Redeye Macro Note 10/25: CPI Review, No Data for October, Weekly Macro Note Preview

In this brief Redeye Macro Note - we discuss the CPI print from Friday, talk about the lack of data for October, similarities to Fall 07 in this period of data blindness, and more. Note avail to all.

Good Saturday evening MacroEdge Readers & Community,

This Saturday we have a brief Redeye Macro Note available to our entire community - discussing the CPI report from September, which was released as required by law, some of the expected data gaps for October, a review of what we’ll be discussing tomorrow, and talk briefly about the Carry Trade rewind that’s set itself up - to a degree not seen since July ‘24 and Jan ‘25.

This week I hit the road with our co-founder and we are again making our way west for several events & meetings. We continue to push the throttle on all of our Transform and Macro Research offerings, and are positioning ourselves to expand further through the remainder of the year, and even more substantially in 2026.

Tonight’s topics of discussion:

Portfolio Strategy Update

CPI Review

No Data for October

Risk Dislocation

Carry Charge Recharge - USD/JPY Edition

Weekly Macro Note Preview

Portfolio Strategy Update - MacroEdge Global Macro Strategy Portfolio (GMSP)

No updates to report for the GMSP for the week, we continue to operate in a patient ‘wait & see’ mode, and are waiting for a more attractive window to put our strategy into motion. We have a lot of interesting events, data, and developments this coming week that are worth watching closely, and once our signals fire, I won’t hesitate to go big.

To learn more about MacroEdge Ozone & access to the GMSP and our portfolio strategies, visit:

