Redeye Macro Note: A Tale as Old As Time, & Time to Ignore the Headlines

In this Redeye Macro Note - we dive into the unprecedented global price action, highlight the latest margin debt data, explore why headline volatility should be ignored, and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Friday evening MacroEdge Readers & Community,

This note will be brief, and more of a rant, as some of these Redeye Macro Notes tend to be.

We find ourselves in a tale as old as time in the modern US market - one where a lot of people are scratching their heads, but few know the reason or catalyst behind a new surge towards the ‘sky’... in this case, being all-time highs. The war is now well in the rear view mirror from a ‘priced-in’ standpoint, and AI + meme stocks screamed higher through the morning, with things cooling off just a bit into the close. The ‘garbage’ basket - one we track of profitless meme equities - has almost doubled in the last two weeks - signalling what a violent risk environment this is. The talk of shortages and risk from a Strait of Hormuz closure has abated as front-month crude contracts have dipped, and collective delusion has hit all-time highs while we see the economy bifurcate further… the end result? Something like this:

While I know that many of you will see this note when it arrives in the morning in the ET, I am still in the PST. I spent the afternoon going through a lot of charts and data to get a better grasp of the historic magnitude of the past two weeks - not only from a % gain standpoint - but also trying to digest what the future implications of the events that we’re seeing are going to be. To cover the price action for the day very briefly - early in the day, Iran’s FM tweeted out a version of a translated tweet highlighting that the Strait was *completely open*, which was subsequently shared by the US president and downstream beyond that into the press, on X, and beyond. Briefly, the markets took this as everything had been resolved - but for now, I think the lesson learned over the last 3 days of 100+ headlines a day is that it’s time to tune these out… as what we’re seeing is mostly bullshit, or an illusion, pardon my French.

I had a brief evening phone conversation with Six, our Head of Portfolio Strategy (fmr. Research), and we were quite surprised by both the past week, and a lot of the looks that we saw in charts. The most obvious (and somewhat humorous) being the massive runups that have been occurring in near-insolvent, and garbage companies like the MEME basket, and some of them look to have moves that are just starting - rather than ending, likely a consequence of the Fed beginning to ramp up liquidity through an expansion of its balance sheet, and continuation of short term issuance policies from the Treasury. I am seeing something similar in the cryptocurrency charts right now, which were largely ‘dead money’ after their October 2025 single-day disaster, which rendered a lot of coins effectively dead in the largest single day liquidation wipeout that had been seen in that sector in $ terms. The next critical junction is likely to be a meeting at the 200dma to decide if we’re going to see a more-2022 style scenario, or see the ‘Venezuelan’ (as I refer to it as) style scenario, where everything begins yet another crash up as the Fed continues to let inflation get far too hot.

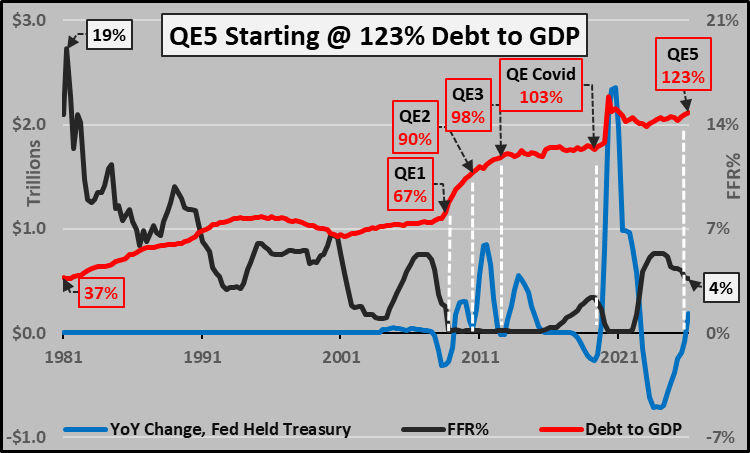

We are starting the warm-up to QE-5 at almost 123% GDP, a terrifying fact for those of us who understand the long-term implications of this policy (in things like birthrate collapse):

(Chart: @Econimica - CH on X)

… A note from CH:

The outcome continues to look one more of a developing nation by the day, and I may have to wheel back out a former favorite series that we had going years ago.

