Redeye Macro Note: The Last Rate Cut?, BoJ Hike, New Reports, Inflation Bubbling, Yields Rising Pt. 1

In this Redeye Macro Note - available to our entire community - we talk about the coming rate cuts, rising yields, risk from Japan, a new possible daily Macro Minute report, inflation, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Saturday evening MacroEdge Readers & Community,

Glad to be back for another late-night report, truly in the ‘redeye’ hours. We’re back into the cadence from the office and pushing hard to finish out the 2025 year strong across all of our independent MacroEdge cylinders.

In this Redeye Macro Note - we’re going to dive into the likely FOMC rate cut and potential implications from it - looking at where the dual mandate currently stands - and how the market is signalling upside inflation risk in recent days from further easing. While we’re likely to have a Central Bank in the dovish ‘driver’s seat’ next year - with Hassett likely to take the helm - the bond market and commodities alike have reacted negatively to this.

While some strategists are emphasizing ‘strong labor’ to fit their own narratives going into 2026 - using initial claims (reduced efficacy in 2025 as we discussed in the Midweek Macro Note) and other labor metrics, I would emphasize strong commodity performance as the core reason for seeing higher yields. With little commitment from any government in the West to fiscal sanity (yes - Japan, and other Asian nations too) - we’ve seen yields, particularly on the long end push back towards their cycle high. This is not unique to the United States, which is seeing steepening in the 2y10y & 3m10y, as yields push to new highs in Japan, Europe (+the UK), Canada, Australia, New Zealand, & elsewhere.

This report has less of an emphasis on equity markets - and much more of a focus on bond markets & inflation globally - so let’s dive in. We’ll call this Part 1 of ‘Inflation Bubbling & Yields Rising’ - and continue this series as we progress into 2026.

Tonight:

New Reports - Daily Macro Minute

End of February MacroEdge Community Gathering - First of Many

The Last Rate Cut?

BoJ Rate Hike Timing

Inflation Bubbling

Yields Rising

New Reports - Daily Macro Minute - In Discussion

I am looking at the roll-out of a new ‘Daily Macro Minute’ available to everyone - that would be dispatched every morning before market open - covering 3 to 5 of the most interesting charts & datapoints for the day, from the week, or anything in between. This has been something requested by our community on X - and there is a poll on my timeline now that you can vote on if you would like to see more frequent content from us from an email delivery standpoint. We may send out this content through the existing Substack, or through a new ‘Daily Macro Minute by MacroEdge Substack’ and this is something we’re going to decide in the next week or two.

If you haven’t yet subscribed to our existing reports, portfolio strategies, and more, you can do so below through Ozone for two weeks, or via Substack.

Development on our new macro data points continues, and we expect to have these finalized going into the new year.

MacroEdge Community Gathering - First of Many

Keep an eye out on a MacroEdge Community event at the end of February - in a winter destination. We are looking to get 12-15 people together for a social get-together over a 3-day weekend. More details will be available soon.

