Redeye Macro Note: The Ghost of Deflation, Emerging Opportunities in Oil & Gas, Distribution Continues, GDP Review & More

In this Redeye Macro Note - we discuss the 'Ghost of Deflation', highlight emerging opportunities in oil & gas, discuss supportive technicals, highlight distributive patterns in tech, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Saturday morning MacroEdge Readers & Community,

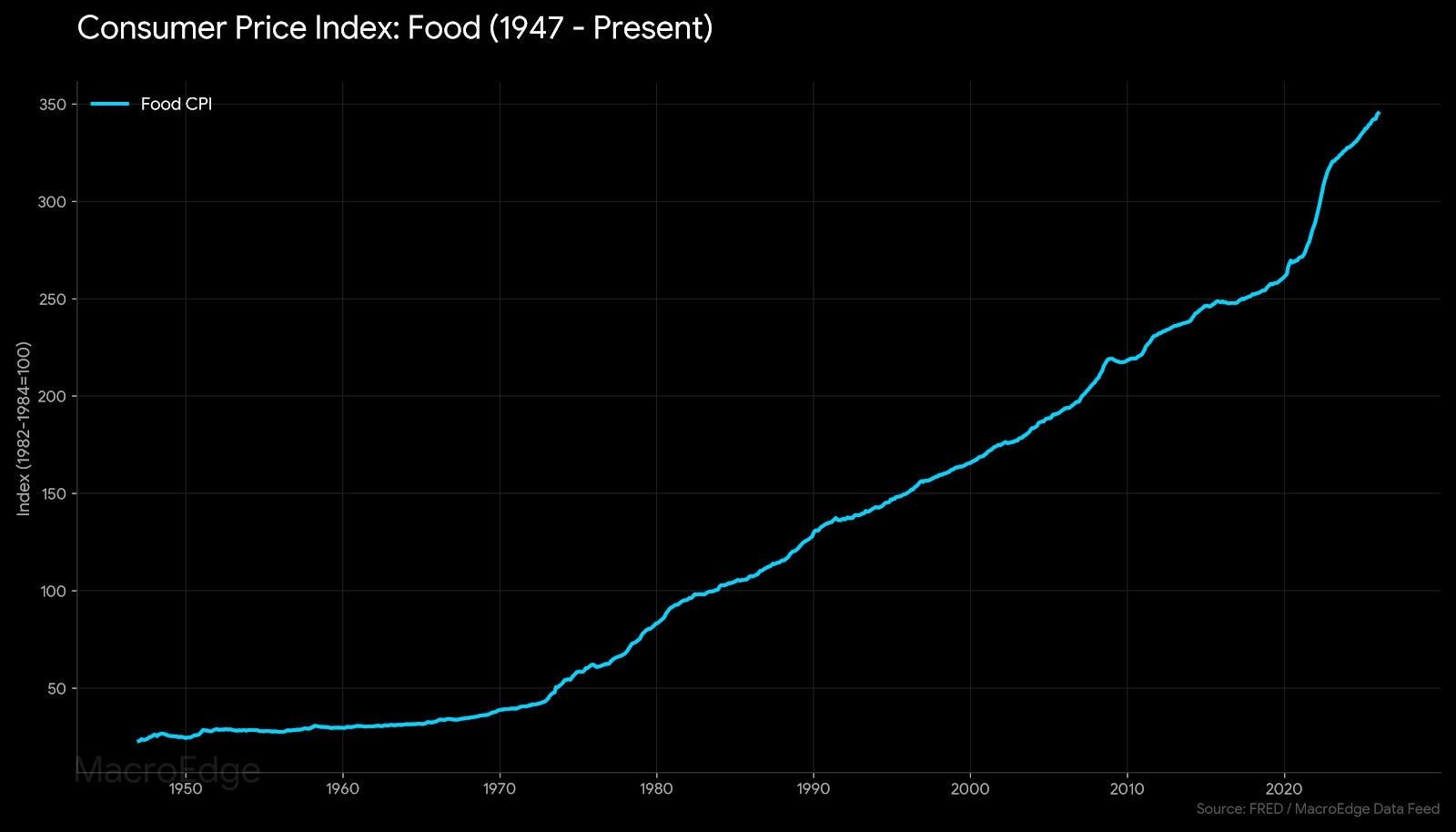

I am counting down the days before I blast off to West Texas for a few days and catch up with a few friends from long ago who have climbed the ranks of the oil & gas world in America’s capital of the E&P scene. There are many interesting developments continuing to happen globally in the energy sector - and that means I & more importantly, we as an organization, want to be on top of the developments before they happen and reflect in public markets. One of the things that I continue to harp on in the face of opposition is the fact that I am not seeing broad price change deceleration reflecting in costs of services, goods, etc. & that has landed me at odds with several very respectable economists and forecasters who continue to harp on the ‘ghost’ that is deflation. The ghost of deflation is something we continue to hear about with things like private measures showing broad price change deceleration - though that just means very high price levels are rising at a less fast pace than what we observed from 2021 - 2023. The CPI as a measure itself is also greatly understating costs in things like healthcare and insurance. Also, things like food inflation are reaccelerating globally, and are especially noticeable in places like Canada and Argentina… but also here in the United States:

On a long enough timespan, we can always count on the ghost of deflation returning with vigor, but that time is not now.

Domestically, policymakers have done all they can to ensure and inhibit native-born domestic population growth - but maybe it doesn’t matter.

From hotel prices, to rents (yes, even though the chartists might say otherwise), airline ticket prices, food prices, healthcare prices, business service prices, home prices, etc. - the ghost of deflation still looms in the shadows, sounding greatly intimidating for those that listen to its call - but fail to realize that it’s not yet approaching.

