Midweek Macro Note: Portfolio Strategy Update, Real Estate Review, A Look at Liquor & Wine, Energy - Time to Shine?

In this Midweek Macro Note - Six provides the latest portfolio strategy update, we discuss the latest developments in real estate (particularly, single-family), talk about the liquor industry, & more.

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers and Community,

I hope you are having a fantastic week. I have a few days aside from the very intense travel schedule I embarked on at the beginning of the year - though it will resume early next week as we begin to expand both our Macro Research & Transform solutions to broader horizons. It’s incredible the opportunity for us out there right now, and we are going to continue to capitalize on it as we expand.

This week has gone by relatively quickly due to the shortened week and the Monday holiday. There hasn’t been much in the way of major developments this week - though this evening we did see Nvidia reduce its investment into OpenAI from $100 billion to $30 billion, based on a report from FT. This is the tip of the iceberg for a space that has many howitzers lined up and pointed at it waiting to fire… While some might say I am being jaded on the whole capex disaster, I think looms (which will result in eventual bailouts of some of the operators), creative financing like we saw today announced between AMD and Crusoe should cause us to pause and pay even more attention to developments in the space. To this day, even with all the hype and share outperformance, very few - especially those on CNBC - are offering valid explanations on any sort of moat to profitability for the LLM companies. On top of that, as we’ve talked about now for the better part of half of the year - community opposition to data centers is now shifting into *surge* mode as it becomes a hot political issue locally and at the state level… even at the national level - bills are being introduced - though we’re not likely to see much in the way of progress with the Trump Administration without a vote that can land 60 votes in the Senate.

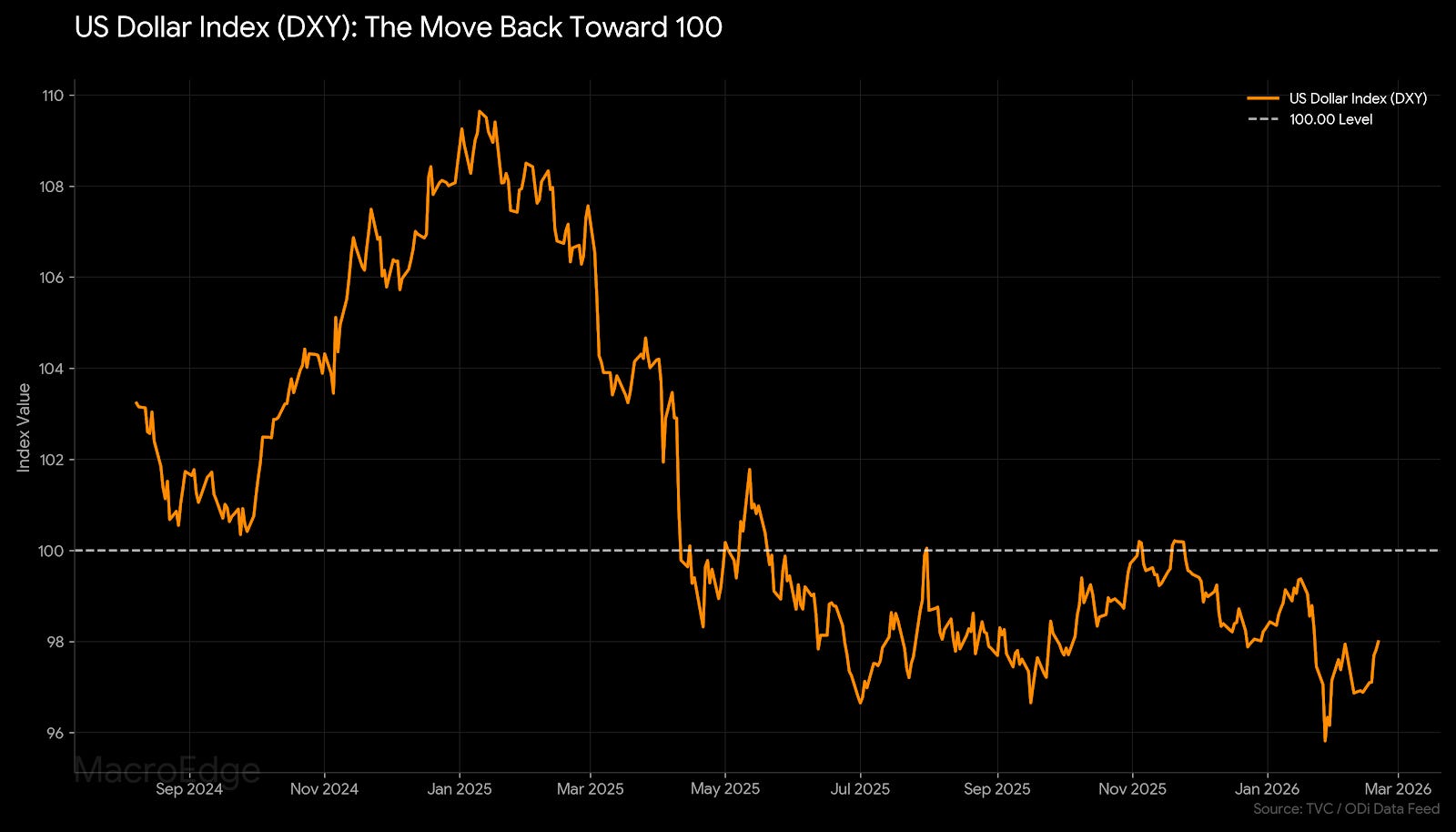

On the bond market & dollar front - the dollar index has popped back toward the 100 level, while yields (particularly the 10Y) has stabilized for the time being above 4%:

