Redeye Macro Note - Laws of Duality, Technicals, Metals, & Back to the Summit

In this Redeye Macro Note, we dive into equity markets around the globe, talk about technicals, metals, inflation, macro risks, and much more. #MacroEdge

Good Friday evening MacroEdge Readers and Community,

We find ourselves back again on a Friday evening meeting for a Redeye Macro Note - a series that I launched over a year ago now to write on longer overnight flights I’d find myself on traveling between the West and East Coast of the United States. Given the obvious time change between the two regions, there really wasn’t a reason to fall asleep, and with the markets opening as soon as I landed, with economic data dropping to match, I found myself writing even more. We have a new exciting development for MacroEdge this week, taking ownership interest in an aviation startup based in California blending lifestyle, technology, beautiful aircraft, & so much more. There will be a new press release available in the next several weeks highlighting our new management role in this firm. If anything, I highlight my continued thanks in the interest so many of you have in our work, in addition to the fact that we have a vision for so much more in MacroEdge. What we’re seeing now is still foundational level, and our team is tasked with continuing to turn us into a household name for as many years as it takes. When I started writing about the things I was already working on in my everyday life, I certainly didn’t think it would land me here, or in things like aviation startups, but we’ll continue growing to serve our customers around the globe. Much in store, so don’t expect me to take this weekend, or any weekend off for a very long time.

