Midweek Macro Note: Tech in a Trance, Yields Shut Down Rate Cuts, New Global Arms Race, Lying About Inflation

In this Midweek Macro Note - the team covers significant ground. We talk about new evolutions to Ozone in 2026, data delays, inflation, Japan, yield risks, new portfolio opportunities, and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

This evening we’ll cover some of the data releases from the week, talk about price action, Six will discuss portfolio strategy and commentary, and John will add some color on the inflation picture. As the ‘war’ on the Federal Reserve is ramping up

From a geopolitical standpoint - while there’s mobilization underway to the Middle East - the Trump Administration appeared to at least put strikes on Iran on hold (until the long weekend)? In South America - the Venezuelan ruler is being kept in place - and some of that hinges on compliance with what the current Administration wants out of them - oil.

For the Redeye Macro Note - we’ll discuss the latest developments out of the data center world - which we know keep a close on with our own MacroEdge Data Center Tracker covering cancellations, postponements, delays, new construction announcements, and more. There’s many interesting developments going on here, and community opposition to data centers is surging across states - namely due to their impact on local electricity prices & impacts on things like water supply, as well.

Subscribe to MacroEdge Ozone, now through Substack:

This evening - I am going to discuss the latest data delays, like PCE, that are still being blamed on the October government shutdown, talk about rising yields shutting down rate cuts, the Japanese situation, and ‘tech in a trance’ - as we have seen a whole lot of hype and got a whole lot of nowhere in many names since late summer/October timeframe in 2025 leaders. These notable shifts into small cap leadership shine light on the continued bifurcation in markets - with continuing rotation, bubbles being blown up across the globe - that we frequently highlight, and ‘whack-a-mole’ macro risks that have shifted more towards inflation and higher yields - once again.