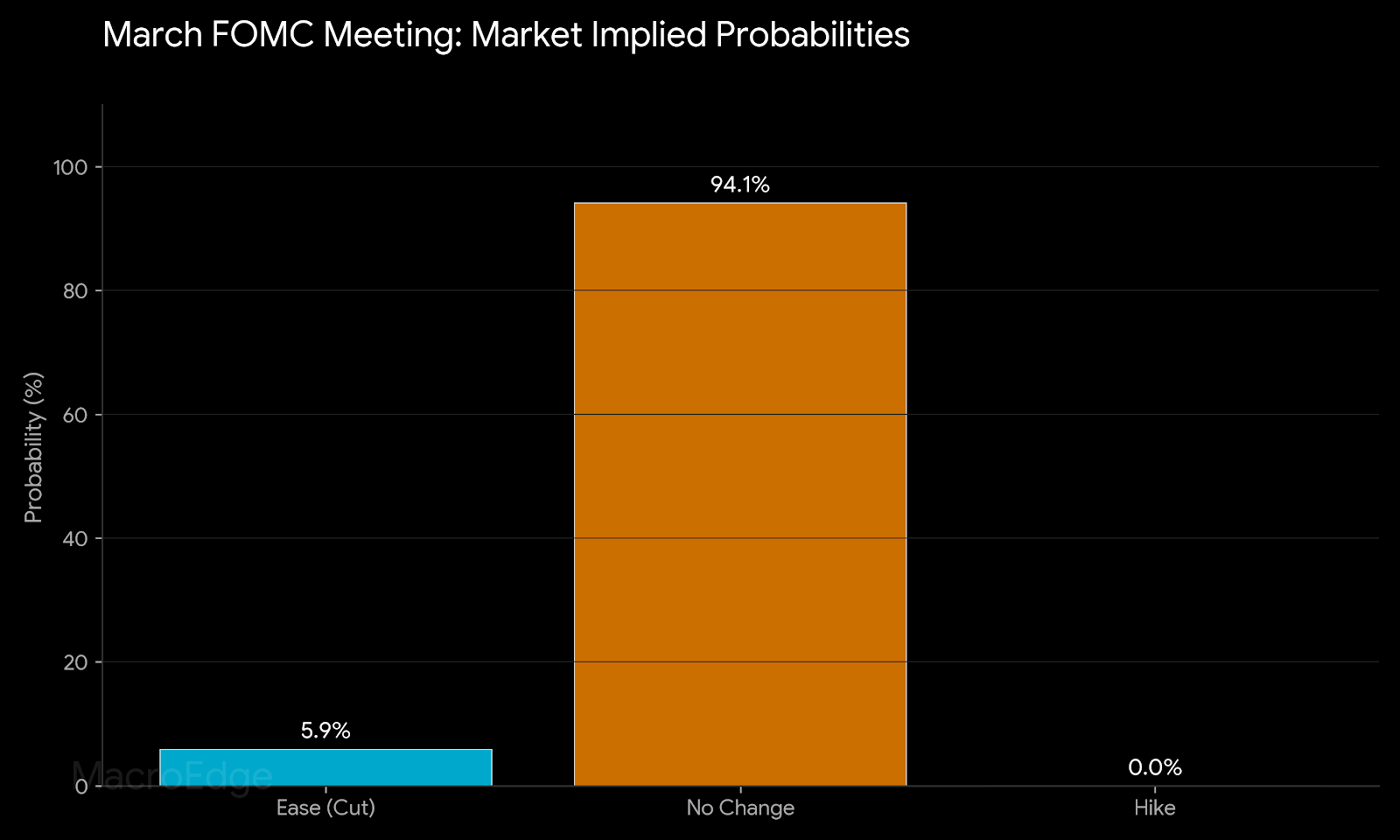

The next move in the bond market is likely to be directionally very important - as we wait to see if we can finally shift from the rangebound mode to something considerably lower (for bonds) or higher if the macro environment weakens and supports such price action. From a March FOMC standpoint, it is looking very unlikely that there are any rate adjustments made next month:

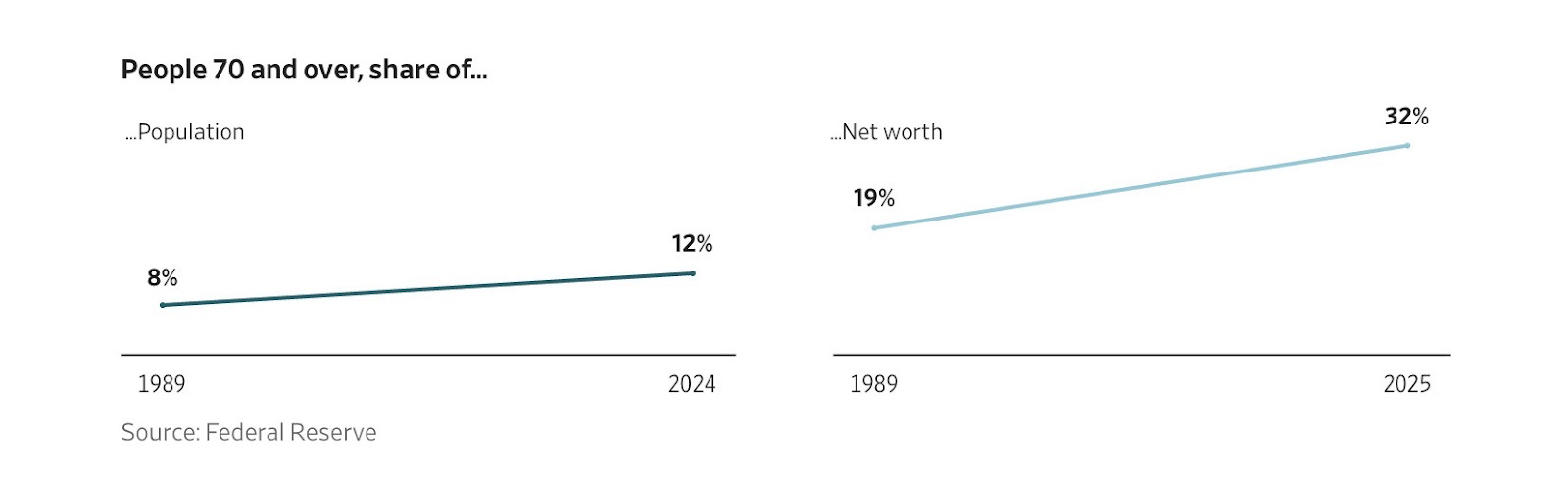

Chart of the report… the widening wealth gap is largely an age-driven gap, and that trend has accelerated steeply since the pandemic days:

Thank you to this fantastic reader comment this morning and shoutout - it really started my day off on a very positive note:

In the meantime, enjoy all of the coverage & data below - and let’s see what we learn about the aliens and UFOs tomorrow as those files start getting released…

Real Estate Review - When in Doubt, Blame the Snowmen

(Continued below: our real estate review - single-family & CRE, a look at liquor and spirits, energy - time to shine?, next reports in the queue, MacroEdge Portfolio Strategy Update & Performance Review).

To get all of our data, reports, research, and much more - join Ozone below:

The real estate market (from an activity standpoint) across the board continues to be very weak in transaction volume, architectural billings, in CRE, and more. While prices are frequently cited as a reason to be excited about the state of things, I continue to believe that real estate in some markets is in a pretty precarious state - and though policymakers refuse to let price discovery happen in single family homes (since that’s where the bulk of Americans have their net worth and wealth derived from) - can kicking can’t last for an indefinite period of time.

Things remain very soft in real estate land (especially CRE & single-family) - and it was noted today by an analyst that I follow that things are largely shaping up to be like 2025 was. I also noted myself today that housing has morphed into a bizarre swap meet (at least for the time being) for the asset/capital class, while volumes remain extremely suppressed in the sub-$1 million segment. The $1mm+ segment remains extremely robust - especially in niche markets like Park City - and as long as asset prices, particularly, equities, remain sky-high, things should be okay in that particular segment. We do have a fade-out occurring now of the ultra-low rate buyers, and by the end of the year, the market will be split between those with >5% versus those with lower rates who are stuck in their pandemic-era purchases. There’s also some movement still occurring for things like tax flight - though a lot of this is occurring at the upper echelon of the income band - especially for business owners exiting states like California.