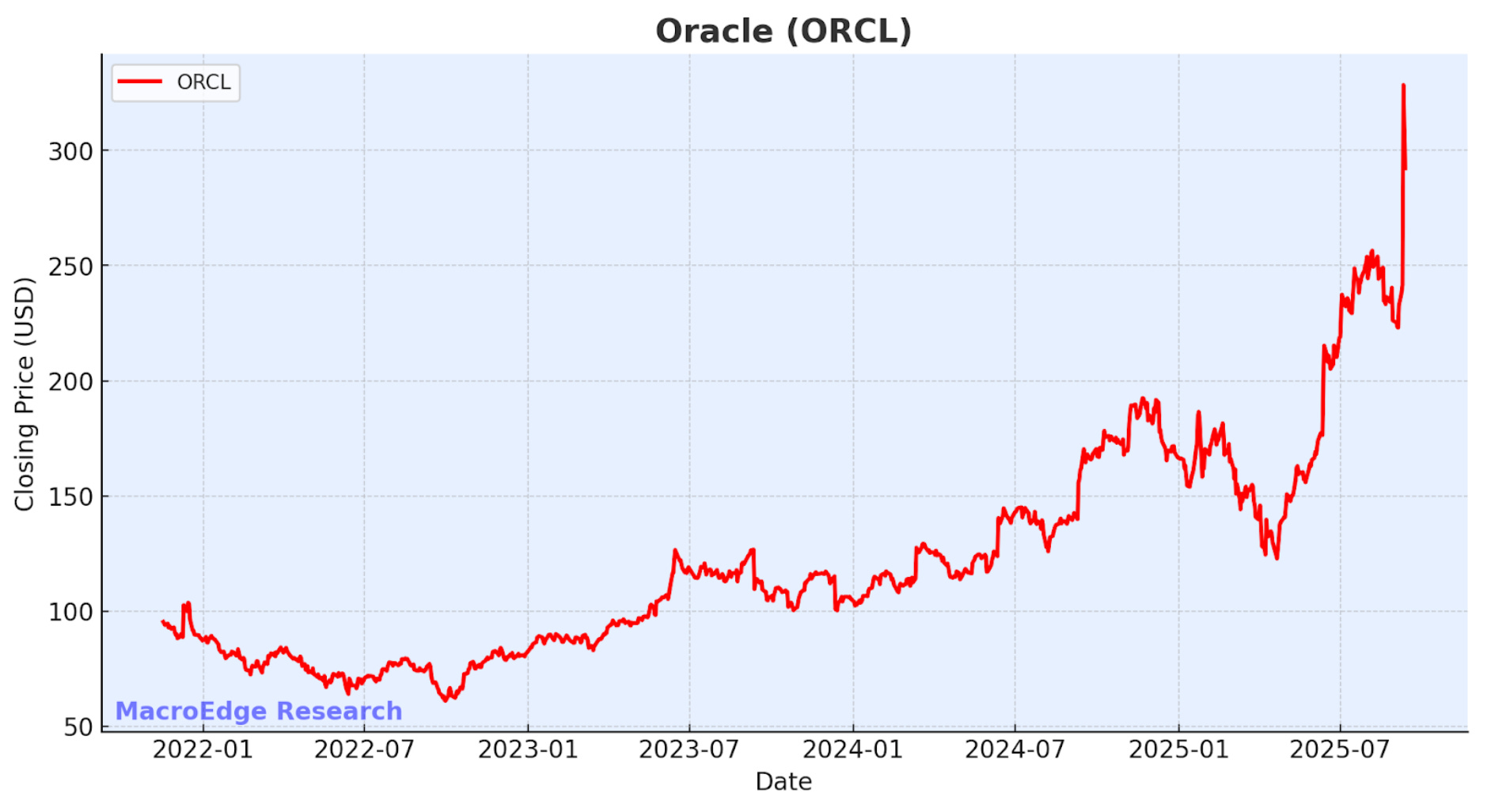

This week we saw an over 40% single-day move in Oracle on missed earnings (being EPS and revenue) - projections released for cloud rev through 2031 were absurd. We’ve talked a lot about the ERP theme, being in the space ourselves through Transform, and Ellison continues to demonstrate the value of databases… hello PLTR…

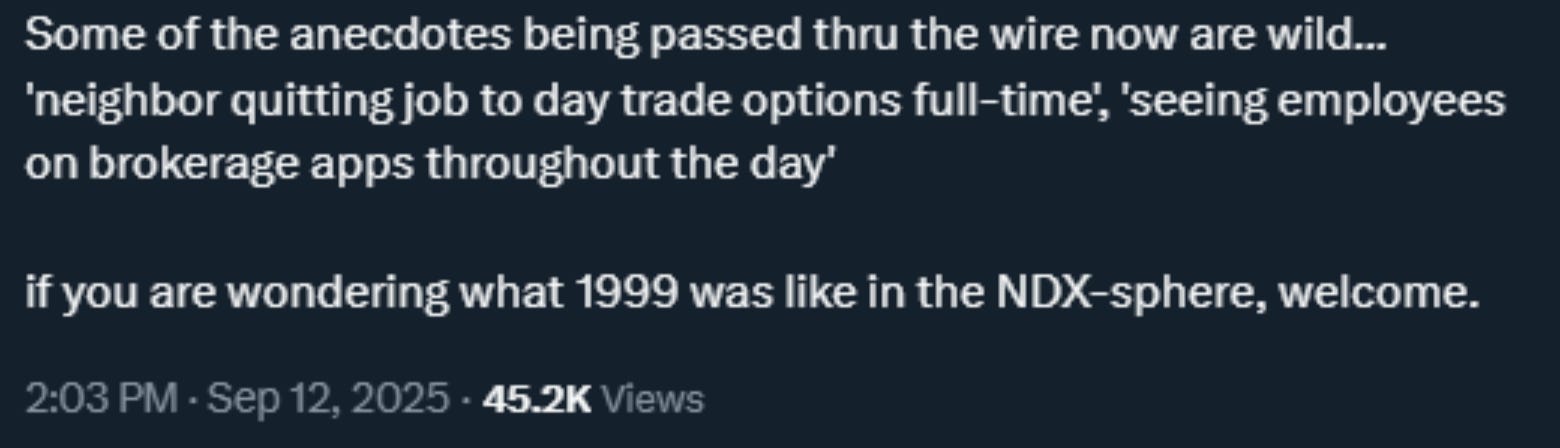

The selloff over the last two days has been largely technical and mechanical - though, as noted below, & we’re now at the technical peak of the broadening formation in NDX.

We’ve not just priced in stupidity and risk – we’re well past that point now. I noted on X earlier that for those wondering what 1999 felt like, we’ve now hit that moment. Anecdotally, daily, I am flooded with new notes from our community members - with two today being the following:

This week we’ve got an FOMC meeting, a BoJ meeting, and more that we’ll discuss in the Weekly Macro Note.

Read our Press Release on MacroEdge Institutional Research

We’re making steady progress in the development of MacroEdge Institutional Research, our new division, which arrives on October 1st. This will include a state-of-the-art client interface, the MacroEdge Institutional Research Portfolio Index (MIRP) led by @SixFinance, and our new Global Macro Strategy Portfolio will be led by yours truly.

We’ve had the concept for a proper dashboard, with MacroEdge data, as well as relevant data from around the globe to arm us for smarter decision making, for a long time - and we anticipate having a live version ready for Institutional Research members by our 10/1 launch date. Data is being integrated as we speak, along with bug workarounds, and much more to deliver a product that helps us all make better-informed decisions, and most importantly, makes us all more profitable.

