Redeye Macro Note: Inflation Genie, Real Estate Situation + Homebuilders, Rising Bank Stress

In this Redeye Macro Note we discuss the inflation genie, continued softness in the residential real estate market, homebuilders, rising bank stress, and more. Redeye. For those seeking more.

Good Saturday evening MacroEdge Readers & Community,

This evening we’ll have a thought-provoking look at three main topics: the inflation genie, real estate situation (w/homebuilders included), and discuss potential rising bank stress that we’re seeing in some of the data. As the ‘tactically bearish macro, tactically bullish equities’ regime has continued - there’s continued crosscurrents across the board as the new paradigm growth in things like the ‘AI trade’ have continued. One thing that surprises me about the AI sector is how much government support and backing they’re receiving under this current administration, and it’s concerning the degree they’re willing to grow the bubble to a point that equities rise every day. On Thursday after market close, Trump & Bessent both noted in comments that they could get equity markets back on the right course after a roughly 2% drawdown, as we’re nearing the 2000-peak in terms of valuations.

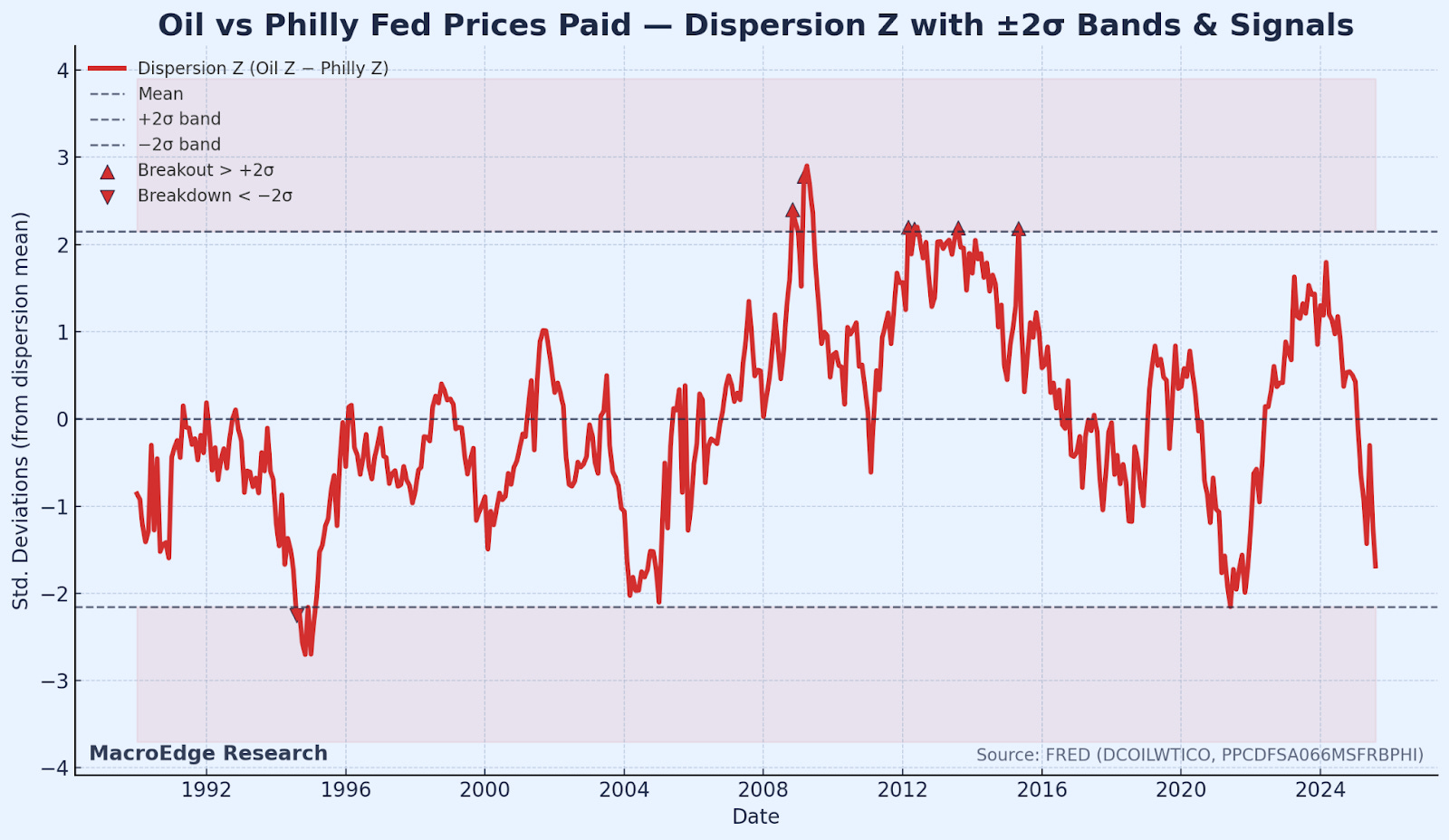

On the inflation issue, on Friday we got the latest PCE reading (2.9% y/y) as was noted by Powell earlier in the week on Tuesday, and leading prices paid indicators continue to signal accelerated price pressures. Commodities, metals, and again (oil) all ticked higher this week, with metals leading the charge. It appears that oil rallies will attempt to be capped to a degree under the more-centrally planned economy that we’re seeing today, though upside risks remain if the market tightens into the winter. One of the themes of our next Institutional Report related to energy and uncovering the opportunities in the sector, especially with the crisis emerging from the data center boom being in power and energy costs…

On Friday - we had a fantastic MacroEdge Radio, which you can catch on our YouTube or Apple Podcasts, below:

Sunday we’ll discuss the global bubble in the AI names, opportunities, and set up the theme for our next Institutional Report next week, something you won’t want to miss.

