Redeye Macro Note: Portfolio Strategy Update/Commentary, Has Interest in AI Peaked for the Cycle, Employment & Inflation Review

In this Redeye Macro Note - we discuss the latest MacroEdge Portfolio Strategy Update/Commentary, highlight interest levels in AI, discuss the January employment (faux)port, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday morning MacroEdge Readers & Community,

I hope you had a fantastic week, and you are having a fantastic start to the holiday weekend. I know that many of us won’t have Monday off - but with the holiday, it’s worth noting that the Weekly Macro Note will be shifted to Monday evening (instead of Sunday evening), to accommodate the shift in the calendar. I am continuing my multi-month MacroEdge expansion trip - and there’s a lot still in the pipeline. I have met so many great people - from Scottsdale, to Atlanta, Sioux Falls, Catalonia, and much more - and I’ve appreciated the fantastic hospitality in these places.

It certainly does seem that we’re nearing the end of the line on everyone & their grandmother offering financial advice and input - though it’s going to take a washout for that to occur. From Facebook to Instagram and even physical airport advertisements - we’re seeing financialization promoted at levels that we’ve never seen before in modern times. Forget the HELOC era of 2005-06, home panic buying of 2020-2022, and coworkers meeting up for speculative stock lunches in the late 90s during the Dotcom-era - what we have today is eclipsing all of those instances 10-fold. The absolute level of grift is reaching crazy heights - and from former hedge fund managers to high school students - everyone seems to be pursuing the pathway of *I’m an expert… trust me* - and I think we’re at or near peak grift - especially with midterms so close. This also applies to what we’ve seen in the AI/data center bubblesphere - and with new regulations, laws, and opposition kick into a slightly higher gear - I don’t think the wild west free for all that we saw in places like Abilene, Texas, for Stargate is going to continue. While data center power demand continues to surge (now consuming almost 10% of all electricity in the United States), parabolas do not usually resolve in a skybound trajectory for any extended duration. I think what we’ll see is something more like a flight path - and we’re currently still at cruising altitude… It’s going to be quite obvious once we begin the descent.

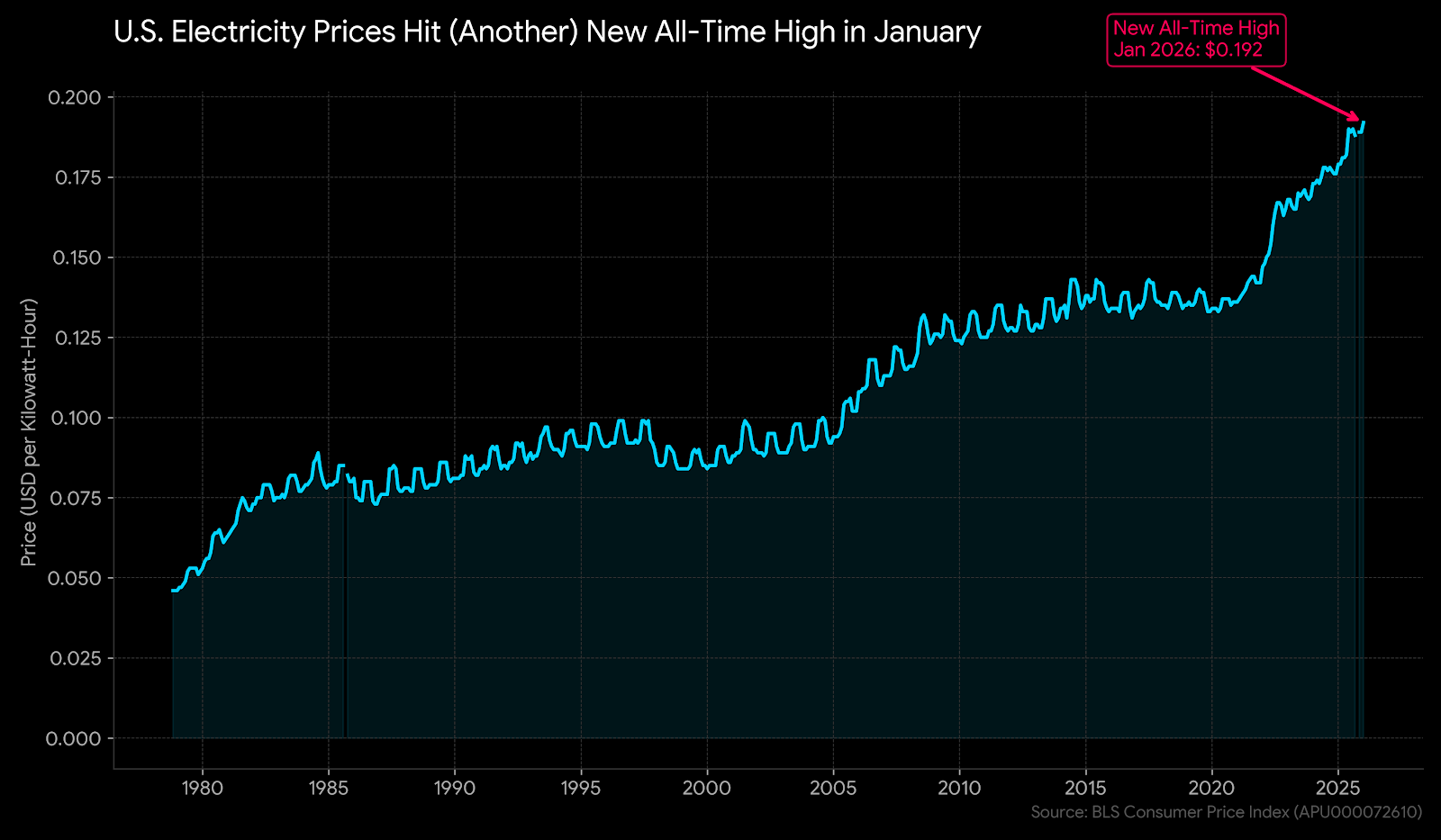

Take a look at the runaway electricity prices that many American power consumers are facing as prices hit a fresh all-time high in January:

This morning - we’re diving into:

An overview of our 2026 event schedule thoughts

Employment/inflation review

(Yet) another government shutdown

Has interest in AI peaked for the cycle?

Not a MacroEdge Ozone subscriber? Subscribe for 7-days below now exclusively through Substack:

MacroEdge Event Schedule

As part of our 2026 expansion plans, I am planning on having us host several gatherings this year around the country (and globe). Depending on where you are in the United States and/or the EU - I hope you are able to join one of these gatherings, where we’re going to have a unique opportunity to connect in person, learn from each other, build new friendships, and most fun of all, for several of the gatherings, enjoy a unique experience. Below is a general overview of what I am thinking thus far - though these won’t be finalized for the next week or so. I know that several of these dates are already pretty close, so attend what you can - and I look forward to seeing some or many of you all along the way.

