Midweek Macro Note: When Doves Cry

In this Midweek Macro Note - we dive into the dovish FOMC announcement - the new 'not QE' balance sheet expansion program - discuss the looming BoJ hike - bond risks - AI bubble troubles - and more.

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers & Community,

In this Midweek Macro Note - we’ll cover the new ‘Daily Macro Minute - arriving on Monday - as well as the latest Fed easing announcements as Powell & most FOMC members decided to revert back to their post-09 dovish nature, putting them right at home. While the Fed is not calling the latest ‘technical’ balance sheet program quantitative easing, it has many of the same features, as we explore below.

Additionally, Powell has been unable to break the back of the 2Y & longer duration yields, which remain rangebound and are set to move higher. Let’s dive into an exploration of ‘not QE’, a looming BoJ hike, and struggles in the AI bubble.

Daily Macro Minute - Arrives Next Monday (and new MacroEdge Data)

For those that are pressed for time, we’re rolling out a bite-sized version of MacroEdge data, coverage, and commentary - delivered to your inbox every morning the market is open. We’re covering 3-5 of the most important charts, datapoints, and items for the day, and the goal is to have it be a useful tool for our community to utilize in your decision-making, for your business, portfolio management, etc.

The Daily Macro Minute has its own home on Substack now, and you can subscribe to start getting these updates below:

In addition to that, we’re also wrapping up development of three new MacroEdge macro datasets & indicators. These indicators will become available in January:

MacroEdge Hiring Tracker

MacroEdge Data Center Tracker

MacroEdge Inflation Tracker

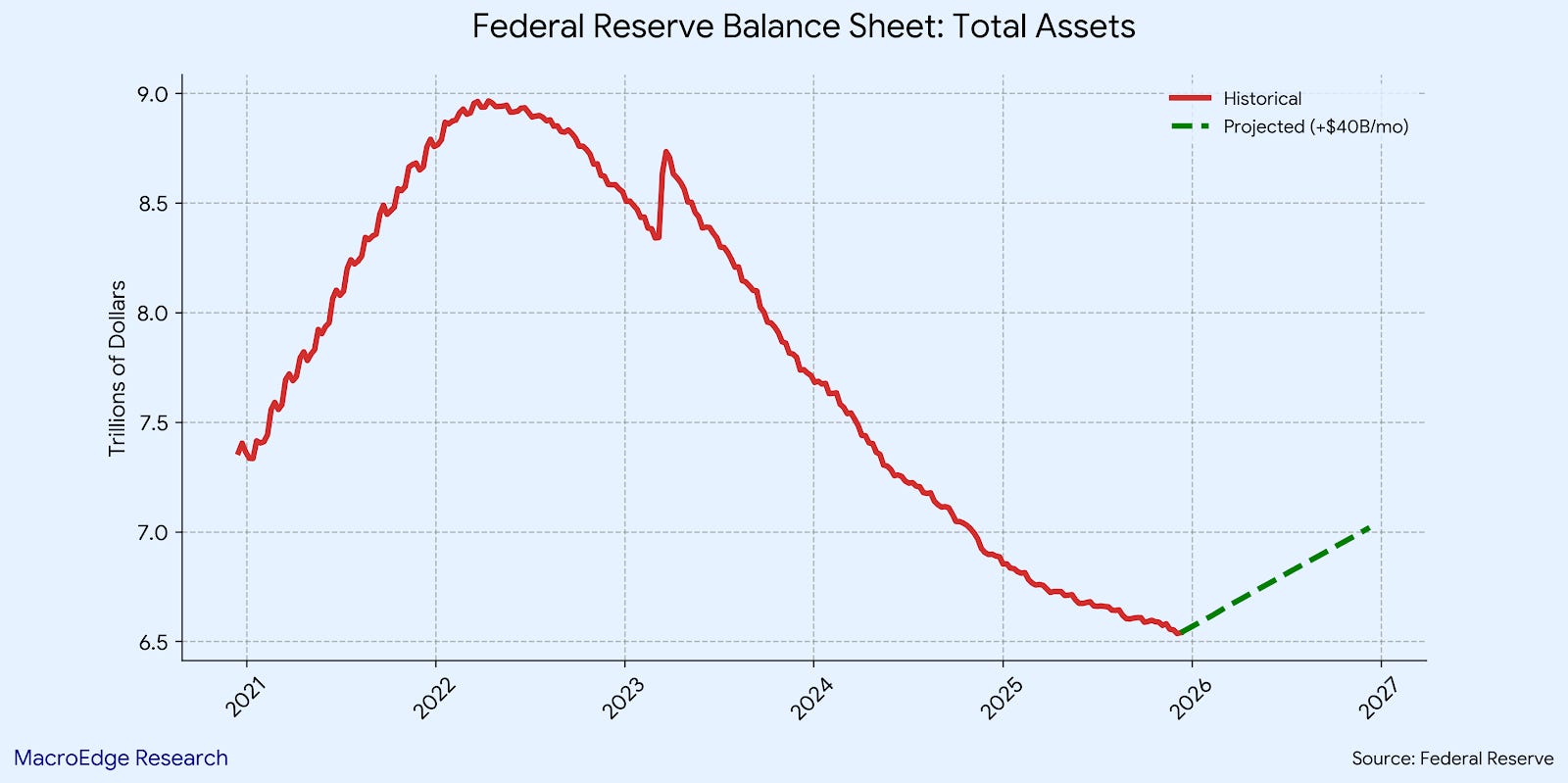

When Doves Cry: Fed Starts ‘Not QE’ Again

Powell was not at all hawkish yesterday in his presser - though division amongst FOMC members was at the highest levels we’ve seen all year. The rate cut was very expected, though equity markets we’re very excited about the news of the ‘not-QE’ QE that the FOMC has abruptly restarted. With the latest balance sheet expansion announcement (for the time being) we can expect this QE-lite program:

Fed to resume buying Treasury securities ($40bn per month) to supposedly ‘prevent funding stress and maintain ample liquidity in the banking system’... seems more like front-running of other issues.

Net balance sheet effect over the next 12 months:

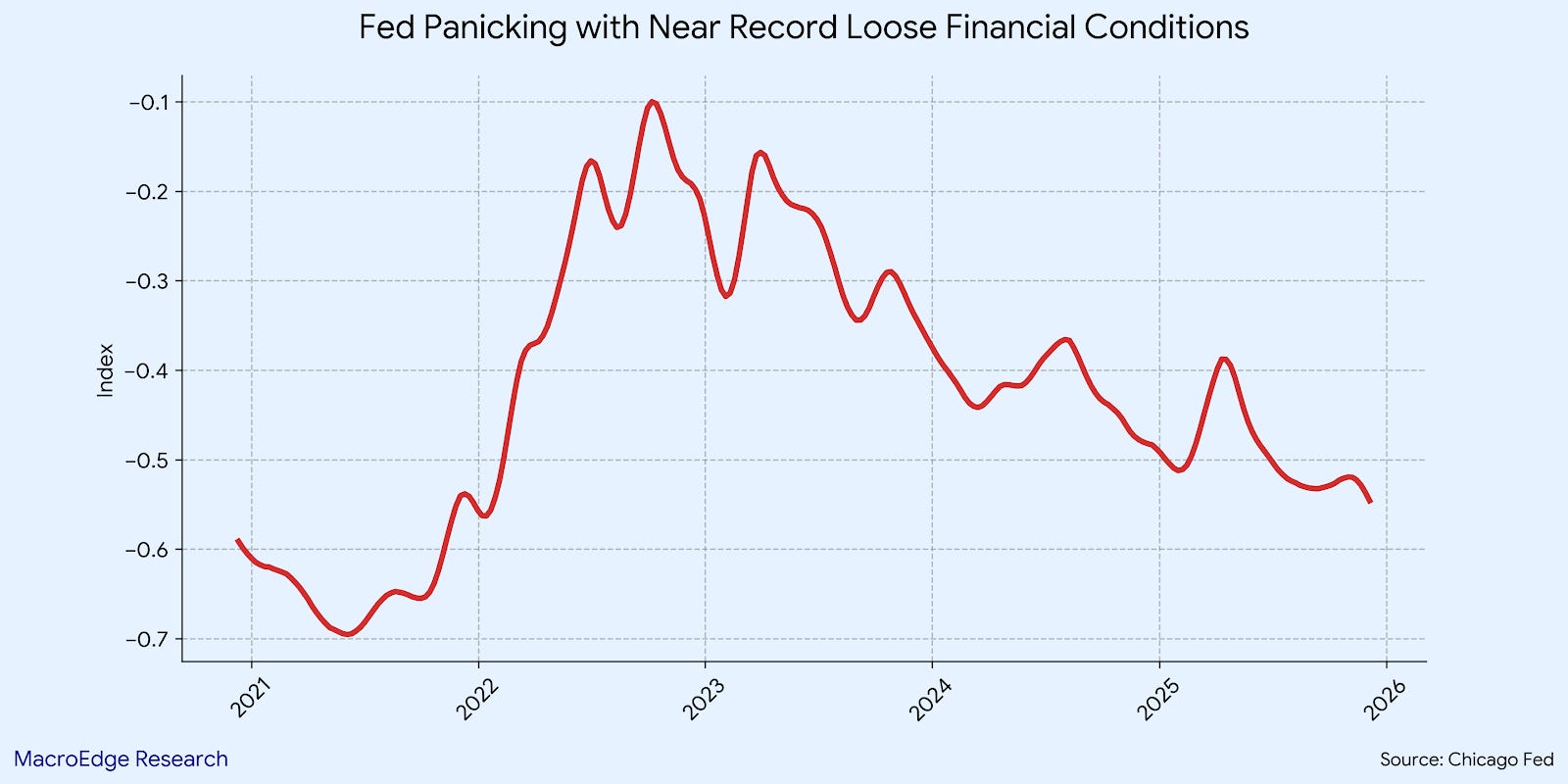

As we’ve seen over the last few instances of these ‘temporary’ market stabilization measures, this is likely the beginning of another march much higher in the Fed balance sheet (sad truth), and enough to even make the biggest doves cry. Powell failed to bring inflation back to the Fed’s mandated 2% level with his soft tightening program, which didn’t even move financial conditions into tight territory on the aggregate level. With the level of panic & the looseness of current financial conditions, something is clearly going wrong in the plumbing behind the scenes.

The Fed only controls the short-end. Powell’s intervention in the longer-dated yields is lasting shorter and shorter, with the 10Y already back above 4.15 and the 30Y moving higher. With sovereign risk & fiscal insanity in total play with where we’re at - I believe yields look constructive for higher levels in the short-term.

10-year:

2-year - continues to tighten in this range:

30-year:

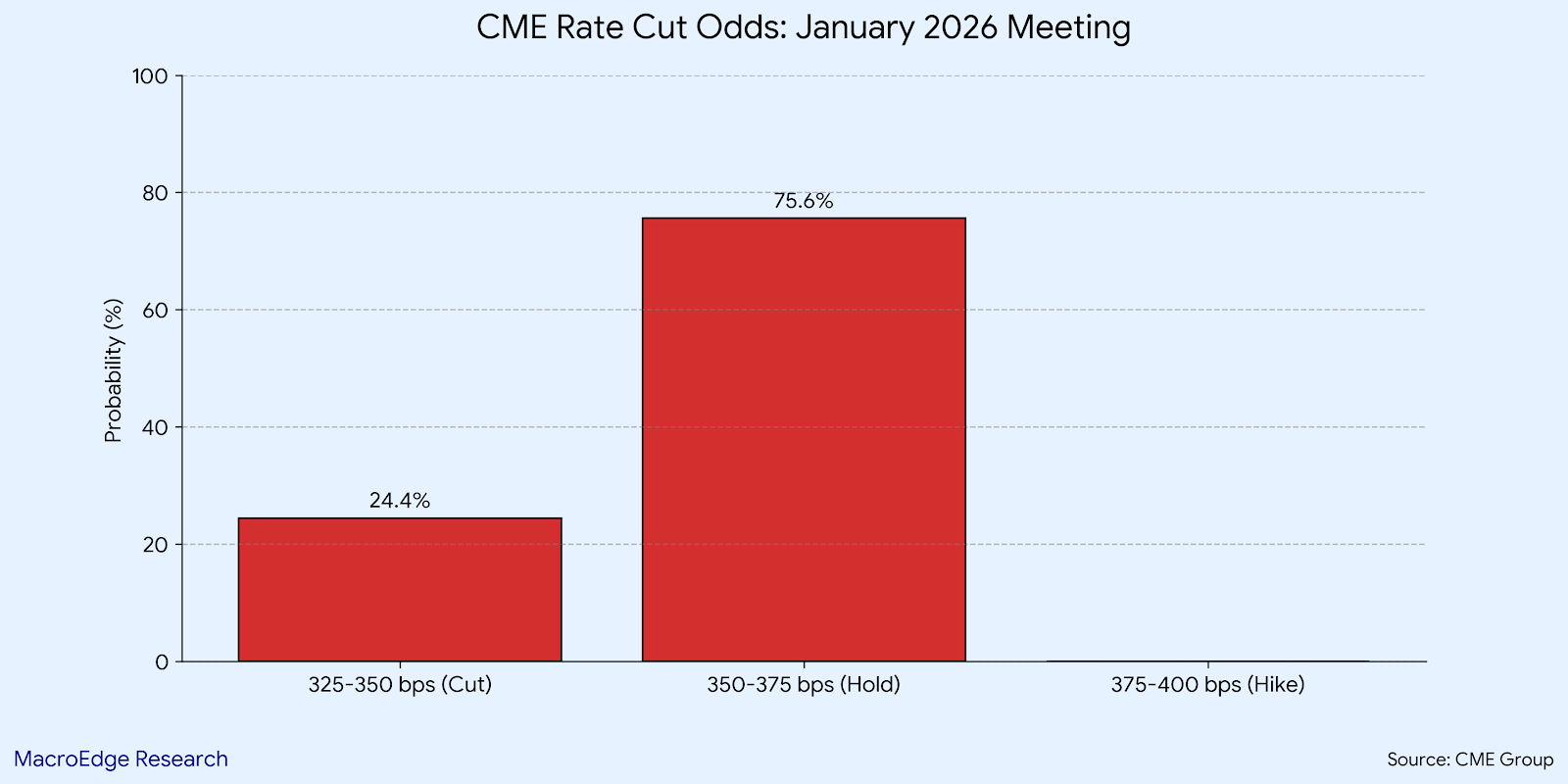

Odds are this doesn’t turn out to be enough, and as we’ve hammered on for the past 6-12 months, an ultra-dove like Hasset pushes us something more like outright yield-curve control (YCC), a policy pioneered by the Bank of Japan in modern times.

Odds of no cut right now are about 50/50 - a coin toss - or red/black roulette choice - and the coming lagged data releases next week will pretty much seal the deal on direction. If the 2Y starts to tick back higher - we’ll see no cut in January - and given the yield action across the west (Canada, Australia, New Zealand, Europe, UK) there’s little reason for a cut right now.

Don’t miss a MacroEdge Macro Research beat, with two week access to MacroEdge Ozone:

The bond market again has a unique opportunity to price in more risk than equity markets do, and widen the dislocation between reality & fantasy.

Next Up to Hike: Bank of Japan

The Bank of Japan is the next to hike, with OIS (overnight index swaps) pricing about a 90% chance currently.

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.