Midweek Macro Note: Walking the Tightrope, 'On the Ground' Pt. 2 - Preview, Technicals

In the Midweek Macro Note - we discuss how we're 'walking the tightrope' when it comes to the macro picture in things like inflation, preview Part 2 of our 'On the Ground; research, and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers,

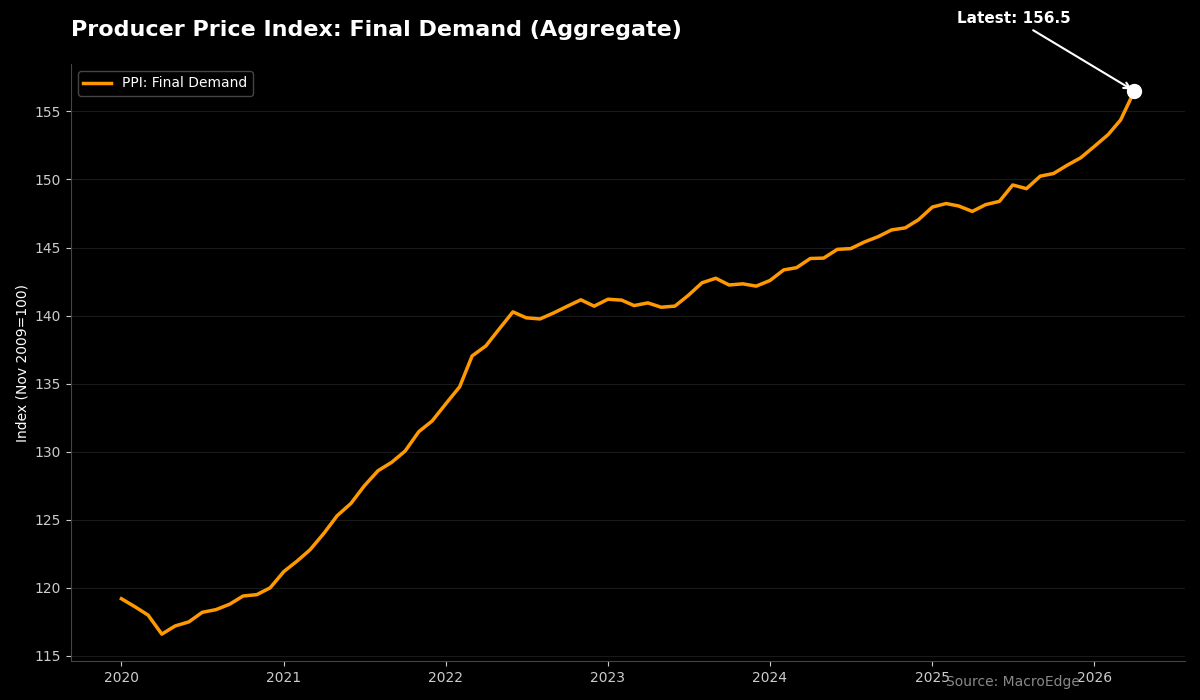

This evening we’re going to have a brief ‘debrief’ on the last few days in markets & beyond. Inflation is running very hot as we’ve consistently been beating the drum on, and actual price pressures are catching up to the obvious ‘real-time’ signals in some ways. There is still a lag to another leg higher in prices, because prices at these levels are still not yet conducive to demand destruction. I am wrapping up my time in the Panhandle of Texas this evening, here for a final night, and I had to enjoy some fantastic Texas BBQ… the background of a wildfire and near ‘dust bowl’ conditions set quite the mood that this was going to be an interesting summer for not only this town, but the entire High Plains region. There is a general calm, but concerned consensus about not only what the rest of the year may look like, but what next year may look like too. Farmers & ranchers are sitting with very little insulation to broad-based price pressures and the result is margin compression as they lack control over the broader commodity market for the goods they are selling. Inevitably, this is going to lead to more failures in the farm (and ranch space), and one just needs to spend 20-30 minutes driving around south of Amarillo to see the sheer number of for sale signs on the land that was once occupied by crops.

I still strongly expect that we are seeing a topping process in the number of data centers under construction, and the Silicon Valley shadow crew is going to lose the narrative there with the general public in a larger way as we head toward November. Opposition to the data centers hasn’t found a single force to unify behind, but I do expect that becomes a bigger reality. Guys like Kevin O’Leary hopping in the ‘grift tank’ for an outlandish mother of all projects in Utah are just further evidence. I have still yet to see any clear pathway to profitability for 90% of the AI investments I am seeing made today - outside of headcount reduction - and I really do sit and read through several of these articles a day, wondering what the broader agenda at play is here.