April (EU - Catalonia)

April (EU - Switzerland)

May (USA - SE Florida)

Summer (USA - Chicago)

Summer (USA - Texas)

Fall (USA - Arizona)

Foundationally, these are going to be a great way for many of us to connect, and for some of you to learn more about our transformative solutions and economics suite.

Stay tuned for more to come here, as gathering space will be very limited.

Employment and Inflation Review

The employment report came in as somewhat of a *surprise* against both consensus forecast and our own forecasting. The seasonally adjusted report has become a roulette wheel of nonsense, and the non-seasonally adjusted (NSA) data was even more comical - especially in the Household survey. We noted in a viral X post the NSA data in the Household survey showing the steep drop in native born workers versus foreign born workers. While the inevitable reality over the next 25+ years is that all net employment growth in the United States will inevitably come from the foreign-born segment, this tweet sparked outrage that we didn’t know what we were talking about… the data is bad! While I (and we) could’ve told you that several years into this data disaster we’re seeing unfold, in terms of quality and accuracy. Somehow - in every single private sector measure and survey we see employment data worsening - but the BLS manages to lob out a report showing otherwise… The interesting thing over the last week is that the bond market has not really believed the hype about any sort of reacceleration…

[Continued below: January employment report synopsis, (yet) another government shutdown, has interest in AI peaked for the cycle?, margin debt growth, portfolio strategy commentary & update from Six]… don’t yet subscribe to MacroEdge Ozone - join our movement to transform & dominate the macro landscape for years to come:

While we’ll discuss the bond market more in the Weekly Macro Note - I do worry about getting sucked into another whipsaw in bonds (which has been common over the last 24 months) - where the 10Y is nearing its major support level of the past couple of years:

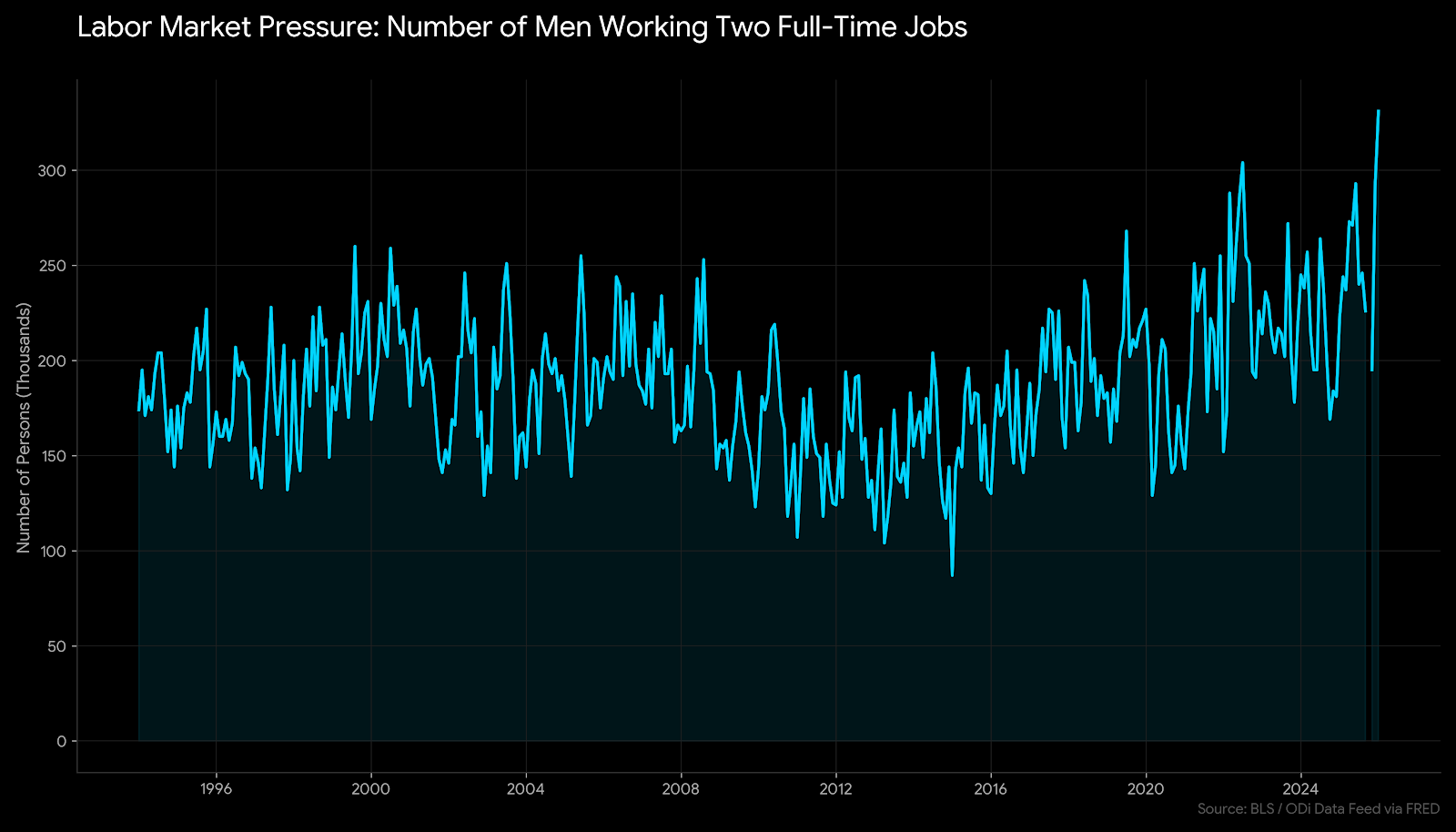

A viral chart I posted from the employment report - the number of two full-time jobholders (at least the ones that are reported) printed its second highest level on record - while the number of men working two full-time jobs hit a new high… for a perceived ‘golden age/era’ much of this is not trickling down in the lower 90% of the i in this new economic era.