While the end game will be deflation in some way, shape, or form - from a combination of demographic decline (which is just beginning to get a foothold in the United States & even more so ex-immigration), these unsustainable price levels relative to income levels on the aggregate, and the widening gap between the hyper wealthy and bottom 80% of the ‘i’ - the ghost of deflation should be ignored for the time being until we see another material spike in energy costs as the primary driver. While we’ve committed ourselves domestically to repeated policies of energy stupidity (with unreliable grid additions) and now with unsustainable growth in demand from data centers, all of the above really just leads us into a broader discussion about emerging opportunities in oil & gas - and how structurally, positive signals could be emerging for our differentiation thematic for the year - especially in identifying these opportunities in oil & gas.

I hope you find the report this morning interesting, and most importantly useful - and let’s have a fantastic rest of February.

Trident I Update Part 2

We are going to have several new announcements on Trident I in the coming weeks & months - and I am excited to share them with you all. While we originally had planned for much earlier announcements here, we’ve gone through countless discussions and hours of planning to get the plan correct for Trident. Focusing on a broad spectrum of opportunities and a global macro thematic with no mandate - we’re going to be delivering the future of fund management through Trident.

Emerging Opportunities in Oil & Gas

As a follow-up to yesterday evening and our theme of differentiation for the year, I continue to seek out less sought-after opportunities this year from a return standpoint. While everyone is chasing things like memory & data centers (as well as the entire AI thematic that I still believe will crash & burn to a scale we haven’t seen since the Dotcom bust) - the commodity basket continued to advance higher today after a brief pullback over the last 2 weeks:

(Below: 7 opportunities in oil & gas - E&P pure plays, distribution continues - especially in technology, Project ZA update next week, reports for the rest of February, GDP report, consumer spending, and more)…

As discussed yesterday, we’ve also seen some moves materializing across the board in energy prices, but particularly in oil and gasoline. This has caught my eye, as oil has held the key $54bbl half a dozen times or so since the April bear trap oil last April during the whole tariff tantrum.