Institutional Research Live in a Week

MacroEdge Institutional Research will be live in just under a week, and the third edition of our Monthly Institutional Report will be out next Saturday. All MacroEdge community members will have a chance to access MacroEdge Institutional Research for 4 weeks, starting on October 1st, or for the month of October, depending on when you submit your email. You can signup for access below by completing the form on our Institutional Research page:

Included in Institutional Research:

Actionable Portfolio Strategies & 3-12 Month Trend

2 Live MacroEdge Portfolio Strategies

MacroEdge Dashboard Access

Two/Three Weekly Ozone Reports

Monthly Institutional Reports

Intra-week Institutional Macro Notes

Redefining What We Are

At the forefront of our growth is a clear cut view and vision of what we’re doing. We’ve consolidated our team back into two primary divisions: Macro Research & Transform, to streamline understanding of our transformative solutions - from financial services, economic intelligence, business transformation, and much more.

Under Institutional Research

Institutional Macro Research

Ozone

Under Transform

Data and Analytics – Data Warehousing, Management, Oversight

ERP System Development and Integration

Economic Advisory

Bespoke Innovation/VC Work

Sales and Marketing Intelligence

Learn more about Transform below:

We’ll be expanding our team again come the end of the year and in Q1, as growth continues to enable further growth, under both of our divisions listed above.

