Redeye Macro Note - The Lagging Hormuz Closure Impacts, Warming Things Back Up, Portfolio Strategy Commentary and Note

In this Redeye Macro Note - we 'foam the runway' for the week ahead, outline the schedule of coming reports, discuss an inevitable Strait of Hormuz lag that has yet to materialize, and more...

Don Johnson (@DonMiami3), Chief Economist

Good Saturday evening MacroEdge Readers & Community,

I hope you have all had a fantastic past week and start your weekend. This past week has been a whirlwind, and I apologize for our brief downtime on the reports on our end. I will be making my way out of Mountain Time in the next few days and returning east to get things fired back up from the office. Over the last week, we’ve collected a lot of interesting data and are continuing to watch rapid evolutions in both markets and the economy. The trend of an ‘i-shaped’ economy has accelerated in recent weeks as we’ve seen the Nasdaq make an almost 20% move this month, while consumer confidence and current economic conditions, as measured by the University of Michigan, are near all-time lows.

The report this evening is going to be a nice laying of the foundation for us to kick back into high gear for the weeks and months ahead. We are back to our regular report schedule after the brief delay - and the full schedule for the week ahead will be available tomorrow evening.

The latest on the geopolitical front is one of a lot of noise. Things are pointing more toward a ‘re-arming’ on both sides at this point than any sort of off-ramp. The debacle of the last two days was one where Kushner & Witkoff were supposedly going to visit Pakistan to meet with the Iranian FM, but both parties backed out of actually meeting with each other, and things quickly fell apart. Right now, it appears that there is little to no communication at all between the two sides - and US military resources continue to be ‘surged’ into the region. Israel made new strikes on Southern Lebanon today, and it’s quite likely that we see things continue to flare up there as well for the next week or two. The exact timing of when a broader operation may resume is impossible to time, but some smart individuals that I talk to seem to think between now and May 15th are a potential window if things continue the way that they are. The Hormuz reality is one that is accumulating in its size and impact, and I don’t think people can wrap their head around how severe these impacts will be if it remains closed. While much of the globe has been able to ride through the first almost 2 months of the Hormuz closure without substantial impact, the bite is going to hit now, and especially so if/when Iran begins to curtail oil production.

Iran is now likely within a week of needing to shut-in some of their production capacity, so keep an eye on data related to this in the coming days, and we even saw them bring an old VLCC out of inventory in the past few days to act as an ‘offshore buffer’ for production capacity now that onshore storage is full.

Not yet a MacroEdge Ozone subscriber? Access Ozone and get all of our research, data, reports, and more, below:

The Lagging Strait of Hormuz Impacts We Must Continue to Respect

One of the most obvious points to note is that the Strait of Hormuz closure is going to impact Asia, Oceania, and Europe the hardest (and before the United States). As tankers rush to the US to fill up and take product back overseas, we’re going to start seeing aggressive draws on onshore US refined products, which will tighten markets further… This is especially true since we’re not seeing any meaningful production or drilling activity spike right now. I expect that we start to see drilling activity move materially higher come Q3, but for the time being, producers that I speak to are not expecting others (or themselves) to ramp up activity in any meaningful way as everyone remains very cautious about ramping up capex with such a negative outlook on E&P companies from Washington DC. Politicians seem to think that exploration companies want to hold the bag and ramp up production while being targeted - but for the time being (and this is not going to last forever) - capex discipline is still in force.