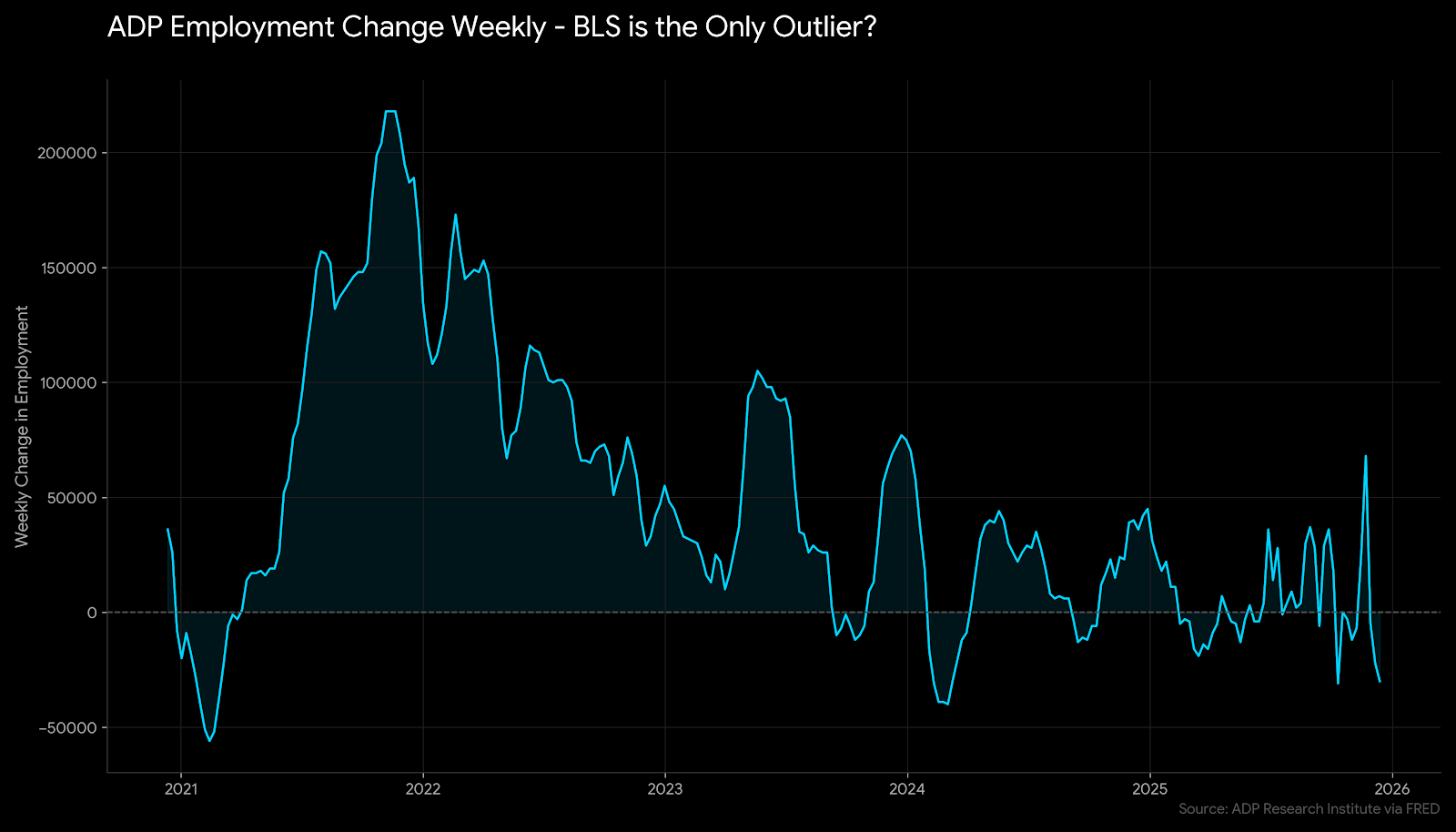

Let’s ask ourselves - why is the BLS the only outlier in over a dozen private sector data releases?

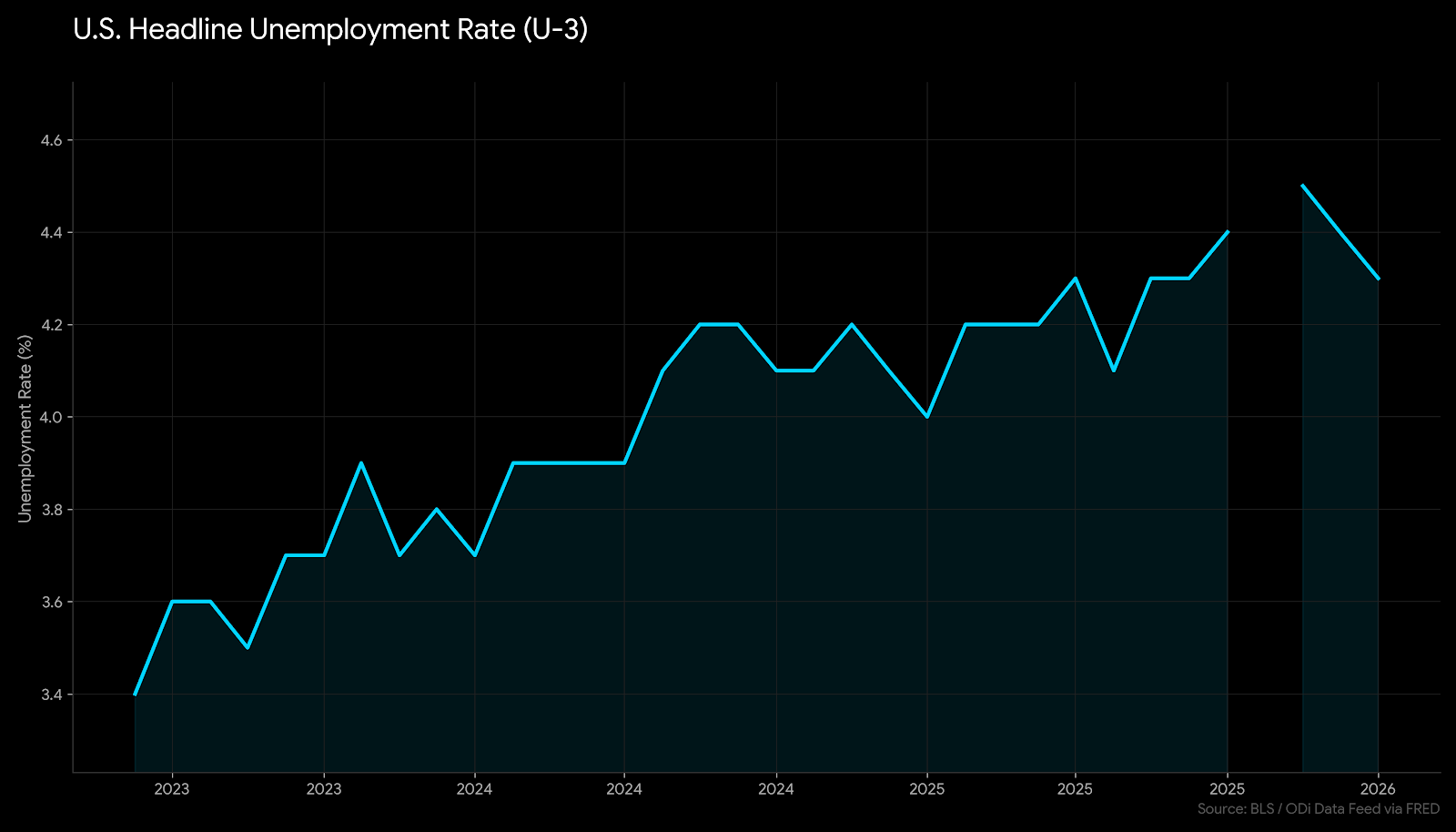

My 2C in summary - if the labor market report released by the BLS was actually factual, we wouldn’t have seen such a steep dip in yields and boost to bonds. For the time being, I’d continue to take initial reports with a grain of salt - and that goes for both inflation and employment. January is likely to see more revisions over the course of the next several months - and even though markets have seemingly ignored revisions thus far, the nearly 1 million deduction from job growth to 2024-2025 was further evidence that the employment market is a whole lot weaker than what the headline U3 rate is saying at 4.3%:

In the inflation report, which is starting to reflect some of the outlier price decelerations in things like rents, home prices (in some markets), and other consumer goods - things continue to be confusing. Fed officials have largely shifted their tone for the time being, however, and right now it looks unlikely that there will be a rate cut in March, which still falls under the Powell Chair tenure.

(Yet) Another Government Shutdown

The government shutdown that began on Saturday (yesterday) is much more limited in scope - and likely will not impact the operations of the BLS or other data agencies, which are funded through the summer right now. The more limited DHS-related shutdown is going to be a contentious one, however, and I do expect to see a rolldown of immigration enforcement into midterm elections in order to secure some kind of compromise on DHS funding. Rarely do politicians have the gall to let these shutdowns last long enough for the everyday person to feel pain from it - but given the one we saw (now a shutdown ago), we may have some limited things like TSA delays and Customs impacts at airports/ports of entry if it becomes long enough.

Has Interest in AI Peaked for the Cycle?

A question I am asked more frequently than any other of late from clients (and our readers, too) is whether or not interest has peaked in AI for the cycle. Having been to several conferences over the last few months - those who read my posts on X may recall my mention of how prevalent these AI conversations are… I really, really do not understand the hype with the current version of AI that companies are implementing at scale… and very high cost… today.

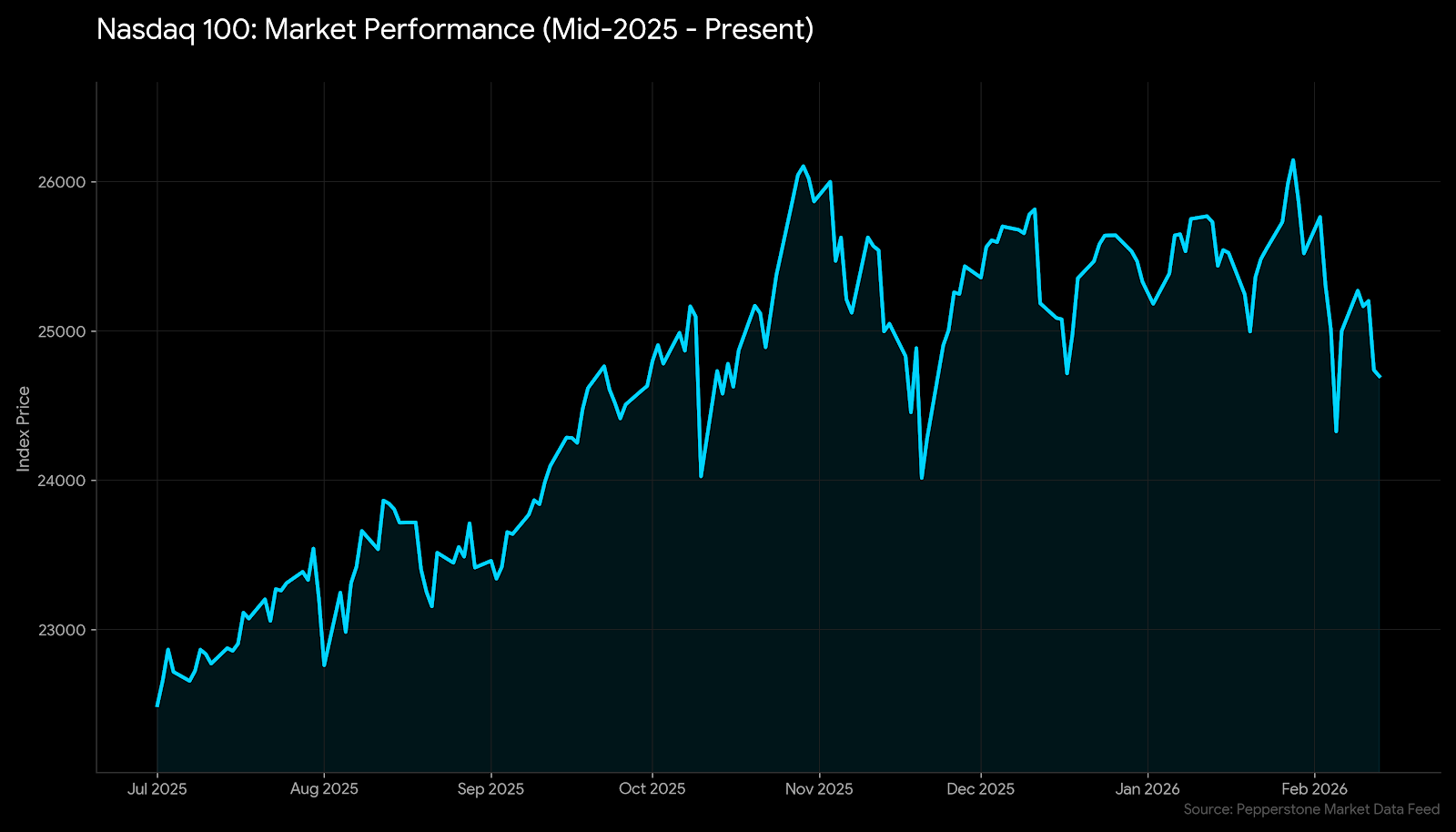

The Nasdaq itself - largely tied to Nvidia, MAGS, and (now) other hyperscalers has sat flat for about 6 months.

As discussed in several reports over the past 45 days, this pattern looks a lot more distributive (ie: Dotcom and 2022) than a constructive pattern building a base to move higher. I think that’s something to stay aware of in the coming months as things like broader data center opposition move their way into the spotlight. For the time being, the data center sector itself, and the AI (AIS) basket have remained near all-time highs - though I expect these to flag some wounded-bird syndromes in the near future as investor concerns catch on to what is the craziest investor hype of our lifetimes, largely into something that generates no ROI for firms.