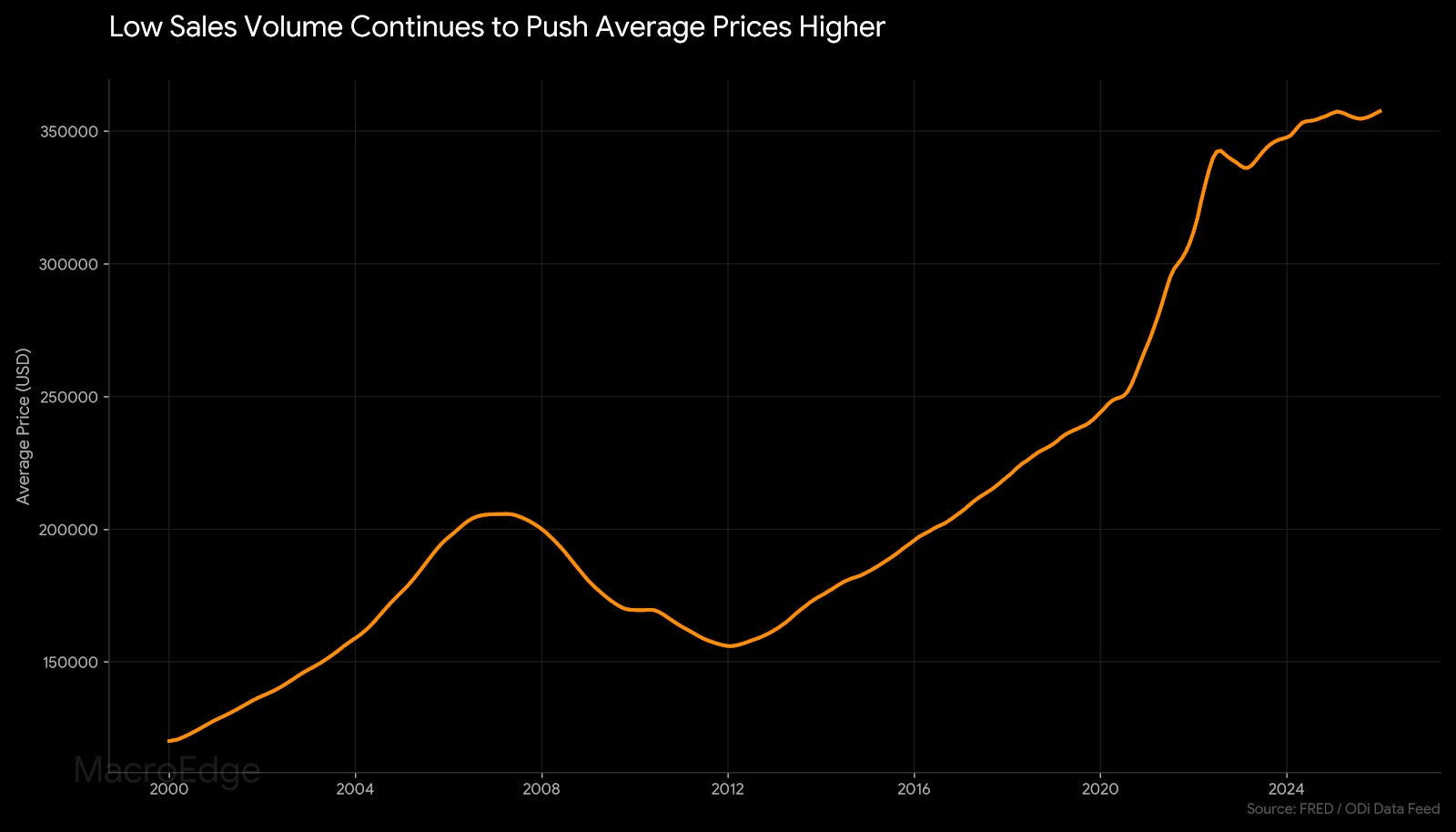

The low transaction volumes nationwide are continuing to push the average price measures (like the ZHVI) higher:

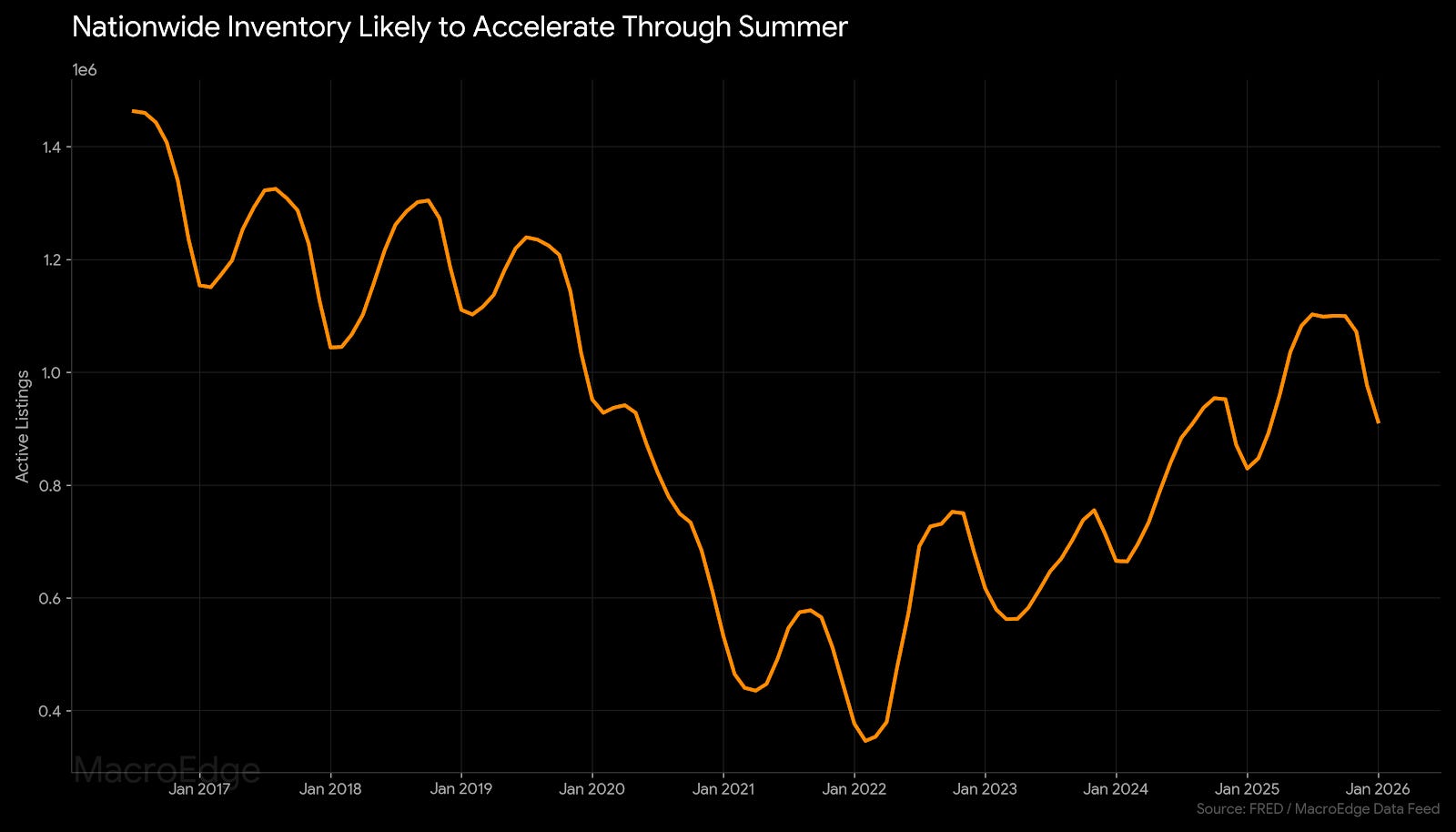

Nationally, we’re likely going to see inventory accelerate now as it usually does through the mid-summer, though with the weird market conditions - sellers haven’t been in a huge rush to actually pull the plug on their home ownership if they don’t need to.

It’s going to take a higher rate of mortgage delinquencies, higher inventory, and more forced sellers to meaningfully impact price on a national basis - at least in the next 18-24 months. That may happen, though the Administration is very focused on housing, and the President himself noted that he would love to keep prices up. With so much of the US economy tied to the retiree and asset class that owns real estate and equities, the entire situation is a vulnerable house of cards, though one that is protected with great firepower from policymakers in the short-term.

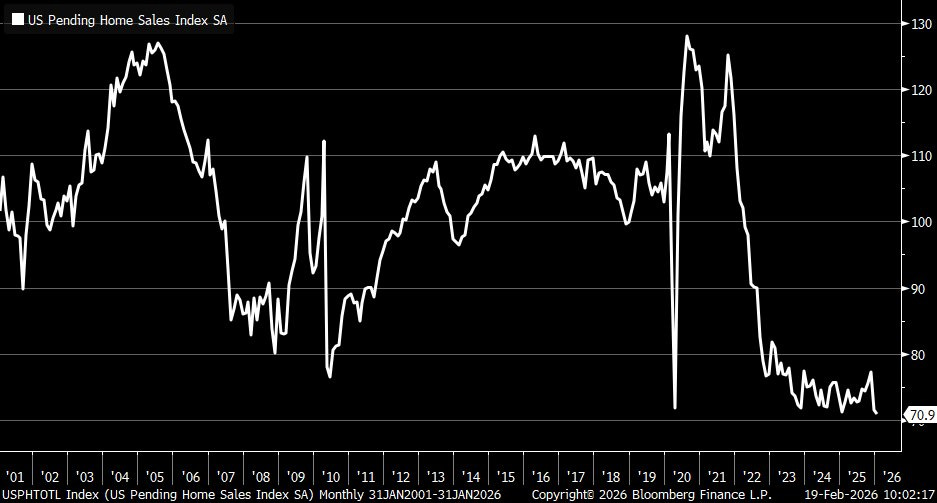

On the transaction volume front, things are very abysmal. The MBA Mortgage Purchase Index (which tracks new mortgages) and the NAR Pending Home Sales Index, are in very soft spots. The Pending Home Sales Index hit an all-time low reading today.

