Redeye Macro Note: War Update, Oil Surge Continues, Energy Equity Opportunities, Natural Gas Note, NFP 'Crashout' Review, What's Next?

In this Redeye Macro Note - we dive into the latest on the Iran conflict, talk about the continued surge in oil prices, highlight energy equity opportunities, discuss natural gas, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Friday Evening MacroEdge Readers & Community,

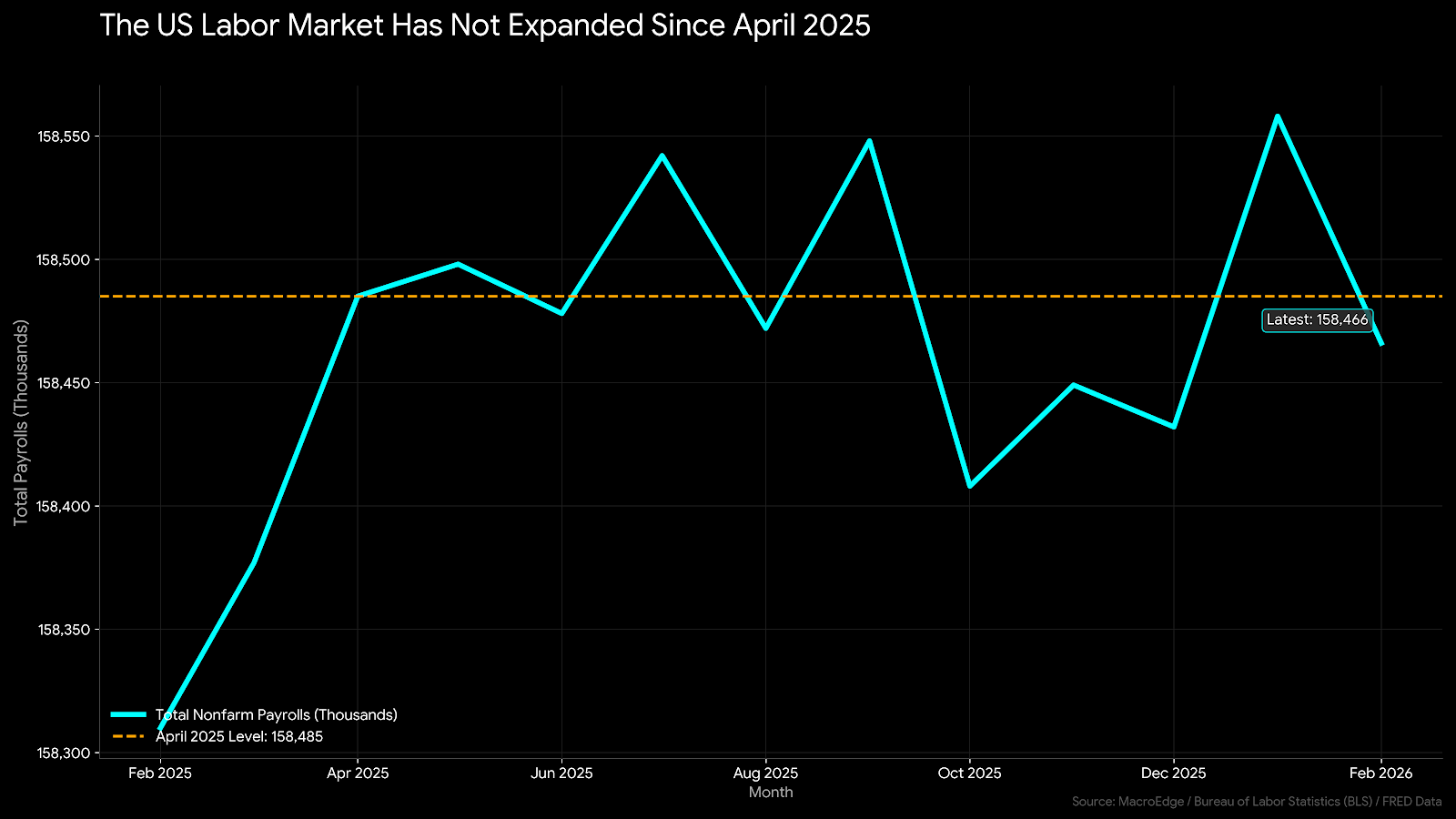

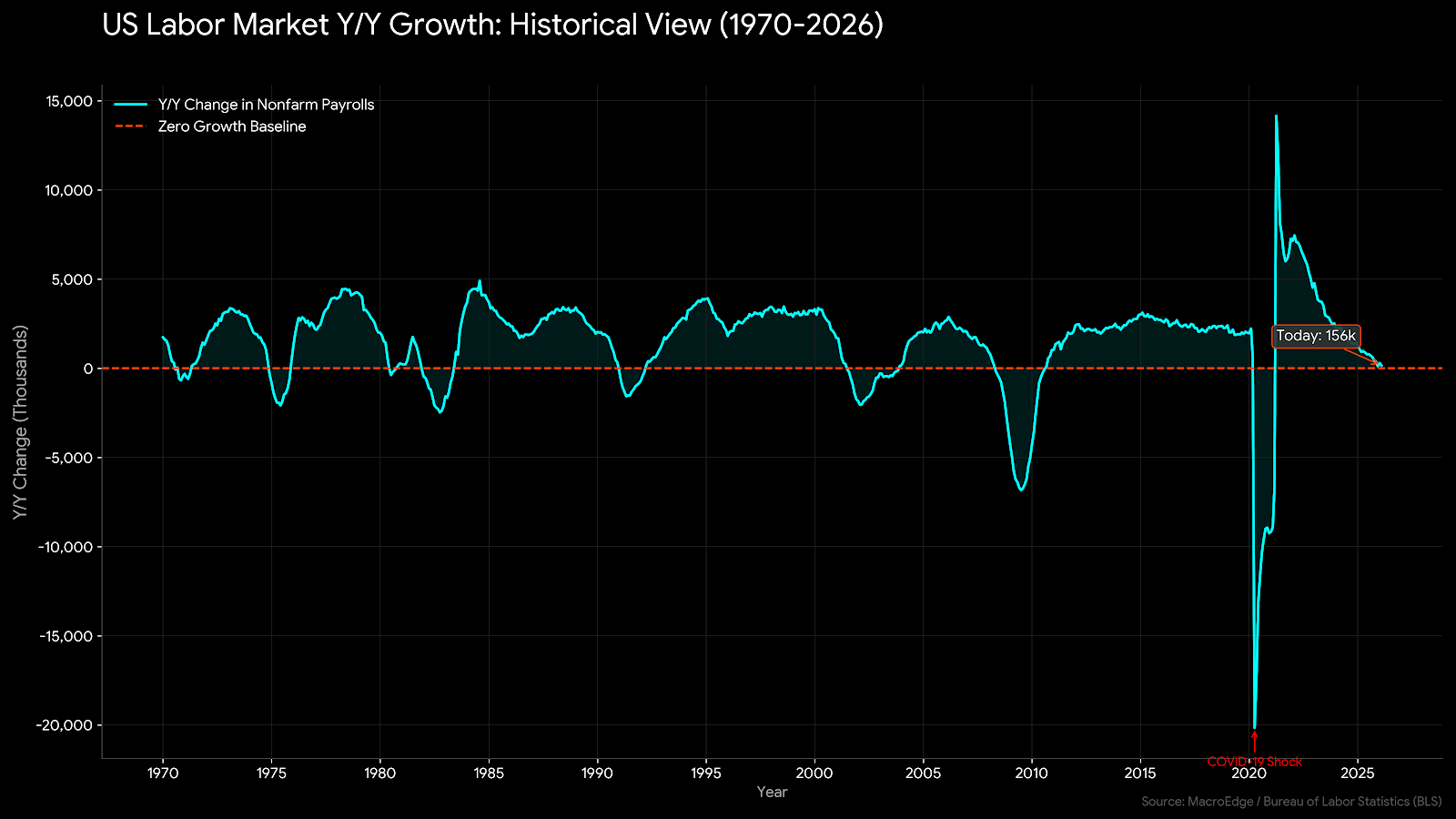

This weekend, we’ll have a packed batch of updates as we continue to see evolutions on the geopolitical and economic front. In the US today, we got some of our worst employment data since the pandemic, with headline payrolls falling at a rate of 92,000. Unemployment ticked back up to 4.4% - and most categories of employment displayed losses on a seasonally-adjusted basis. The continued trend of massive revisions continues unabated, and is something we should be concerned about, as data quality remains highly questionable at best.