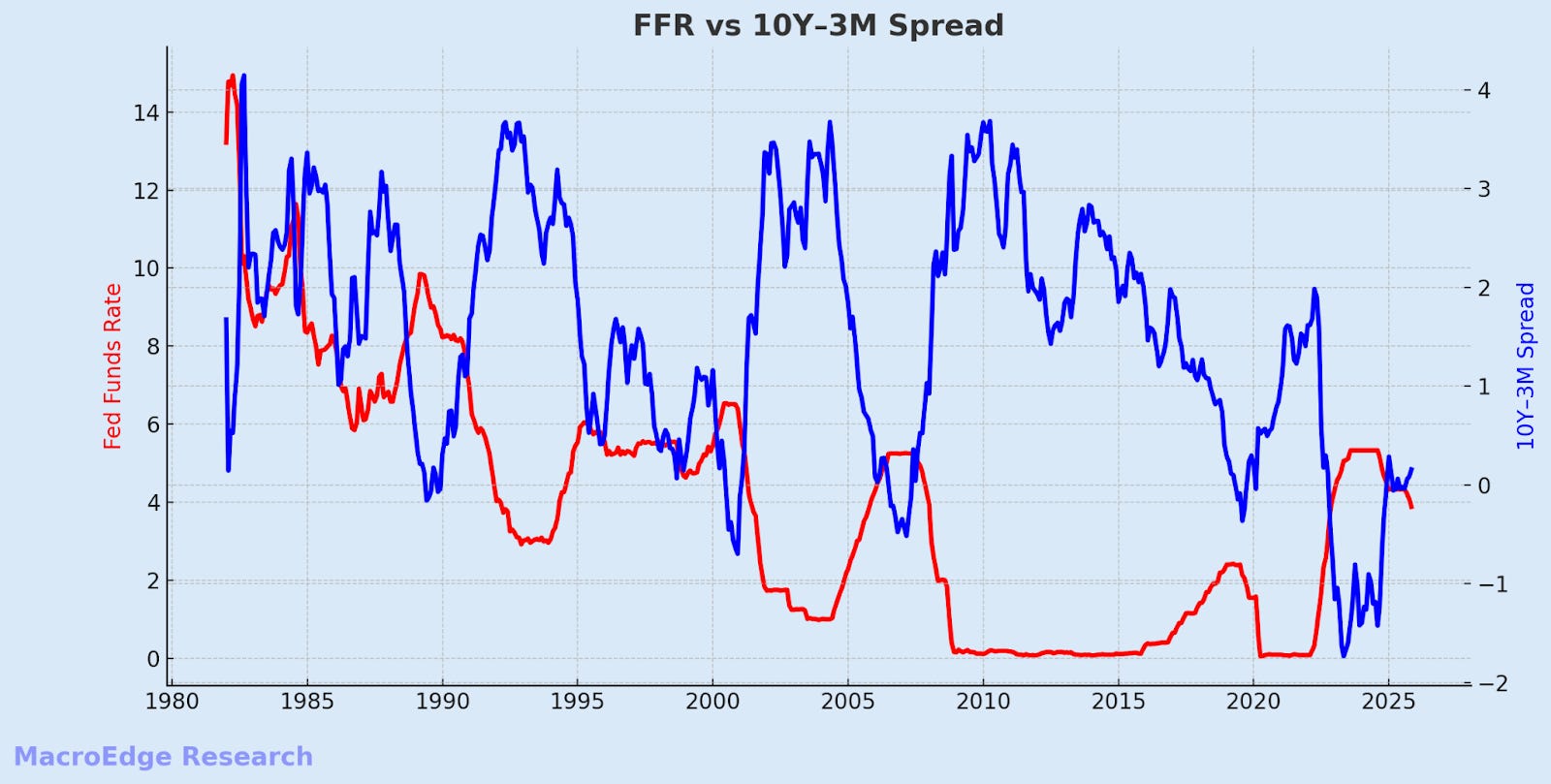

The Last Rate Cut?

Being overweight a continuation of massive rate cuts right now seems like a risky proposition, until & unless we see a broader breakdown in the 2Y/10Y/30Y, all of which are moving higher - around the globe. That being said, a steepener in the 10Y3M spread is historically correlated with a lower FFR, as the spread moves higher. If we see hot employment data, like we saw on Canada on Friday in temporary employment, this could quickly change the dynamic. The current dynamic is mispriced towards another substantial easing cycle, though they that may *eventually* be in the pipeline if commodities continue to hit all-time highs and induce broader demand destruction in the economy.