For crude (WTI - monthly) - the look is quite a positive one for the time being:

The positive MacD cross & bullish RSI divergence are further positive technical signal here…

Five different support level holds in the 50s:

Yesterday, we discussed some of the structural factors supporting higher prices here - and any number of the below factors could fuel the fire of WTI and quickly return prices to the $75-$90bbl range (obviously, the political administration isn’t aiming for this)...

Gasoline prices also look highly constructive for higher levels:

While the 2026 consensus is strongly against higher oil and gasoline prices, consensus is where our differentiation theme goes to die. There are plenty of momentum factors that could easily push prices higher from here: geopolitical risk, tighter OPEC discipline, an SPR floor, shale and drilling discipline (we’re seeing some of this finally), & demand resiliency in developing/EM countries.

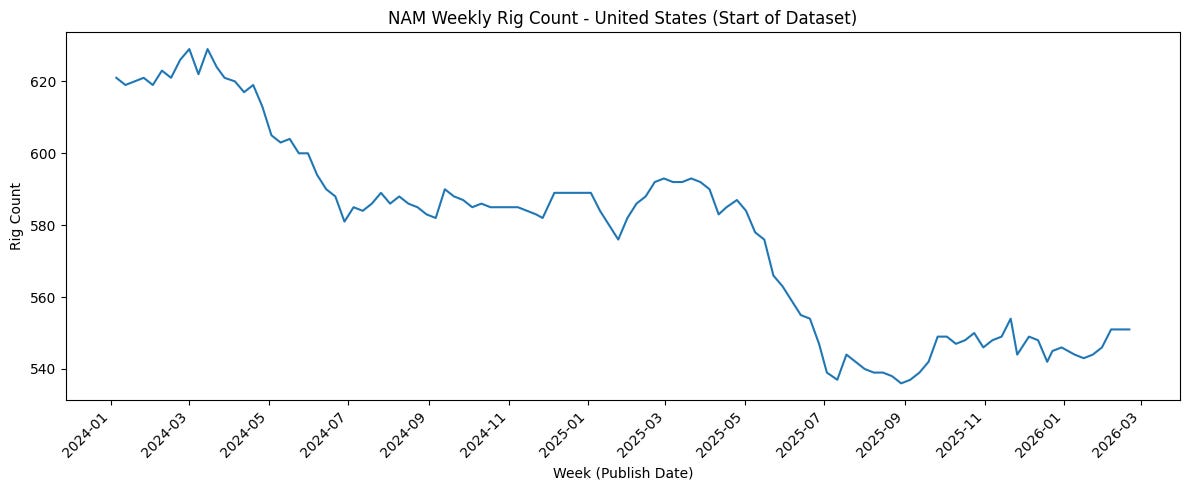

Baker Hughes NAM Weekly Rig Count:

For my favorite E&P pureplays for a broader move higher in WTI -> play the Delaware Basin & capital disciplined E&P names, and seek out opportunities in niche leaders like Chord in the Bakken.

Matador Resources (MTDR)

Permian Basin Trust (PBT)

Venom Energy (VNOM) - the yield vehicle for Diamondback Energy

Chord Energy (CHRD) - the king of the Bakken

Permian Resources (PR) - exposure across the Delaware Basin

SM Energy (SM) - acquisition target

Northern (NOG) - dividend king

MTDR:

PBT:

VNOM:

CHRD:

PR:

SM:

NOG:

Very interested in the opportunities above, and if WTI continues to hold this $65/66 level as a springboard, these names above are going to respond very positively, and offer exposure to a WTI rally.

Distribution Continues

Today’s reaction to the Supreme roll-back in IEEPA tariffs was very tame… I was frankly expecting much more given the market environment we’re currently in.