Access MacroEdge Ozone for one-week:

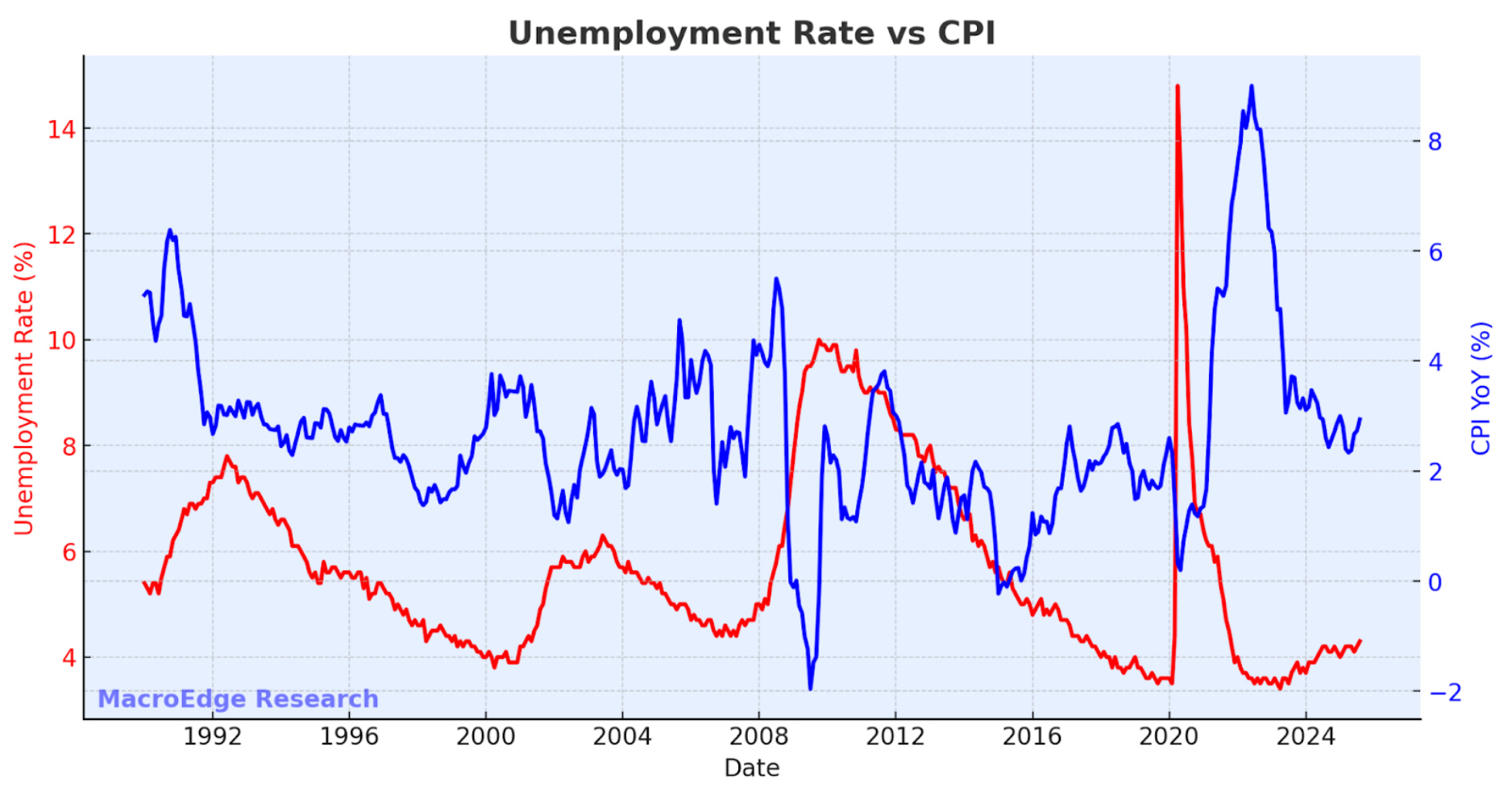

Laws of Duality - Inflation & Unemployment

The Fed carries a dual mandate - stable prices and employment. It’s failed horribly on the former - with CPI running above target now for 53 consecutive months. The hidden tax (being inflation) on everything that the everyday American doesn’t understand is a crime, and unemployment continues to make a slow late-cycle move higher.