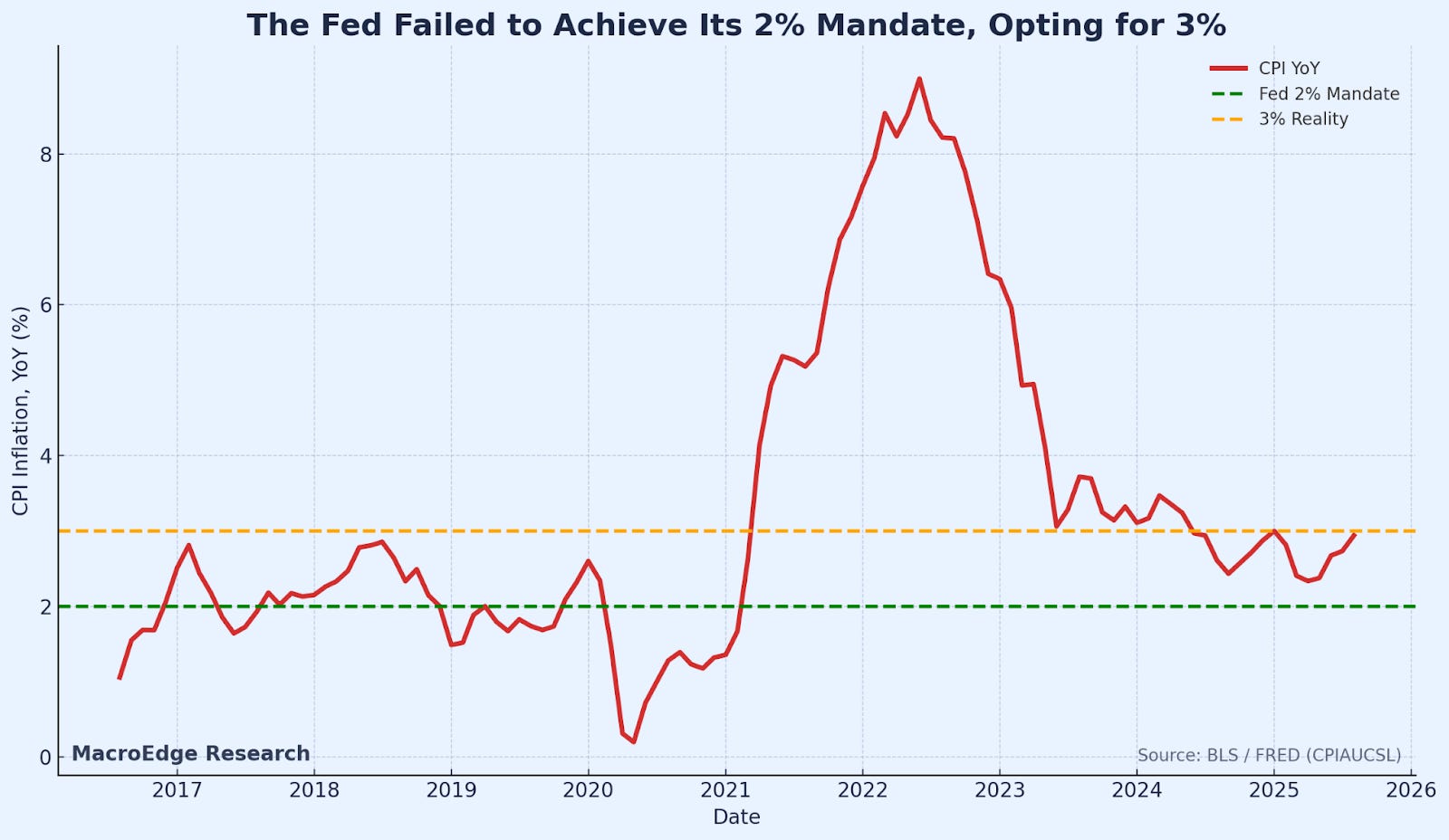

Inflation Genie

The PCE reading confirmed what Powell already informed us of earlier in the week - a PCE of 2.9% Y/Y - that does not mean inflation is defeated, we’re rather at a slower pace of price level acceleration. If the unemployment data does not cool through the end of the year - and the 2Y moves higher - we will be scratching our heads again questioning why the Fed is cutting rates. Especially if asset price melt-up enablement AND support continues - the recipe for a reacceleration in inflation - especially as M2 rises and if oil joins