On the geopolitical front, we’re going to discuss any last minute chances for an ‘off-ramp’ which is looking increasingly unlikely as both sides dig into the conflict. While we will likely see Saudi Arabia and other major OPEC players ramp up their opposition to the war, there are now many players involved in this conflict hoping for different outcomes. The dispatch of a third carrier and rumors of deployment preparations for troops does not give me confidence that we are going to steer away from a deeper involvement in the region. If anything, the Administration is running out of time with how midterms are currently projected to play out, as economic unfavorability remains at its lowest levels on record.

Upgrade to Ozone today →

The geopolitical front transitions us right into the energy front - and we saw the largest single-week gain for oil prices since 1982 this week. This outsized move reflects the supply shock markets are experiencing, and there’s still opportunity even with this massively outsized move on a week over week basis. While short-term technicals are indeed at ‘overbought’ or extreme levels, the largest moves (like today) are oftentimes made from the most overbought locations. As noted above, the Administration is running against a shot clock to get things opening back up from an energy standpoint, or the risk is indeed substantially higher than where we’re at now. Retail gasoline prices are up anywhere from 40 cents - $1 in various cities, and diesel prices are up even more. Airline equities - as we pointed out about a month ago - are seeing downside pressure as their input costs surge and eat into margins. While we’re not yet at the point of no return from an oil & gas standpoint, we are now watching the clock closely - and I would consider us to be higher on our right tail risk matrix outlined in the first War Note from earlier in the week.