The word supposedly is one I frequently interject now, because it seems that they care a lot, lot less about price stability than they used to. Those on the Street & on Fintwit that I frequently find myself in discussion with highlight that if we see 15% CAGRs on our portfolios, we face no issues in our own lives, it’s still not all rainbows and unicorns. One example being Tricolor this week:

Auto delinquencies, particularly among subprime, are at their worst levels since 2010.

The 10Y remains at a key inflection point:

And was saved from further pressures today with the slight selloff in bonds.

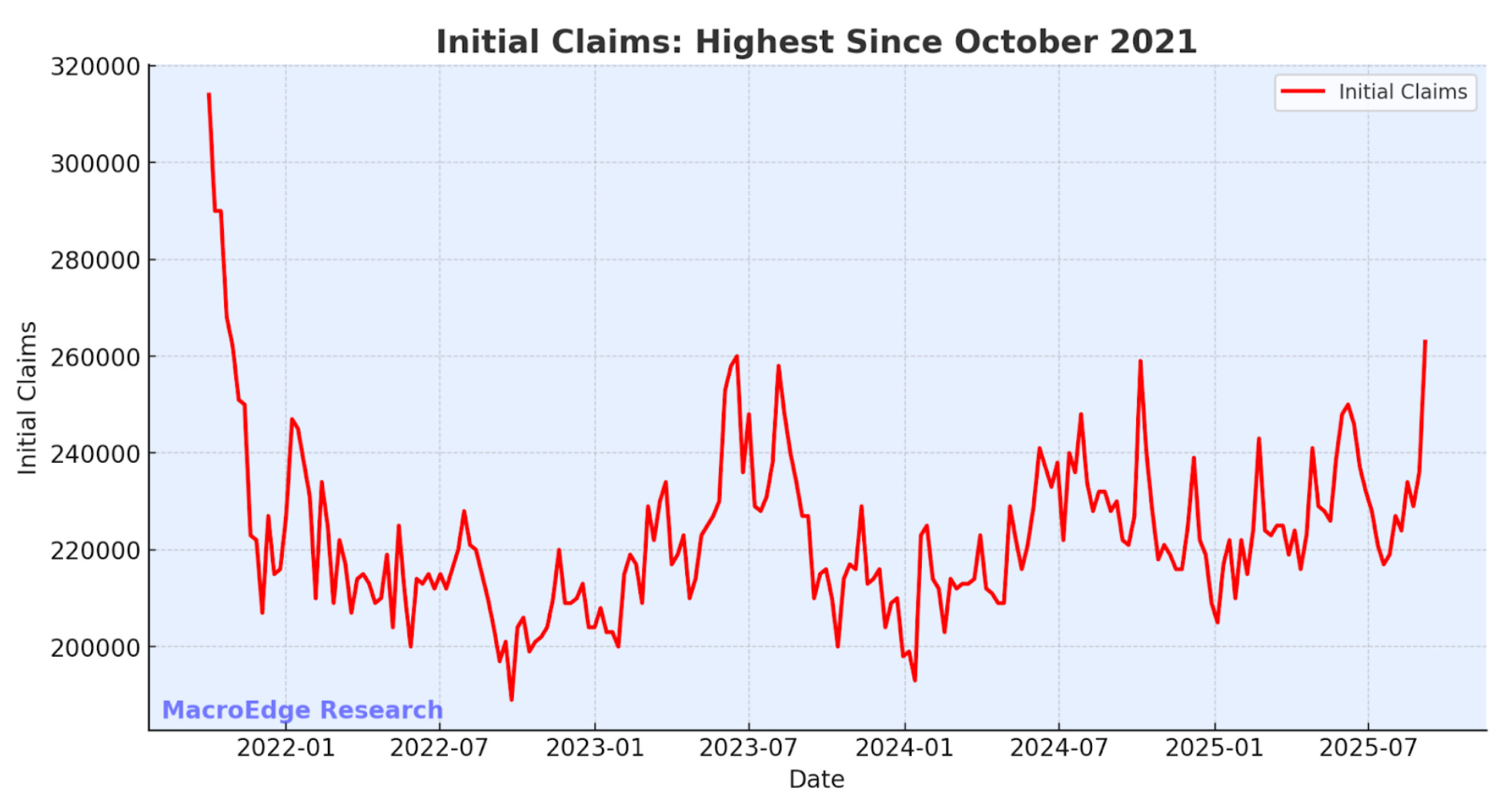

Anyone catch the ‘Initial Claims’ move this week, as MacroEdge Job Cuts tick back higher?