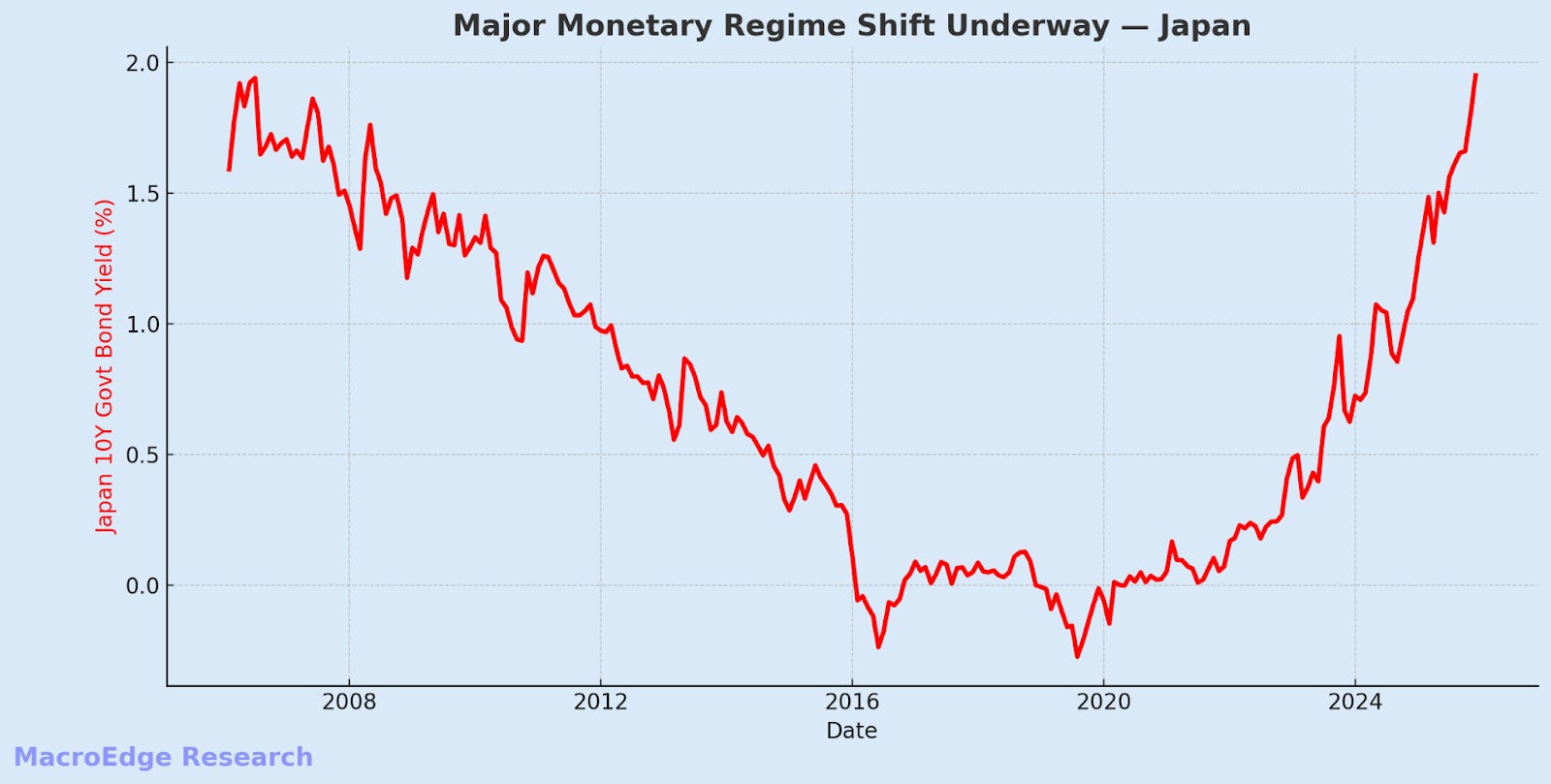

BoJ Hike Timing

I continue to place a key emphasis on the fact that global tremors are often felt when the BoJ begins easing, signalling troubles forcing said easing - rather than the opposite scenario. The BoJ is almost certain to hike at this meeting in a week, barring any intervention from Bessent.

Major monetary shifts are underway in Japan - with yields pushing towards record levels across timeframes.

The bond market & vigilantes are alive and well - and even though there’s been a massive reload of the Carry Trade from July - November and a boost in leverage.