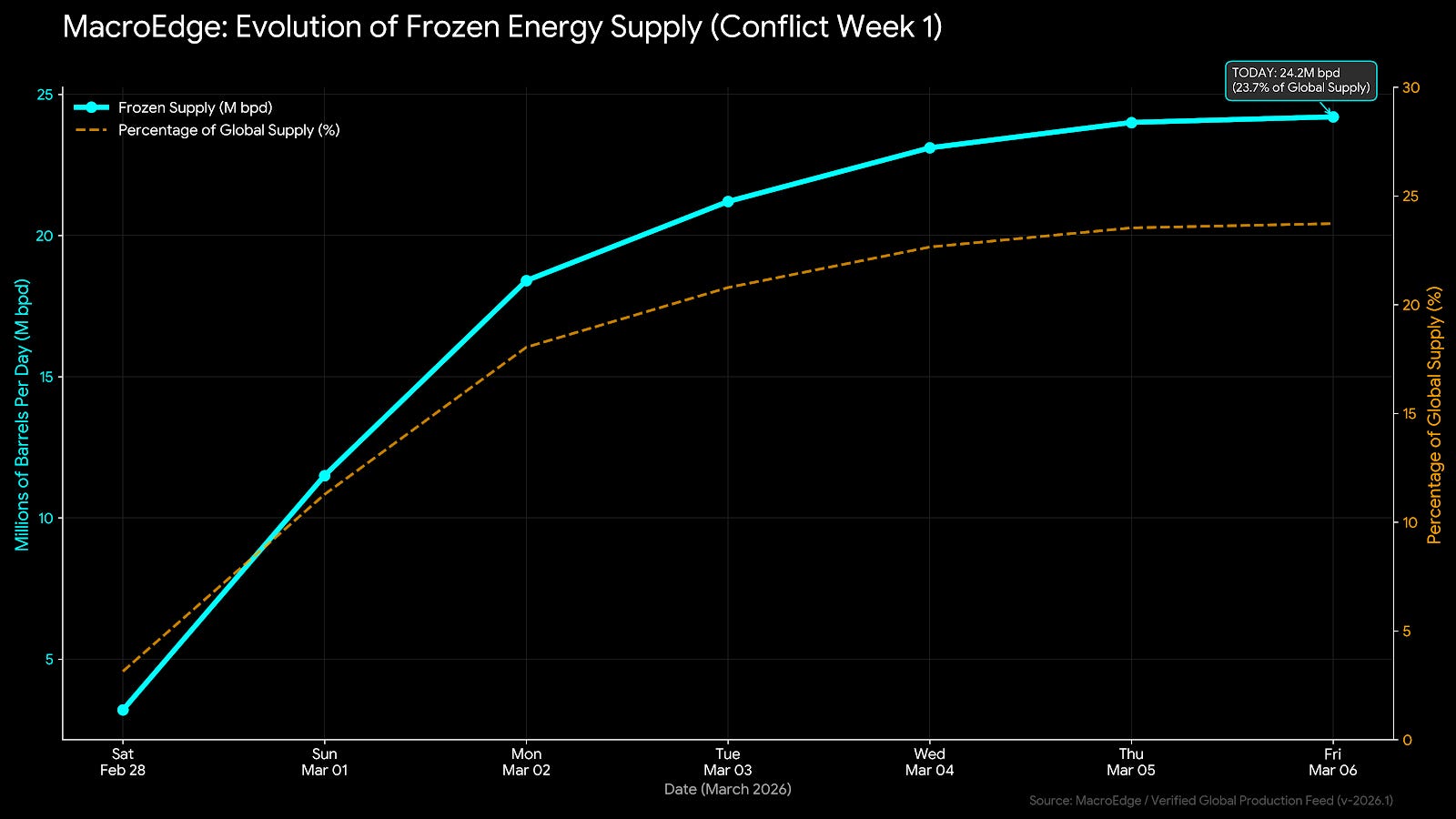

Evolution of Frozen Energy Supply (Week 1 of the War):

~24.2M bpd offline, 23.7% of global supply currently impacted. If we expand into a broader ground campaign, this may remain at/around these levels or potentially tick higher if Iran begins broader energy infrastructure attacks in the region.

Today, markets were jittered by very stagflationary data, and stagflation is something that the Federal Reserve has a nearly impossible task of dealing with, given our current debt levels and rate of money printing. Add war into the mix on a much broader scale, and we could certainly be seeing the conditions materialize. As odd as it might sound for the time being, without any off-ramp becoming visible for the time being, this Administration is once again giving me the same ‘empty stomach’ feeling from the late February & early March pandemic-era press conferences… I sure hope to be wrong in this case, but again, my goal is to help provide the information and ideas from an objective and positioning perspective - though color may be added as well as I often do on X.

I look forward to expanding on our discussion this week and highlighting opportunities as this whole conflict evolves.

Not yet a MacroEdge Ozone member? Our entire Ozone ecosystem is now on Substack - upgrade to paid below, and try Ozone for seven days, and stay for a lifetime. With access, you will get all of our research, data, reports, equity strategy, and so much more:

Community Building & Discussion

In the interest of community building and intellectual discussions about market opportunities - especially in energy - I continue to take a community building approach this year to our network across our different social media platforms. We’re always looking for new industry connections and ways to connect. If you want to chat about energy opportunities or broader market opportunities with the current geopolitical tailwinds, fill out our contact form below. We’re assembling an opportunity-seeking group of thought leaders and I look forward to the discussions.