For energy equities - it remains relevant to continue monitoring the conflict (case and point being the morning story) - but I strongly recommend ignoring the minute-by-headlines - as many are made-up or part of a broader information warfare strategy on both sides. Because we have the pleasure (not really) of waiting until the next futures open, we can discuss the next update here on Sunday evening on this front. The setup, structurally, remains very positive for our energy strategy basket - even though short-term front-end manipulation is greatly impacting the sector from an investment standpoint.

In terms of this insane equity action - look to the next major IPOs: SpaceX, ChatGPT, Anthropic for our ‘topping signals’ - even Michael Burry noted today that the ‘needle top’ is quite rare - and even though we’ve seen it instances like 1990 Japan - this equity price action is much more violent, and much more backed by policymakers than we’ve seen in previous instances. I could also cover the blatant fraudulent trading taking place in markets now - in assets like CL - but I will leave those rants to my X feed.

While the FINRA Margin Debt story was likely a brief intermission head fake & ‘real macro’ data continues to point toward a very troubled 90% in the days, weeks, and even years to come, I am quite confident that we’re going to see these trends continue. As we highlighted last night in the Midweek Macro Note, the Fed’s liquidity cannon is once again back on.

In being a data-driven organization, it’s time to tune out the bullshit headlines, and continue to master our craft at delivering the precision data that matters, and how it translates into intelligent strategy, in this time of great noise.

Not yet a MacroEdge Ozone subscriber? Access Ozone below and get all of our research, data, strategy, and much more. There’s a lot that we’re rolling out between now and June - so don’t miss a beat.

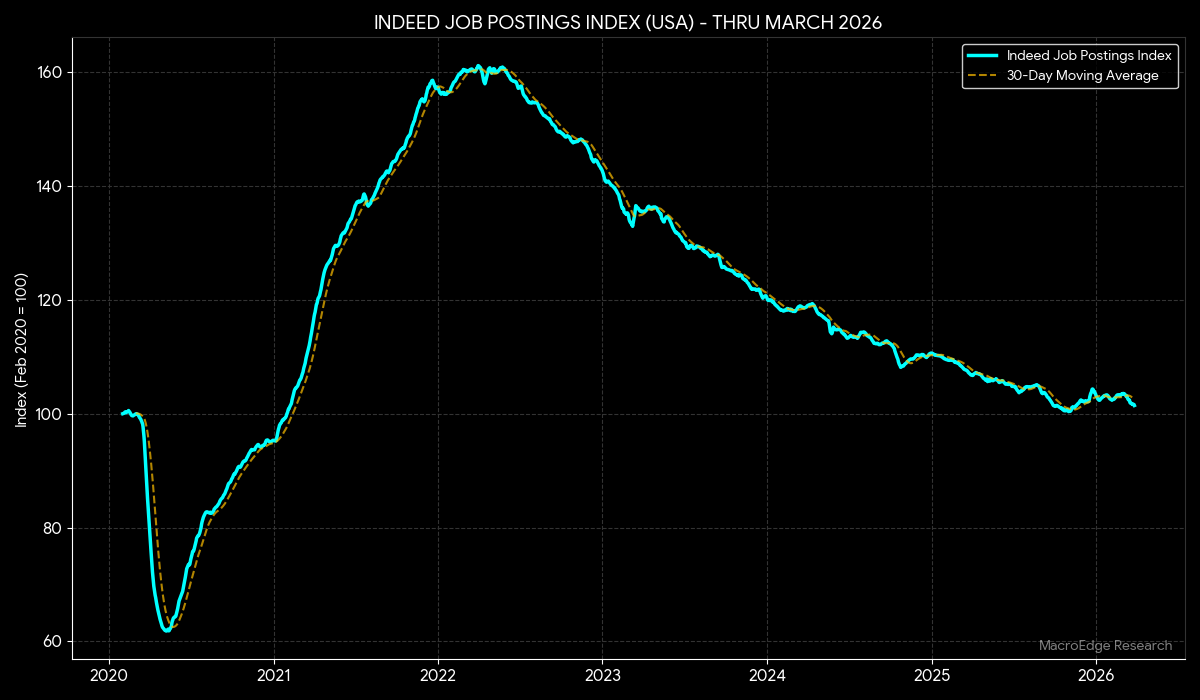

Mid-Month Employment Update

Employment this month is softening - as seen in job openings resuming a decline after a very brief reprieve:

While some may claim this is due to *AI* - there is structural weakness in the American labor market well beyond AI job displacement taking place at technology companies.