CPI Review

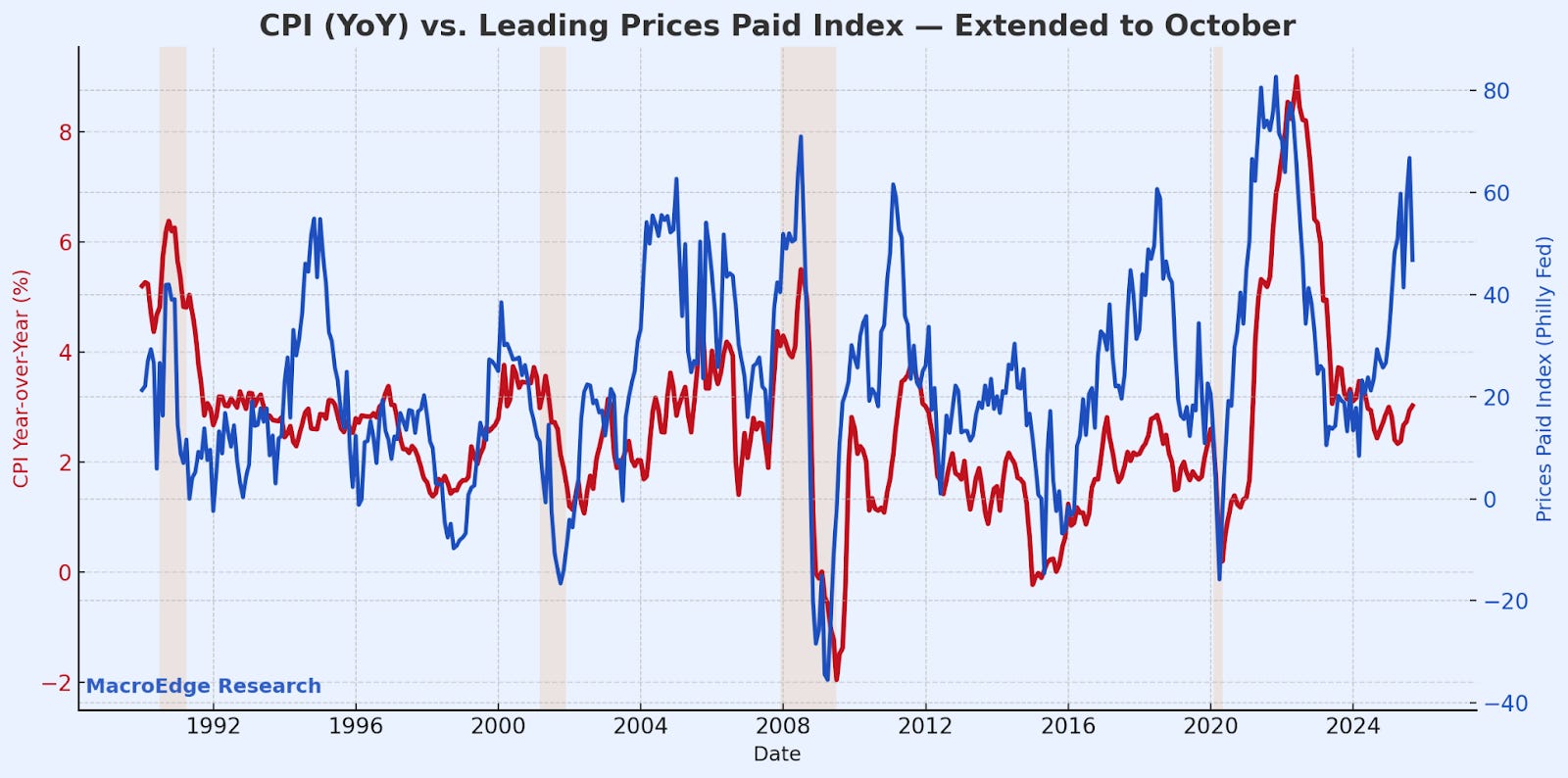

The CPI report came in slightly cooler than economists’ expectations at 3% year-over-year (y/y), versus 2.9% previously. This was the 5th consecutive month of higher y/y prints, and it’s very likely that we get no data for October, given the shutdown extending into November.