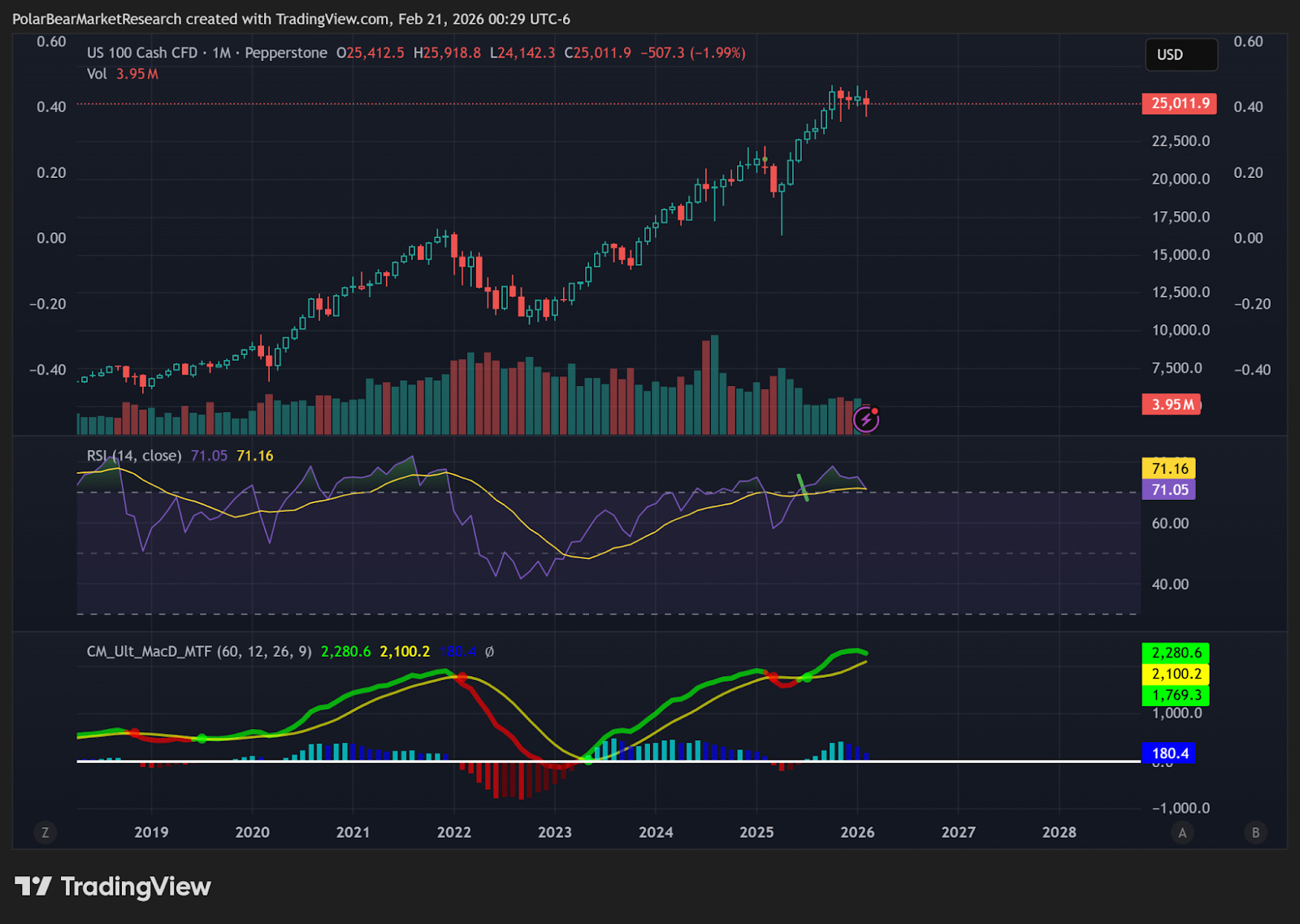

Tech led the rally for the day, while the S&P rose about .5%, and the Dow/Small Caps lagged the former indices. The price action stall in the Nasdaq is continuing to become more noticeable:

While negative signals haven’t fired, they are moving in that direction without any move higher in the next two quarters or so. Even with the huge rallies we’ve seen in individual sectors within tech, the MAGS struggling has contributed greatly to the stall in higher price action.