For the Pending Home Sales Index (a major yikes - hitting the all-time low reading today) ->

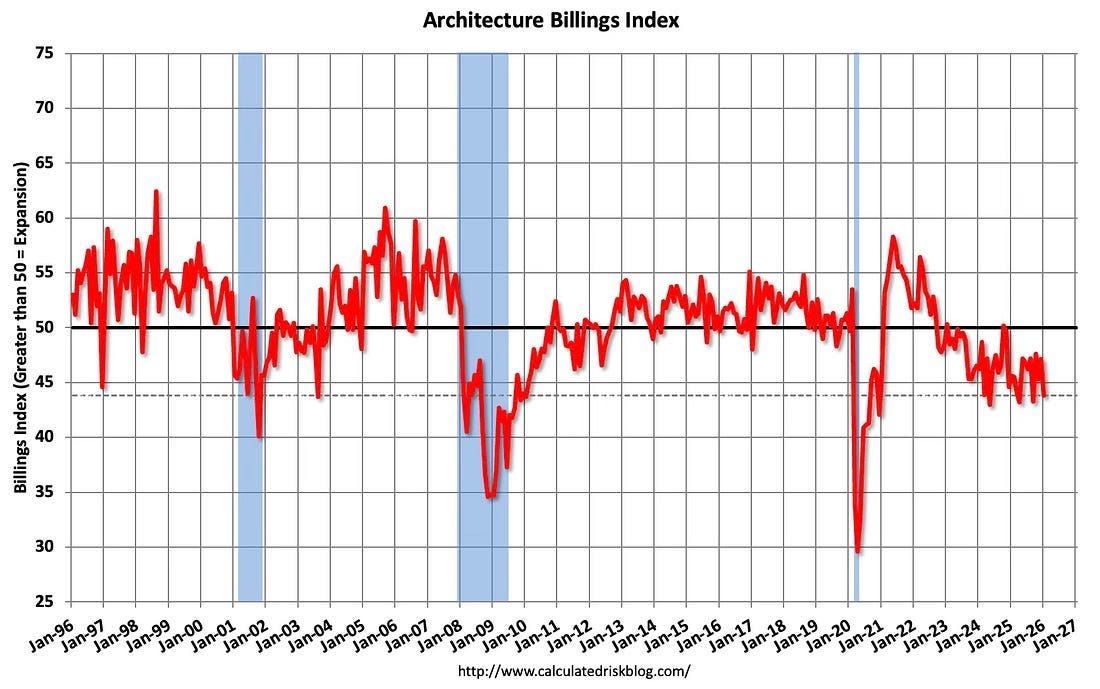

AIA Billings Index:

While these very poor readings haven’t bled into the averages (especially from a home price standpoint), and I am very cautious about buying into the whole rent deflation narrative - because many of those individuals are overweighting things like concessions, ex-fees, etc.

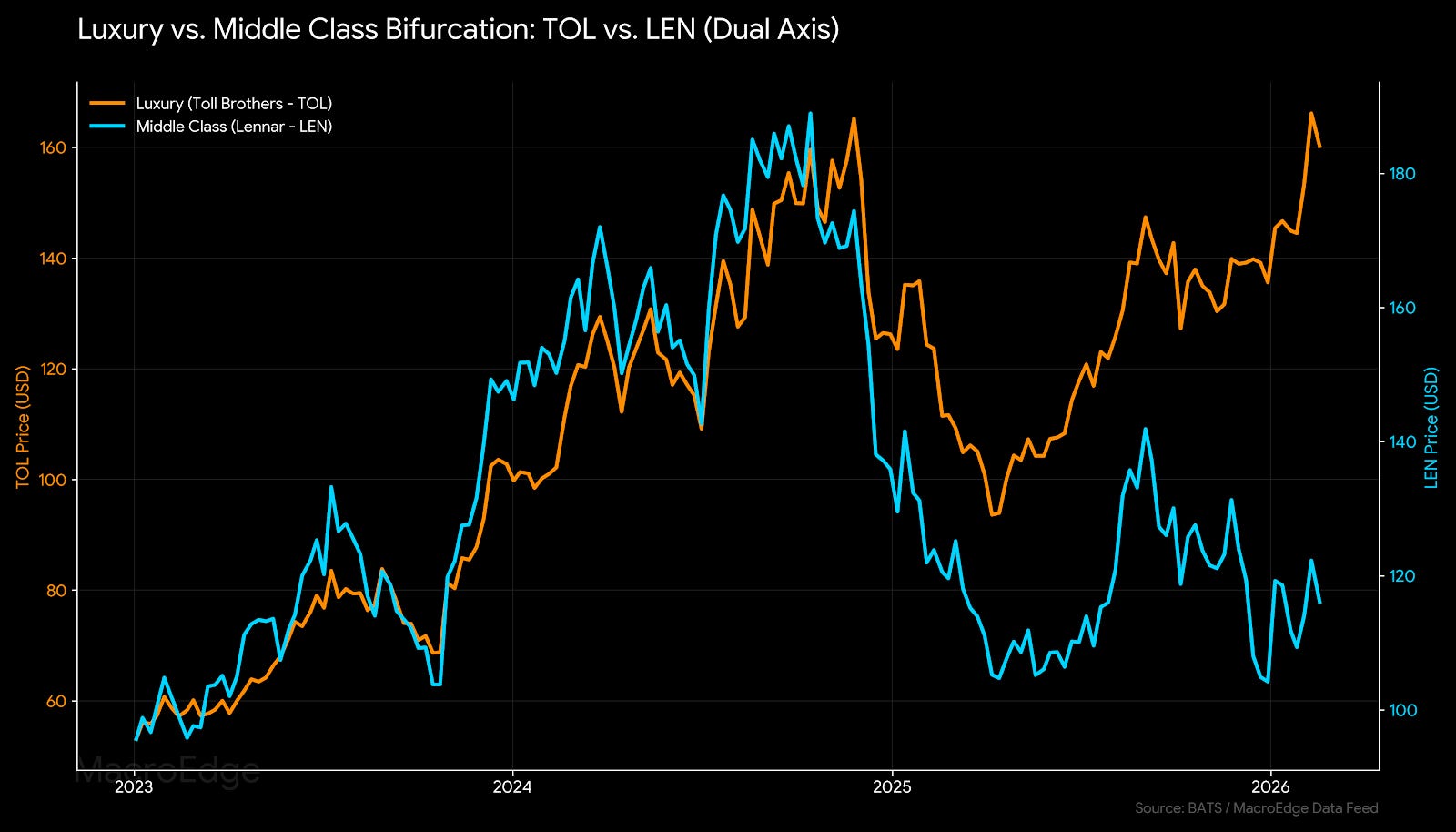

For homebuilding equities - what has this meant? Higher on the aggregate, though the story again has been a split one of luxury v middle class, as have many other stories been in our ‘i-shaped’ economy of late.

I expect that with the Administration’s focus of late on homebuilders (though not affordability), we start to see performance here sour if the cyclicals once again face another bout of softening. Though tech has entered this long mid-air stall, cyclicals caught a bid to start the year - though with rate cuts being shifted later, I see little reason for homebuilders to be outperformers based on actual market conditions.

(i-shaped economy example - widening performance between luxury and middle-class builders).

A Look at Liquor and Wine

Back in reports in early 2024 - we were frequently discussing the problems facing the liquor industry.

A lot of the leading indicators and data pointed toward very challenging times ahead for the liquor and spirits industry - and many of those issues have materialized into very poor share price performance across the board.

With rising use of marijuana - especially among the 20-34 crowd - and more frequent marijuana purchasing, chewing into alcohol budgets and demand, many of these trends have started to impact liquor companies much more broadly. Today in California, Gallo, the largest wine producer, announced a major facility closure in Napa. This trend has not been limited to wine, as bourbon and whiskey producers, tequila makers, and more have struggled tremendously.

