Midweek Macro Note: 'On the Ground' for Ag Part 1, FOMC Recap, Airline Bailouts?, Portfolio Strategy Update and Commentary

In this Midweek Macro Note - we kickoff our 'On the Ground' series for Ag (Part 1) with a brief discussion, highlight the airline industry begging for bailouts (once again), and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers & Community,

This evening, we’re going to kick things off with Part 1 of our ‘On the Ground’ series - beginning with the agricultural sector. A few weeks ago, I outlined how and why we were kicking off the ‘On the Ground’ series, which will act as a natural extension of much of the incredible data we have already been collecting directly from industry experts and participants. Prior to the beginning of the Iran War, we began a quasi version of this series in visiting the Permian Basin, and this same process of collecting, understanding, sharing, and executing will continue as the ‘On the Ground’ series is kicked off.

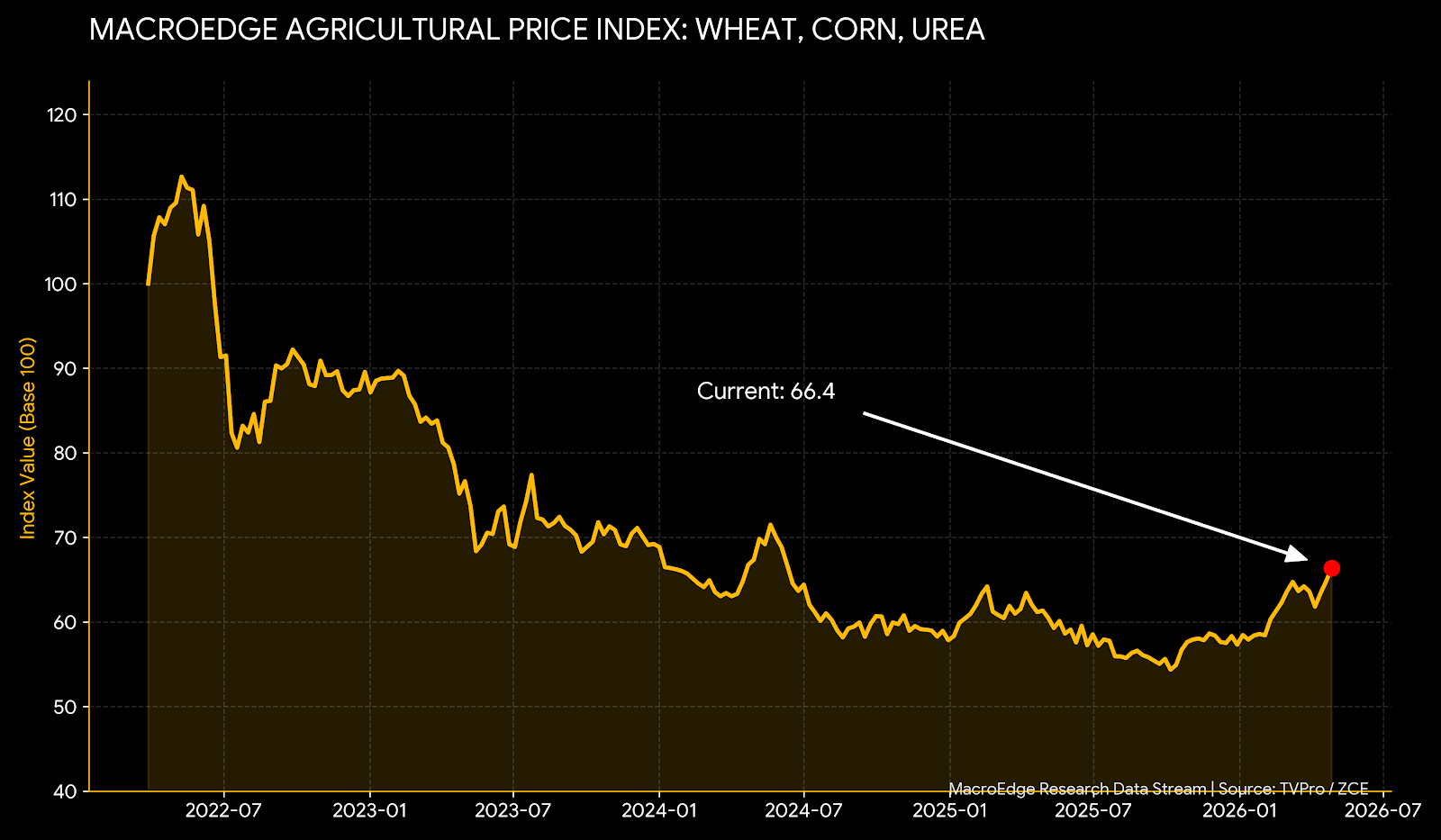

Next week, I will be visiting the Texas Panhandle with Six to begin the data collection process in the ag sector focus areas that we’ve identified - corn, wheat, and fertilizer. These inputs and staples are critical signals for both ag and broader economic price pressures more broadly - and price pressures here tend to lag other early-inflation warning signals. With fuel and petroleum-associated products soaring, there is still a massive disconnect between these staples and oil (yes, the same goes for natural gas right now)...