Until further notice, I consider this pattern to be a distributive one, as I have for the better part of the last ~3-4 months in tech.

Project South Africa Update

This coming week, I am going to drop the first MacroEdge ‘Project South Africa’ update in a long time. For those who have been reading since our founding, and even before, I have labelled the broad long-term economic thematic in the United States as such.

In this, I will discuss some of the underlying trends and similarities in the United States we continue to see shaping up in a ‘South African’ fashion that are greatly concerning, and warrant paying attention to.

Up Next in the Weekly Macro Note

On Sunday evening, there’s a lot of ground to cover going into the last week of the month:

Macro Week Ahead

GDP Growth & Inflation Pulse

Supreme Court Tariff Ruling

New Tariffs & Analysis

February Cryptocurrency Report

Technical Deep Dive for February

Remaining reports for February:

Weekly Macro Note (Sunday)

Midweek Macro Note (Thursday before market open)

Data Center Update - February / AI Bubble Update (Saturday morning)

Weekly Macro Note (March 1st)

About That Golden Age GDP Report for Q4 2025 (@RealJohnGaltFla, MacroEdge Contributor)

Yesterday’s GDP report came out and of course the media focused on their favorite metrics but the statement from the Bureau of Economy Analysis couldn’t have been release before President Trump released his usual social media commentary.

Actually, “Two Late” (sic) Powell could have cut rates 100 bps in September but the President who is nothing even remotely close to being an economist much less a banker doesn’t understand anything about the Fed’s transmission rate or duration.

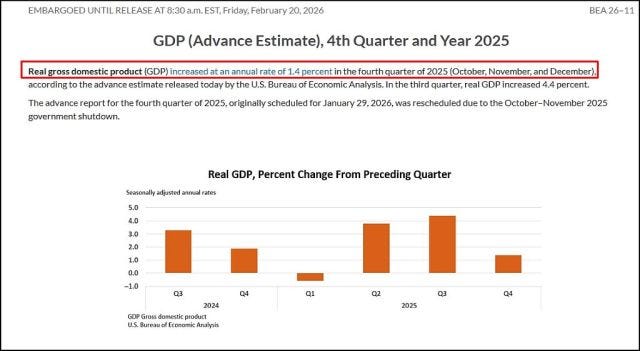

The report was ugly enough for him to truther so let’s see why together:

That’s brutal, a 3% drop primarily attributed to 1% for the shutdown and a general slow down in economic activity across the board. This has nothing to do with the Federal Reserve and everything to do with a higher cost of living as this article will outline.

The financial media as always is selective as to what information they wish to highlight because the general idea is to promote happy happy fun fun news to keep retail motivated to put every penny they have into equities and justify their existence as casino barkers.

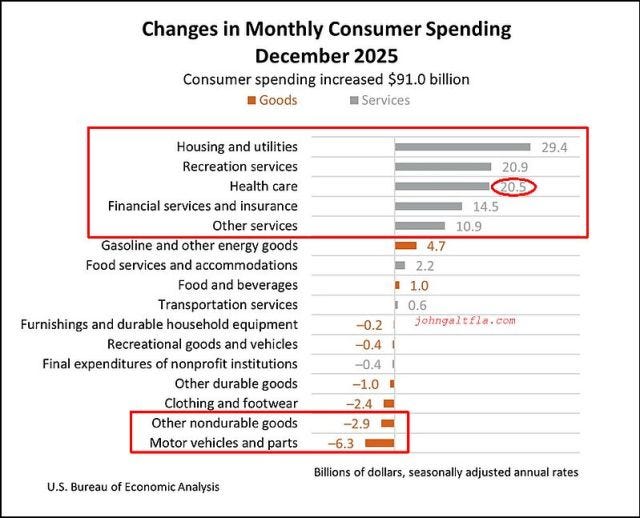

Unfortunately, another report is issued as the same time as GDP via the BEA and it was somewhat disturbing. The Personal Income and Outlays Report indicated just how dire of a condition the consumer was heading into year end. For example, this report on Changes in Monthly Consumer Spending should raise a few eyebrows.