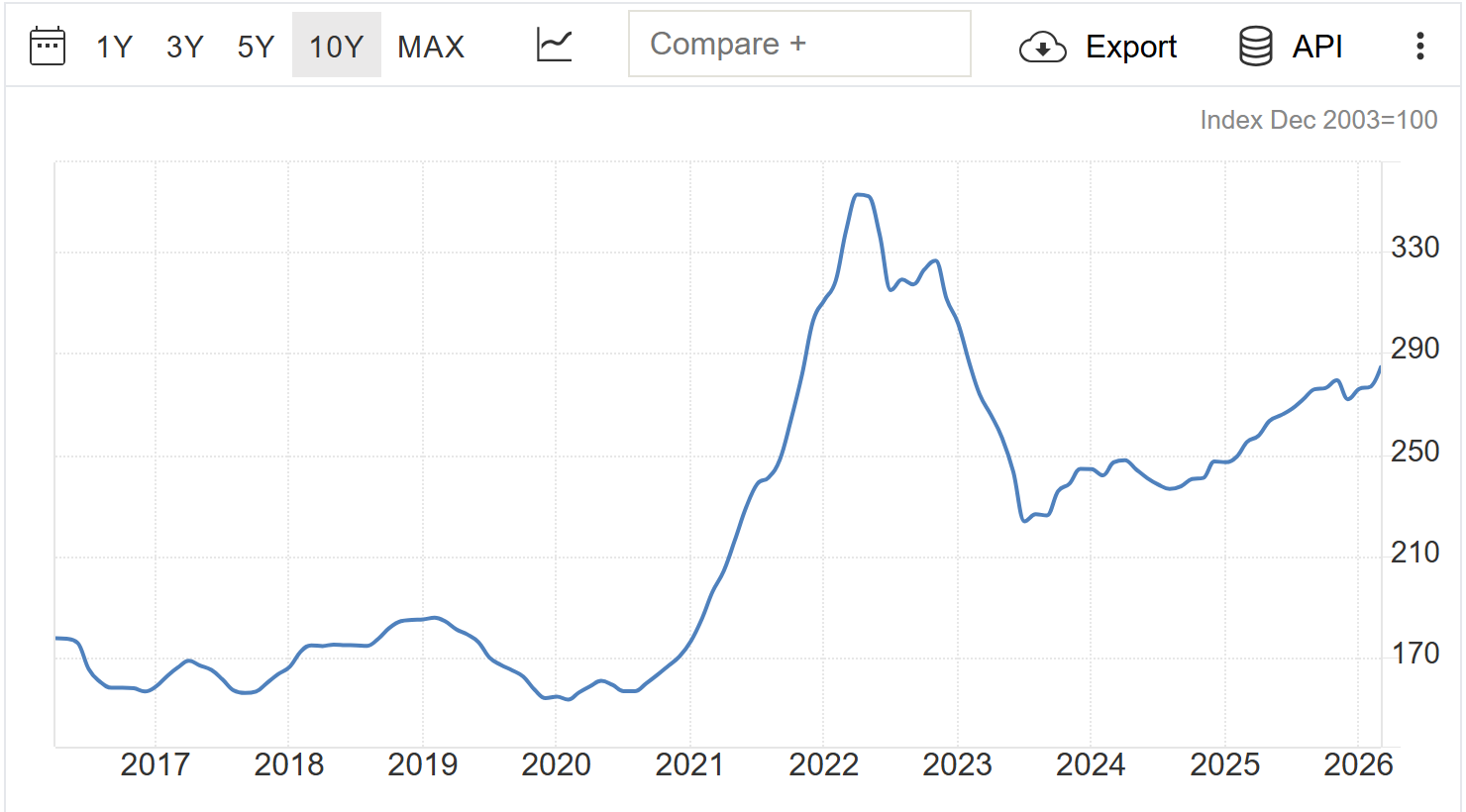

While there are offsets to things like oil production through the North American valve (and SPR releases) for the time being - the same cannot be said for other commodities. One of the most obvious impacts outside of the oil and gas space from the Strait closure continuing is going to be food supplies and input costs in Urea and fertilizer. Fertilizer costs are starting to ramp back up:

And that will likely produce some sort of ‘farm bailout’ package in the months to come.

Continued below: The Lagging Strait of Hormuz impacts we must continue to respect, Energy Portfolio Strategy update, Portfolio Strategy update and commentary from Six)