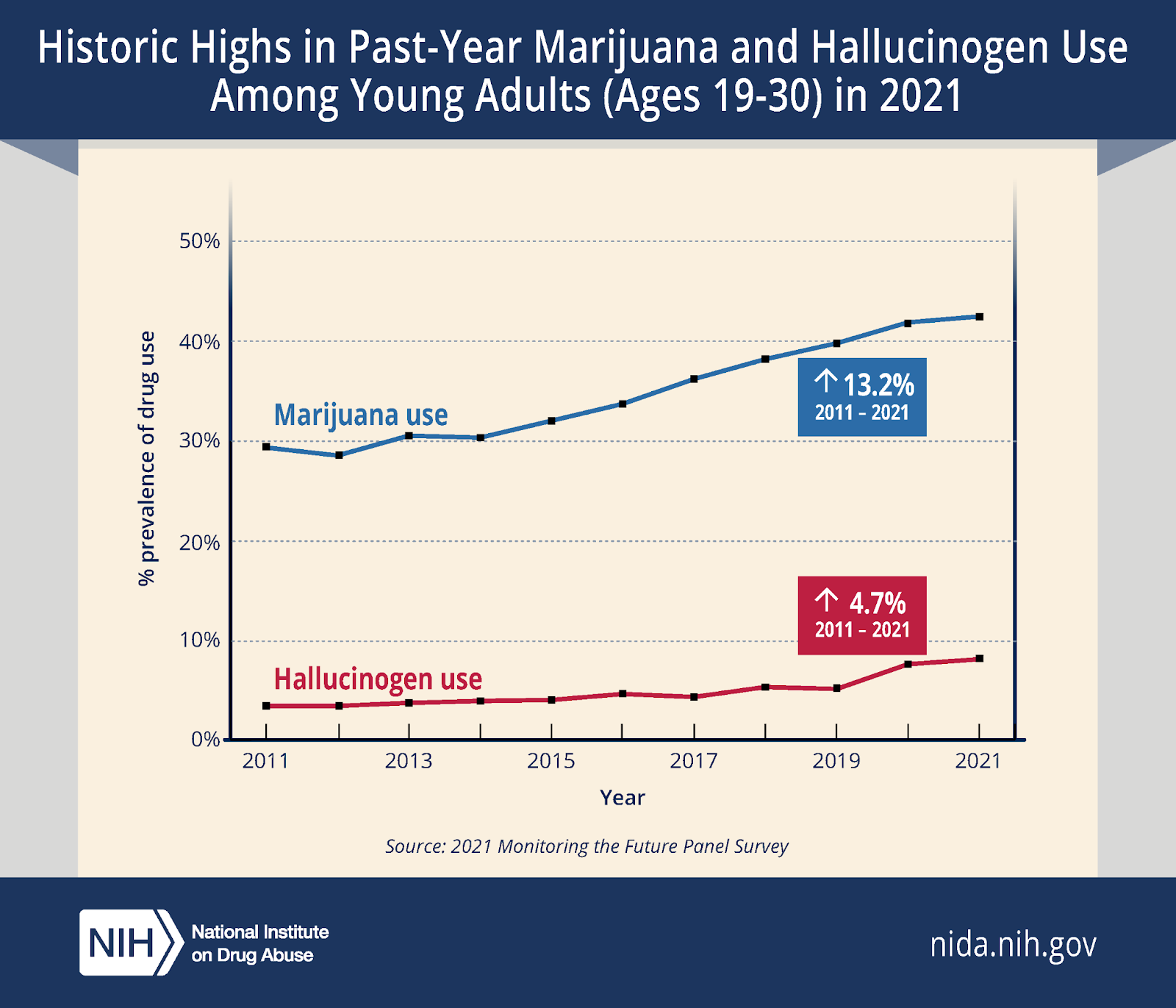

A large driver of that is the shift in young consumers (20-34 in particular) to marijuana:

(note that this is only through 2021 - and is now around 20%)