Feel free to shoot us a DM on X as well @MacroEdgeRes

War Update

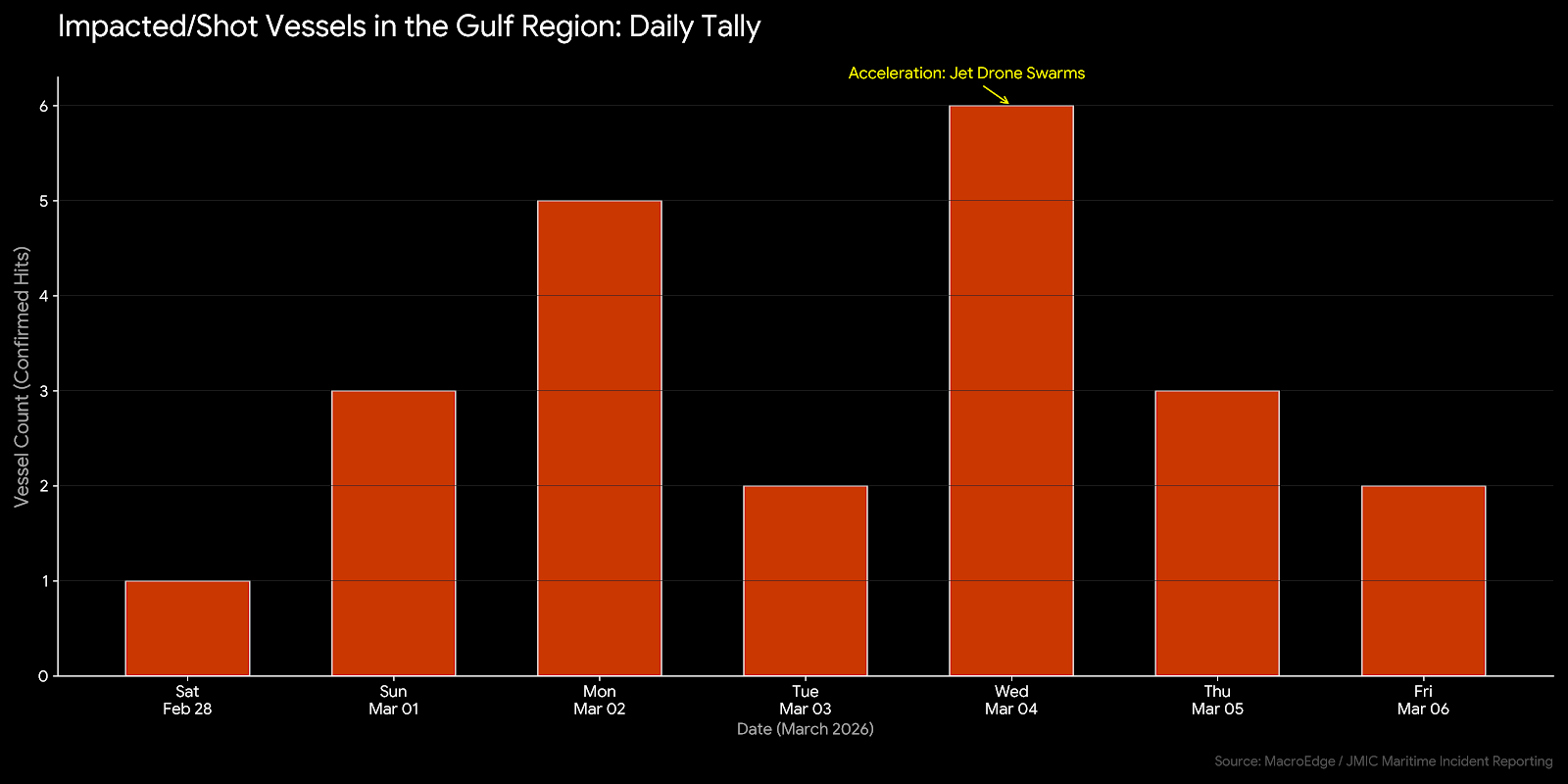

1. Iran Accelerates Jet Drone Deployment

Iranian drone tactics have shifted from harassment to high-speed strikes. The first confirmed mass use of the Mohajer-10B Jet Drone occurred today against naval targets. These UAVs travel at roughly 450 mph, making them significantly harder to intercept than previous propeller-driven models. This move represents a concerted effort to overwhelm modern missile defense systems through speed and volume.

2. Trump Eyes Ground Campaign and Rice Consultation

In a notable policy shift, President Trump has reportedly expressed interest in a limited ground campaign to secure the Strait of Hormuz. Adding significant weight to this development, Condoleezza Rice was brought to the White House today for a meeting. Her involvement suggests the administration may be seeking the institutional backing required for a major military escalation in the region.