VistaShares AIS / US AI basket:

The AI / Japanese & Korean trades continue to be entirely one in the same… an absolutely fascinating phenomenon:

There are other components to this all-one-trade thematic - but it’s especially relevant for the AI space.

Investors, namely CRE investors, continue to flood into datacenters as a source of profitability, and many of these later cycle entrants will be left holding… or ‘hodling’ as they might say… the bag.

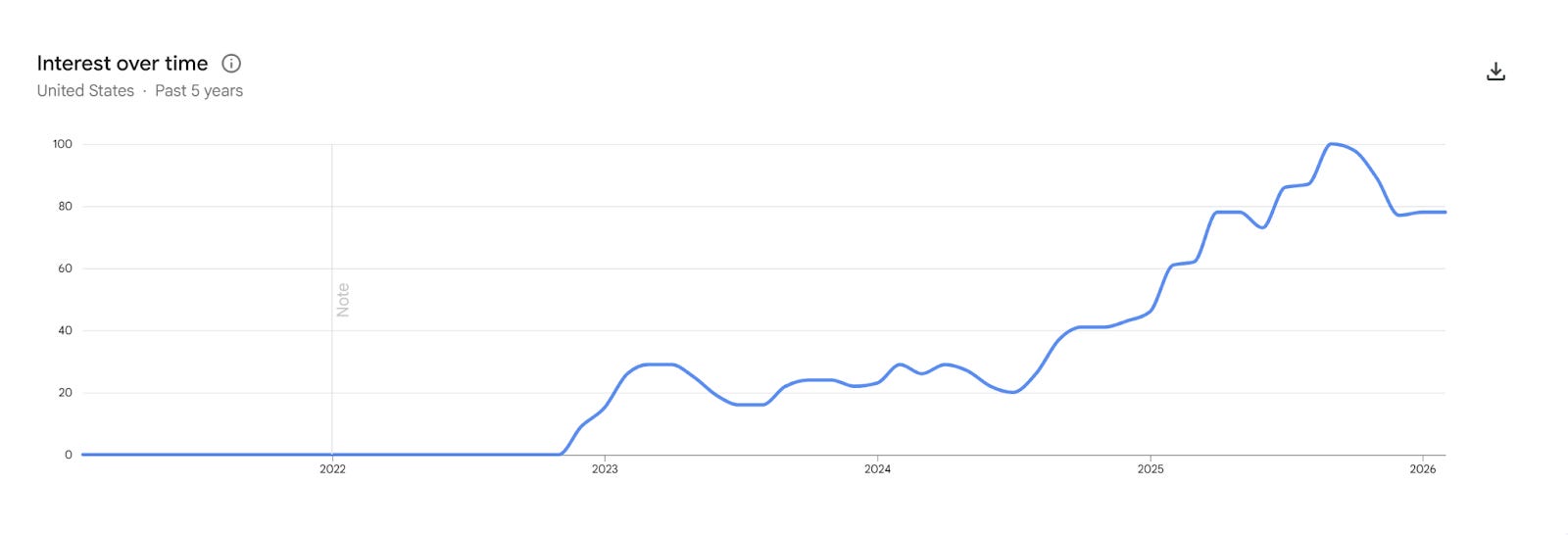

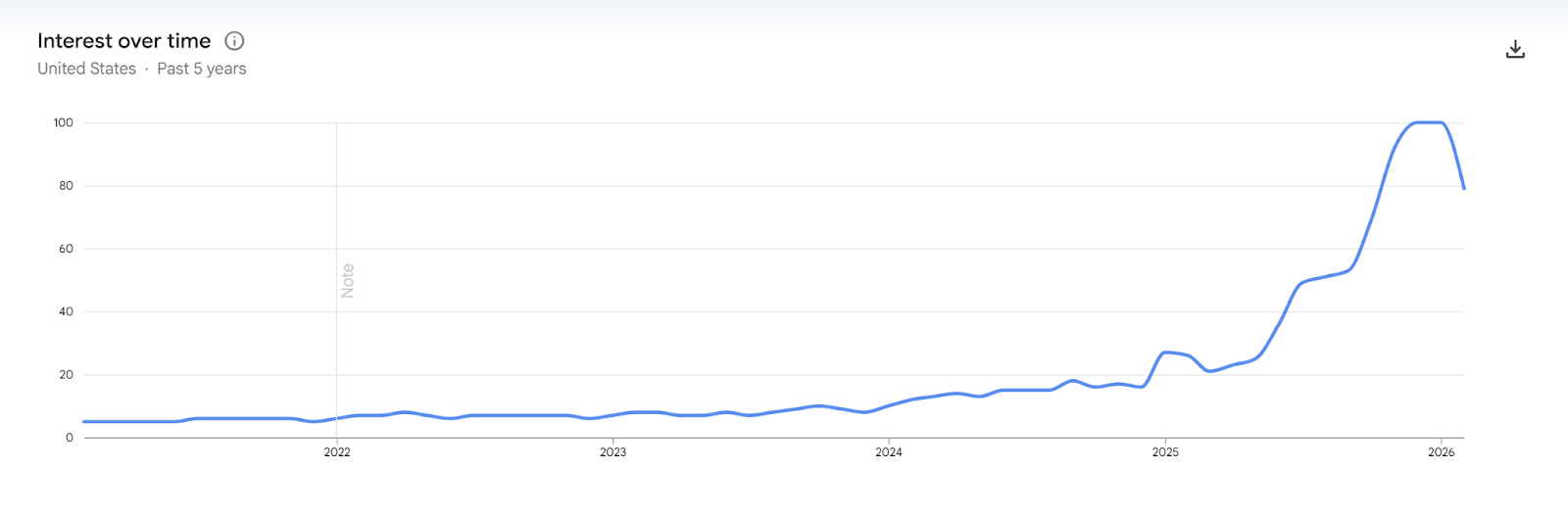

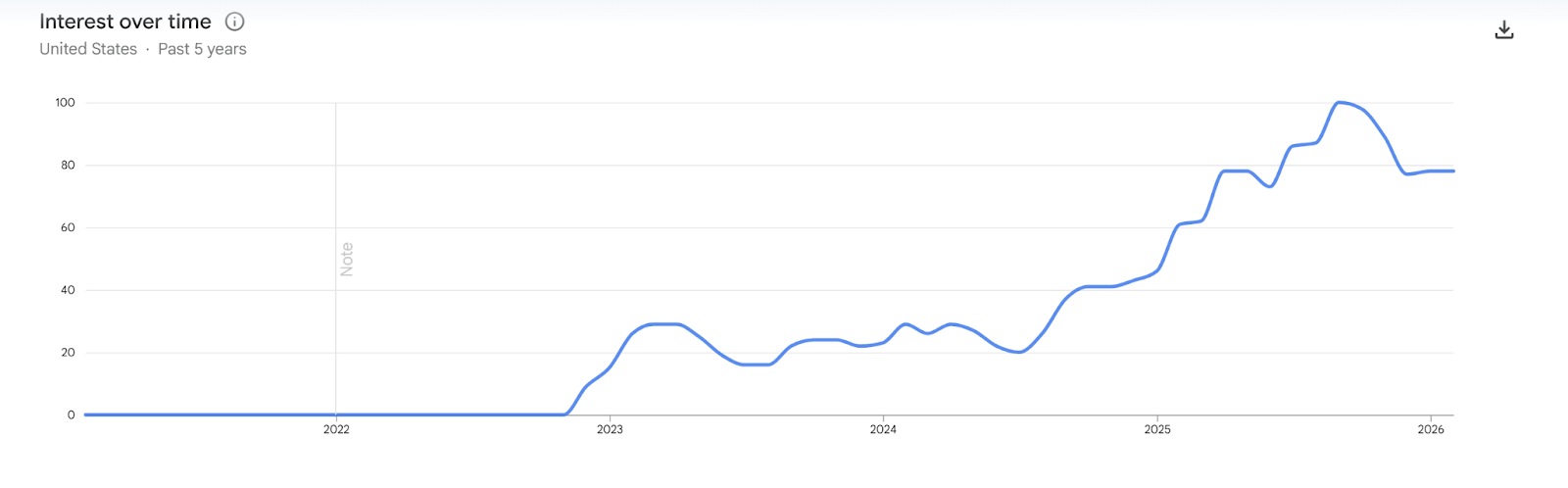

While these narrow equity sectors continue to push higher and VC/investor capital is still flowing, there are early warning signs - especially in the data center financing world. Red flags are being waved as some of the latest Nvidia games have been brought to light & regulatory risks are dead ahead into midterms. While, as I’ve noted many times, we’re very early in the regulatory and pause/moratorium/ban phase, the movement is still gaining momentum. While that is happening, we’re seeing the general public lose some interest in all of the hype:

(Google Search Trend results - 5YR basis for ‘AI’)

(Google Search Trend results - 5YR basis for ‘data center’)