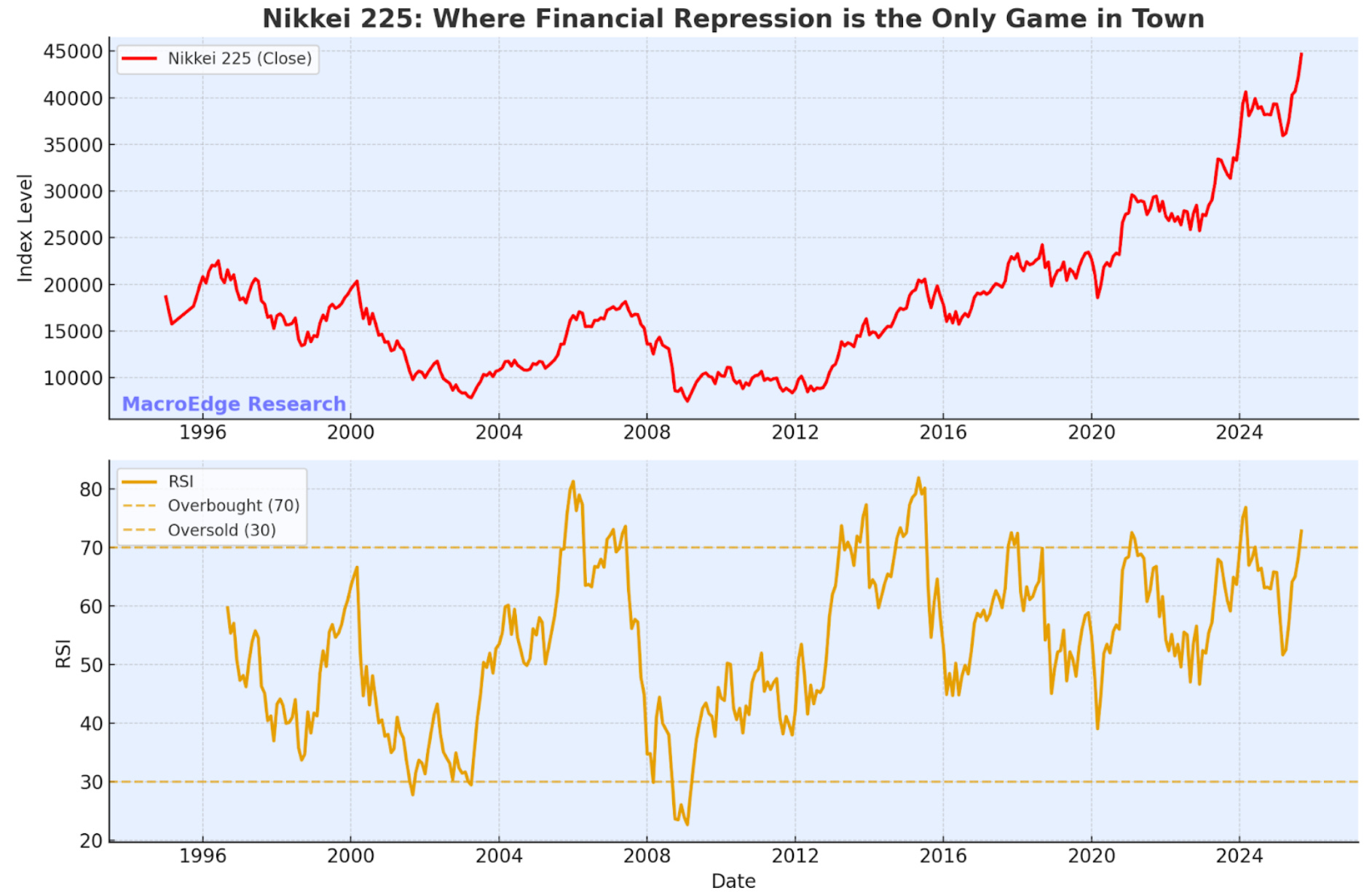

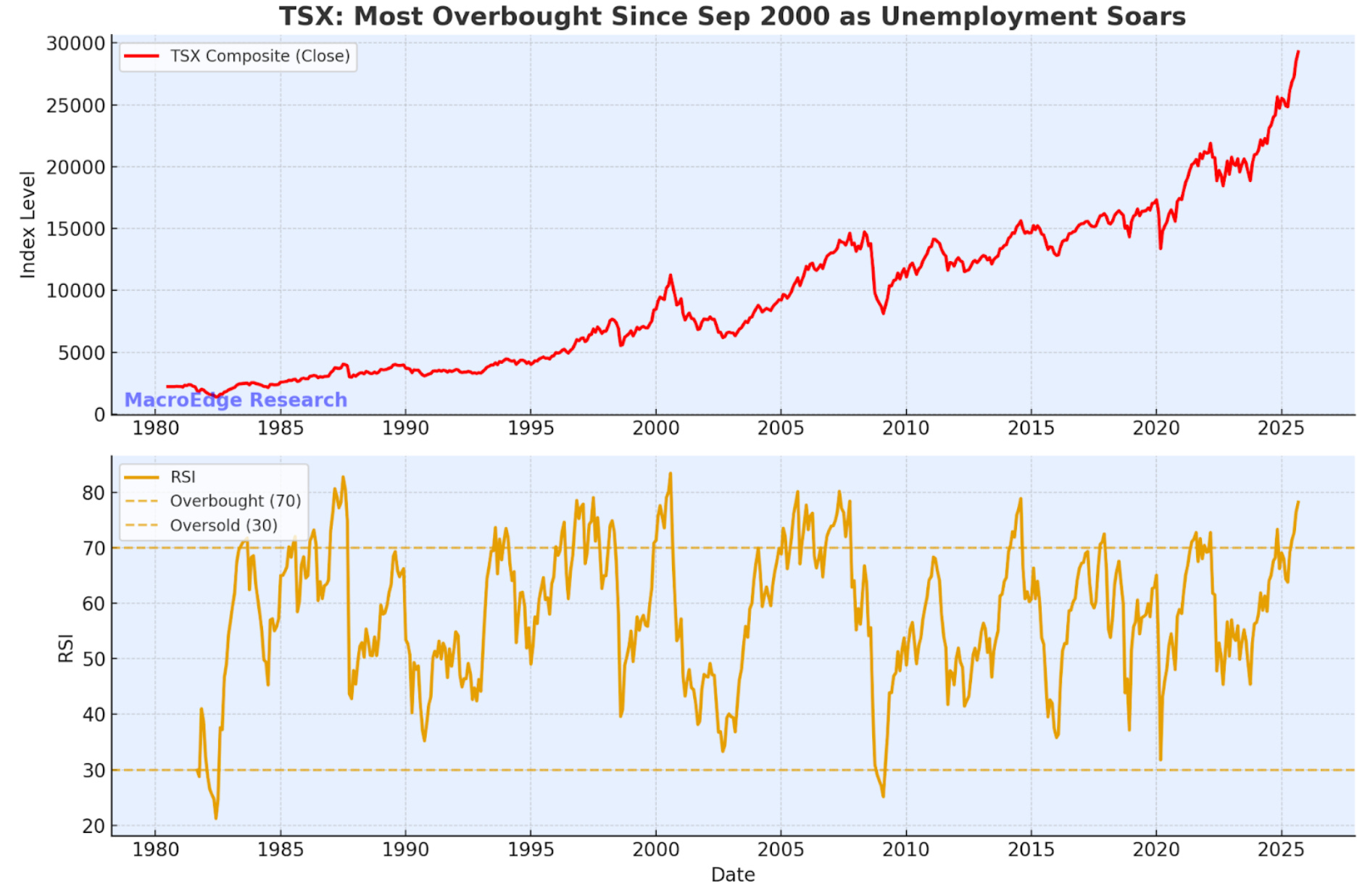

Globally - Political Leaders only Care About Equity Markets

From Canada’s TSX to the USA’s NDX, to Japan’s N225, political leaders are moving towards abandoning any concern about things like delinquencies or unemployment rates. The drug that is money printing is too attractive for both fiscal and monetary policymakers, and right now they show zero intention of stopping our current trajectory (especially relevant in Japan where they face population collapse over the next 3 decades, and are now using immigration as a temporary bandaid). In a largely homogeneous society, that is being forced by financial repression to keep their parade going for another few decades - will the net benefits be positive over the long-run?

Note the TSX, being its most overbought since Sep 2000 as unemployment soars… who cares anymore, right?

Technicals

For the Nasdaq (NDX) we’re back at the peak of the broadening formation:

Really hard to pencil any positive R:R barring a break to the upside, and then not even I can forecast what scenario might look like for inflation or asset prices (w/multiple expansion to match)

Metals

Gold continues to tell us some of the ‘real’ story:

And how about silver?