3. The Ground Campaign Trap

Military analysts warn that the US could be walking into a massive strategic trap. A ground campaign in the mountainous and asymmetrical coastal regions of Iran would likely lead to a logistical quagmire. This type of commitment risks a “forever war” that drains the US Treasury at a time when energy-driven inflation is already hitting record highs. Iran’s current defense posture is specifically designed to bleed a landing force. In addition to this, a third carrier strike group is joining the two currently in the Middle East, and rumors online are circulating that the US has begun activating troops for combat.

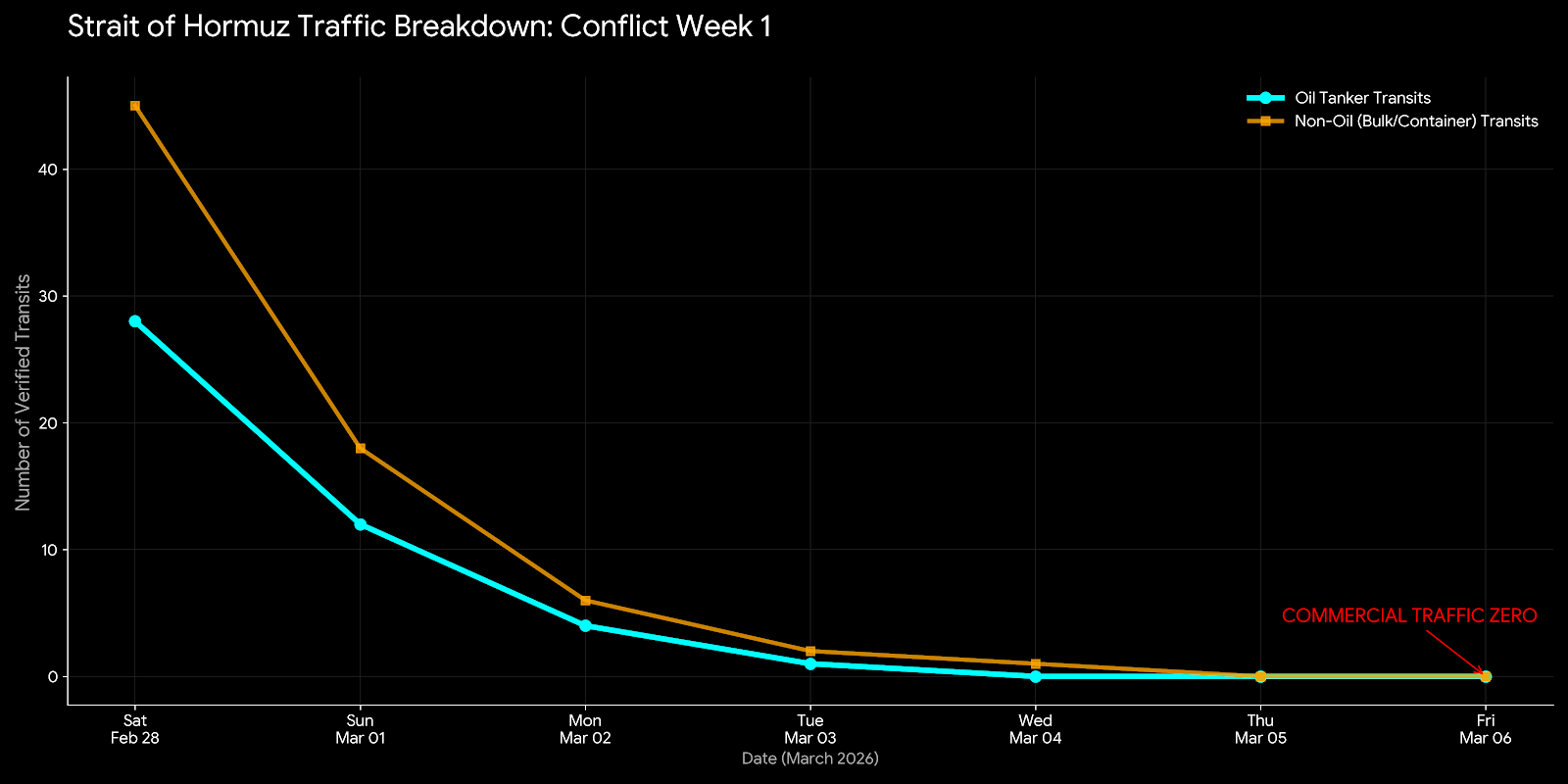

4. Strait of Hormuz Total Maritime Darkness

As of this morning, satellite data confirms few to no commercial transits in the last 24 hours. The insurance market has effectively closed the region, with War Risk premiums now exceeding the value of the vessels. This total maritime shutdown is the primary driver of the 24.2M bpd in frozen global supply.

