Redeye Macro Note: Moody's Downgrade - Does it Matter? 98 or 00, Technical Note

In this Redeye Macro Note - we explore the Moody's downgrade, comparisons to 1998 and 2000 being frequently made, and dive into the technicals as a warm-up to the Weekly Macro Note.

Good Saturday evening MacroEdge Readers and Community,

This evening we’ll focus on our Midnight Macro Note on the ratings downgrade announced after close on Friday by Moody’s – marking the last major ratings agency to shift the US debt rating from AAA to aa1 (other ratings scaled used on an agency/agency basis). The point of this discussion is not to praise Moody’s or put on a blindfold and say that the ratings shops themselves haven’t had issues over their history (especially in past financial crisis’) – but the downgrade seems obvious. While Moody’s could’ve made this adjustment late in the term of the last president, the judgment in waiting to see if the Trump Admin would follow through on its fiscal hawkishness seems quite warranted. The substantial pivot through April after the tariff debacle back to Bidenomics/Yellenomics – blowing out the deficit further, more short-term borrowing, planning tax reductions — are all contributors to why the bond market has continued to give the finger to further rate cut ideas since the cuts since July 2024. While there are many thesis out there now - around this financialization of everything shift underway since 08/09 - especially as it pertains to market involvement of both fiscal tools and the Fed.

This evening - as is standard with our Redeye Macro Notes - we’ll keep it short, and hopefully no one else joining us to read this was flying out of DFW today on AAL - since it’s been an absolute mess. Busy travel schedule ahead and looking forward to our Weekly Macro Note tomorrow with the team.

On the Sunday menu from the team:

> Vision Note

> Housing Data Review (starts, active construction, & more)

> Seeing Beyond the Tariffs

> The Left Tail and the Right Tail Visualized

> Questioning the Macro Internals

Trident & Ozone

Trident I Global Macro Fund, LP is a fundamentally driven hedge fund currently in development, focused on identifying asymmetric return opportunities across global markets. The strategy is built to capture value from macroeconomic inflection points, market dislocations, and left-tail risk events through extensive research and tactical execution. Learn more about how Trident I is being structured to deliver differentiated performance across asset classes and geographies.

This is a 506(c) offering for accredited investors only.

Access MacroEdge Ozone for two weeks below, and get all of our reports, data, and more:

Ratings Downgrade and Market Impacts

The ratings downgrade shouldn’t really be a surprise to those paying attention to the fiscal situation in the US. The shift from 09 has been one of a ‘Weimar/Zimbabweanization’ as it pertains to deficits, Keynesian policy, and pressing for yet more to protect asset prices. This isn’t just a US phenomenon - with fiscal policy makers around the globe on the same ‘protect asset prices’ agena - with Canada being another egregious example.

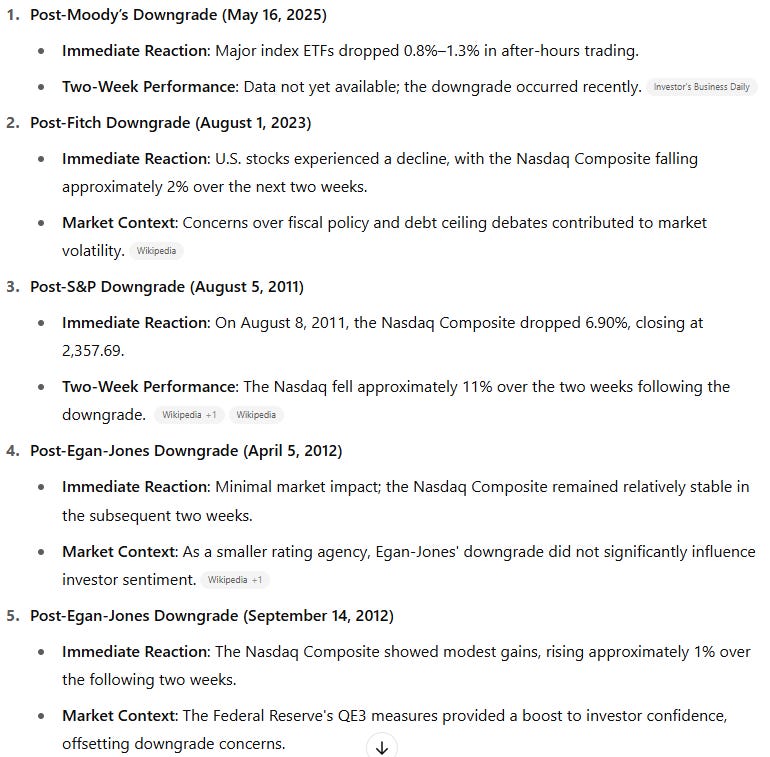

Previous ratings downgrades have been met with brief dips in equity indices - though they’ve occurred at different times. Note the last 5 downgrades of US debt:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.