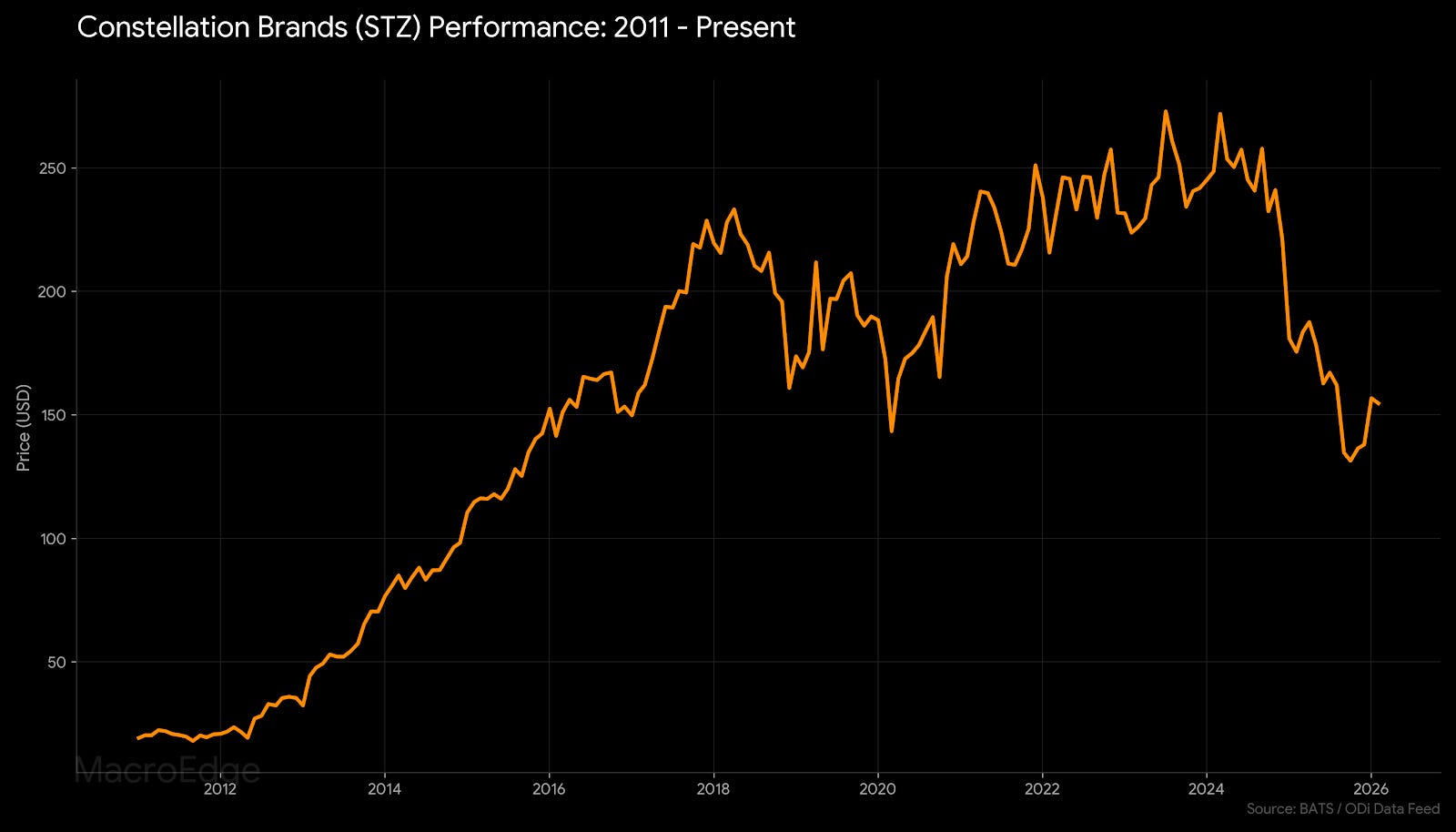

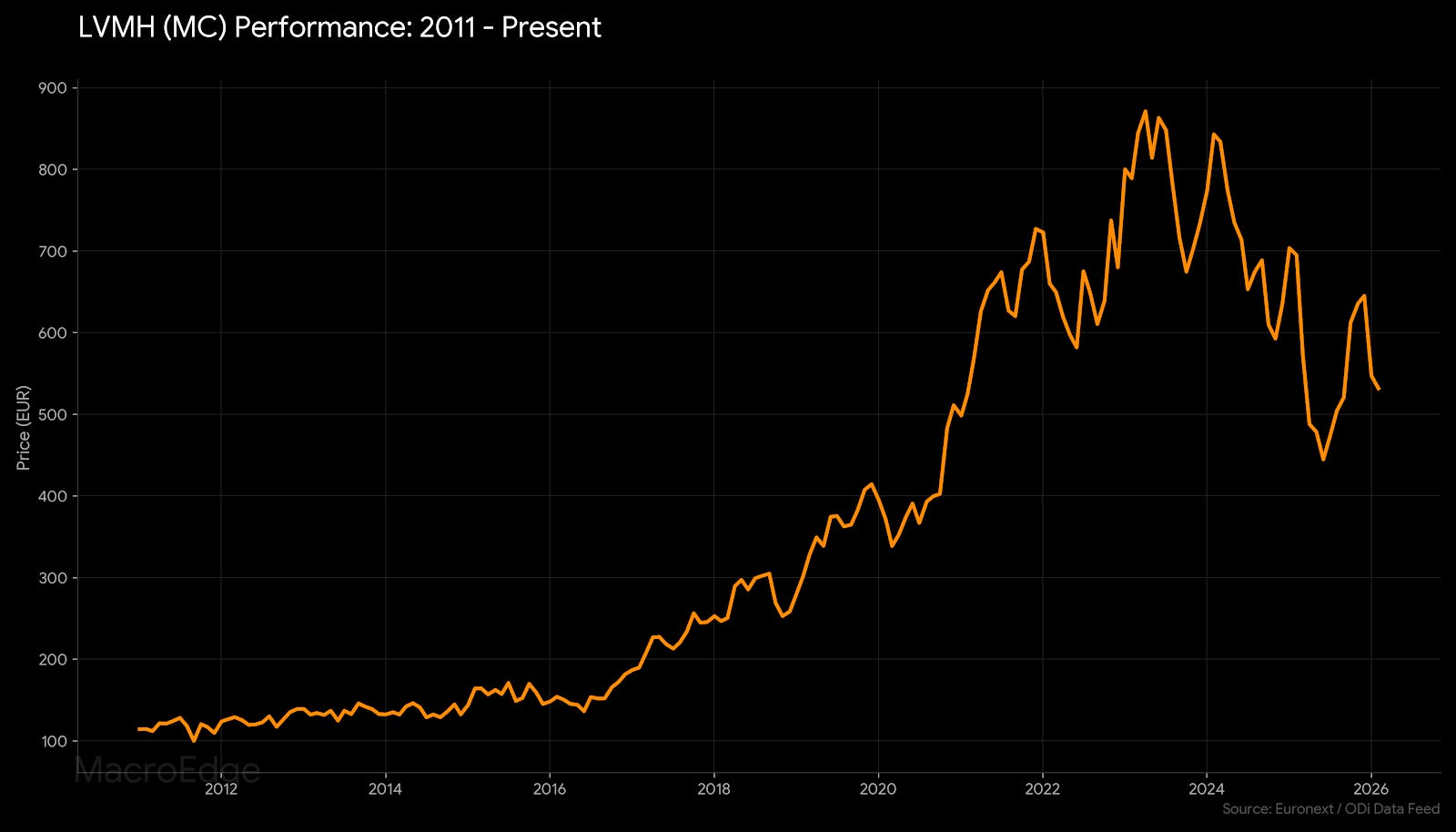

STZ (Constellation Brands), Diageo, and LVMH have all followed very similar trends:

(DEO)

(LVMH)

With closures accelerating and demand continuing to wane - especially in the more youthful category - there are undoubtedly many board meetings & marketing meetings happening right now trying to figure out how to reverse these trends in demand. With tobacco companies finding their ‘youthful’ pivot with the evolution of pouches and vapes, I do think the liquor industry will figure out some kind of pivot to make themselves more attractive again - even if it’s with a more niche audience. When that moment does happen - and if a brand gets their act together here in the next several months - it could present a unique opportunity to purchase one of many of these very beaten down equities - though for the time being judging based on how poorly GenZ is doing in the labor market, socially, and in family formation figures - I am leaving it alone for the time being. When the mainstream media & Substackers start blasting the space and calling for the end of it all - especially for an industry that’s been around so long - that’s when I will grab my shopping bags and pick up a few bottles (of shares)...

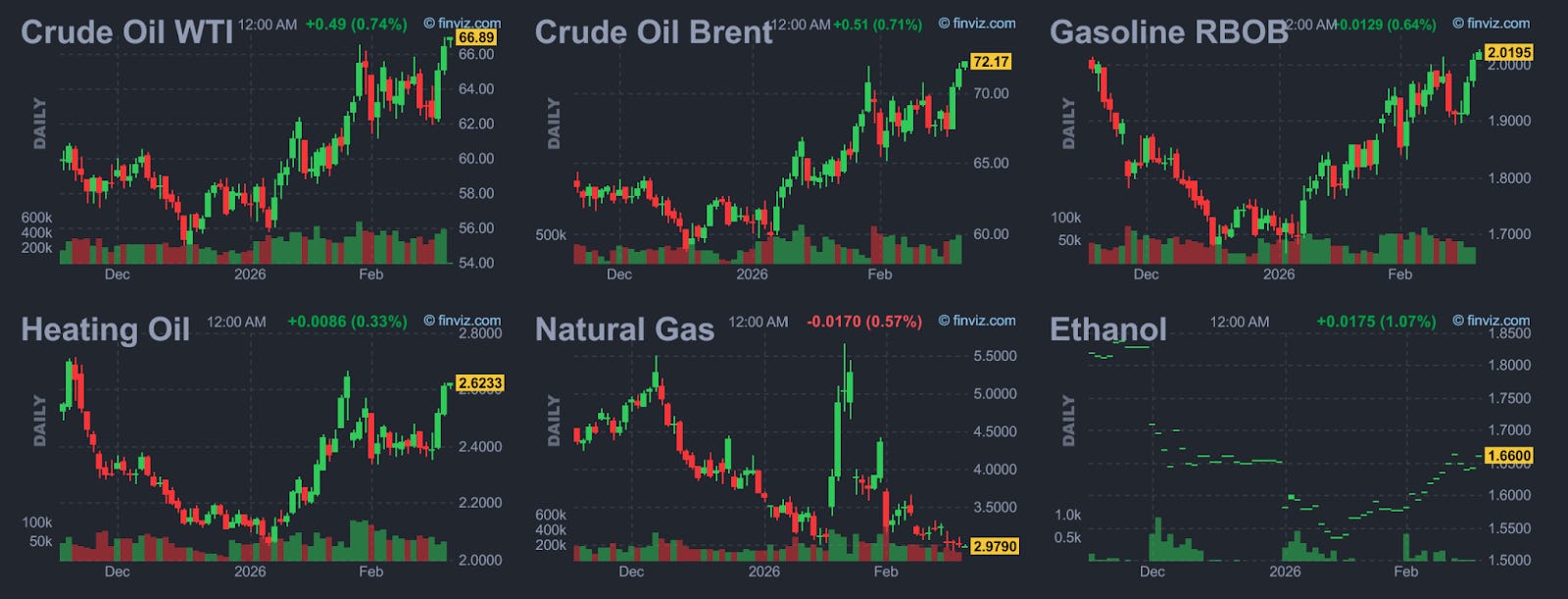

Energy - Time to Shine?

The energy outperformance today was quite notable again, and across the board - things in the space look very constructive. Oil (CL) is pushing above major key moving averages again - and production continues to move lower as rig counts drop. While the geopolitical factor is a component (it usually always has some role in the major price spikes), I think there is more than just a Hormuz risk being priced here as production falls. With OPEC+ and particularly Saudi needing prices higher, they could start to move to tighten the market, and if the President loses the political mandate from the fall onward, the opportunity could accelerate here further (and rapidly).

In the Redeye Macro Note - we’re going to lay the foundation for further discussion on opportunity in the space from an equity perspective - and Six is going to add further color to the macro data as to why this might make sense.