5. Seeking Opportunity Amidst Political Mistakes

While Washington appears to be pivoting toward an interventionist mistake, MacroEdge remains focused on the resulting market dislocations. History shows that when politicians walk into traps, it creates massive inflection points for investors. We are continuing to identify opportunities in South American energy assets and domestic infrastructure that are poised to thrive as Western policy failures escalate the global supply crunch.

Impacted/Shot vessels in the Strait:

Strait of Hormuz transits:

While we reflect zero commercial traffic at zero, there have been several instances of ‘rogue runners’ identifying as Chinese ships and passing through the Strait. Until the Chinese pick up the phone to the Iranians, they remain aptly supplied to absorb the early days of an oil price/gasoline price shock, and are positioned beforehand. While the CNBC talking-heads have highlighted things like Venezuela, it doesn’t really do anything for the US in the near-term from an energy supply standpoint.

Oil Surge Continues

The oil surge continued today, with a ~12% move on CL. This notched the weekly move up to one of the largest moves on record, and the largest since 1982, in percentage terms. The chart structure looks fantastic, and many of the technical signals we’ve been highlighting for the last six weeks or so have materialized. We will well ahead of the curve here, and dismissing the academics & CNBC parrots has proven to be the best way forward, yet again.

Continued below (Oil Surges Continues, Natural Gas Note, Employment Review - February Bombs, Saturday Macro Note Preview, & More).

While short-term technicals look extreme, monthly & 3-month technicals look very constructive for higher levels. The longer the conflict lasts from here on out in the manner it’s in - especially with energy impacted to the degree it is, above $95 WTI and clearing, we are likely to see much higher levels from there.

Many of our high-torque E&P plays highlighted over the past few weeks have moved significantly. We’ll talk more about these tomorrow.

The L&G commodities basket has room to run higher:

Natural Gas Note

Following up from the Macro Note yesterday, the outsized move in natural gas today was captured by many of you who had X alerts on, and I was glad to see the comments mentioning the even more outsized move in BOIL today. It continues to be a relevant callout - especially with Asian nations dealing with LNG crises very soon, and Qatar Energy being almost totally offline - that there’s some catching up that Henry Hub prices can do relative to the move in oil prices. While some, like our guest on MacroEdge Radio this evening, astutely noted that oil and gas stocks have been a very mixed picture throughout the week, I primarily chalk that up due to hedging & lack of torque.

Lots of supportive divergences on natural gas - and unhedged E&Ps in the US are the best way to capture upside here:

Employment Review - February Bombs

The employment report was largely a ‘crashout’... dumpster fire, describe it how you please. More massive revisions and the economy shed almost 100K jobs in February. The ‘run it hot’ crowd faced a large blowback today as stagflation shot a poison dart into that narrative for the time being.

Employment growth on a Y/Y basis is about to flip negative for the first time since the pandemic (but more importantly, the GFC):