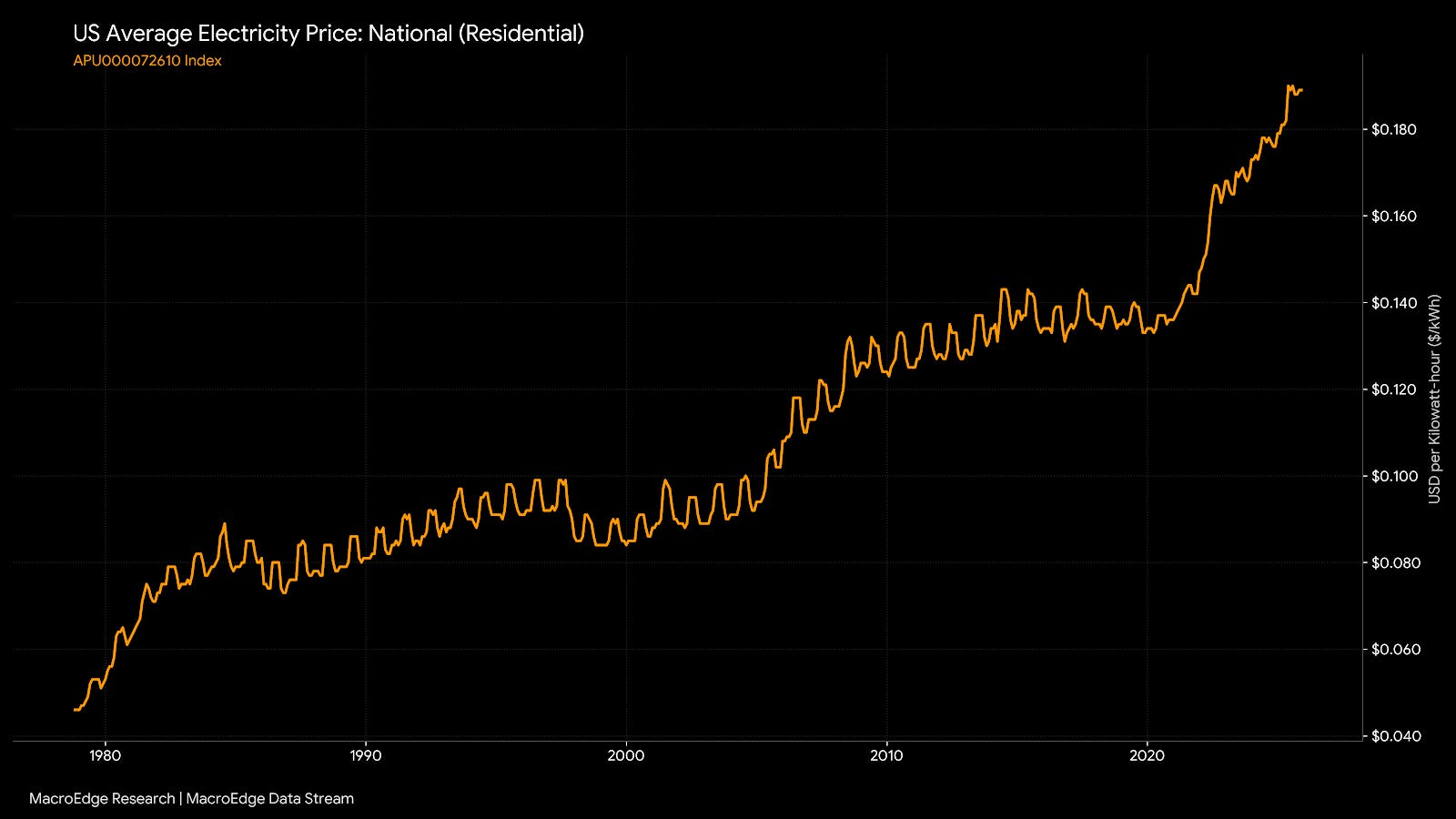

Average electric prices are stabilizing after their near-doubling from the pre-pandemic days. In data center towns - some residents are seeing 200%+ increases in bills, as they’re forced to ‘bid’ against data center infrastructure.

With the market and federal government closure next Monday due to the holiday - the next Weekly Macro Note - will fall on Monday evening, rather than the usual Sunday evening delivery.

Substack Update

We’re consolidating things like membership management and billing under the Substack umbrella to simplify our Ozone offering. This means that things like trial periods, and delivery will all happen through Substack - and we are gradually phasing out the PDF report format for Ozone to eliminate a duplicate email from us for each report. As we’ve continued to expand our Economic Advisory practice, there’s a greater need for customization on our part in reports & more - and I am making this shift to simplify things on our end, and yours. The portal directly on the website will remain available, and Ozone Pro members remain able to access the Ozone Pro dashboard. As we finalize 2026 plans, there will be some additional changes and adjustments to our Macro Research offerings.

This year, we are going to be placing a much higher emphasis on the portfolio strategy & equity research component - under the Ozone umbrella. With all of our data, we’re turning it into real-time strategy, and setting up our runway for success into things like Trident & our Economic Advisory Engagements. With our innovation-focused approach, things are going to be constantly shifting and improving for you all, and I wanted to share these early-year updates.

To experience MacroEdge Ozone for 7 days, through Substack, you can subscribe below:

More Data Delays

Data delays continue out of this Administration - with January and February PCE/income data now delayed another month… (yes, data in the future).

This is part of a broadening trend we’re seeing with government data, and if government funding lapses again for even a short period of time - this year is going to get very messy, and the data will get even more questionable.

Yields Shut Down Rate Cuts - No Rate Cuts for January &... Beyond?

Yields have shut down rate cuts for the time being - and we’ve been beating the drum here on the fact that yields never broke lower than key levels needed for further cuts. The 2-year yield has moved higher in recent days, and the deflationistas have continued to beat the ‘wrong’ drum - cherry picking things like WTI over food & insurance to paint a narrative of falling prices… but where though?

US02Y:

US10Y:

As I’ve said for several months now - there’s absolutely zero reason for rate cuts given the current environment - inflation is too high, and the labor market is not slowing down fast enough. We’ve seen upticks in activity in cyclical sectors like trucking & housing, and cutting rates further would be idiotic (as are things like the $200bn MBS purchase - which is like shooting a fire extinguisher on a forest fire)... that seems to be how we continue to conduct business from a fiscal & monetary standpoint - however, and it’s been that way for a decade+ now.