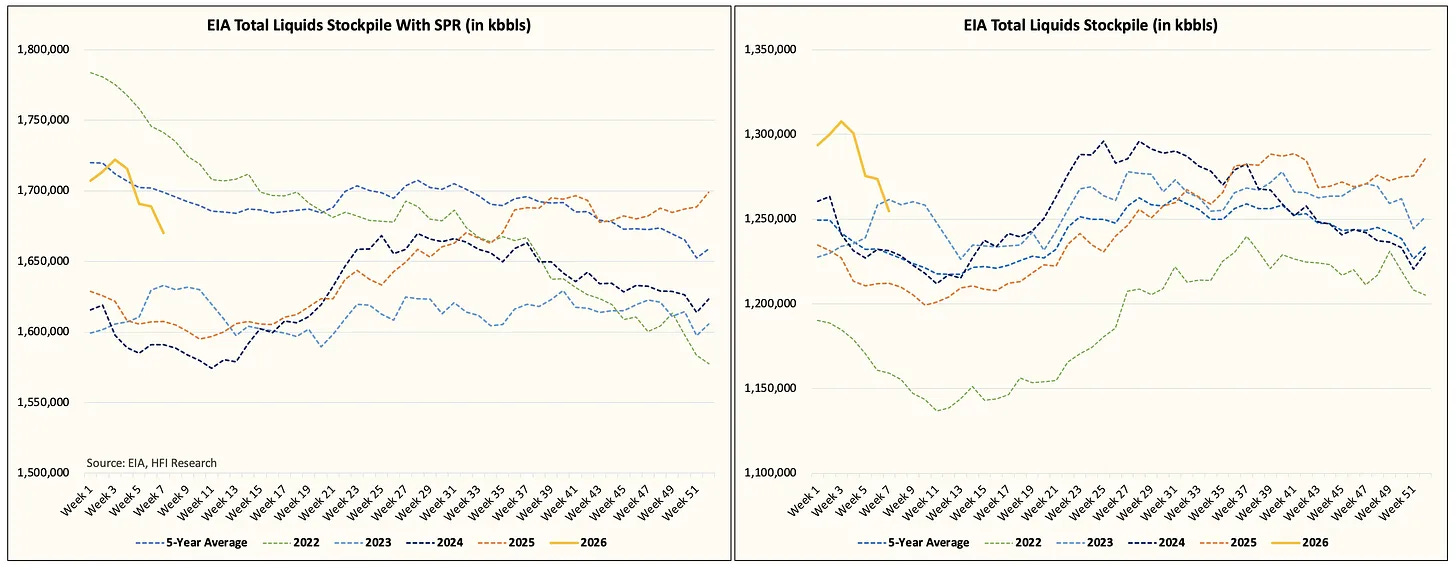

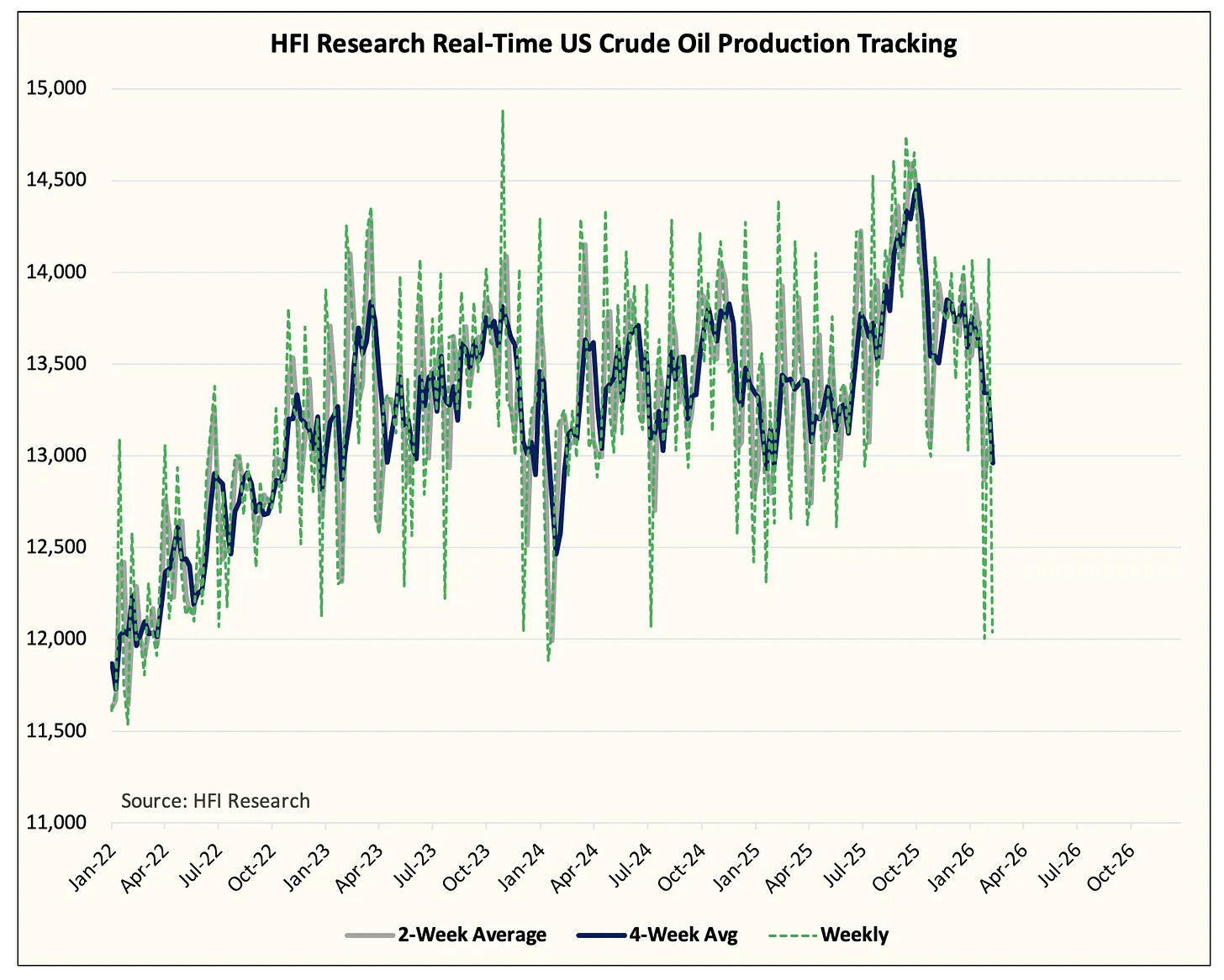

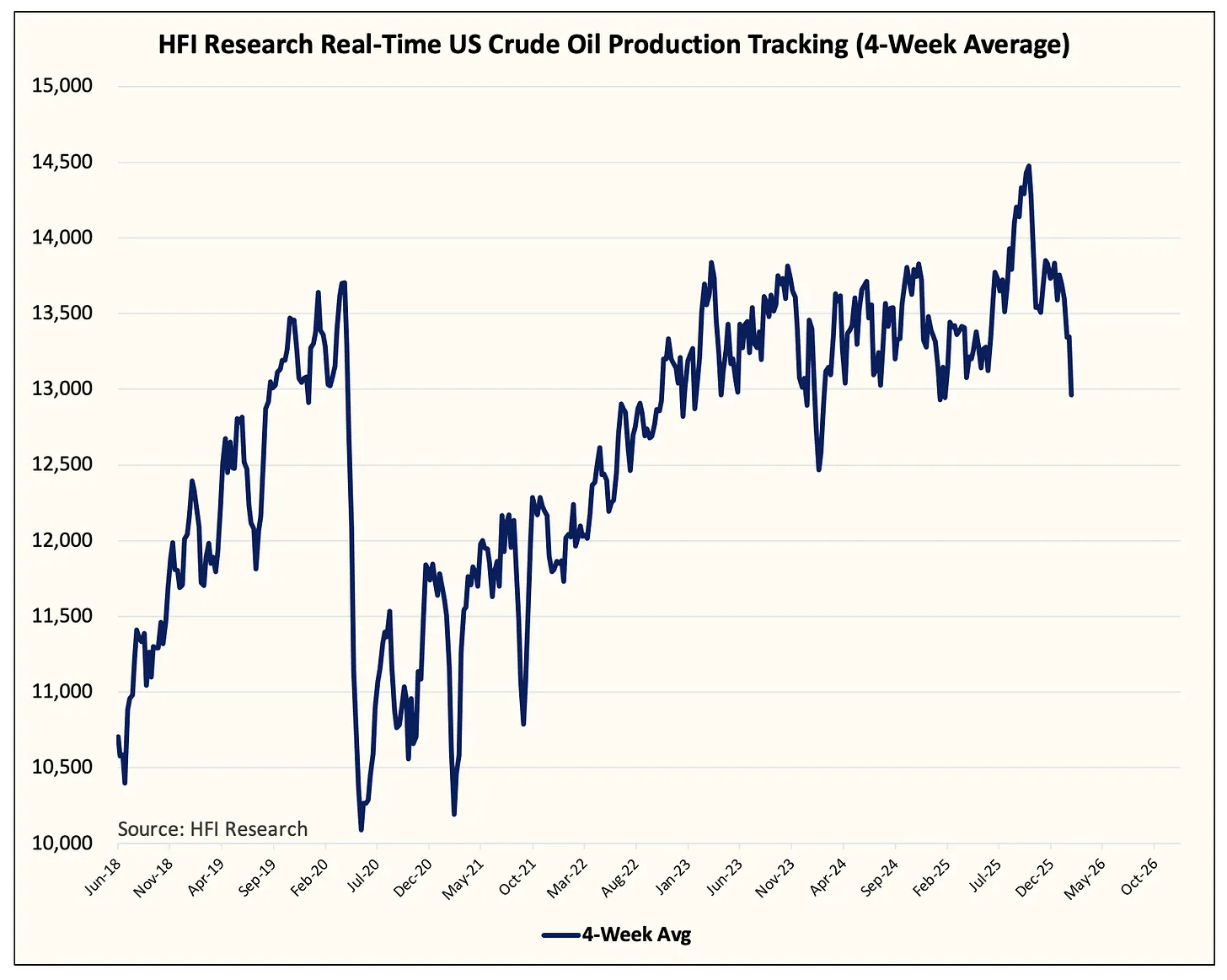

Data from HFI Research below:

(EIA Liquids Stockpile)

(Implied Crude Production is seeing a steep drop)

The 4WK MA:

Which is translating to bullish movements across the board in oil and gas prices:

I think there could be huge upside in a lot of the smaller E&P plays here if prices continue to advance higher - and names like XOM have already seen huge moves higher on things like the Venezuela events & more.

Next Reports in the Queue:

The next comprehensive data center and AI report will be available at the end of the month - with a special guest author and longtime MacroEdge friend adding color to the fantastic data we are tracking.

Redeye Macro Note (Saturday AM: Trident I Update Part 2, Energy Opportunity, Distribution Continues, Technical Deep Dive for February, Project South Africa - a Rant)

Weekly Macro Note (Energy Opportunities Part 3, Monthly Crypto Report, and More)

I hope you all have a great last day of your week - and stay tuned for the Redeye Macro Note on Saturday morning - there’s a lot to cover - and I look forward to publishing our next AI/data center report at the end of the month, too.

MacroEdge Portfolio Strategy Update - February 19, 2026 (@SixFinance, Head of Research)

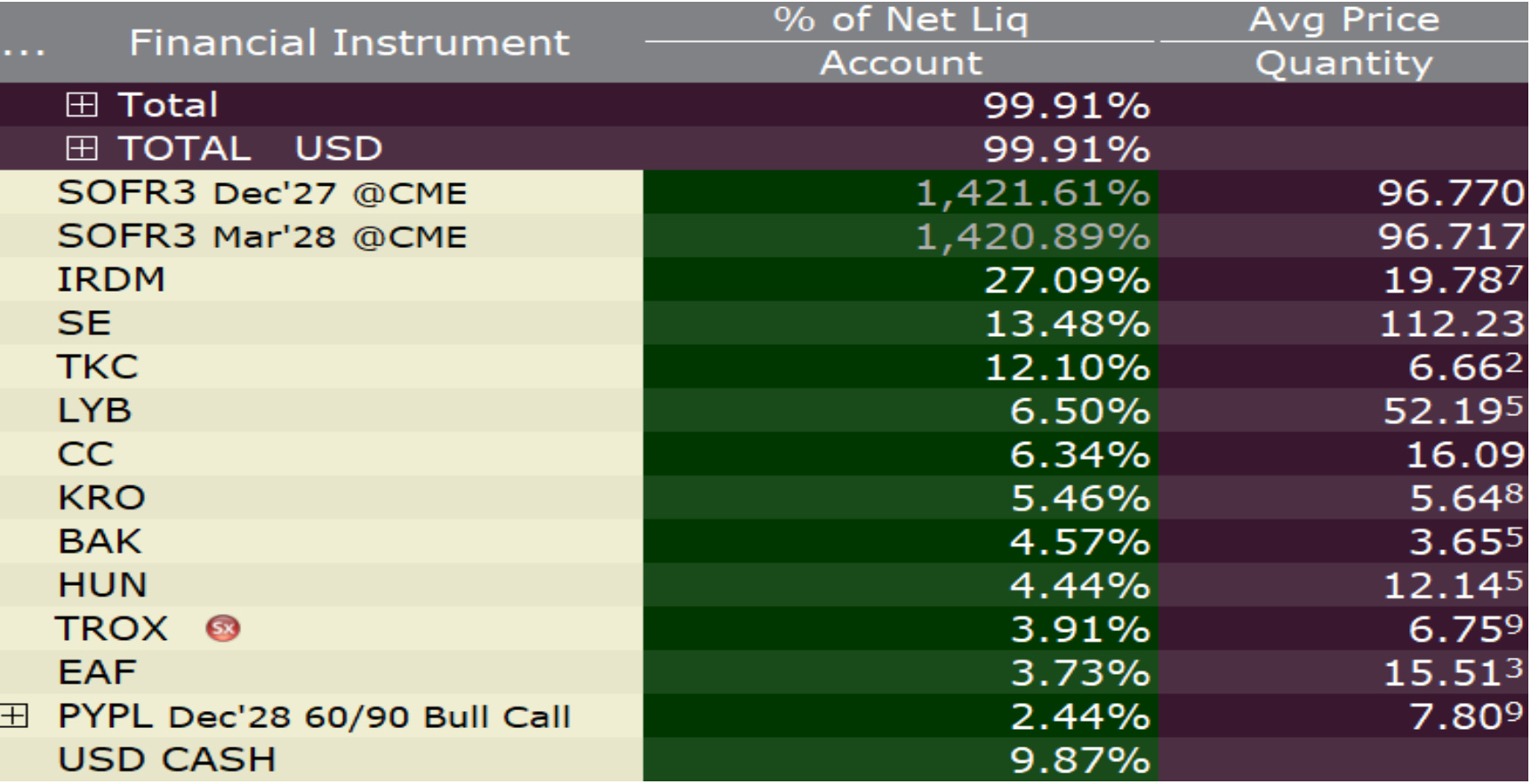

The economic data flowing in continues to show the early stages of a potential inflection in the manufacturing sector. Earnings season has been, plainly put, a disaster for the basket that I put on to capture what I believe to be asymmetric upside exposure to an early-stage ‘Bessent Boom’ in US domestic manufacturing. While the Q4 numbers are uninspiring for the majority of these names (CC, HUN, LYB, KRO, TROX, EAF, BAK), and in EAF’s case a total cluster, the backwards-looking nature of these numbers has little influence on my forward outlook for the group, for which I see macro drivers aligning.

I have added SE to the portfolio. Aside from merely sporting a phenomenal existing growth outlook while being nearly 50% off its recent highs, its primary growth market is turning around. Brazil was once a cash furnace for Sea LTD as they moved to establish a competitive market position, adding to the downward stock price spiral from their COVID era all-time highs. Since the euphoric highs, revenue has doubled, and margins have turned positive and are continuing to improve.

In Brazil, what was once a deep loss market has now transformed into a profitable market, and next month fee hikes will be initiated on their Brazilian e-commerce platform Shopee, which will bring their net profit per order from 10 cents to an estimated 15 cents as they gain pricing power in the country in the number 2 spot trailing MercadoLibre. I am very bullish on Brazil; their equity market is roaring. Additionally, SE’s largest market, Indonesia (~33% of revenues), has just tonight signed a trade deal with the United States.

Where we move from here in commodities will set the stage for how to think about risk on/risk off sentiment in the markets. Recent memory has seared the “debasement trade” into the minds of participants, and whether BCOM consolidates into something of a cup and handle, or has made a lower high will be an important input into risk behavior, especially driving export-heavy EMs.

Wheat futures look quite constructive here despite global oversupply. ~500 has acted as the low end of the range for the past couple of years now, and the cold front in January may act as a tailwind to prices, despite early projections that the crop was largely shielded by the snowstorm. Regardless, price is moving to the high end of its trading range and warrants a close eye here.

Tomorrow we have a large set of economic data. MoM and YoY Core PCE is forecast to accelerate higher, which may force me to reduce or drop my SOFR long altogether. Should Core PCE be soft, as CPI was, I see the rates trade having more room to run, as the market prepares itself for the new Fed Chair. I will also be watching for the manufacturing PMI to show further indication of manufacturing inflection.

For more details, please refer to our Terms and Conditions.