Midweek Ozone Macro Note: Natural Gas Surge, EU Tariffs Cancelled, Portfolio Strategy Update & Commentary

In this Midweek Macro Note - we discussed the continued natural gas surge, talk about the tariff walk back, Six highlights the latest portfolio strategy update & provides commentary, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Wednesday evening MacroEdge readers and community,

Today was an interesting day in markets - we saw a capitulation from both sides (US/EU) on the tariff spat in response to a surge in long-end bond yields. While the financial news is looking for things beyond that, or some might think ‘5D chess’ - the 10Y at 4.3% was an alarm signal for the Administration to settle for something. It’s likely that there will be some agreement before midterms for military base access or something of the like, though Denmark will retain control of Greenland. We’ll get more information over the next few months - though I expect the temperatures to cool a bit with the tariff (t) card pulled off the table for the time being. We could see a pivot back to the Panama Canal or Cuba next.

The Administration is currently ‘walking on ice’ with midterms and continued sourness in consumer sentiment, so doing things that spook the market is exactly what they’re seeking to avoid. Elsewhere in Japan, we saw some panic yesterday from Japanese policymakers, who threatened to intervene in markets if long yields did not halt their parabolic ascent. That, like many temporary interventions we’re seeing these days, will be just that - temporary. In the US, the $200 billion MBS purchase program through Fannie/Freddie didn’t even make a dent, and the dip in mortgage yields lasted all of about 5 days. Yields are back where they were prior to that move, and the long end has continued to hover near cycle high levels. While PCE is tomorrow, all of this continues to be indicative of no rate this month. While the policymaker tightrope continues to be thin with markets around the world (both bond & equity market dilemmas)... + currency issues… oscillations will continue for some time until there’s a large enough macro trigger that can overcome short-term intervention like we saw today. The President mentioned he’d like to see the Dow double over the next 3 years, though the *real* question of course should be whether or not that’s in *real* or nominal terms… and I think we know the answer.

For news out of South Korea, it appears very unlikely that they are going to follow through on their investment promises made through the trade deal. Due to currency weakness, the initial investment package is being delayed at least until later in the year, and they’re uncertain about even paying the full amount. A lot of it seems like appeasement without payment, though markets (particularly bond markets) are hating the uncertainty. Subscribe to Ozone below:

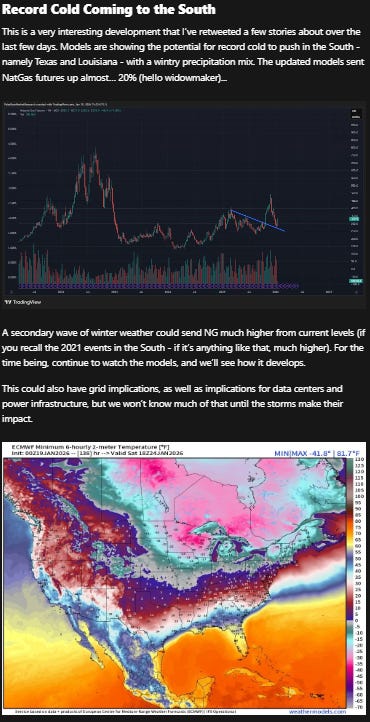

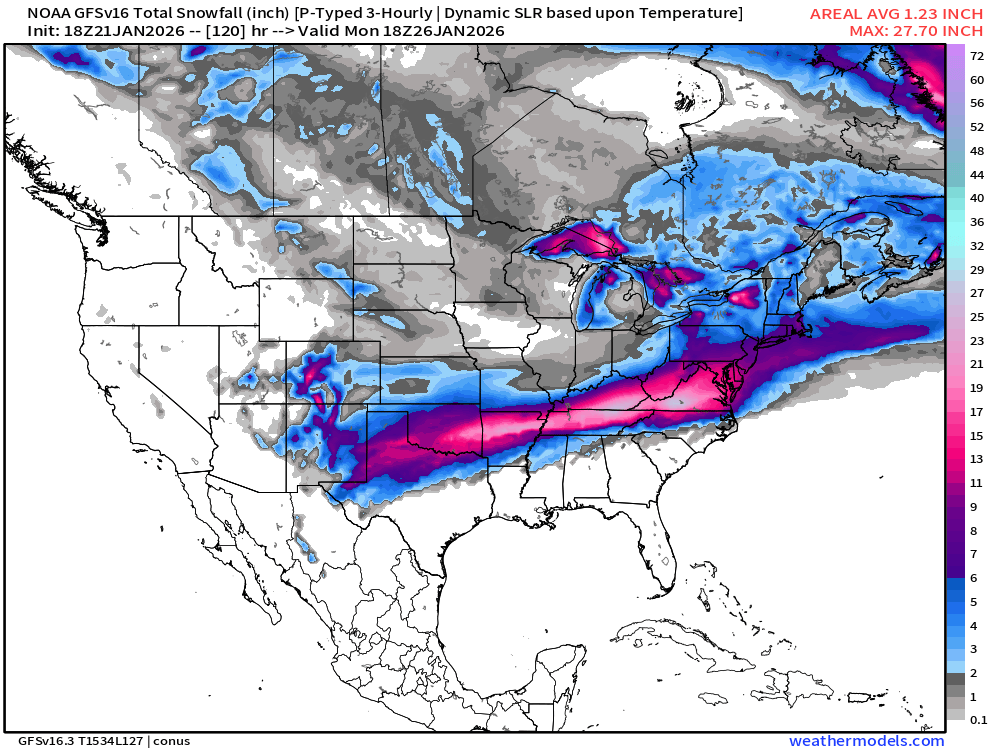

Natural Gas Surge Pt. 2

On Monday evening, in the Weekly Macro Note, we highlighted the possibility of a tremendous surge in natural gas due to historical storms lining up the weather data modeling. While I source this data externally, following the right people in the space is very useful for determining what’s actually going to occur. Last Friday, it became apparent that modeling was pointing towards a smashing cold front that would push deep into the South & SE USA. That’s now en route, and I am luckily making my way out of the South in the morning & over to Albuquerque first thing.