Month-to-date job cuts are sitting at about ~40,000 - highlighting that this will not be another slow month by any shape of the imagination. With the Administration looking to visa issuance to boost population figures, however, I think that we may see job growth in some of the lowest wage bands start to move higher.

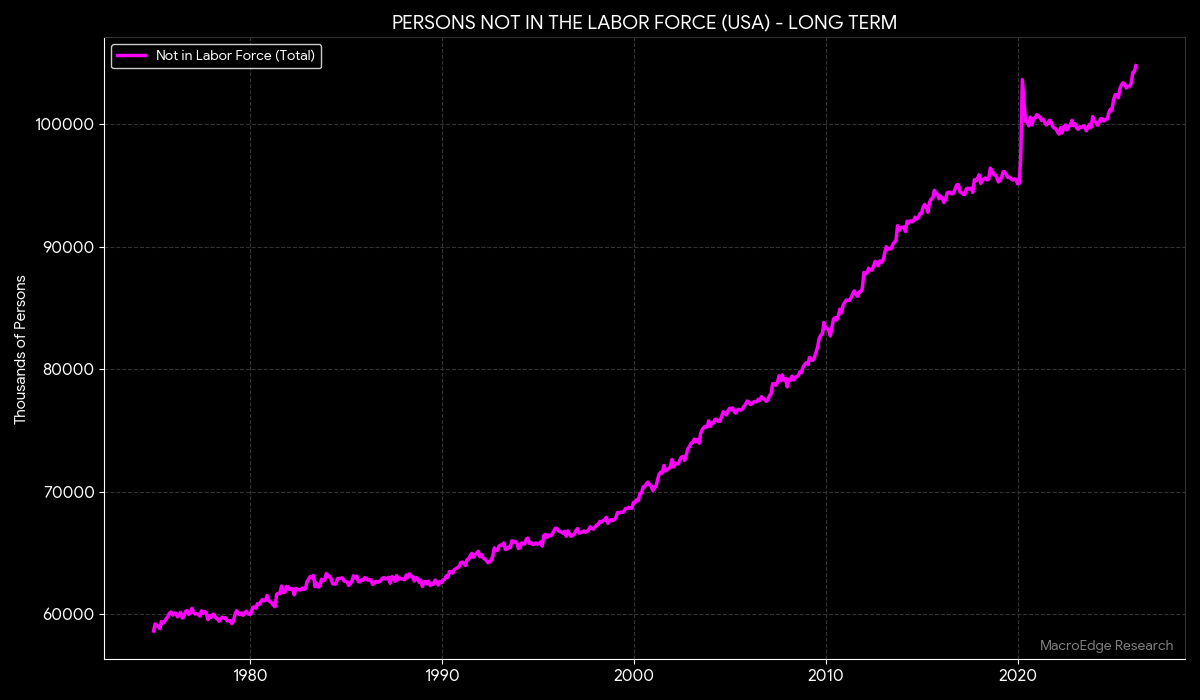

I also would like to remind our readers of the shifting demographics and aging of the US workforce - this is likely to drive a structurally lower unemployment rate for the time being, as workers age out of the workforce in the thousands per day.

That is a lot, lot, lot of people that have to be subsidized.

MacroEdge Global Bubble Index

(Below: MacroEdge Global Bubble Index - a breakdown of the index, what it means, and what to look for in the next 3-6 months, a preview of the Saturday Macro Note - where we’ll look at first ‘On the Ground’ Report happening here in a few weeks, and also take a look at the preview for the Weekly Macro Note)…