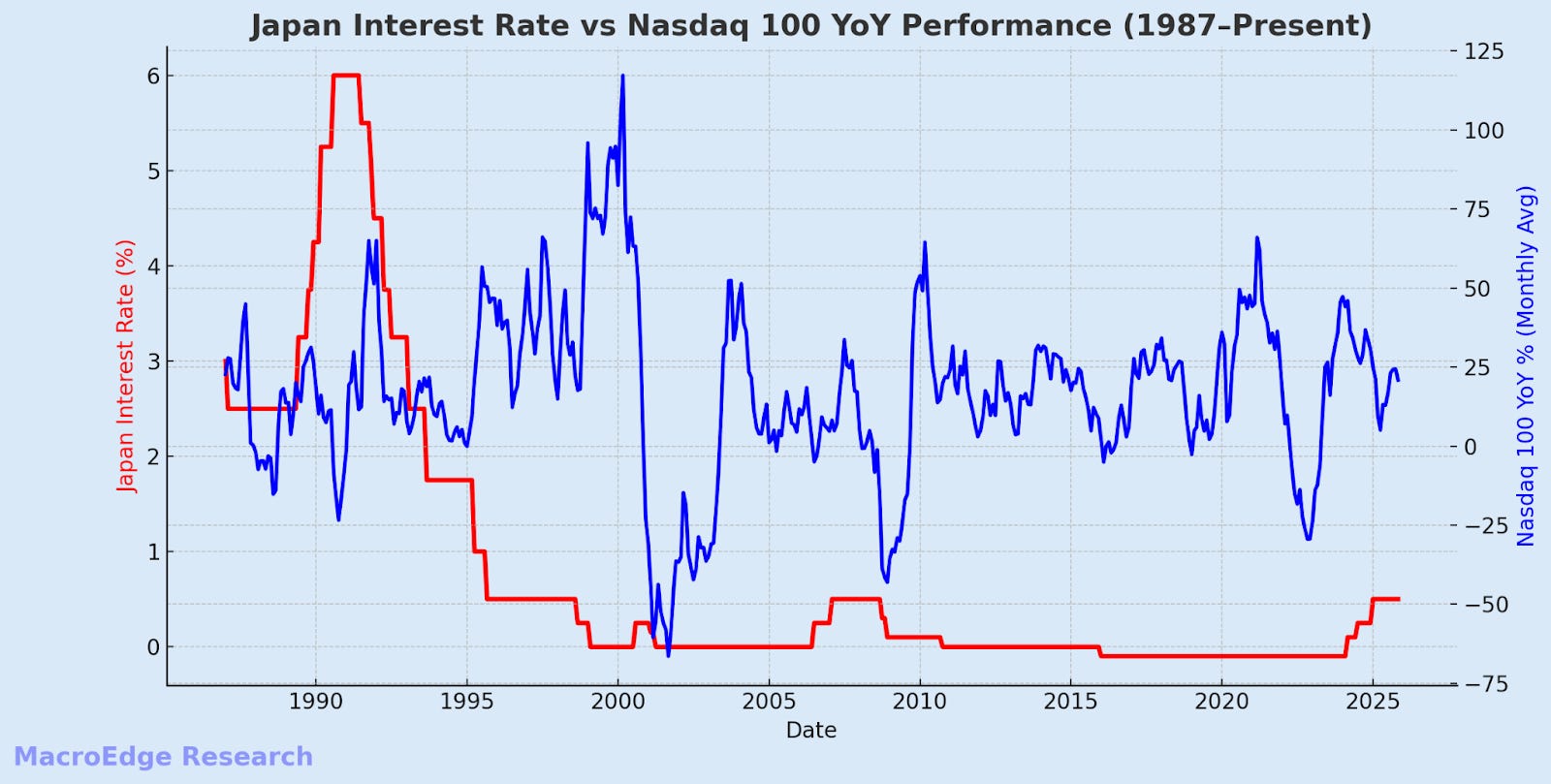

When Japan begins easing, note the significant underperformance of the technology index.