(Google Search Trend results - 5YR basis for ‘ChatGPT’)

ChatGPT & AI are tracking similar search trends - and both notably peaked around the same time that the Nasdaq did, even though the more narrow bubble baskets have continued to push higher. Also note that not all ‘AI’ names have been treated equally… just recall the Oracle smashing, which now actually looks to be finding a slightly more solid footing in the mid-100 range:

Nvidia, the biggest canary of them all that continues to list at sea like a cruise ship before the full impact of the storm arrives:

The TACO-tariff rollback party of April to August/September in most equities and broader indices themselves has come to a halt - though the theme of differentiation is a strong one this year to this point.

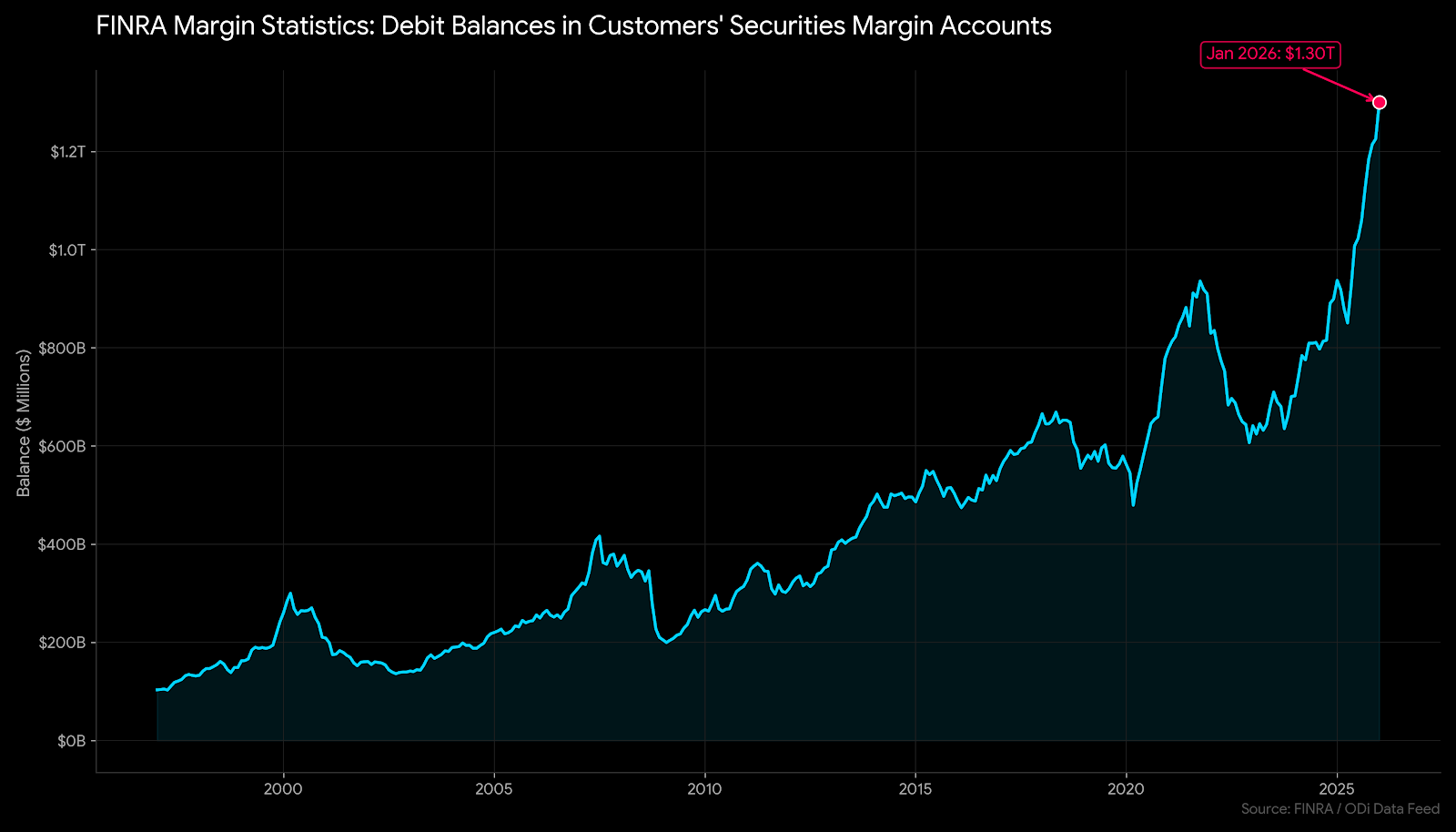

Margin Debt Growth - a Problem Even Though Wall St. Doesn’t Care

The latest data releases on the size & scope of this current boom in speculative, especially retail, trading continue to be alarming. While there are some analysts and CNBC talking heads who go on and adjust for random non-relational variables like M2, we’re in one of the great retail speculative bubbles of our time.