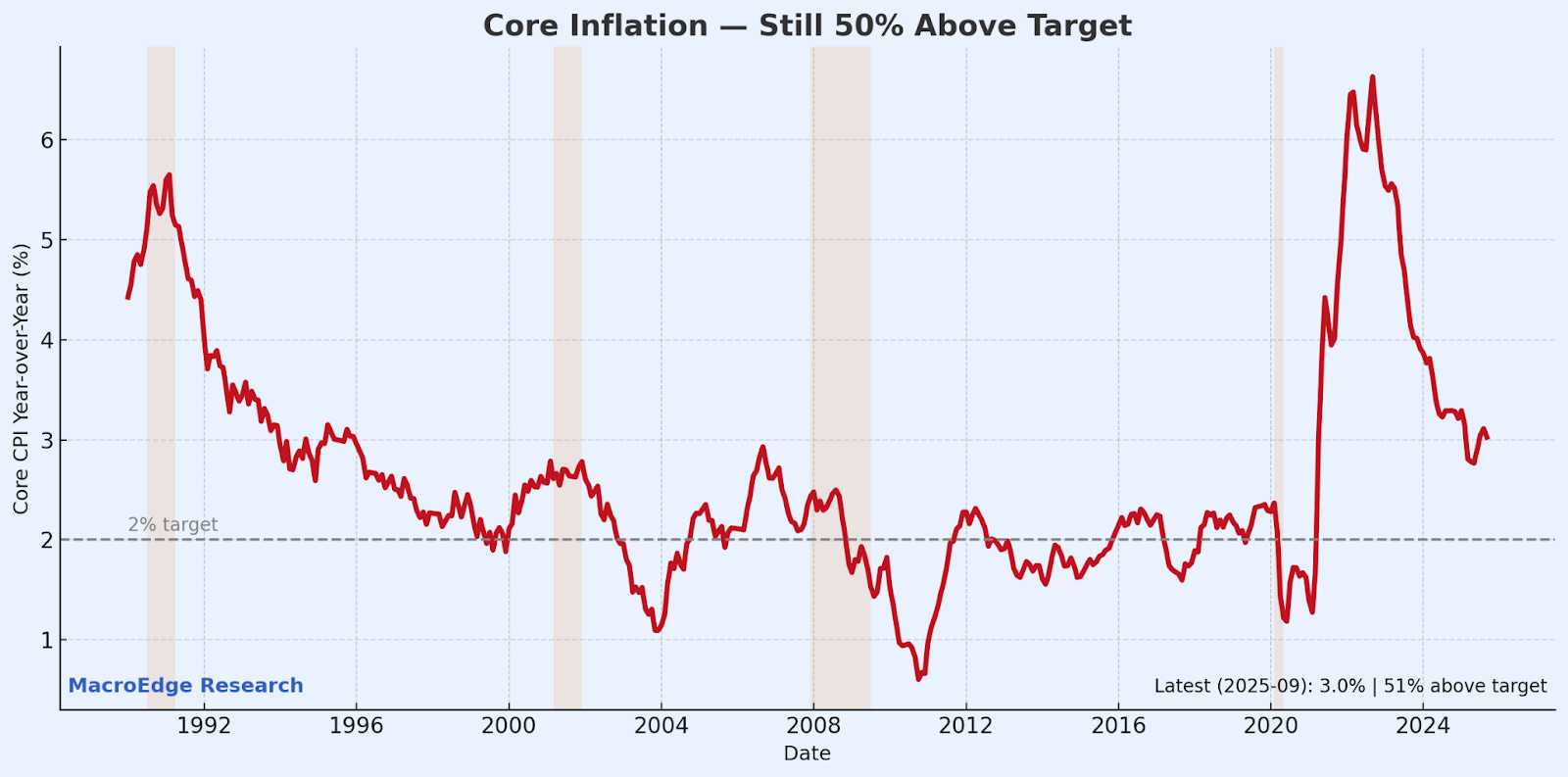

CPI continues to track an impulsive move higher in prices paid (mostly tariffs for the time being), so policymakers either know about some deflationary impulse in the pipeline driven by something like residential real estate & credit destruction, or the 2% target has truly been abandoned for the time being. Same goes for Core:

I am not a fan of the ‘3% is the new 2%’ now being parroted by absolutely every financial talking head - but for the time being, there’s little fiscal sanity being pushed anymore. The US added debt at its second-fastest pace on record Q/Q, adding $1 trillion to the national debt (now above $38 trillion), and heading much higher. The CBO expects that figure to be as high as $40 trillion as we roll through the 1st quarter of 2026. A debt owed per taxpayer of roughly $350K.