So if consumer spending increased but most of it was spent on services, that begs several questions. For example as highlighted above, the CPI report via the BLS indicated declining health insurance and other medical costs yet somehow it’s the third highest expense for consumers?

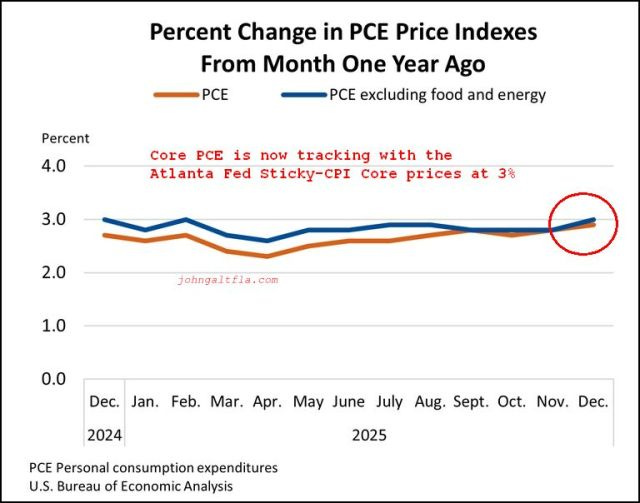

Perhaps there is a tad bit of inflation lurking out there as the PCE report highlights this morning:

This just goes to justify the FOMC standing pat on interest rates as a core rate of 3.0% that should pop a tad higher as energy and the flow through of tariff price increases hit in Q1 2026 begins to body slam the consumer even harder.

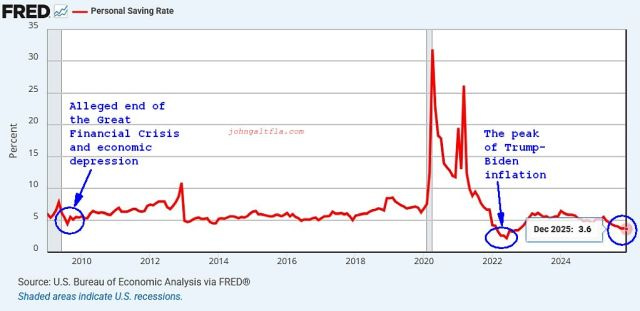

Needless to say, if everything was getting more expensive the savings rate declined again as the report demonstrates.

Ouch. And when one looks a table 2.6 line 37 it doesn’t take a rocket scientist to see the personal disposable income has been stagnant since the third quarter of last year.

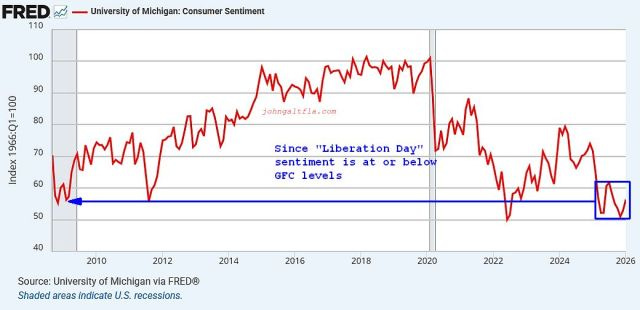

Perhaps all of these hits to the consumer have been too much leading into Christmas of 2025 and that’s what is keeping consumer sentiment in the proverbial doldrums. From today’s release of the University of Michigan consumer survey:

Maybe it’s not such a “golden age” after all since the so-called Liberation Day the American people were promised.

For more details, please refer to our Terms and Conditions.