In the macro data picture for the week, the main trend continues to be one of increasing price pressures. With gas and diesel prices pushing to cycle highs (and now in many states - all-time highs) - price pressures are going to continue pushing higher. The deflationista camp continues to sing a loud tune about the looming price compression - but we are still not there yet. While I do believe that the cure to high prices is high prices, we are living in a weird macro-period where the government is now reliant on perpetually pumping assets higher to keep the music playing. This artificially stimulated demand from a small percentage of the population is keeping the party for now, and this will continue until there is the next ‘shock’ event that halts the equity meltup in its tracks. For now, the price environment is looking a lot like 2021 for the time being, and inflation is still not in a red flag area for asset prices (it may actually be a tailwind right now) being way above the 2% target, but not high enough to dent demand.

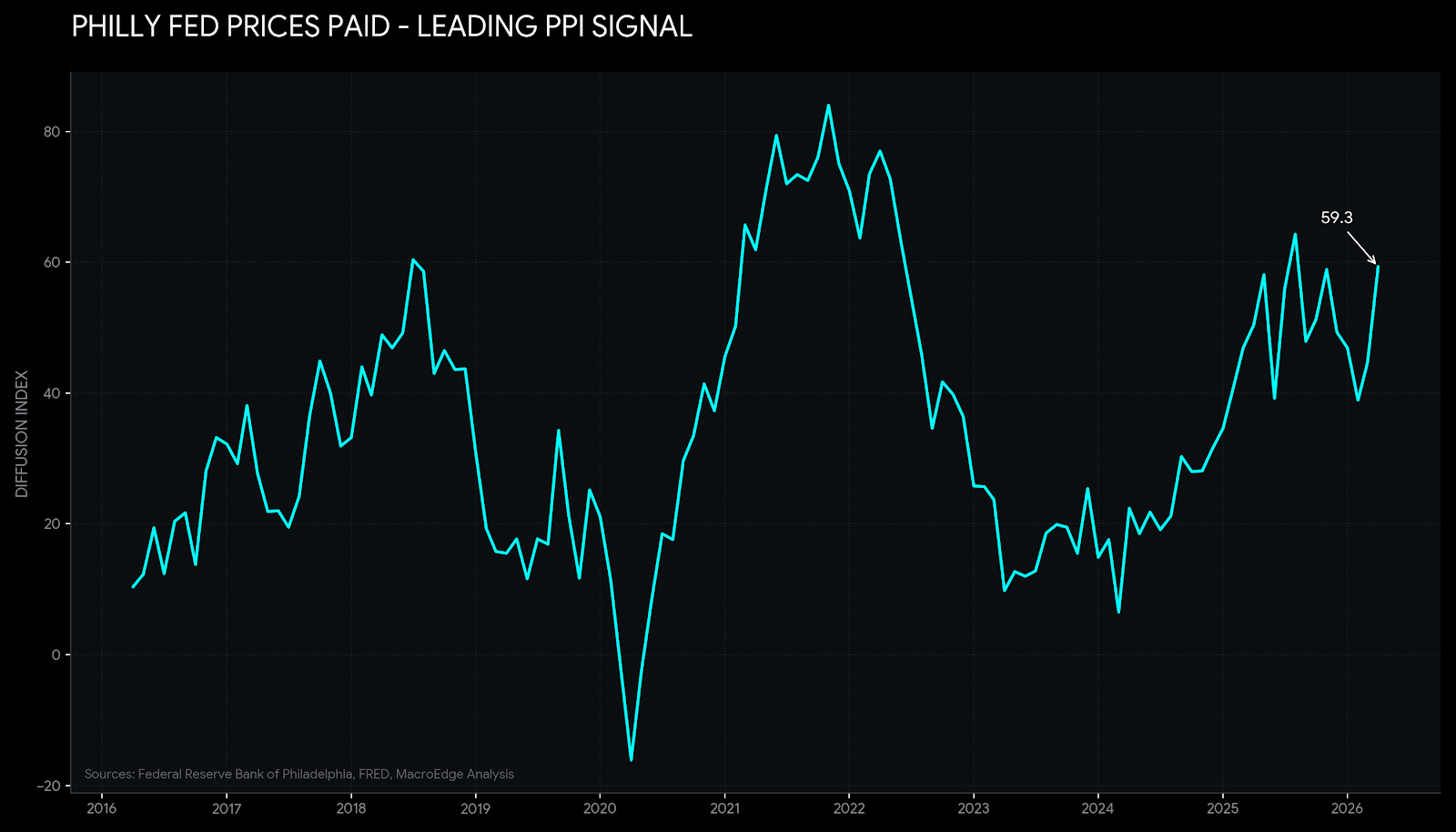

PPI/CPI usually have a 1-2q lag to the leading regional Fed signals:

Not yet a MacroEdge subscriber? Get Ozone below and access all of our research, data, portfolio strategy, and more:

On the Ground for Ag Part 1 - Time for Amarillo

Next week, we will be hitting the road to the Texas Panhandle for Part 1 of our ‘On the Ground series - focusing on corn, wheat, and fertilizer. There is a wide gap between the performance of these lagging critical food staples and input costs and where broader price pressures have trended. Our goal is to uncover if there is an opportunity here in the trade, highlight the risk of potential shortages, discuss the Strait of Hormuz impact, and unearth inflationary impulses directly from the operators. Beyond this, we’re also looking at things like crop yield, and figuring out how the farmers and operators feel about the situation, right from the ground-level.

A look at the equal weighting of wheat, corn, and urea, below:

FOMC Recap

As expected, we saw no rate cut in the FOMC meeting. While this was Powell’s final meeting as Chair, it appears he is going to stay on as a Fed Governor for some time, while an investigation into him & the Fed continues to play out. He’s likely waiting out a political regime change in the midterm environment to give him clearance to finally bail. While I could start a long rant about Powell and his abject failure (failure after failure) to control and keep price levels in check in the United States, it’s not worth giving him the light of day. The fact that we’ve propelled the Central Bank Chair to celebrity status is one of the more bizarre monetary phenomena in the modern era. Powell leaves with inflation running hot, an economy more reliant than ever on money printing, and asset bubble after asset bubble across the board. The ‘inflation is transitory’ line will live in infamy - and low headline unemployment with structural demographic deficits are not enough reason to give Powell a pass for his many failures as Fed chair. The list goes on and on, but I know that John will touch on some of these below.