No Data for October

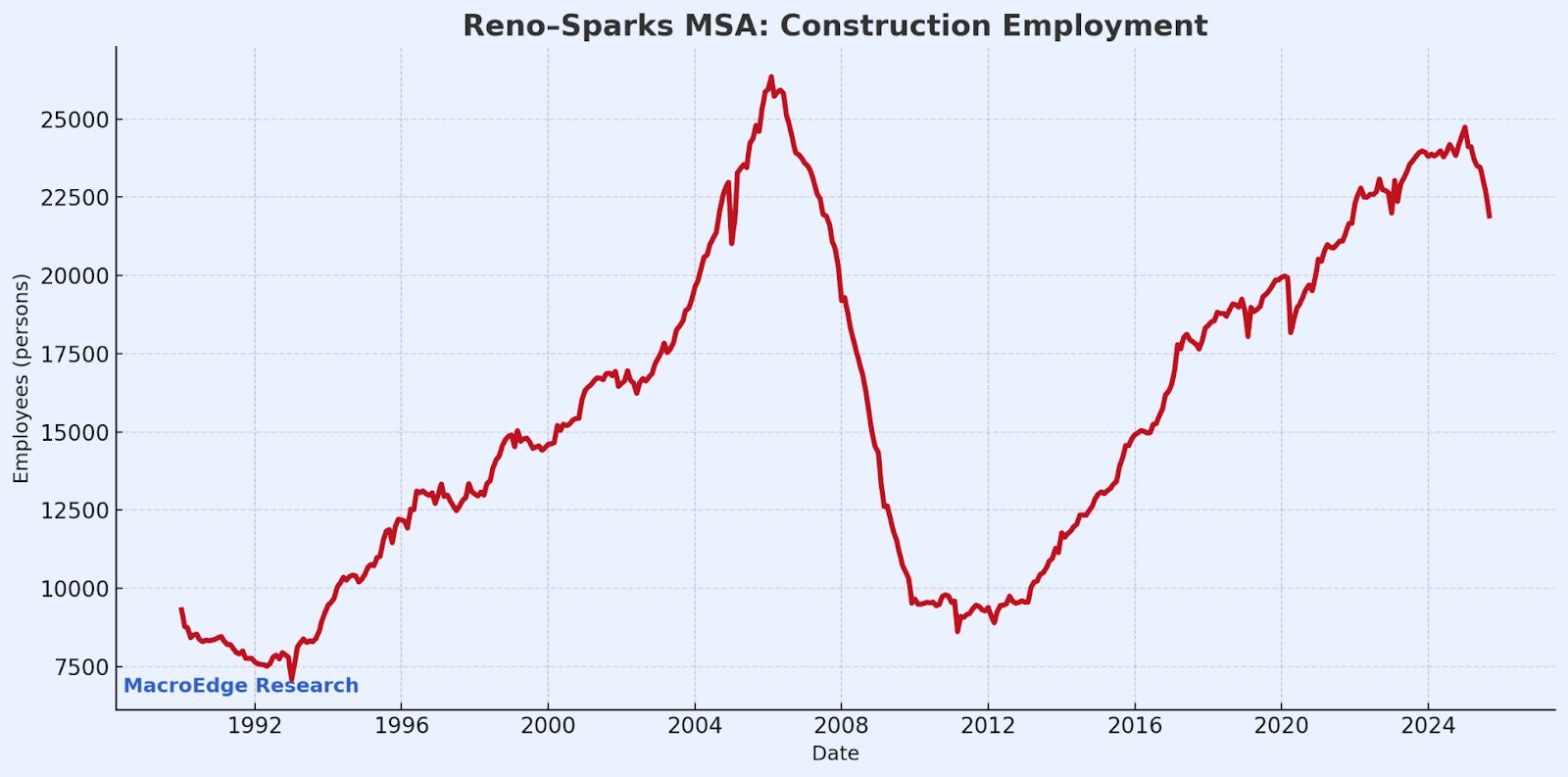

Ironically, we’re data blind - just as a lot of our cyclical indicators began to crack (residential construction employment, construction employment, heavy truck sales, etc.) - so we’re relying on private sector data and internal data for the time being, to give us the best possible labor picture possible. Employment continues to cool, and the cooling real estate landscape - especially for the single-family side of the equation will continue to drive weakness in that sector. Our favorite ‘Silver State’ conditions were and are some of the weakest of any state… remember those reports?

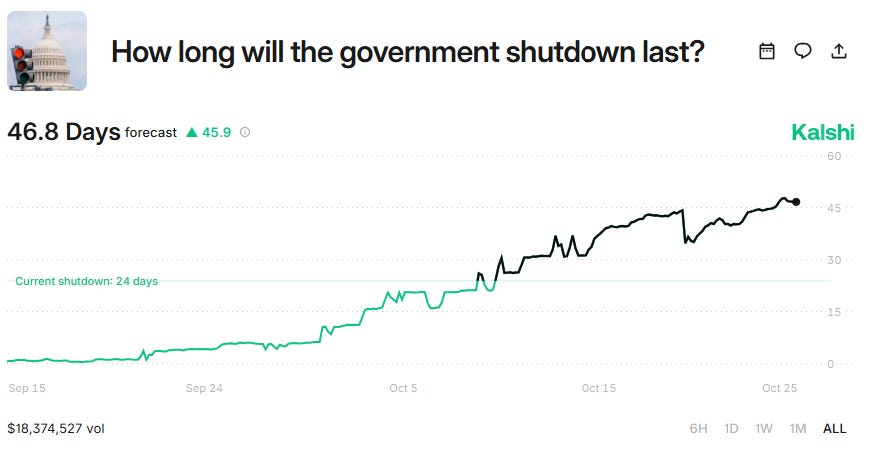

The government shutdown is currently expected to be about 47 days, and rising as there remains little incentive for the government to reopen. The government will only reopen when a combination of fear and pain kick-in from an employment or SNAP standpoint right now. For now, it remains largely political, though if these consequences remain delayed, the GOP will have very little incentive to reopen things, which in the end is a form of tightening from fiscal in the interim.