Inflation Bubbling

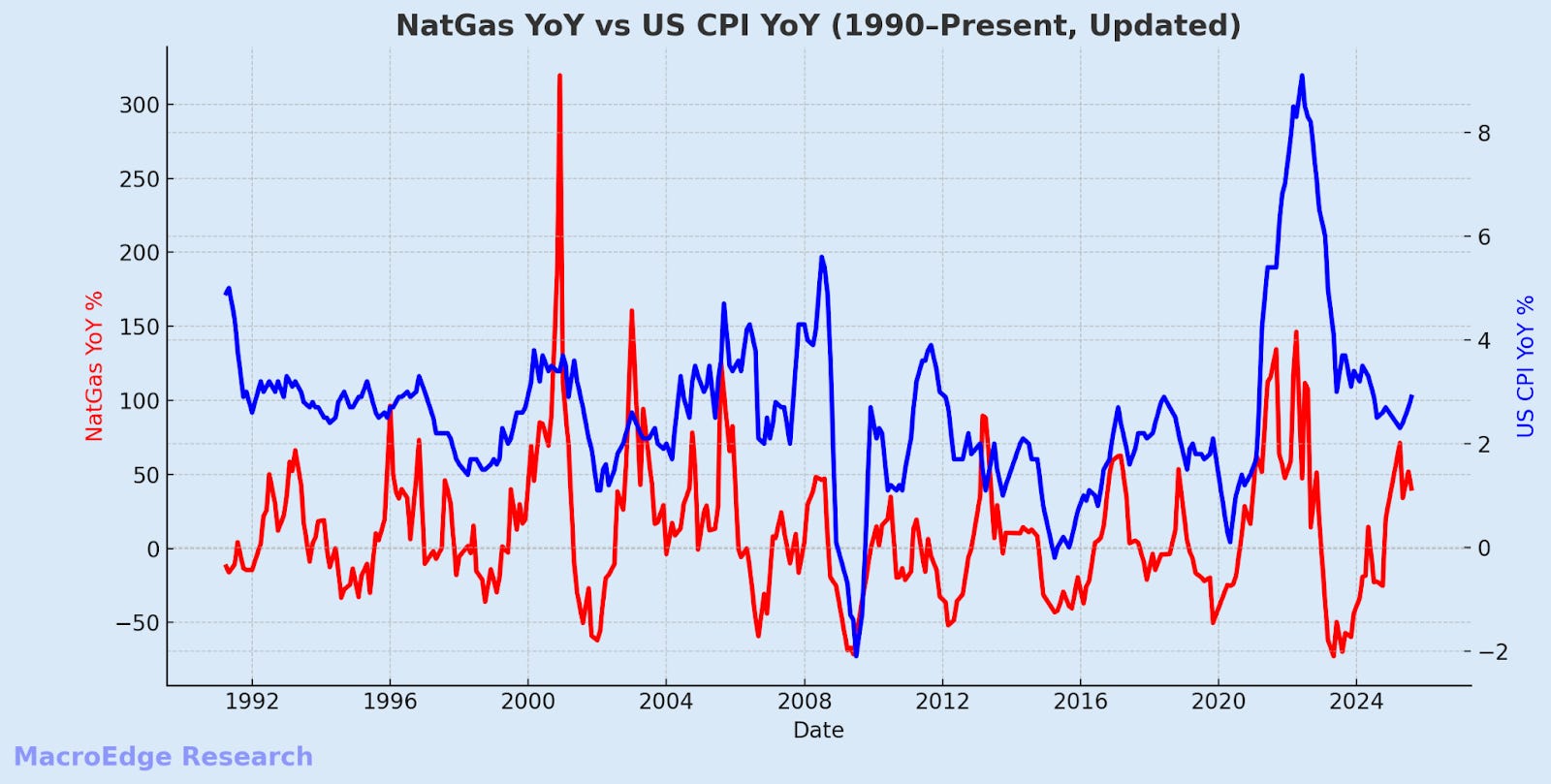

The inflation and bond victory laps are misplaced for the time being, unless yields >2Y continue lower. The missing elements to much more sustained commodity pressures are oil and gasoline prices, and structurally, there’s little reason for them to fall further from current levels - with oil having retested the mid-50s 4 times this year, and gasoline inventories tightening into the winter. Even if air travel demand softens - a geopolitical event would be enough to get WTI higher, and it’s historically mispriced relative to the broad commodity basket.

Take a look at NatGas v CPI, for example (YoY):