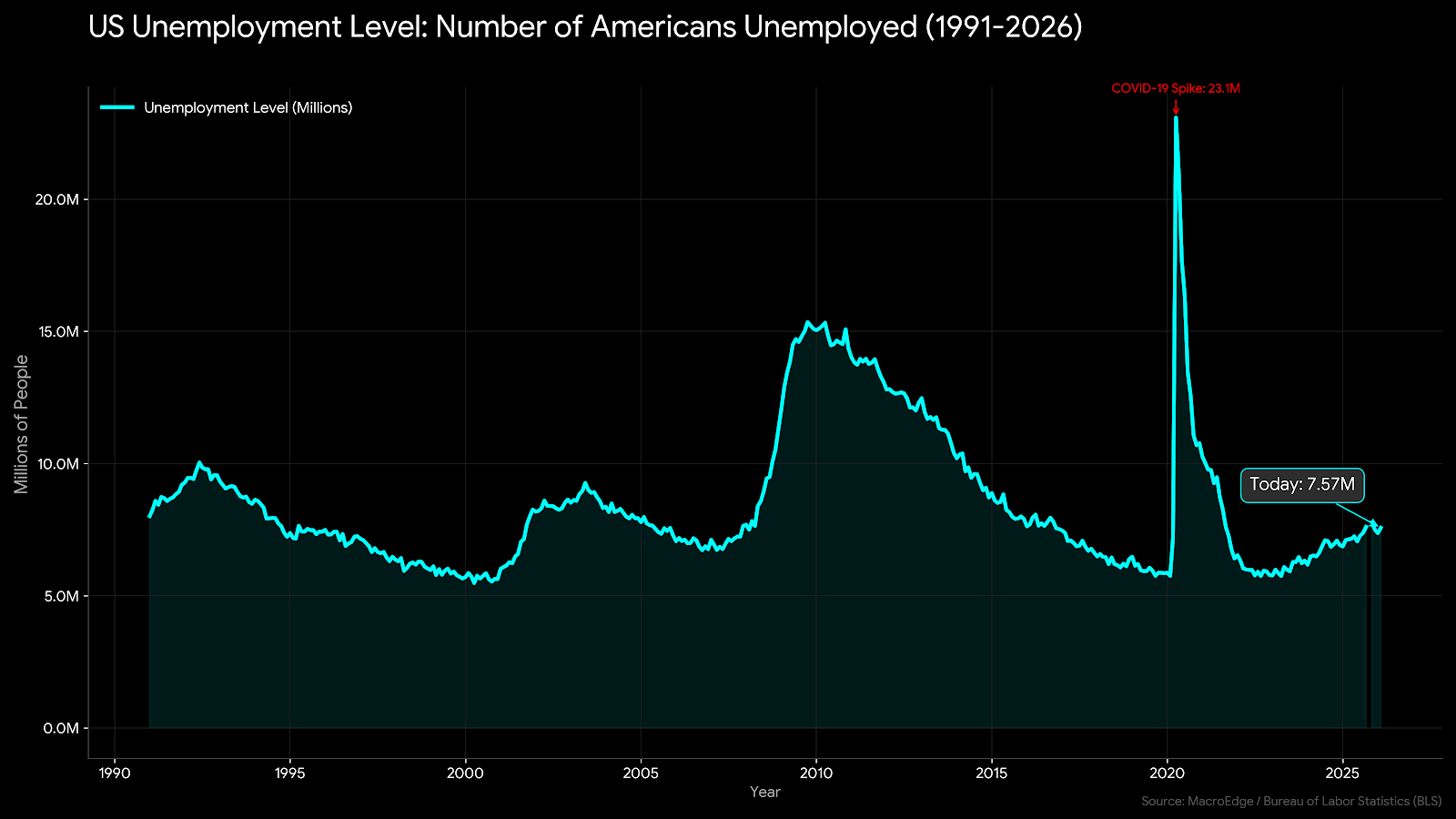

Total Unemployed Americans:

Saturday Macro Note - A Look at the Energy ‘Evolution’ for Opportunity

Tomorrow we’re going to continue the energy thematic - looking at the rotational opportunities as the energy trade evolves. While parabolic energy prices are only good for a very short period of time - because they result in eventual demand destruction in the global economy - we can seek to capture high torque opportunities.

Building an Opportunity-Seeking Community

The Commodity Surge from 30,000 feet

War Note #3 - Is There an ‘Off-Ramp’ or are we escalating

A Discussion on Software - is SaaS > AI Slop?

Data Center Troubles

Portfolio Strategy Discussion*

Sunday Macro Note - Distribution, Futures Update, Week Ahead, and More

Have a great evening, or start to your Saturday morning, and see you soon.

For more details, please refer to our Terms and Conditions.