Below, we outline some of the more important takeaways from the meeting:

Policy Stasis Amid Geopolitical Firestorm: The Committee voted to maintain the federal funds rate at 3.50%–3.75% for the third consecutive meeting. Chair Powell explicitly cited the “prolonged closure of the Strait of Hormuz” and the ongoing conflict in Iran as the primary drivers of extreme economic uncertainty, effectively freezing any plans for further rate cuts in the immediate term.

The “Quad-Dissent” Fracture: The meeting saw four dissenting votes, the highest total since 1992, signaling a total breakdown of committee consensus. While Governor Stephen Miran favored a 25bps cut to mitigate slowing GDP, three hawkish members (Hammack, Kashkari, and Logan) opposed the statement’s “easing bias,” warning that the 3.3% headline inflation spike in March may necessitate a return to rate hikes.

The “Back Side” Energy Mandate: During his final press conference, Powell stated that the oil-driven inflation shock (which saw Brent crude hit $130/bbl) has likely not peaked. He signaled that the Fed will remain in “wait-and-see” mode until they can identify the “back side” of the supply impairment, emphasizing that surging gas prices are now acting as a direct tax on disposable income and consumption.

Neutral Rate Re-Rating: Market participants noted a hawkish shift in the “longer-run” anchor, which moved upward to 3.0%. This indicates a collective belief among policymakers that the era of low-cost capital is over, as structural supply-side constraints and AI-driven productivity gains redefine the neutral rate in a high-intensity conflict environment.

The Warsh Transition: This was Jerome Powell’s final meeting as Chair (his tenure concludes May 15). Incoming Chair Kevin Warsh is expected to inherit an increasingly divided Fed and is already signaling a framework shift toward “price stability dominance” and new inflation metrics that account for the 13.5 MBPD supply deficit.

I continue to believe that the 2-year, and 10-year, and foreign yield curves are signaling a return to an inflationary regime:

The 2Y is now 50bp off of the lows, and even the long-end of the curve looks quite concerning:

(Continued below: FOMC Recap, Airline Bailouts, Agentic Awakening + Portfolio Strategy Update and Commentary - Six, Fed History - John)…

Not yet a MacroEdge Ozone subscriber? Get access below:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.