the party - is very real. Even with property price decelerations and outright declines - the Fed has still failed to get anywhere close to its 2% mandate, and appears to have set more of a shadow 2.8% mandate for the time being, as they refuse to break the labor market with accommodative policy. If the Miran / Trump crew have their way - it’s going to be very interesting to see how things develop for employment.

Risks are much higher as the Fed failed to achieve (and some may even say target) their 2% mandate effectively:

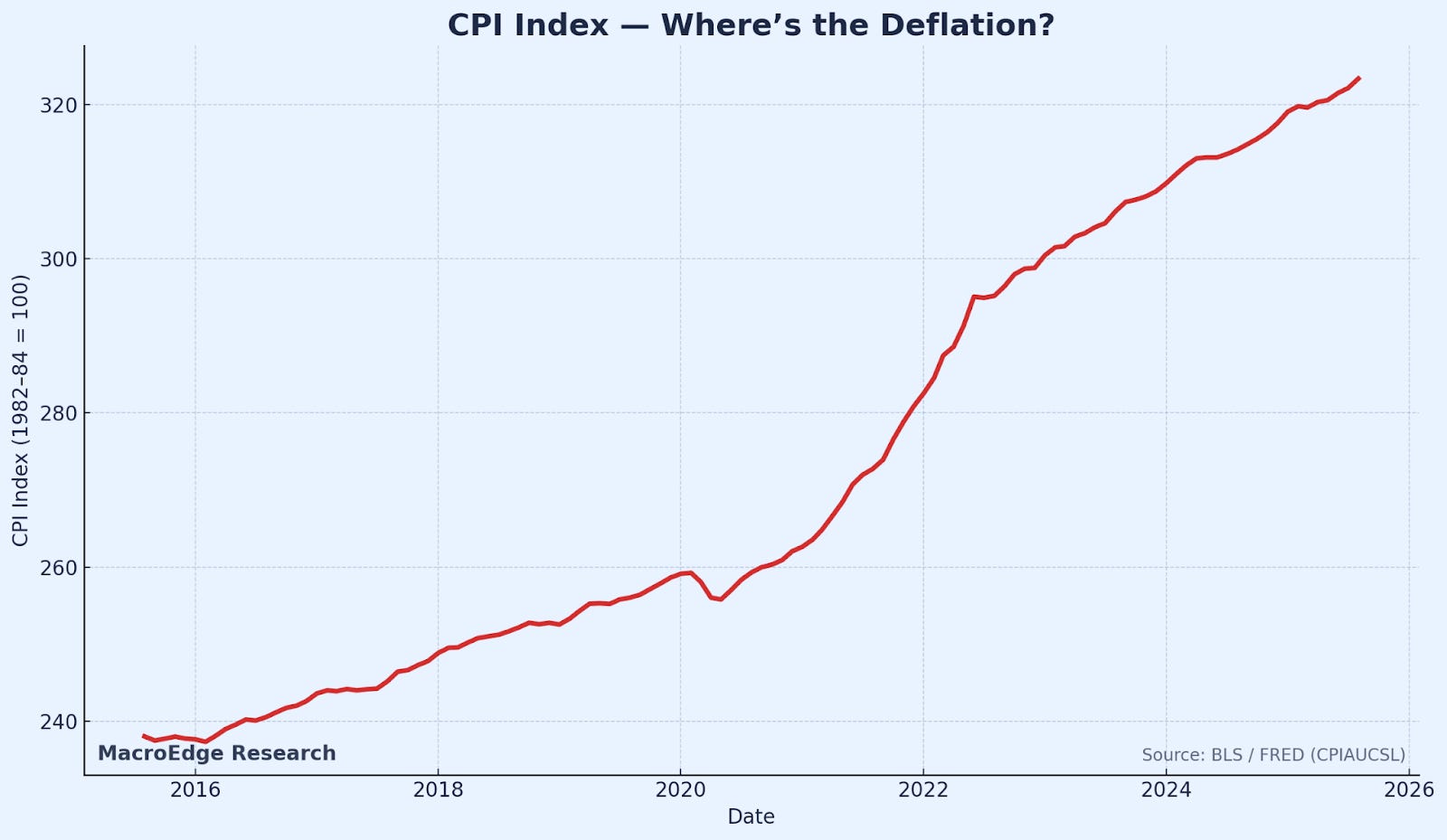

Where’s the Deflation?