From the Weekly Macro Note →

While I always desired to be a meteorologist, the chemistry classes never quite made sense in my head… So I’ve kept it as a hobby… do keep an eye out for weather related posts (as they’re usually for natural gas & infrastructure news)...!

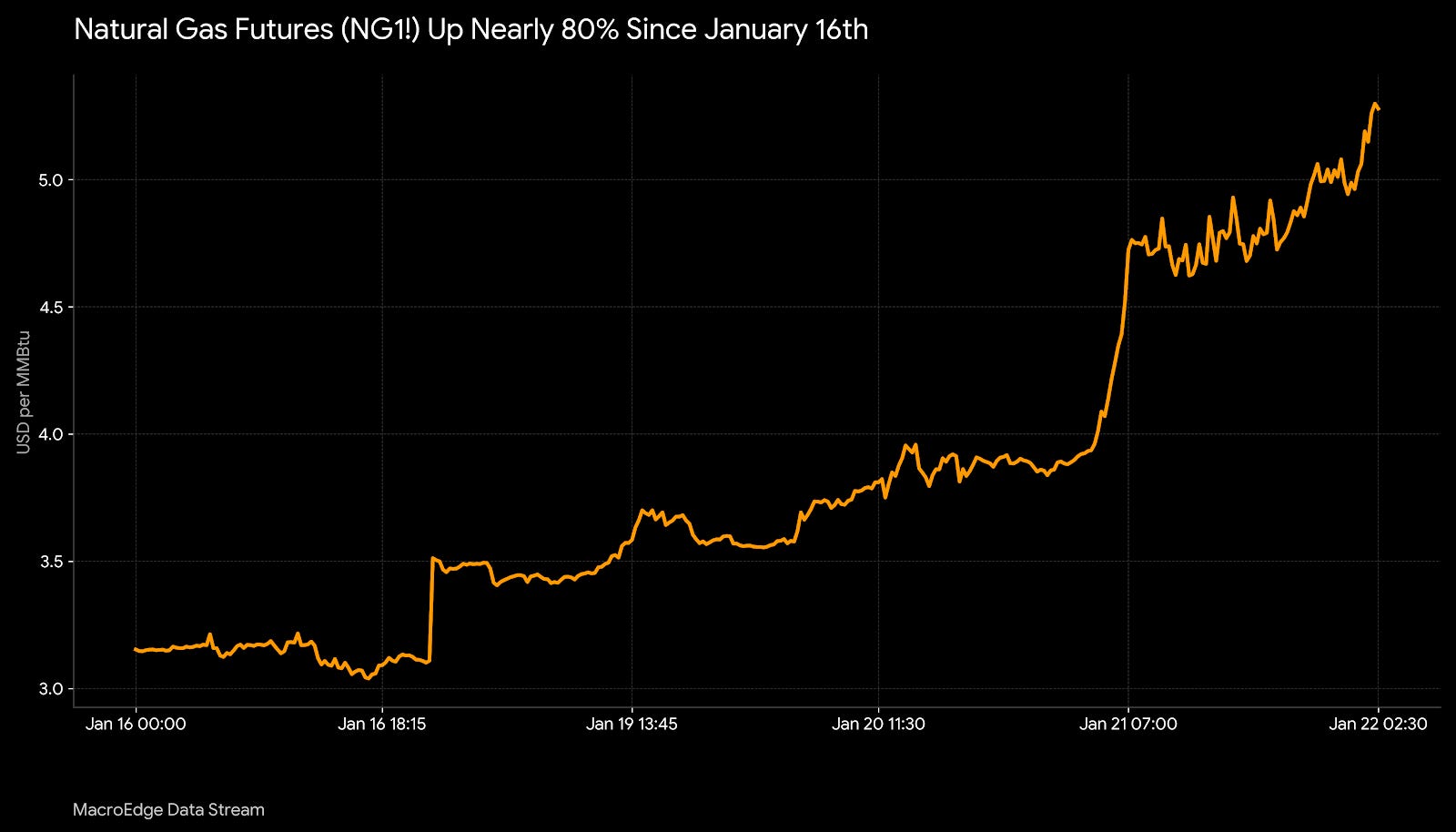

Natural gas is now up almost 80% in less than a week, and about 60% since our Monday evening mention:

Natural gas since the weekend mention:

We’ll continue to watch the latest modeling and forecasting - but shorts here have gotten decimated the last few days… Any abrupt warming in the forecast could cause a sharp correction, but thus far, things continue to look very constructive.

Stay warm… and stay tuned for more updates in our Redeye Macro Note.

(Continued below: EU Tariffs Cancelled, Pending Home Sales, Japanese Policymakers Panic, (Probably) Just a Backtest for Now, and Portfolio Strategy Update/Commentary)

Subscribe to MacroEdge Ozone, and get all of our research reports, data, portfolio strategy updates, and more - try Ozone for a week:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.