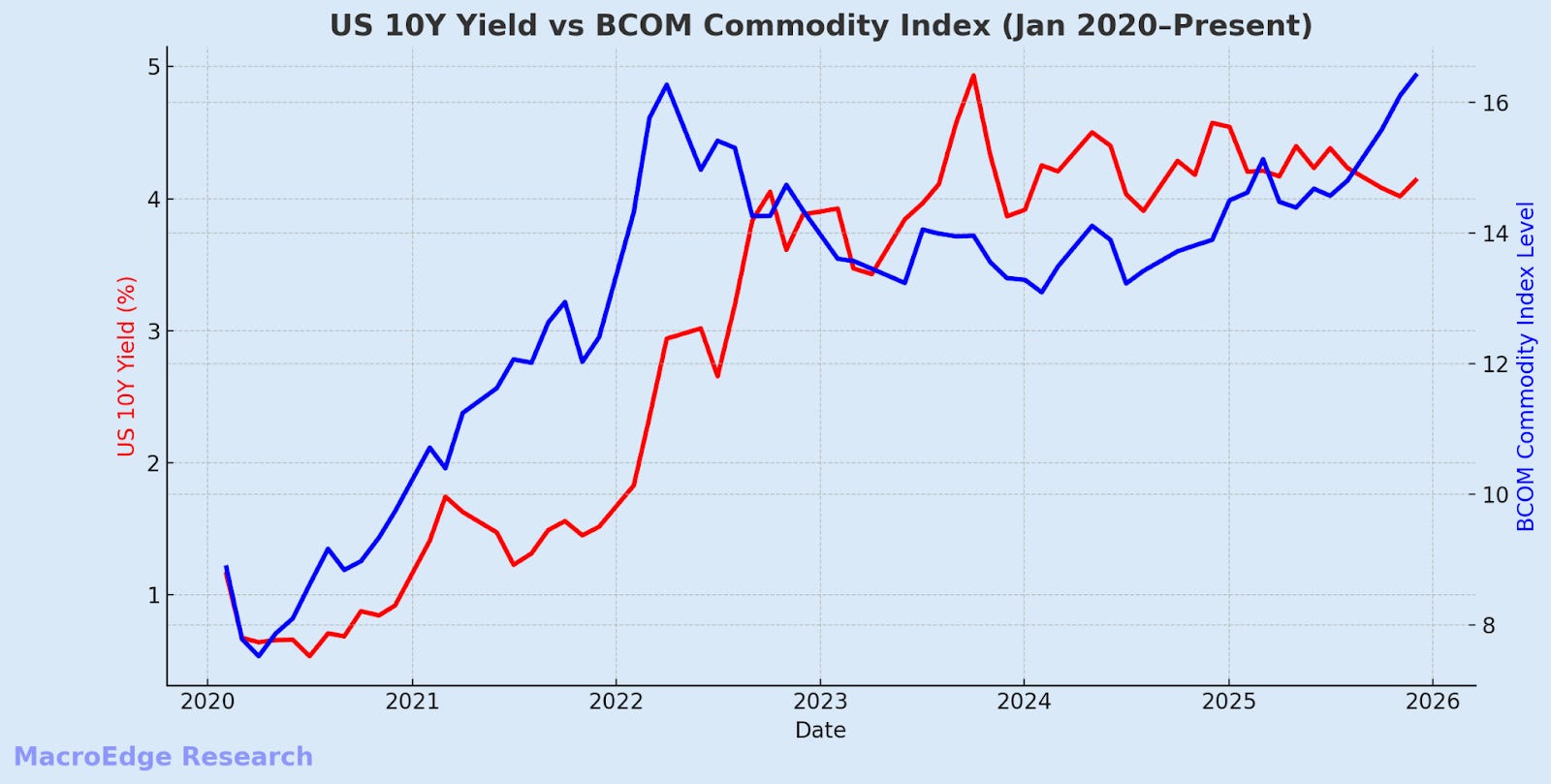

And as stated in the intro - commodities are in the driver’s seat on the 10Y for the time being, not U3.

The Commodity Index (BCOM) is nearing a push through cycle highs.

(and that’s without significant participation from oil & gasoline – yet).