Risks for energy (namely oil prices, remain directionally higher, barring global demand shock):

Real Estate Situation + Homebuilders

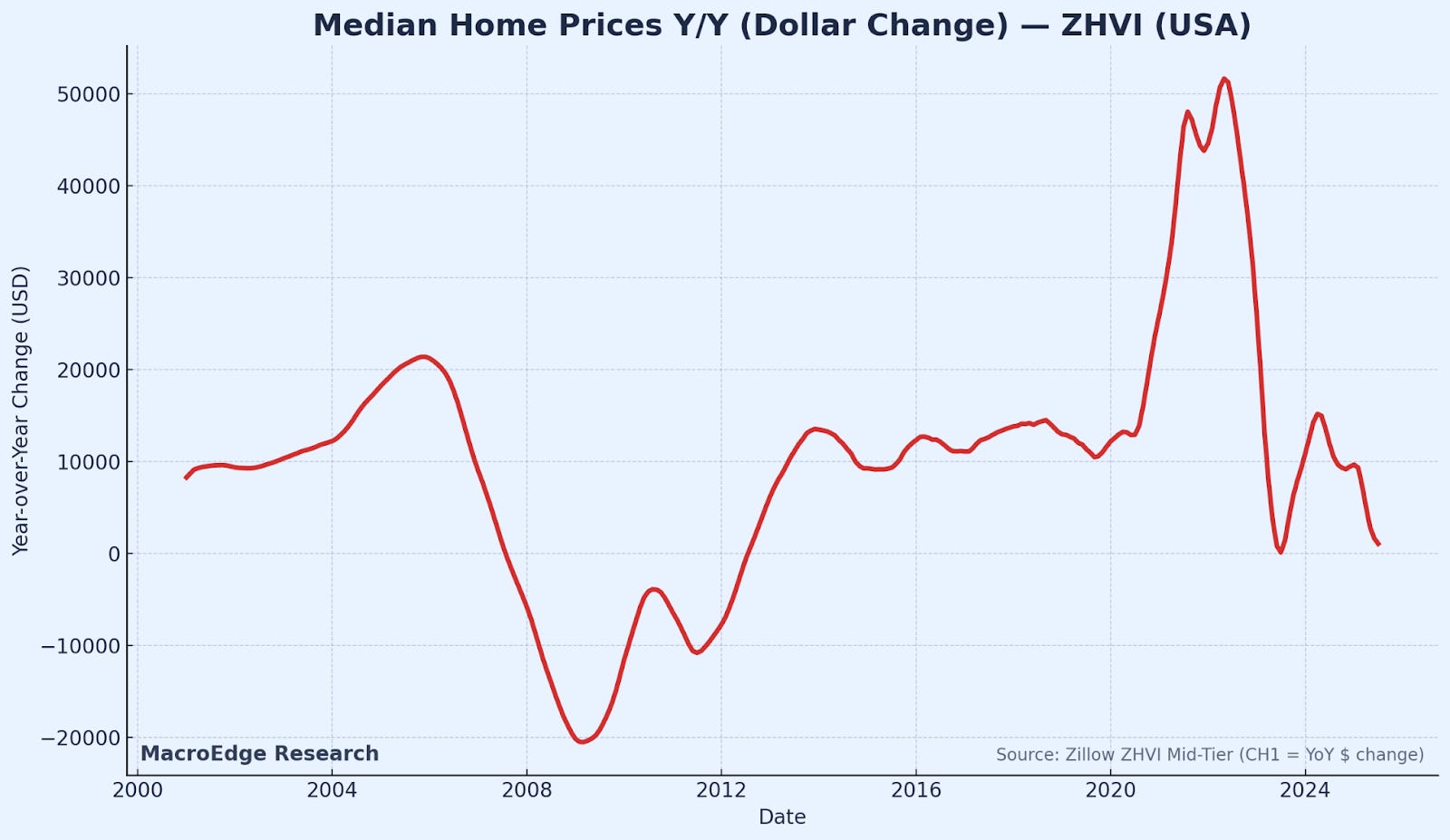

For real estate - home prices have continued to decelerate over the summer - and this has broadened out across the country, in both nominal and real terms. I often reinforce the fact that most American homeowners fail to understand the concept of ‘nominal’ v ‘real’ when we’re referring to price levels, thus I like to show both.