This single indicator is a reliable topping indicator - and even though the absolute top is not an *absolute* warning signal - past cycles are pretty clearly indicative of the usefulness of margin in predicting downside action in the broader equity markets. With the advent of new ways to gamble and speculate for everyone from restaurant waiters to those sporting the ‘broccoli’ hairstyles on TikTok, I would keep a close eye on this indicator for the entirety of 2026.

We’ve put together a very exciting Weekly Macro Note this week, which I don’t want anyone to miss. Just a secondary reminder that it will be published Monday evening in lieu of our usual Sunday evening slot, given the Monday market closure. I apologize for the shift in our deliveries for two weeks in a row, but I also want us to be including the most relevant data in each report that we are publishing to you all.

Weekly Macro Note Preview:

Additional Portfolio Strategy & Commentary

Project South Africa Revisited: The i-shaped Economy

A Look at Bonds and Yields

Stalled Technology Equities - MAGS Struggles

Delinquency Rates Near All-Time Highs (ex-mortgage)

Global Bubble Gauge is Off the Chart

Dow = 50K - Ignore All Else

Trident Update

Additionally, next week, we’ll have more forex coverage looking at the dollar, global currency pairs, and much more. Don’t forget about the cryptocurrency space too, which continues to do interesting things. Stay tuned for it all.

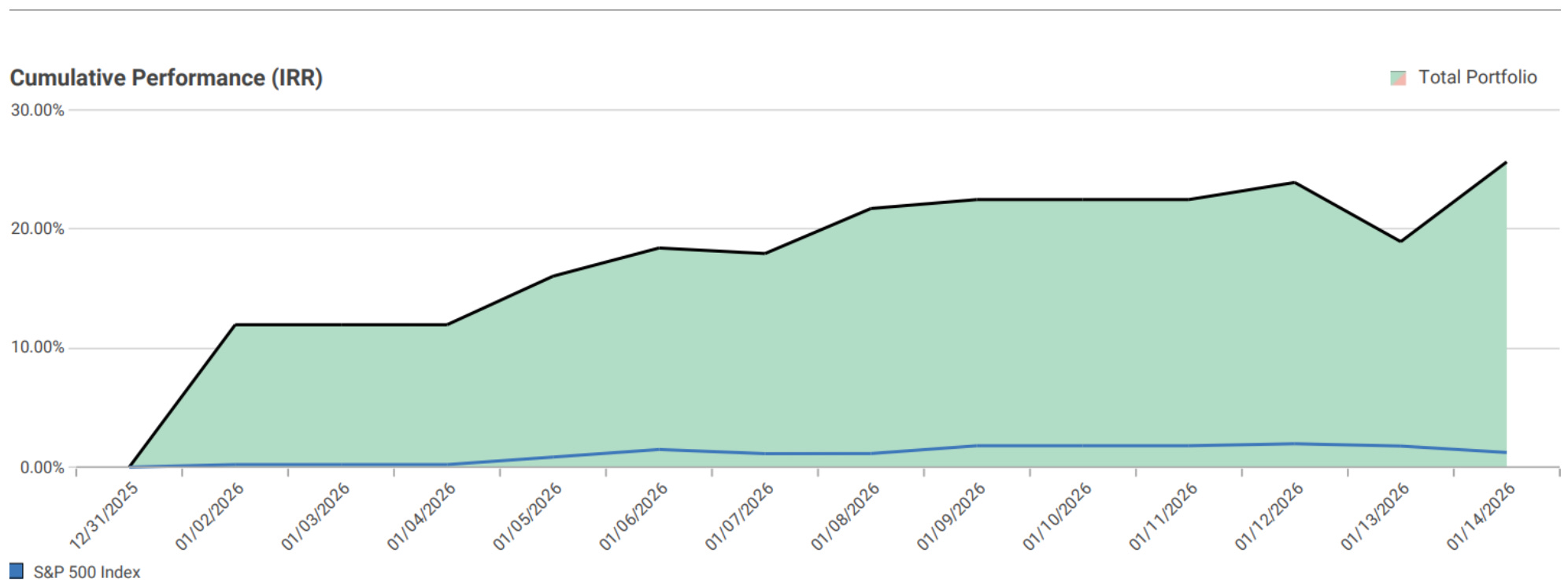

MacroEdge Portfolio Strategy Update - February 15, 2026 (@SixFinance, Head of Research)

(YTD P&L Pre-IBKR Migration)

(P&L Post-IBKR Migration)