Given the spat between the Trump Administration & Powell, and with the looming appointment announcement of the new Fed chair - there’s also very little reason for the Fed to be supportive of the Administration for the next few months.

No… inflation though?

That’s pretty damn hard to argue.

Japanese Situation

The Japanese situation remains fluid with a potential vote in the coming days to call a snap election.

The Yen is near 1990 lows against the USD - and the carry trade is arguably the largest we’ve seen now in the last 5 years:

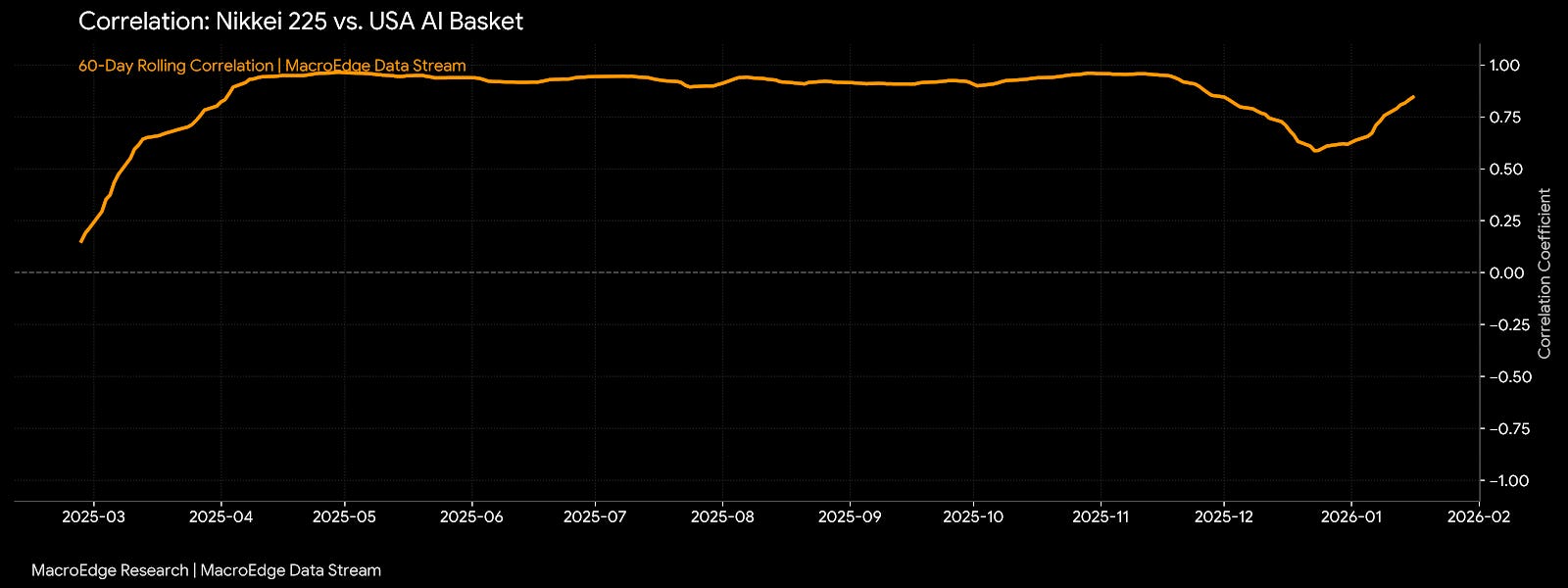

Weak Asian currencies are supporting bubbles in Korea & Japan - which are conjoined with massive retail leverage and speculation. Those are also supporting the AI trade in the US:

Rolling correlation of the above relationship:

(continued below - Japanese Yield Curve, Tech Stocks in Limbo, Portfolio Strategy Update & New Global Arms Race Discussion with Six, Inflation Lies, and more)

subscribe to Ozone:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.