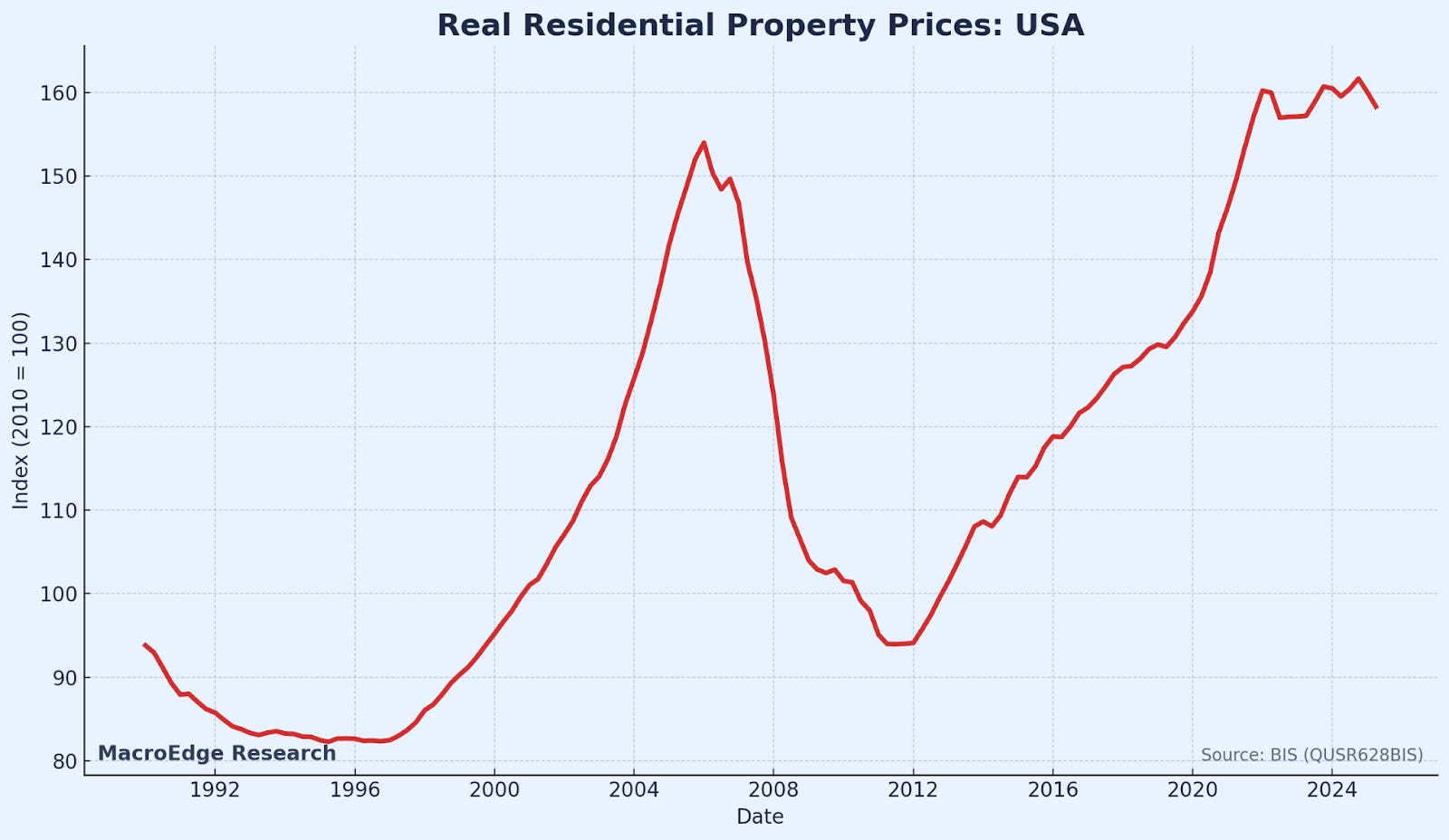

Nominal Home Price - Median (ZHVI) & Real Home Price (Quarterly - BIS)