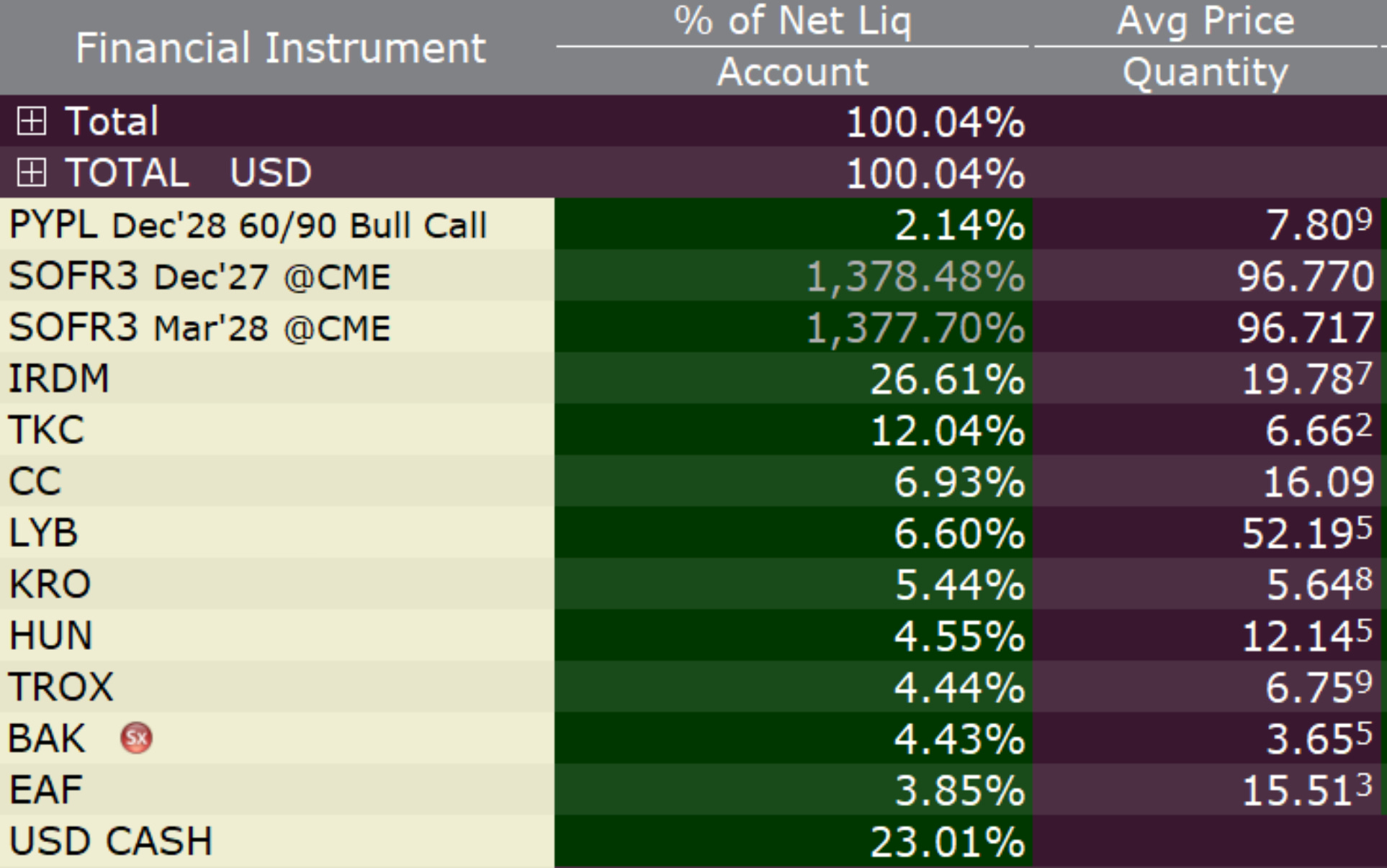

Some large changes to the portfolio were made Friday. Firstly, I exited the long in Constellation Software as it made new lows. Technically, it appeared to be a good low, but that thesis was invalidated, and I have no more desire to stick around for the price discovery. Moving on. Second, I took a large long position in SOFR futures and am positioning for a decline in interest rates. The below tweet is an error typed too quickly - I bought H8 and Z7 tenors.

After the additional purchases made following the firmer-than-expected Nonfarm Payrolls report, I have taken my position up to a 10-year equivalent of roughly 400% of NAV. After quite an extended period of not seeing any meaningful asymmetry in rates, I have now built a relatively strong view.

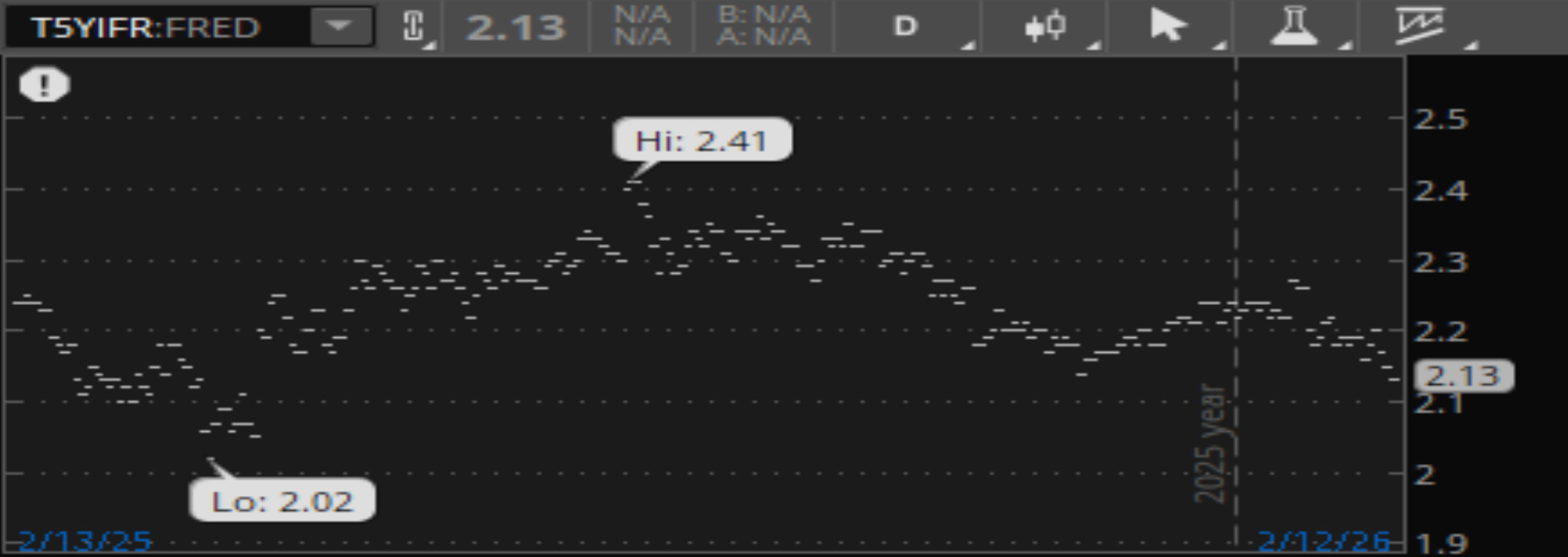

With commercial real estate delinquencies at all-time highs, student loan delinquencies surging since forbearance ended in 2025, weak retail sales, JOLTS touching new cycle lows, 5y5y forward inflation rolling over, the latest soft CPI, and the Mag 7 looking very weak on a technical basis, I am comfortable putting a large amount of risk on in the front of the curve.

(5Y5Y Forward Inflation Expectation Rate)

IRDM, now the largest equity holding in the portfolio, surged following earnings, and the repricing around the earnings lies not in the quarterly results, but in the rhetoric supplied around their future growth segments. Management effectively omitted their PNT chip (their largest potential growth segment) from all forward guidance and provided great color around how to think about the segment moving forward. Management also hinted at IRDM’s value as an acquisition target by larger industry players. I plan to hold this position as I believe the business is on the cusp of substantially inflecting later this year.

The market is increasingly shooting first and asking questions later as it comes to AI disruption risk. Some, perhaps fairly, others quite unfairly. While I do not want to catch a falling knife in a sector that historically has a high beta to SPX in a market regime where I broadly have a somewhat negative view on equity beta, I do see value in accumulating software positions with a longer-term view. Below is the view of the Oakmark fund’s portfolio manager on software. This fund has outperformed SPX since inception, and remains my favorite value manager.

This weekend, I will be outlining early positioning into capital rotations within the equity market for midterms, and the policies that may shape those capital rotations.

Have a great weekend.

For more details, please refer to our Terms and Conditions.