopolitical Update

Friday PPI Report Rundown

Macro Week Ahead

Portfolio Strategy Update

Global Bubble Gauges

Credit Spread Review

& More

Stay tuned for a broader dive tomorrow across the board.

For more details, please refer to our Terms and Conditions.