BIS Real Home Prices

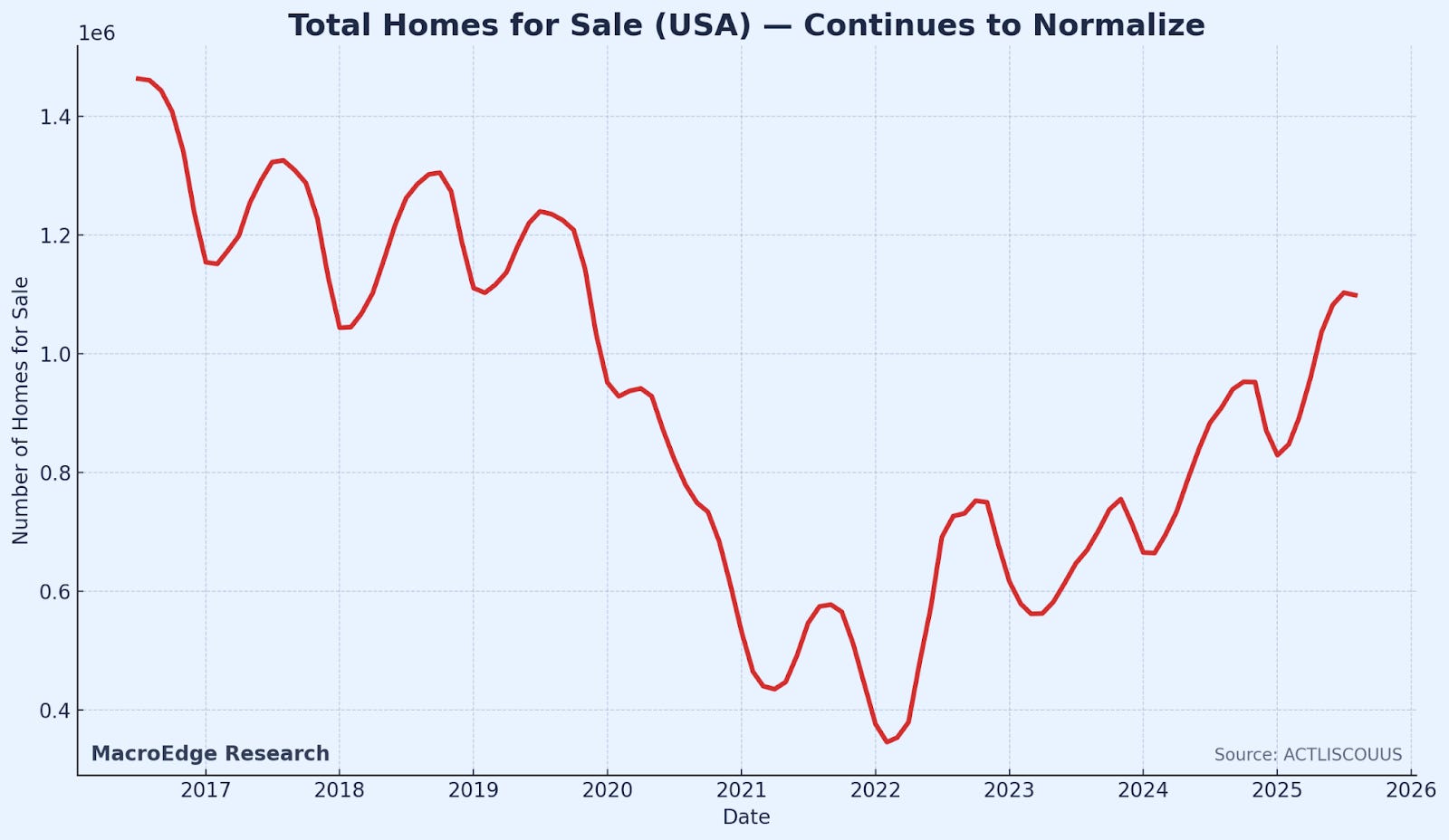

Inventory Continues to Normalize

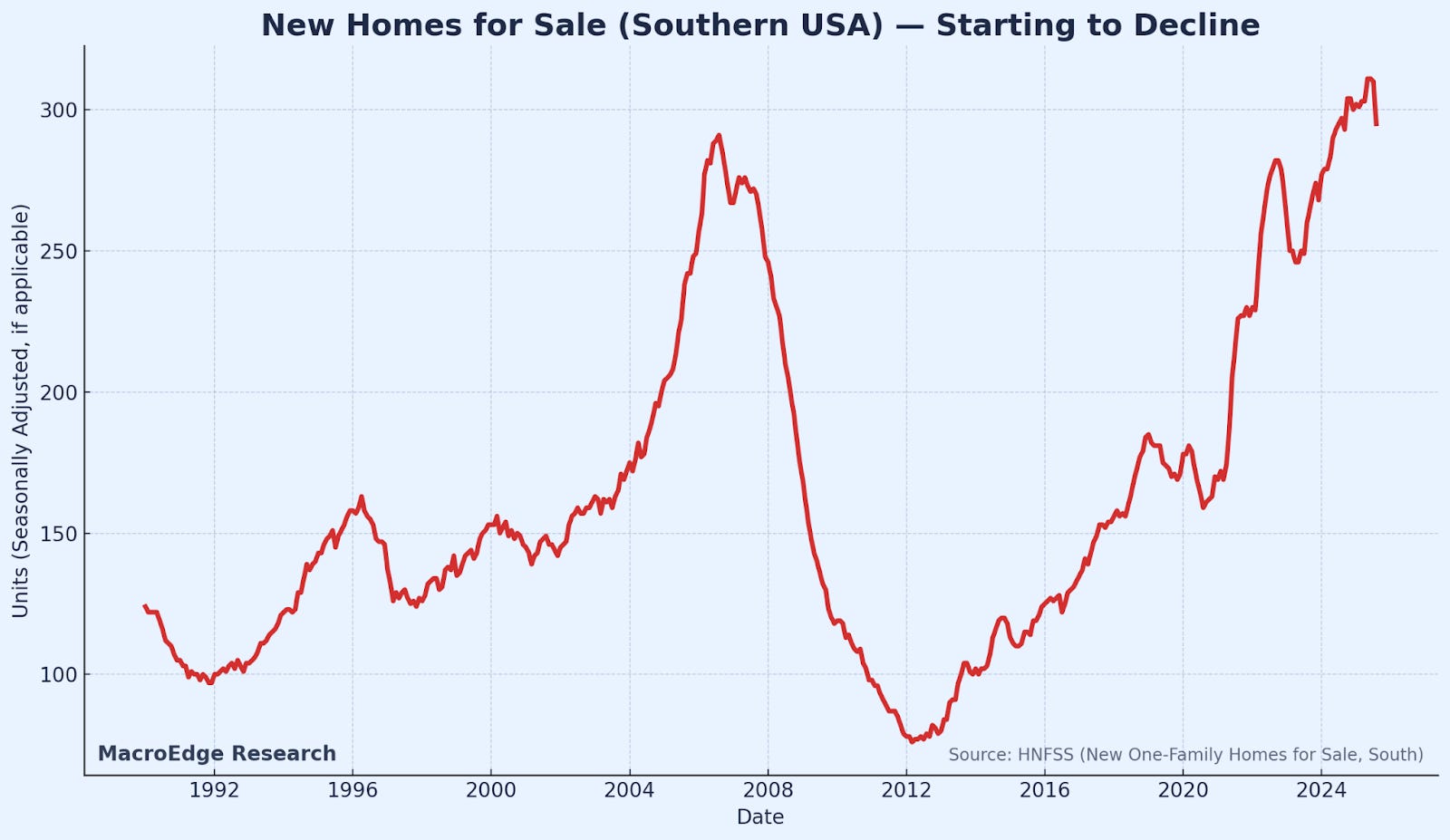

New Inventory in the South

Inventory in the South on the new side has likely peaked for the cycle - especially based on permit activity. This will impact employment, most notably, and builders earnings, as well, if they’re moving less inventory.