Back to the Summit

The IPO (and crypto) market today is unhinged. Companies with no profits, no durable business models, and no competitive moat are being handed valuations that defy gravity. This feels like 1999 in its frenzy, yet it looks more like late 80s Japan, when markets drifted completely away from fundamentals and became monuments to excess. Capital is chasing dreams instead of businesses, speculation instead of strategy. This is not innovation, we call it financial repression insanity. When billion-dollar valuations attach to companies that should barely register, it is clear the game has once again gone off the rails.

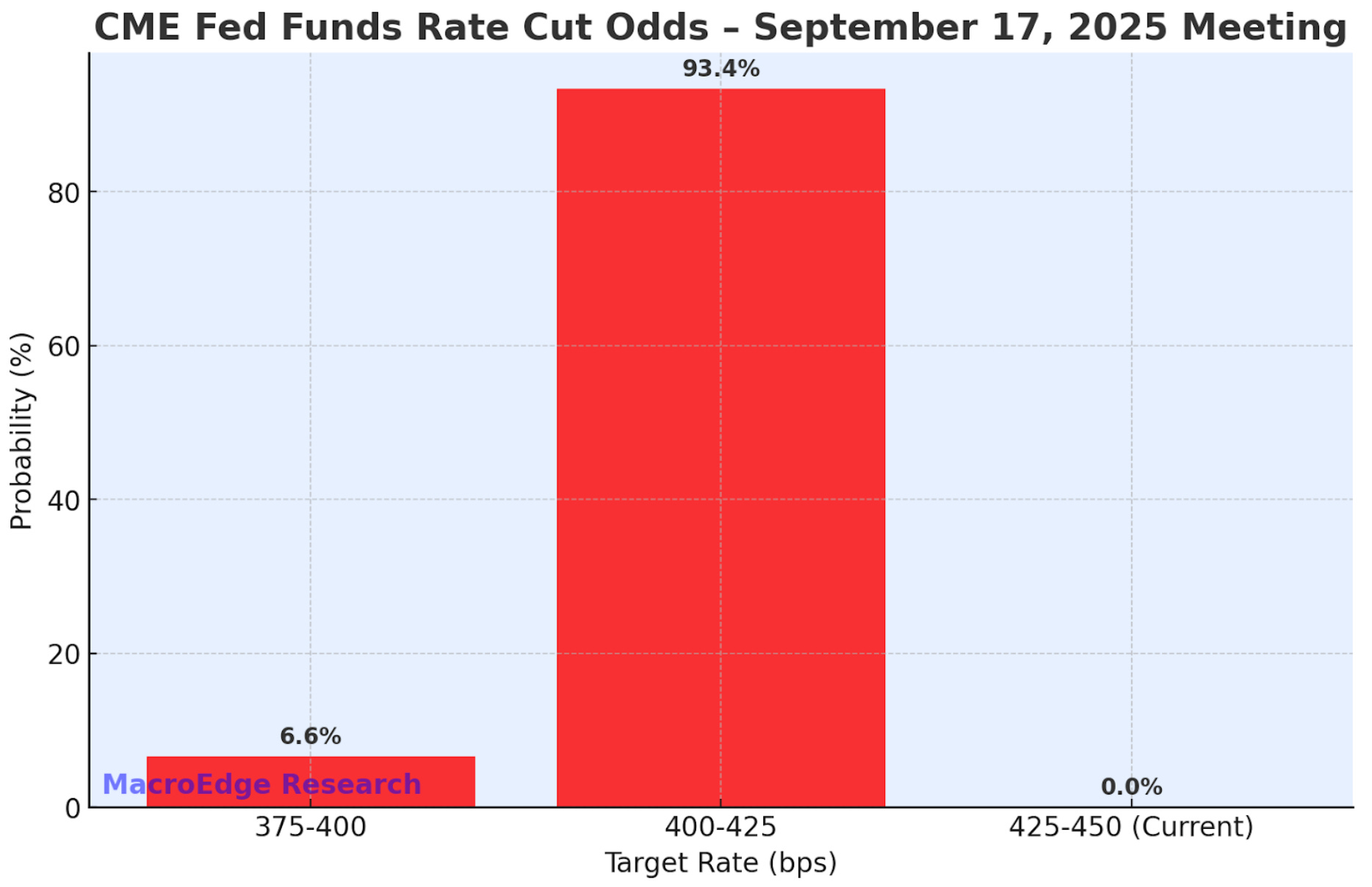

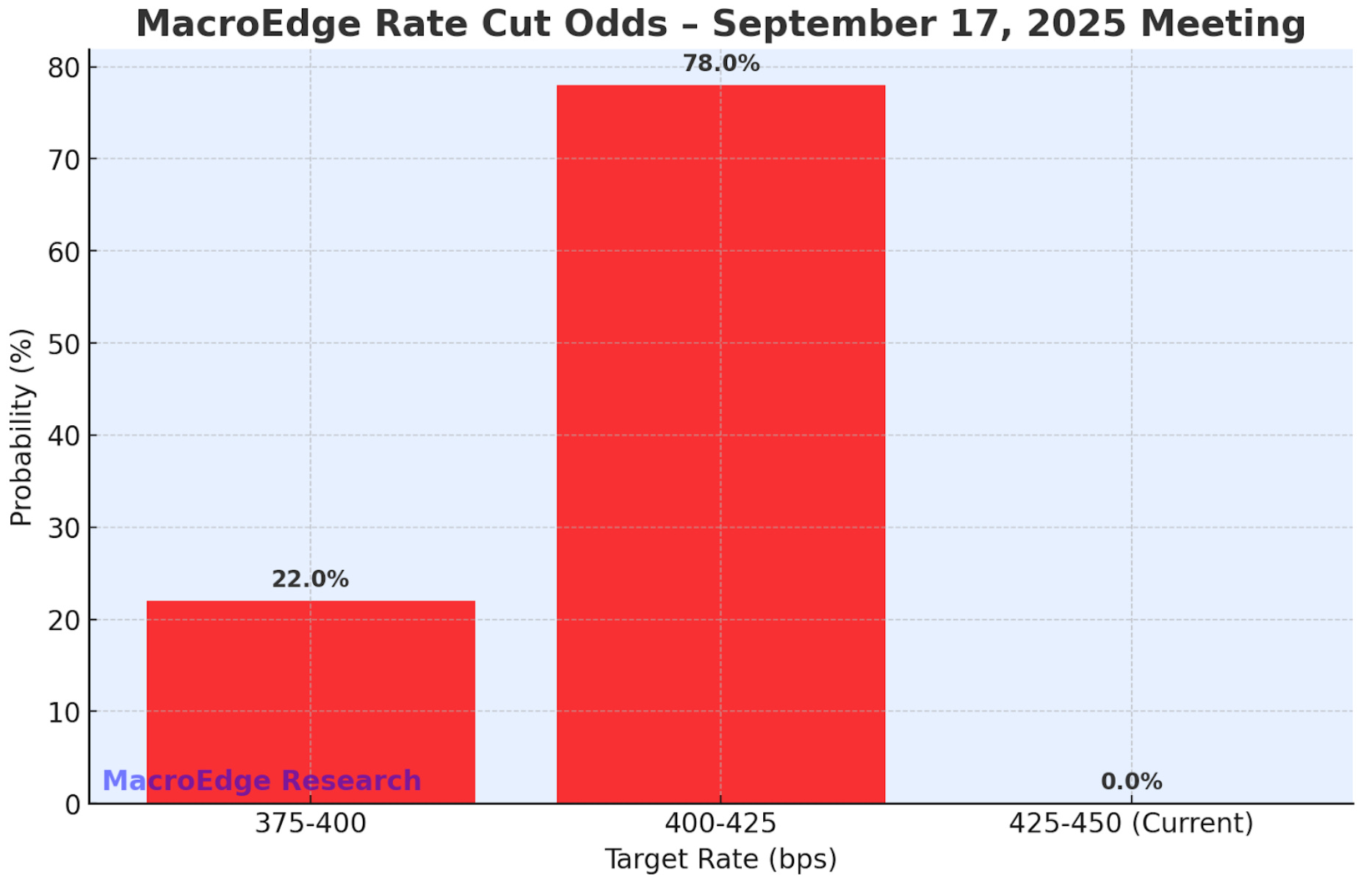

In our Weekly Macro Note on Sunday, we’ll be turning our attention back to what’s ahead as FOMC week comes into focus. While the current CME odds have about a 6% chance of a 50bp rate cut, I currently estimate odds to be around 20-25% with CEA Miran’s confirmation hearings beginning on Monday.

My odds:

See you on Sunday evening.

Don

For more details, please refer to our Terms and Conditions.