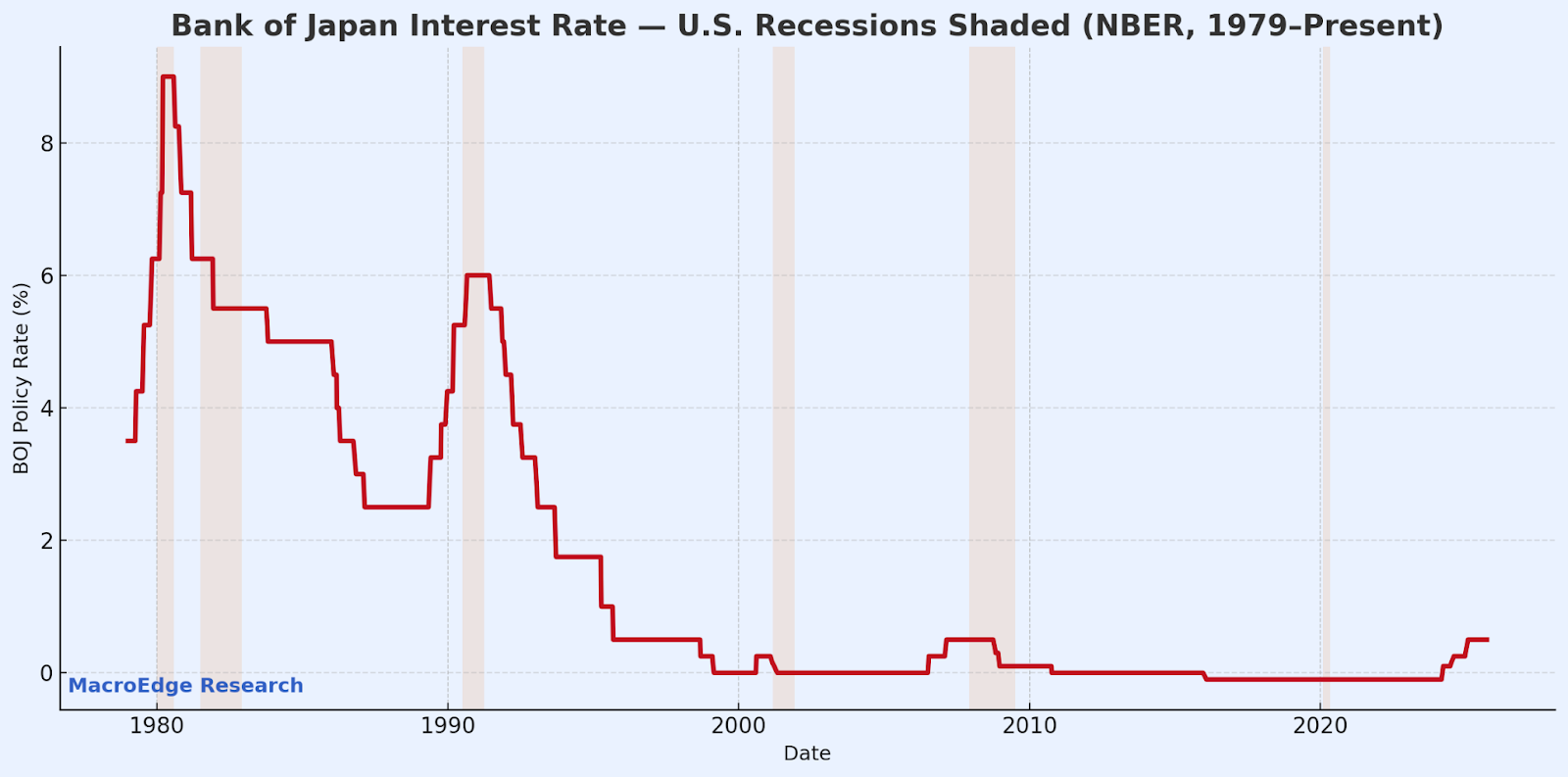

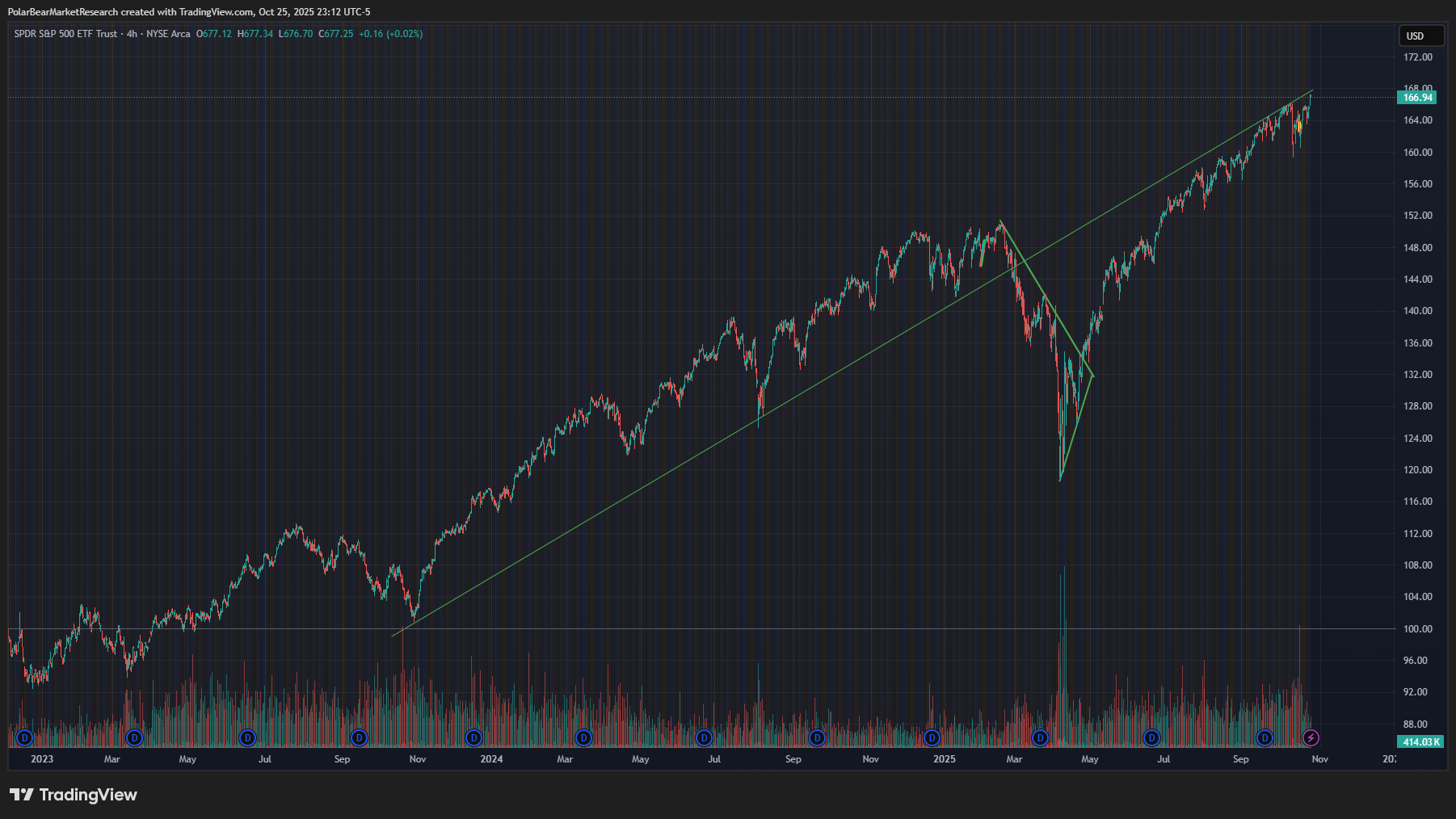

Carry Trade Recharge - USD/JPY Edition

The new Japanese Prime Minister is another Abe-reincarnate, promising to print and blowout the deficit like nothing else to pump the Japanese economy up. This rhetoric has led to renewed weakening in the JPY after the intervention window (highlighted) following the basis trade blow-up and Bessent/Japan/Korea fear in April:

Would be a prudent place for the BoJ to step in here - before things get really ugly for the Yen.

A strengthening of the Yen here would be a negative headwind for US equities once the pair reverses this spike. Recall that it’s when the BoJ cuts that usually signals that the globe is facing (or going to face) broader economic troubles - Japan & the US run a strong R for very obvious reasons.

For the time being, Japan is potentially look at 1 more hike for the cycle, though with their new PM, that’s no longer a *guarantee*.

Interestingly enough, just as we are again running back into a key backtest:

Weekly Macro Note Preview

Technicals Overview

‘Quant Quake 2.0’

Risk Dislocation - Crypto, Homebuilders, Regional Banks - Why They Matter

Weekly Macro Data & Earnings Review (+ trade meetings for the week)

FOMC Meeting Week - Likely Rate Cut

Government Shutdown to Continue Until Pain is Felt

Another Reset for Volatility

Get access the Weekly Macro Note & more with access to MacroEdge Ozone Pro:

For more details, please refer to our Terms and Conditions.