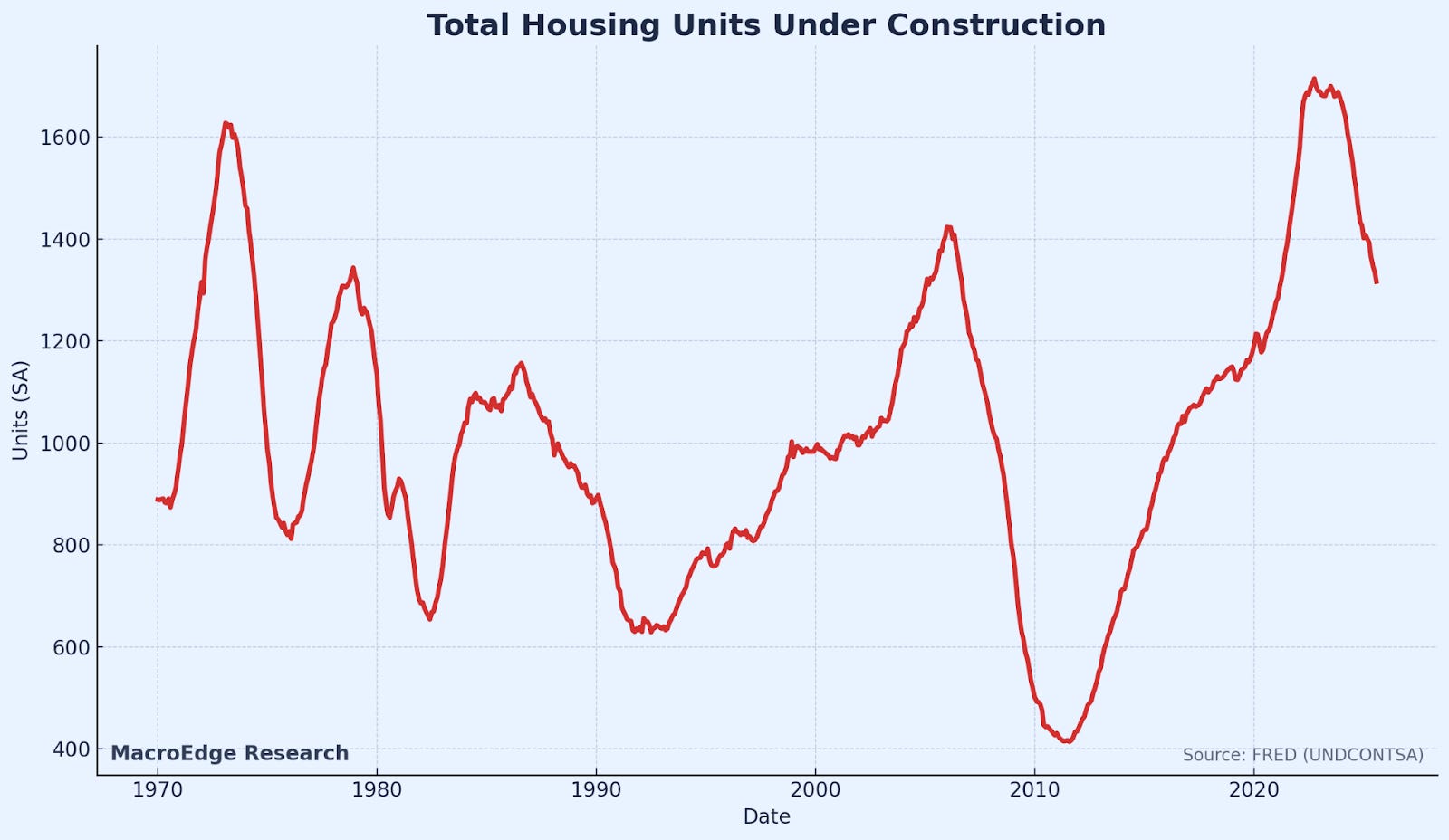

Total Housing Under Construction

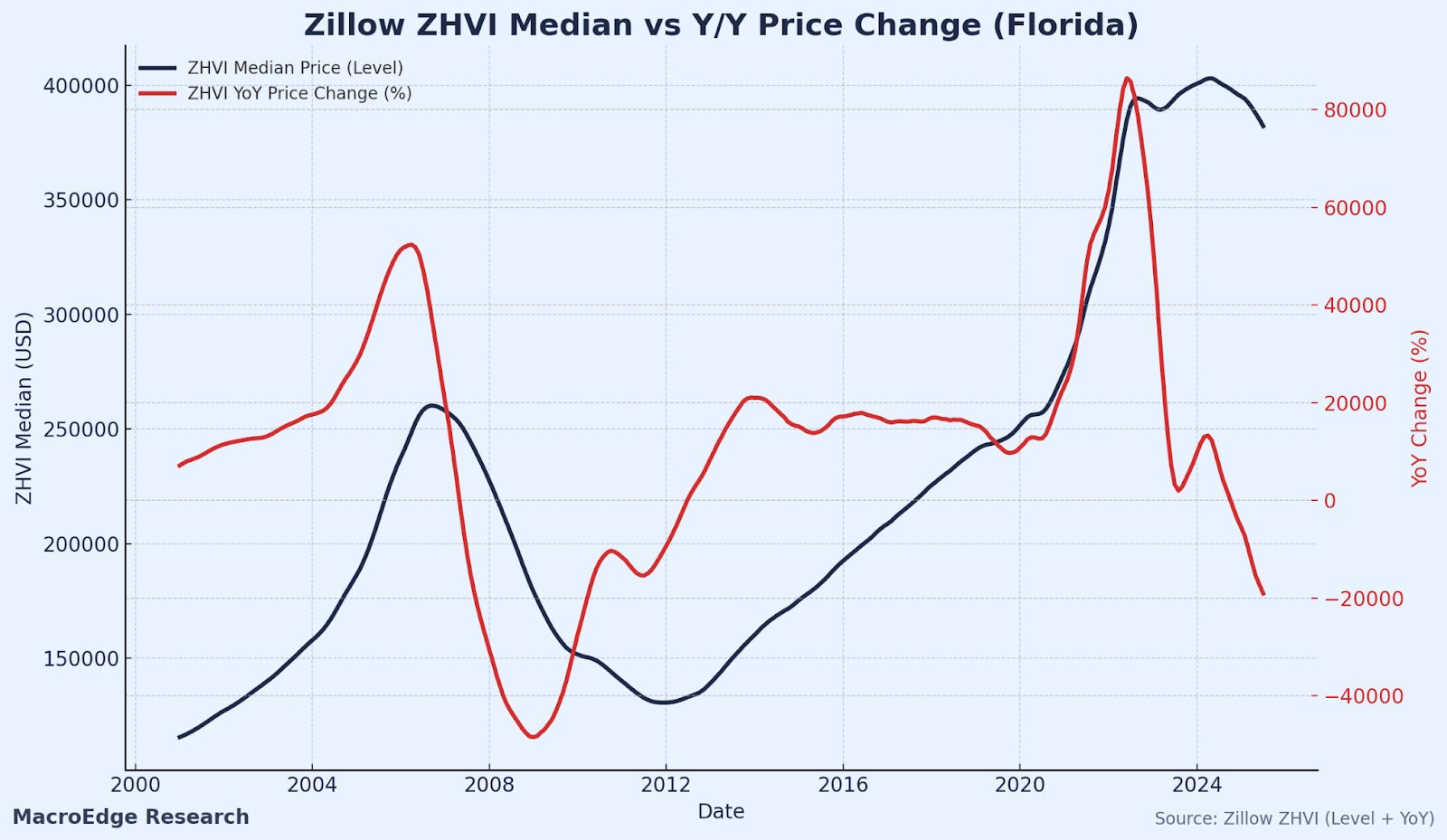

Florida Leading the Way in Price Declines

Homebuilder Equities - XHB

The public builders have failed to reclaim their 2024 highs, though they recovered sharply from the lows as rates eased (10Y briefly below 4%). Biggest risk is a higher 10Y, given the macro backdrop, or a U3 above 4.5%:

Globally - the most important factor to domestic housing markets is going to come down to immigration and demographics.

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.