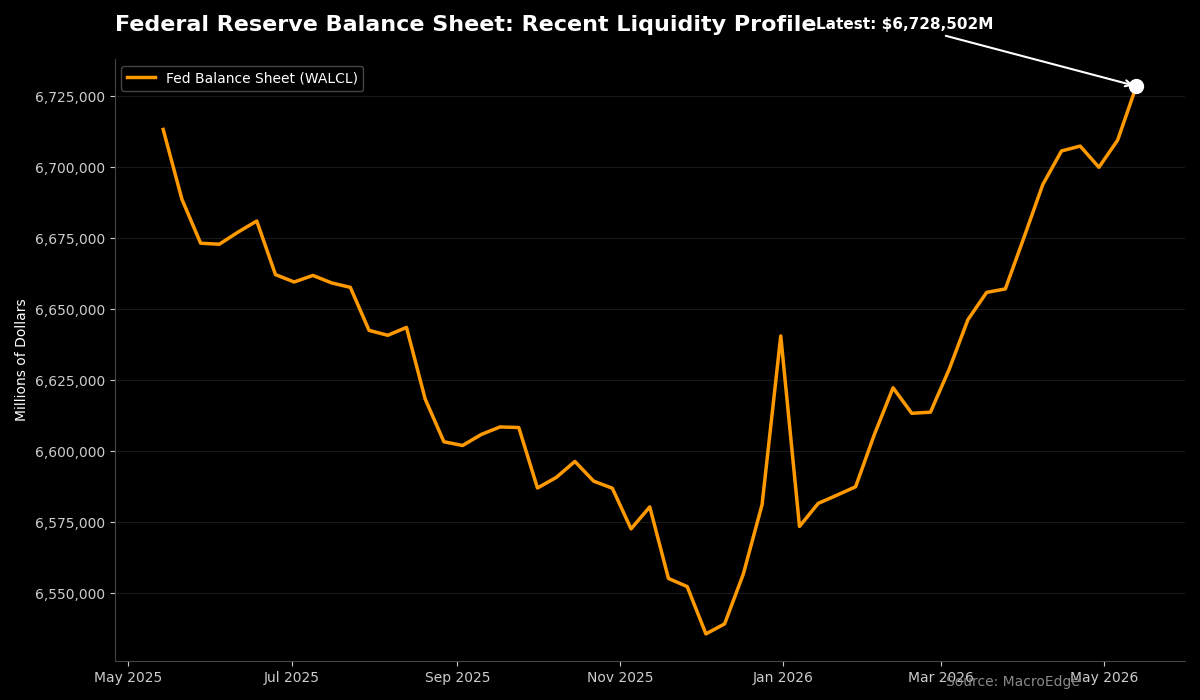

Inflationary pressures are going to continue to shift into investor view - and I would not be surprised if we don’t hear the Fed mention possibilities of hiking come the next meeting (even as they ramp up the balance sheet)... Notable cases like the Bank of Australia - which we’ve covered now for the last 3 or so months - are moving rates higher, and watch the domino effect as yields continue to move higher globally. If you recall from a note last fall, global markets really don’t start seeing trouble until Japan begins easing - and not the other way around. It once again looks like they are going to need to hike again. Central banks are behind the inflation 8-ball, and with how much money there is in the system, we’re seeing it materialize in an asset crash-up in equity markets, not only in the United States, but across our Global Bubble Index basket that tracks this sort of thing. Pouring gasoline on the fire through the relentless balance sheet expansion - which is now positive y/y and accelerating:

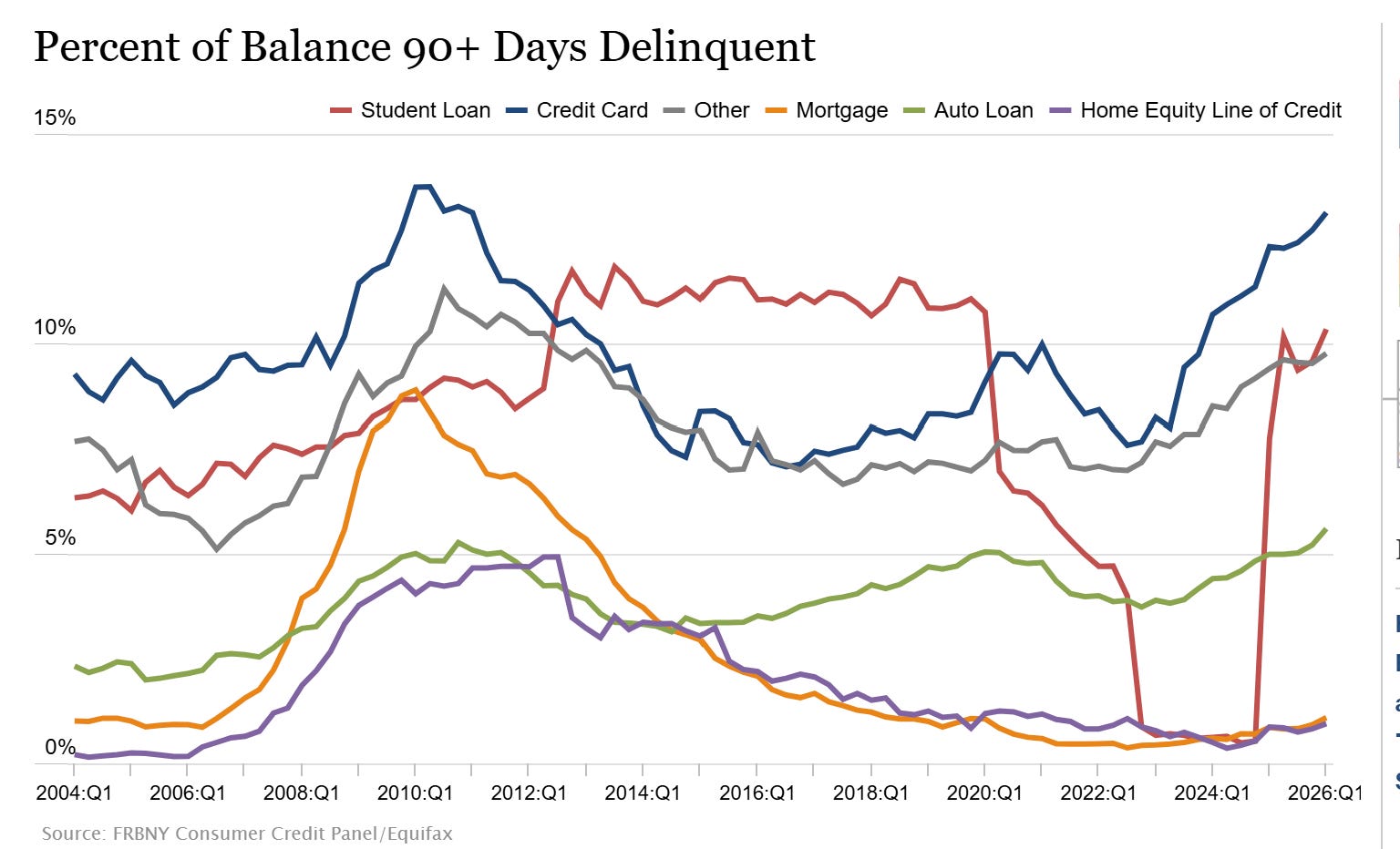

All-in-all - it remains a very dynamic situation with inflation, and I expect that even if the ‘crash up’ continues - as a result of inflation (though there are reasons why one might be cautious of this) - the broader consumer base in the US continues to suffer tremendously, as evidenced by things like delinquency data that we dive into below. K-shaped is a total misrepresentation of the on-the-ground situation in the latest data releases, and I continue to believe that ‘i-shaped’ is the reality we’re shifting to. The window for a course correction on this direction is narrowing, but either way, we continue to position intelligently - based on both our data and the data available to us for said intelligent decision making. There continues to be opportunities outside of the stupidity - and that is where I am most comfortable keeping the strategy ‘kayak’...

Below, we’re going to dive into the ‘tightrope’ we’re walking on - economically and globally - and tee up the next ‘On the Ground’ report - Part 2 from the Panhandle - where we’re going to cover in-depth the discussions I have been having with corn, wheat, and fertilizer experts over the last 2 weeks. Embedding directly into these communities has been an incredible experience, and I believe it provides our team with a unique opportunity to furnish data to you all as if you were here, too… This is going to continue to become more relevant in how we share data with you all going forward, and I look forward to the next one with Part 2 in the oil and gas space, and more.

Walking the Tightrope

The delinquency data that dropped from the NY Fed is quite concerning - even in the backdrop of an inflation-driven asset meltup. The bottom 20% of the economy is quite literally ‘tapped out’ and it’s likely that many of the figures get to levels higher (worse) than the GFC…

With mortgage delinquencies starting to pick up as of Q1, directionally these tides are quite difficult to change - and eventually I think these forces are going to materialize in things like broader opposition to data center construction at the community level. Inflation has the broader population trapped in a spiral of either needing to gamble everything and max out credit lines to stay ahead of the ‘curve’ - which is now becoming a banana:

Continued below:

‘Waling the Tightrope, Continued - ‘On the Ground’ Part 2 from the Panhandle, Technicals, a Preview of our Next Reports…’

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.