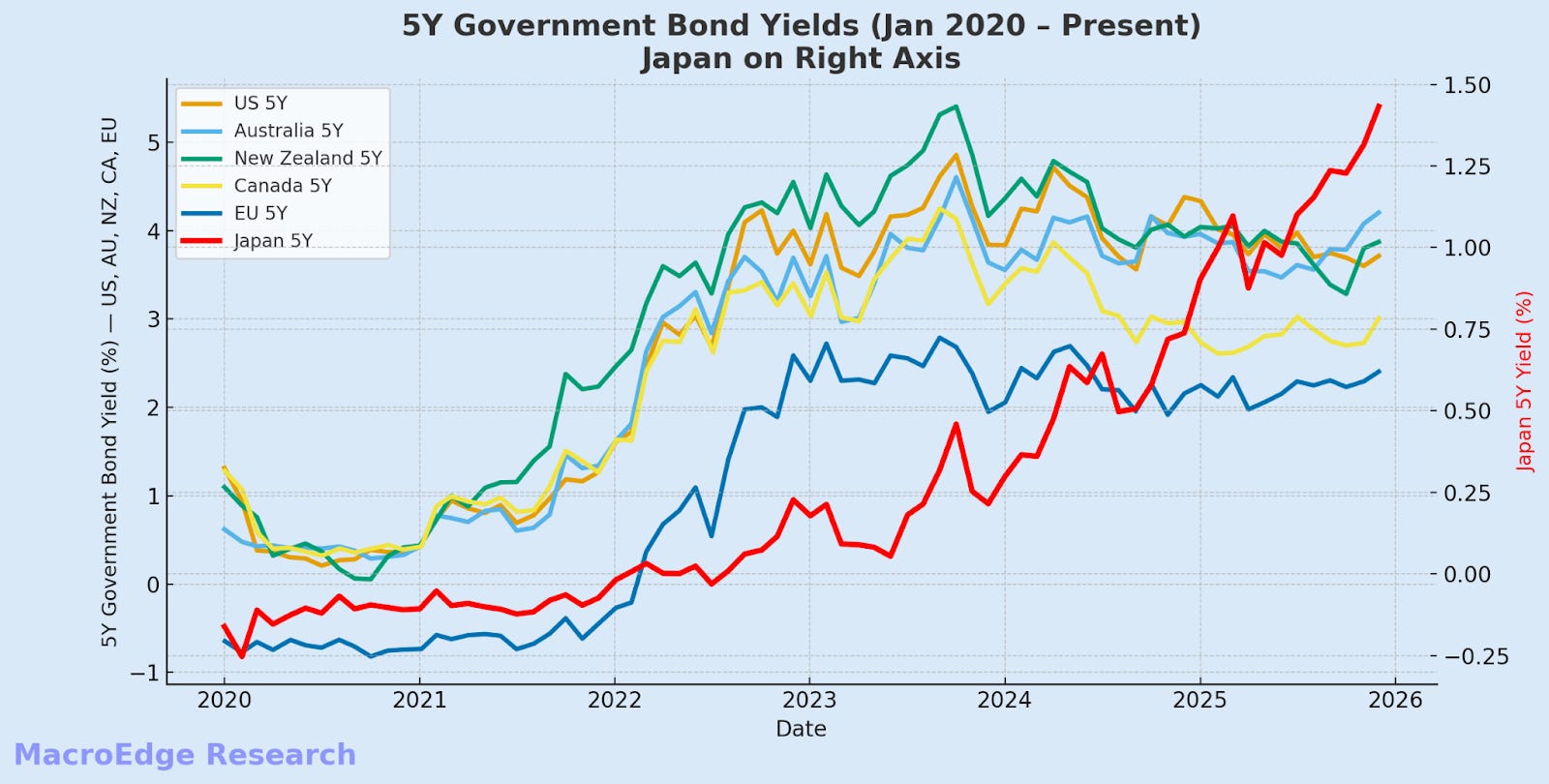

Yields Rising

Yields have been moving higher as bond vigilantes have woken from their apparent slumber. Below is just 5y yields.

‘Running it hot’ will likely be the grand policy error of 2026 - especially if central banks are forced to rapidly pivot & begin hiking again to combat yield blowouts. Yields have been in a multi-year consolidation phase, and the end-result is likely to be an explosive one, with direction still to be decided, though tilting more to the upside in the last several weeks.

MacroEdge Report Schedule for the Remainder of the Year

There’s no slowing down for the remainder of the year - as things are only going to continue to get busier on our end and into 2026. Below gives you an outline of reports for the remainder of the year, and what we’ll be focused on tomorrow.

Sunday 12/7

Technical Overview / Review - Bonds & Equities

Commodity Surge

Dollar & Currency Opportunities

December Monthly Ozone Pro Report Overview & Portfolio Strategy Update

Global Easing Cycle Wrap-Up

Upcoming Employment Data

The Bankruptcy Cycle

Wednesday 12/10 - Midweek Macro Note and FOMC Summary

Thursday 12/11 - Monthly Ozone Pro Report & Portfolio Strategy Update - December

Friday 12/12 - Redeye

Sunday 12/14 - Weekly Macro Note

Wednesday 12/17 - Midweek Macro Note - MacroEdge Product & Service Updates

Friday 12/19 - Redeye Macro Note - BoJ Review

Sunday 12/21 - Weekly Macro Note

Wednesday 12/24 - Christmas Eve Edition Macro Note

Sunday 12/28 - Holiday Wrap-Up, 2026 Outlook

Wednesday 12/31 - MacroEdge Year in Review, Saying Goodbye to 2025

Until tomorrow, when we await the next round of fiscal pumpers to talk about the next reason for a Sunday evening gap up.

For more details, please refer to our Terms and Conditions.